ryasick

Introduction

Thursday, April 3, was 'Liberation Day,' as President Trump called it.

Unfortunately, the only thing that got liberated that day was my portfolio from capital gains, as I had the worst day of my career, losing 6.2% in USD and close to 8.0% in EUR terms, as the dollar took a beating as well.

Then, on Friday, I lost even more.

While the pandemic had worse days in terms of percentage moves, the total dollar amount I lost broke many records. In fact, I lost more money than my entire net worth in early 2020 (times 3), which is quite something.

My portfolio is now down 7% year-to-date, slightly beating the S&P 500, which isn't half bad, and a sign that the growth-to-value rotation is still bearing fruit.

Leo Nelissen Portfolio Performance (Yahoo Finance)

However, I slept like a baby and had one of the best moods in a long time on Friday, as there are a few things to keep in mind:

- I knew exactly what I signed up for when I started investing. Moreover, when I went massively overweight in volatile landowners, I knew my portfolio's volatility would pick up. When the markets opened, I basically knew I would see double-digit declines in my largest two holdings.

- Market corrections are essential to build long-term wealth, as buying stocks at a discount allows us to improve our risk/reward, dividend income, and overall expected performance. As much as I dislike seeing steep declines in my net worth, the overwhelming majority of my current wealth is based on 'unusual' buying opportunities.

- I believe I know what the drivers of this sell-off are, which makes it easier to plan ahead.

I believe the third bullet point above is critical. So, before I give you my picks, let's discuss what's driving the market panic.

How Bad Is It?

"Treasury Yields Edge Below 4% as Tariffs Fuel Recession Fears."

The headline above was published by The Wall Street Journal on Friday. I am using it in this article, as it includes a few very important aspects.

For starters, it shows that tariff announcements have caused markets to believe we're about to see substantial economic weakness. This is confirmed by the horrendous price action of cyclical stocks like transportation companies.

The SPDR S&P Transportation ETF (XTN), for example, has lost a quarter of its value this year, as we can see below, with a big part of this decline coming from Wednesday's tariff announcement.

This weakness is based on fears that tariffs can be met by retaliation and slow down overall global trade. This makes sense, as tariffs make it less attractive to move goods across borders.

While this could result in economic re-shoring to the United States, it will be a slow process, as it takes multiple years to build a factory, and because the United States is unlikely to suddenly produce all of its goods domestically.

For example, cheap production of apparel, footwear, and electronics in Vietnam is unlikely to move to the U.S., as the United States does not have the low-cost workforce that many Asian nations have. Or to put it differently, we can assume America isn't suddenly a great place to produce sneakers.

On top of that, these tariffs are inflationary, as consumers will have to pay more for imported goods, at least for the time being.

Although I am not at all saying we are about to see stagflation, the expectations of slowing economic growth and potentially rising inflation are causing fear.

A global recession is more likely than not to happen this year, following the Trump administration's tariff broadside. That's the opinion of JPMorgan analysts, who raised their forecast to 60% Thursday, up from 40% before President Trump's announcement sent markets tumbling.

Analysts said retaliatory tariffs by other countries, weakening business sentiment in the U.S. and supply chain disruptions will make things worse. Jeep maker Stellantis has already halted production at its auto assembly factories in Mexico and Canada. - WSJ

So, why is President Trump doing this?

I did not predict this sell-off. However, I have discussed President Trump's need to make radical changes.

