Roman Tiraspolsky/iStock Editorial via Getty Images

With summer travel season right around the corner, it's a great time to follow up on a travel stock, so I picked JetBlue Airways Corporation (JBLU), a $1.6B market cap company that serves 100 destinations across the United States, the Caribbean, Latin America, Canada, and Europe.

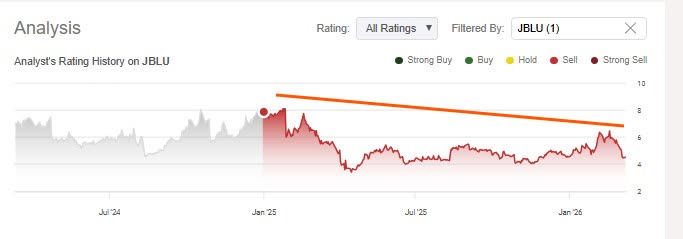

While many of the stocks I rate here often are bullish or neutral views, this was one of those that I called a Sell in my Jan. 2025 article, and this proved to be a great call since the stock is down nearly -43% since then.

JBLU - rating history (Seeking Alpha)

In addition, given the geopolitical turbulence over the last week or so causing added market volatility and what appeared to be an oil shock, this stock is down nearly -28% for the month, as of Tuesday morning, so the larger global events certainly haven't helped it.

What concerned me the first time around was its negative margins and cashflow, a high D/E among peers, and an elevated short interest. It is also not a dividend stock, so in lieu of my dividend outlook I'll be talking about cashflow trends instead, as well as considering the latest data and some figures from their last earnings results in late January where they missed estimates.

Thesis Summary

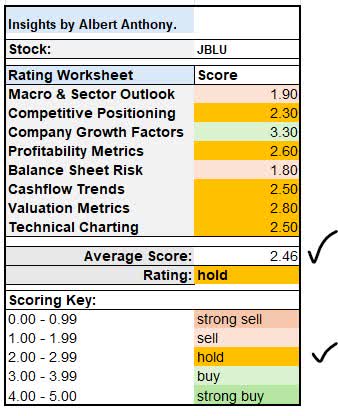

Based on my updated review today, I'm actually upgrading this stock up a notch from sell to hold this time, and the worksheet below shows how my 8 rating categories drove the overall score.

JBLU - rating worksheet (author)

Despite volatile headlines recently about oil/travel/regional conflicts, there are some growth drivers for this airline including new routes and initiatives, but also an effort towards improving profitability and cashflow, and both valuation metrics/price forecasts and technical chart patterns supporting a neutral view right now.

Macro & Sector Outlook

Similar to what I've written about hotel REITs that I cover, airlines also can be prone to major market shocks impacting consumer travel sentiment/spending, and the price of oil too which airlines depend on.

There is a degree of interconnectivity in the global travel sector among airlines, hotels, and cruise lines, and therefore some negative impacts also may be shared.

For instance, CNBC highlighted just days ago how multiple geopolitical conflicts this year that include Iran, Venezuela, and Puerto Vallarta (Mexico) have taken their toll, saying:

Executives have already had to make costly changes: rerouting or cancelling sailings, issuing flexible booking and refund policies, grounding planes and changing flight plans altogether, or discounting hotel rooms.

Well, grounded planes lose money, and that can be further headaches for those like JetBlue that have already dealt with profitability issues as I said earlier.

Even though such conflicts, including the latest one in the Middle East, eventually can resolve, some thought leaders have also pointed out rising costs as headwind.

For instance, in late January, Boston Consulting Group expected air travel to grow in 2026 modestly however also acknowledged that "ongoing growth is fragile," pointing out high cost structures in this industry, saying

"costs per average seat kilometer (CASK) are rising faster than revenues for many carriers due to increases in maintenance, crew, ground handling, and other expenses—putting pressure on already thin margins."

Further, one can't ignore that a major consultancy like Deloitte wrote in its 2026 Travel Industry Outlook last month that many travelers in higher-spend categories may also be pulling back this year. The study said:

Financial pessimism, reaching up to higher income levels compared to recent years, appears to be the biggest cause of this frugal trip planning. And on the corporate side, economic uncertainty may be at the root of more cautious budgeting.

The major canary in the coalmine as of the writing of this, I think, is that the Mideast situation has not yet resolved and any longer-term or larger expansion of this into other regions like the Mediterranean could spell more headaches for airline/travel stocks, even if JetBlue does not fly to that part of the world it does have codeshare agreements with many foreign airlines.

So, from a macro perspective, I am bearish.

Competitive Positioning

In order to position JetBlue within a peer group for comparison, I picked these three airlines: Southwest (LUV), Alaska Air (ALK), and Spirit Airlines whose former stock symbol (SAVEQ) was delisted and now they seem to trade OTC via symbol (FLYYQ).

Although peer data shows JetBlue saw a positive 5-year revenue CAGR of +25%, both Alaska and Southwest were group leaders in this metric, as well as having a better ROE while JetBlue actually saw a negative ROE of -25% which continues to be disappointing.

This competitive niche is somewhat different than big legacy carriers like American (AAL), Delta (DAL), or United (UAL), which are all part of major global airline alliances and I'd say have significantly large global networks, while JetBlue has limited international reach so must compete on fares intensely with carriers like Southwest and Spirit especially.

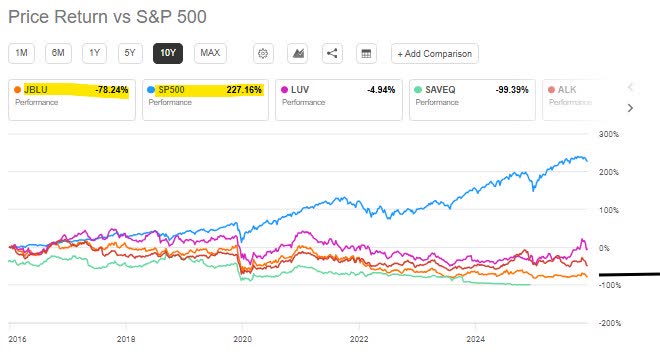

In addition, let's consider what kind of momentum its stock has had so far vs a major benchmark like the S&P 500 (SP500) over the last decade, and how these peers did too, to get a sense for historic price return:

JBLU - momentum vs sp500 (Seeking Alpha)

From the data above, JetBlue is among the two worst performers against the S&P 500, along with Spirit Airlines.

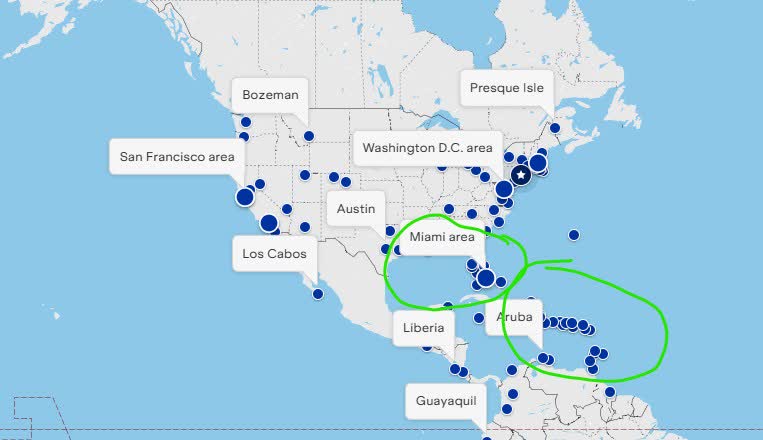

Where I think the JetBlue brand could continue to have a competitive foothold is a robust network of direct flights to multiple destinations in Florida and the Caribbean, as their route map shows:

Jetblue - route map (company website)

So, JetBlue is a case of weaker top-line growth and ROE than some key peers, as well as severe underperformance vs the S&P 500, but a significant route network covering Florida and the Caribbean, in addition to the West coast and other key destinations like Austin.