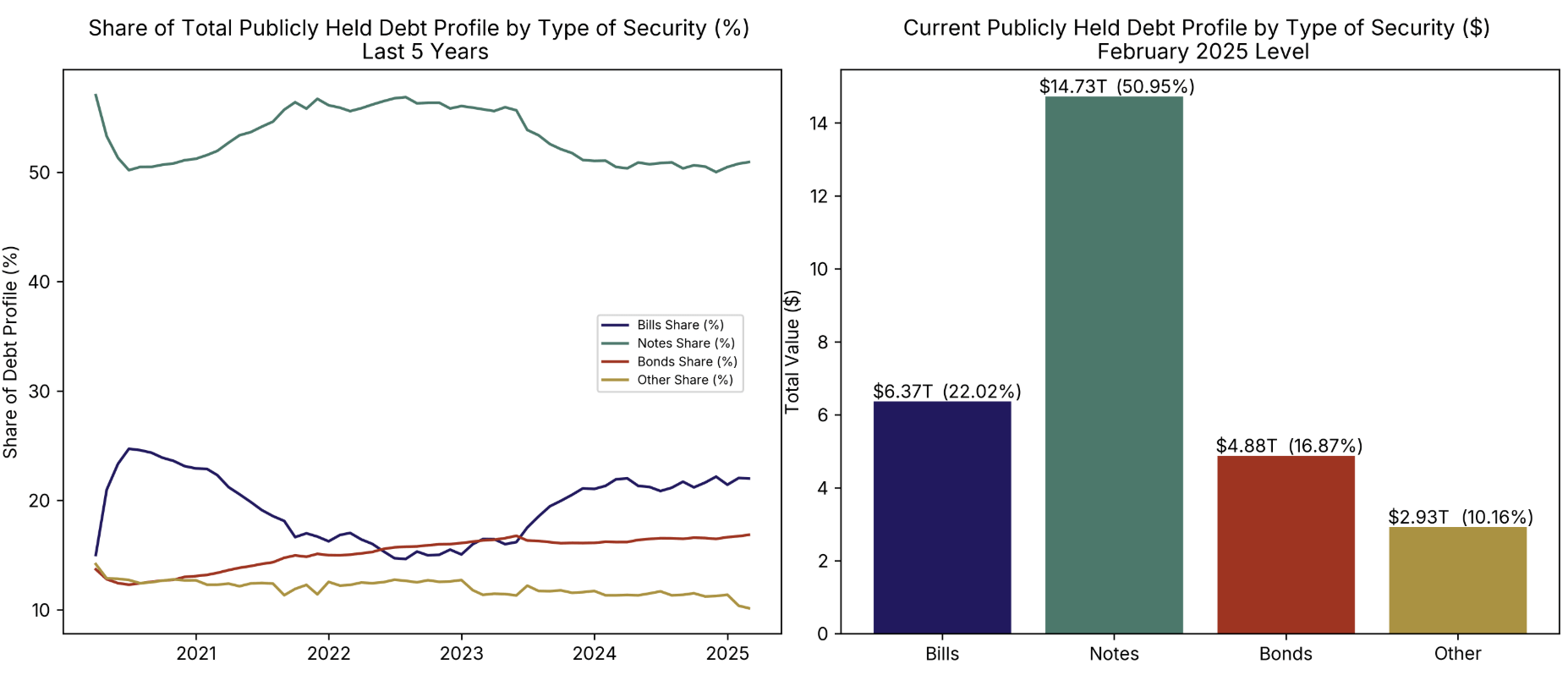

For example, as I discussed in a recent article, the former administration used aggressive short-term debt sales to finance its deficit. They did so to keep long-term bonds from becoming too volatile in an election year.

This strategy worked, but also caused the majority of U.S. debt to mature within 12 months, as we can see below.

Wells Fargo

In other words, regardless of politics, it was known that the new administration had to make some radical changes. In this case, it's President Trump who has to deal with these challenges.

The quote below is from my friend and hedge fund advisor, Albert Marko, on X (formerly known as Twitter). I should also add that he has no political agenda.

This tariff drama was scripted long ago to address problems left over from Biden. Tariff revenue is being tried to be included in budget projections to offset tax cuts coming around May. Also helps Bessent address Yellen’s issuance debacle and end QT.

Many think Trumps actions were erratic, but I promise you that it was all planned out in advance. - Albert Marko (via X)

Moreover, to add another quote, Tony Nash, whom I quoted yesterday as well, noted that President Trump had consistently commented on interest rates. This, too, is more evidence that there is a much bigger focus on temporary pain to lower rates than on stock market stability.

X/@TonyNashNerd

To give you more evidence of the tactical use of tariffs, I am using the table below. We see that the overwhelming majority of tariffs announced so far were punted, dropped, or quickly removed.

Signum Global Advisors

In other words, while I fully expect that the U.S. will see economic re-shoring to de-risk supply chains, I do not expect that Trump actually wants to hurt the economy. There is no evidence for that.

What we are likely dealing with, supported by data, is a move to (temporary) lower interest rates by pushing capital into longer-dated bonds. By doing so, the government can refinance debt, improve its balance sheet, and pave the road for potential economic support to kickstart economic growth.