For this reason, I thought it would be fair to at least give it a cautious hold rating.

Company Growth Factors

A major potential growth opportunity seemed to collapse when the proposed merger between JetBlue and its peer Spirit Airlines failed to move forward. The Guardian reported in 2024 that the two airlines are "seeing no path forward after a US judge blocked the deal in January on anti-competition concerns."

Subsequently, Spirit filed for Chapter 11 bankruptcy protection, as reported in a major financial site in 2025., and was delisted from the NYSE.

So, the other growth factor I went looking for was new or expanded routes, as this could drive future passenger growth, boosting the top line. Earlier, I mentioned JetBlue's key penetration into the Florida market, and this month the airline announced new service from New York JFK to Destin Florida, with the company saying:

These new routes build on JetBlue’s continued growth across Florida, where the airline now serves 11 destinations and is a leading carrier between the Northeast and the Sunshine State.

The company also announced it is adding to daily nonstop flights between Houston and New York, with the company pointing out last month that this helps

"customers gain additional access to JetBlue’s broader network, including destinations across the East Coast, Europe, Latin America and the Caribbean."

Thus, those are key examples of growing routes as an upside driver, however also notable are some other initiatives in 2026 that could grow the brand, and the company mentioned those in their Q4 results in late January:

We have many exciting initiatives rolling out this year, including executing critical implementation milestones for our Blue Sky collaboration with United, opening our Boston lounge and rolling out domestic first class.

From another angle, Seeking Alpha data shows expected fwd revenue growth of +4.3%, which is relatively positive despite being slightly below the sector average.

I gave this stock a bullish view in this section, since I like the potential momentum all of the above factors could be driving, despite the Spirit Airlines merger not having succeeded. Also, since its core market is the U.S//Caribbean region, I think it will be considerably less impacted if regional travel demand drops in the Mideast.

Profitability Metrics

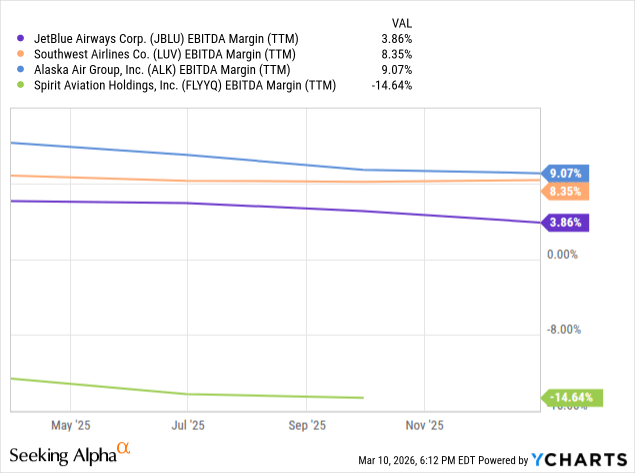

The margin I chose to compare vs. peers is the EBITDA margin, which strips away one-time accounting items and noise from depreciation of assets, so I think it could have a huge impact on core earnings:

In this example, JetBlue's EBITDA margin of +3.8% was indeed positive but also trails behind two key peers, Southwest and Alaska, and also its trend line (dark blue) seems to be declining rather than improving, so this could impact core earnings if the trend continues.

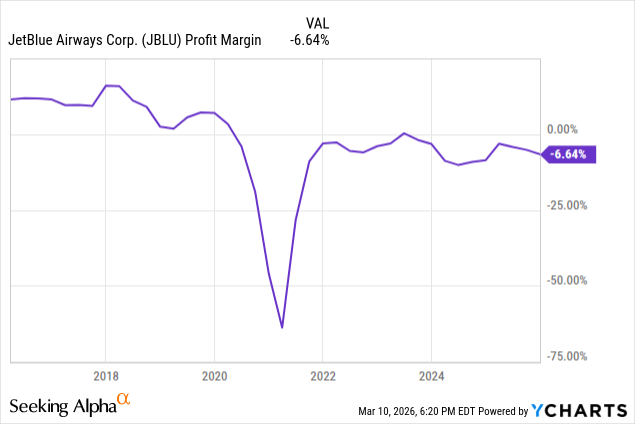

As far as the net profit margin, which could ultimately impact headline EPS numbers, we can see the airline took a huge impact during the pandemic years, tried to make a recovery, but still struggled to be profitable:

There is some sunlight piercing the clouds, however, with consensus EPS estimates call for some growth this year and next, although with expected EPS remaining negative.