Bloomberg's John Authers seems to agree with me, as he brings up a few important points that align with the quotes and data I just brought up:

Bessent has been clear that he had three aims from markets — a weaker dollar, cheaper oil, and lower 10-year Treasury yields. In combination, these allow for far greater US dynamism. The problem is that these things seldom overlap with a strong economy, so it was difficult to see how his targets could be achieved without a recession. The idea of a “Mar-A-Lago Accord” to negotiate a weaker dollar has been popular in large part because it would allow the US to square this circle. - Bloomberg

On Thursday, Bessent got all of these things, supported by OPEC's decision to boost output, which could not have come at a worse time for investors - or a better time for President Trump.

Bloomberg

While I did not predict this event, I see my bigger thesis confirmed, which is one big reason why I am not worried about my portfolio.

Yes, short-term pain isn't fun, but the macroeconomic and political environment is much less 'random' than one might think.

More likely than not, this is the needed decline before the next move higher.

Buying The Best On Weakness

I cannot tell you when markets will bottom. I won't even try it.

All I care for is the risk/reward.

Given the bigger picture, the more 10-year rates fall, the more likely we are getting closer to a point where economic support can be expected.

On top of that, valuations have gotten a lot better.

Currently, the S&P 490, which excludes the top ten holdings, trades below 18x earnings. Although that's not a very low number, it is far from overvalued and indicates a high likelihood of decent long-term returns, all else being equal.

JPMorgan (Notes Added By Author)

When digging deeper, we can find even bigger opportunities.

Cyclical stocks are especially interesting, as the chart below shows. You're looking at the transportation ETF I brought up earlier in this article.

- The upper part of the chart shows the outright stock price of the ETF.

- The lower part shows the distance (in %) the ETF is trading below its all-time high (the red line) compared to the ISM Manufacturing Index, one of the most important leading economic indicators. As we can see below, a lot of weakness has been priced in, similar to the 2022 recession fears.

XTN, ISM Manufacturing Index (TradingView)

Needless to say, this is just an example. I'm not telling you to all jump into transportation stocks. It's mainly a good indicator for the risk/reward.

To give you some food for thought, I am looking into a wide variety of stocks at the moment. This includes transportation stocks. In the weeks and months ahead, I will provide a lot more detailed research on these.

For example, a few weeks ago, I doubled my position in Union Pacific (UNP), America's biggest and most efficient public Class I railroad. Although cyclical, it also enjoys an ultra-wide-moat business model with a network that covers all economic hubs in the Western two-thirds of the United States.

This includes major ports like Portland, Oakland, Los Angeles/Long Beach, and Houston, as well as a record number of gateways to Mexico, a 26% stake in Ferromex, a major bulk/merchandise franchise, and partnerships like Falcon Premium with Canadian National Railway (CNI) to compete with Canadian Pacific Kansas City's (CP) three-nation footprint.

Union Pacific Corporation

After struggling with profitability after the pandemic, a leadership change triggered a huge improvement in its operating ratio (inverted operating margin), as the operating ratio is now 60.0%, the best number in its industry for four consecutive quarters.

Union Pacific Corporation

The railroad also has a leading return on invested capital, meaning it's the best when it comes to efficiently putting capital to work (capital expenditures).

This matters a lot, especially in capital-intensive industries like railroads.

Currently yielding 2.4%, the railroad has hiked its dividend for 18 consecutive years since 2006. During this period, it has grown its dividend by 17% per annum and bought back 44% of its shares.

While it needs to be seen how impactful tariffs are (this applies to all stocks in this article!), analysts expect 8% EPS growth in 2025E to be followed by 12-13% growth in the two years after that. Applying its 10-year average P/E ratio of 21.3x, we get a fair stock price of $320, 42% above the current price.

UNP (FAST Graphs)

In general, I like railroads. This includes CSX Corp. (CSX), Norfolk Southern (NSC) - in that order - and the Canadians I just mentioned, as tariff fears have provided a great risk/reward.

I also like other modes of transportation. In this case, I am an aggressive buyer of Old Dominion Freight Line (ODFL). Although it yields just 0.7%, it has a sub-20% payout ratio and a five-year CAGR of 34%.

Its unique less-than-truckload business model, which comes with a dense network of (mostly) fully owned distribution centers, has made it the most efficient less-than-truckload operator with more cash than gross debt.

At current prices (and anything below), I love the ODFL ticker.

ODFL (FAST Graphs)

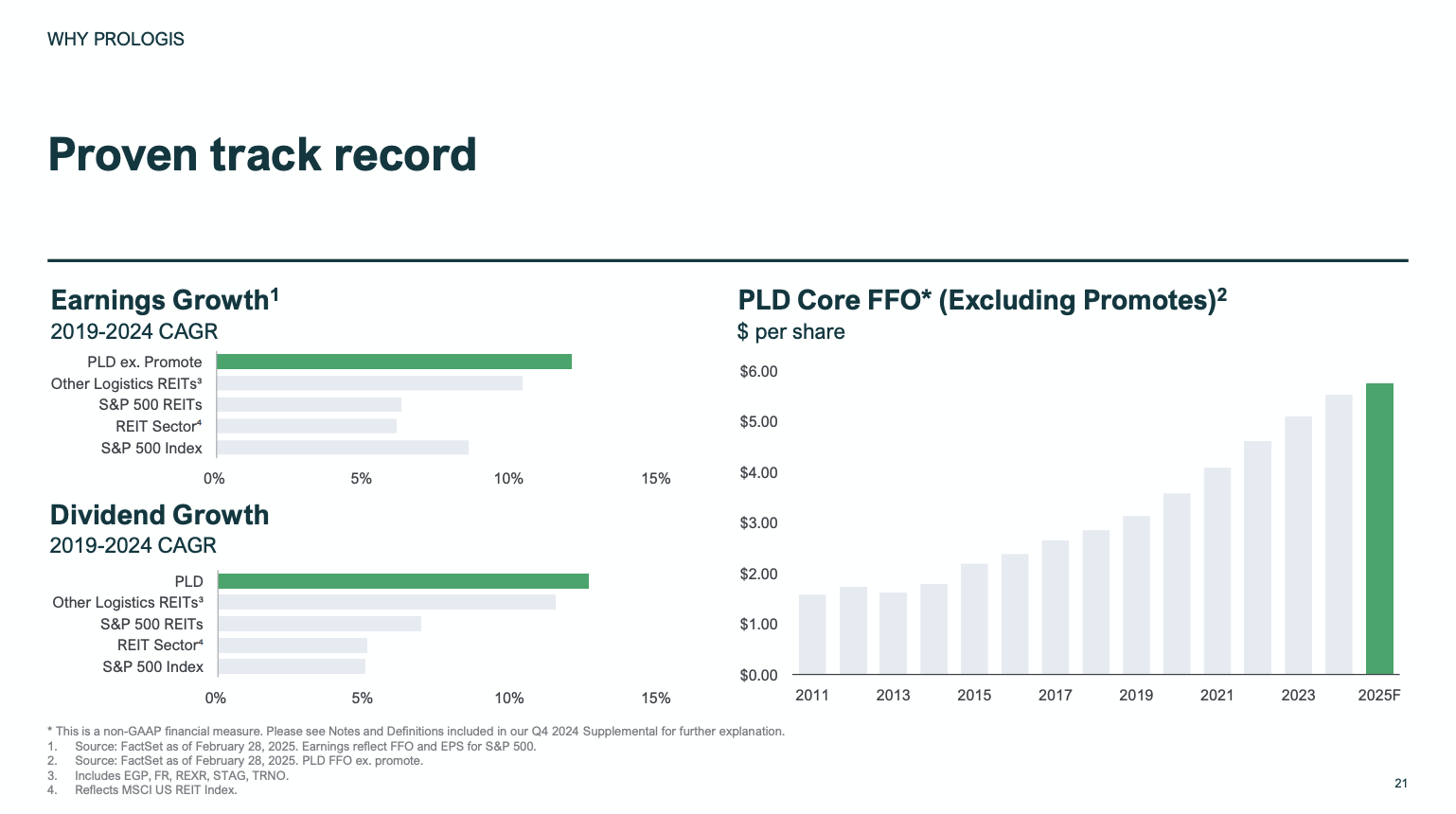

Another stock I mentioned yesterday is Prologis (PLD), the world's biggest warehouse owner. Because tariff fears are expected to hurt global trade, the demand for warehouses could be lower than expected. That's why it sold off almost 10% after the tariff announcement.