Now, I like to add something about how a company may be trying to be more cost efficient and give credit where it is due. I also tout my horn a lot about the value of AI if used for practical reasons, so notable about JetBlue's Q4 investor deck (pg. 12) is the company boasting of cost savings through the JetForward strategy, saying they used "improved tools and utilization of AI to optimize planning, better manage disruptions and enable greater self-service."

The major canary in the coalmine, however, could be an extended oil market shock like we saw in the last few days, since even though airlines can "hedge" fuel costs to an extent, but a drawn-out spike in oil costs can end up squeezing margins or force them to charge very uncompetitive fares.

It seems like an ongoing situation as of this writing, with fluctuations daily, and as of Tuesday afternoon BBC reported that "oil and gas prices fell sharply on Tuesday after U.S. President Donald Trump said that the war in Iran was 'very complete, pretty much'."

So, it would appear JetBlue has an EBITDA margin that could do better, a profit margin that absolutely has to turn positive, some tailwind from AI-driven efficiencies, and also uncertainty over where geopolitical conflicts will push oil prices. Because of this mixed picture, I am neutral on this stock in this section.

Balance Sheet Risk

In this section, I'll touch on credit ratings, debt vs equity, and asset risk.

Notable is that a major agency like Fitch had downgraded JetBlue to a below-investment grade "B-" rating last year, mentioning "ongoing operating losses and high debt" as key factors weighing down on this company.

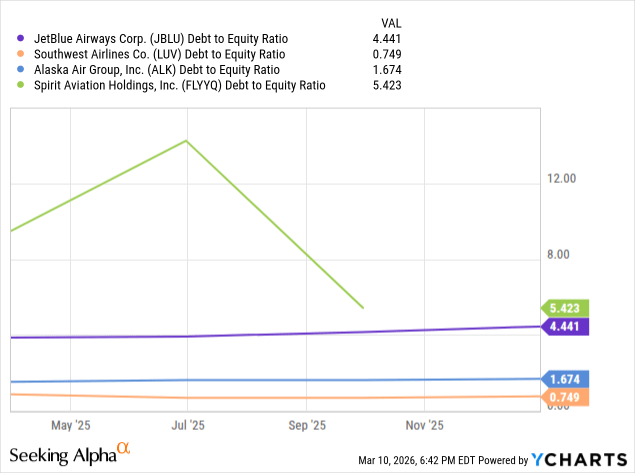

As for D/E, here is how JetBlue looks vs. peers:

From the chart, we see JetBlue has among the highest D/E of this group, at 4.44, right below Spirit, and so this continues to be a concern, especially since that trend line does not seem to be coming down meaningfully and so the leverage risk seems elevated.

As far as asset risk, consider from balance sheet data that this airline's largest asset is neither cash or tradeable securities but around $17B in gross property/plant/equipment, so what comes to mind right away is their vast fleet of aircraft owned, as well as any buildings/facilities they may own.

The type of asset risk faced in this case is that these aircraft have to be flying as much as possible since they lose money the longer they are on the ground. The downside risk of being grounded is very real for all airlines. For instance, as Newsweek reported recently, JetBlue's recent nationwide ground stop due to a system issue, which was since resolved, is a rare but impactful event and can lead to "large impacts on flight schedules, causing delays for hundreds of flights."

Therefore, investors thinking about risk management should consider the elevated D/E and below-investment grade rating of JetBlue, as well as this being a business sitting on a very costly fleet of aircraft that cannot afford to be grounded long. The risk needle here is quite high for me, and so I am bearish in this section.