Now, it yields 4% and comes with a five-year CAGR of 12.4%. While dividend growth has come down to the mid-single-digit range, it has one of the best dividend growth profiles in the entire REIT universe.

Prologis

It also benefits from the fact that its warehouses are mainly focused on local consumption, meaning trade wars have a limited impact. Moreover, just a third of the goods flowing through its warehouses are cyclical consumer goods.

The company also enjoys an A-rated balance sheet and a valuation that implies more than 40% upside in a conservative scenario.

PLD (FAST Graphs)

Then there's energy, a sector that got hit hard after a great start.

In addition to buying more LandBridge (LB) and Texas Pacific Land (TPL), I am closely watching Topaz Energy (TPZ:CA), a Canadian oil and gas royalty owner.

The company owns mineral rights predominantly in areas like the Western Canadian Sedimentary Basin, where it allows oil and gas producers to produce (you guessed it) oil and gas in exchange for royalties.

Essentially, the company makes money on these operations without spending a single penny on production. That's why it has a 92% free cash flow margin, as it turns every revenue dollar into C$0.92 of free cash flow, a number that is almost unheard of.

Even better, as long as WTI is above $55, the current dividend yield of 6.0% is breakeven at $0 AECO, which is the Canadian natural gas benchmark. This is the benefit of not having production costs, as these are all being paid by the oil and gas producers using Topaz's mineral rights.

Topaz Energy

The company, which aims for a 60-90% payout ratio, could technically double its dividend in a $5 AECO/$85 WTI environment, without incorporating any production growth.

If I had a bigger focus on income, I would be a buyer of Topaz, as I love its business model and believe it makes sense in addition to owning midstream.

Note that Topaz is a Canadian C-Corp. It does NOT issue a K-1 form.

Speaking of midstream, because of Chinese retaliation, even super-safe midstream companies are getting hammered on the stock market.

That's unusual, as midstream companies do not care if oil trades at $60 or $90, as they make money based on throughput. One company I love but don't own (as of yet) is ONEOK (OKE), a giant in areas like the Texas/New Mexico Permian.

ONEOK

ONEOK's 60 thousand-mile network delivers natural gas liquids, crude oil/refined products, and gas. It also owns gathering and processing assets that allow oil and gas companies to produce natural gas liquids.

Despite steep commodity price declines in 2014/2015 and 2020/2021, the company has not seen declining EBITDA. Through 2026, it is expected to see at least 15% annual EPS growth.

ONEOK

Currently yielding 5.0% (up from the low-4% range before the sell-off), I believe ONEOK offers tremendous value, as I love the mix of secular growth, safe income, and the general midstream business model.

Needless to say, these are just some of the ideas that I absolutely love in this ultra-volatile market.

In the days, weeks, and months ahead, we'll discuss a lot more in-depth opportunities and track the global trade war, as I just funded my account again, ready to put a lot more money to work(!).

For now, stay cool and focus on owning high-quality stocks, even if their stock prices may currently suggest otherwise.

Takeaway

April, so far, has been brutal, including two of my worst single-day losses ever.

But I'm not worried.

I have been through volatility before, and I have built my portfolio knowing that big drawdowns are part of the game when you chase long-term upside.

The macro setup may look chaotic, but it's far more strategic than it seems.

If tariffs and rate moves are part of a bigger plan, this sell-off might just be the setup for the next leg higher.

That's why I'm staying focused on quality, buying names like Union Pacific, Old Dominion, and Prologis, three assets of many more that, I believe, are deeply undervalued with long-term tailwinds.

Volatility isn't fun, but it's the price we pay to play the long-term game.

Risks To My Thesis

The biggest risk is a global recession, triggered by tariff retaliation, rising unemployment, and the domino effect that could trigger much lower economic demand down the road.

Right now, the market is pricing in such a scenario.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Test Drive iREIT© on Alpha For FREE (for 2 Weeks)

Join iREIT on Alpha today to get the most in-depth research that includes REITs, mREITs, Preferreds, BDCs, MLPs, ETFs, and other income alternatives. 438 testimonials and most are 5 stars. Nothing to lose with our FREE 2-week trial.

And this offer includes a 2-Week FREE TRIAL plus Brad Thomas' FREE book.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}