Cashflow Trends

Although I typically cover dividend stocks, such as REITs and other sectors, in the name of diversification today I'm covering this non-dividend stock so instead I'll point out some cashflow metrics.

Earlier, I said this business sits on a huge fleet of aircraft, so they have to generate cashflow since the company is so leveraged.

In the peer data below, what sticks out is that JetBlue has significant negative operating cash flow of -$94MM, while Alaska and Southwest remain positive:

JBLU - net operating cashflow (Seeking Alpha)

One way to improve this is reducing capex, and so the company said in their Q4 investor deck (pg. 13) that they "strategically reduced 2026-2029 capex by ~$3B since 2023," so I think that is a positive sign, also mentioning the JetForward strategy can be a "driving path to positive free cash flow by the end of 2027."

Because of this, I think a cautious neutral rating is fair in this case, and the challenge for JetBlue will be to continue executing on that pledge and show they can really make a cashflow turnaround.

Valuation Metrics

Because my usual valuation worksheets depend on there being a positive EPS, in this case JetBlue has no fwd P/E metrics, as valuation data shows, so in this case I too a look at the EV/EBITDA and the price/book value.

JetBlue's fwd EV/EBITDA is 11.60, slightly under the sector average, while the price/book multiple is just 0.79, considerably undervalued vs the sector.

It seems the market is trading this stock at a slight discount to the future EBITDA, there may not yet be overly bullish confidence there compared to peers with stronger margins, and the market also seems to be not willing to pay a premium for this airline's book value, considering the risk profile of owning an asset like aircraft while also being highly levered up.

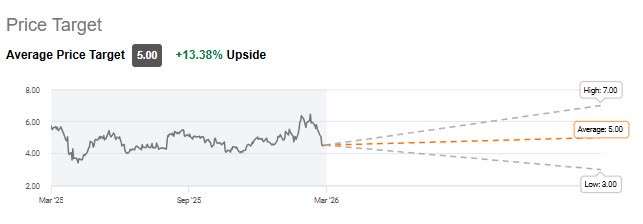

Interestingly, the avg Wall St rating implies there could be further +13% upside in the share price:

JBLU - price target (Seeking Alpha)

So, this seems to be a case where there is good reason for the market to have undervalued the stock price, but then there is also expectation of future upside, and I think this will depend heavily on continuing successful execution of the profitability and cashflow improvement program. So, I am neutral in this section.

Technical Charting

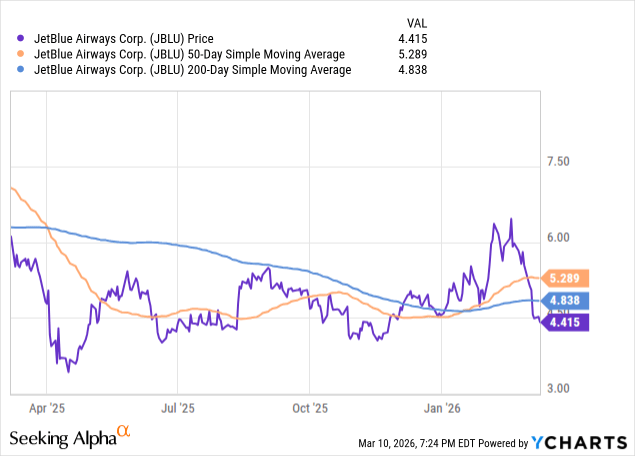

Moving away from the fundamental topics discussed so far, let's consider this technical chart comparing the share price over the last year vs. the 50 day and 200-day SMA:

In this chart, we can see a clear buy signal (golden cross) happened around January when the 50-day SMA crossed above the 200-day. The two moving averages have been parallel for a little while, however the share price has broken its bullish trend and pretty much sunk below the 200-day.

Right now, there is no clear sell signal (death cross), but the bullish case also is in question until we see where the trend may go further, so for now I am neutral/hold.

Incidentally, this technical pattern also reinforces/supports the overall neutral view I have on this stock this time.

Risks and Challenge to Thesis

The key challenge to my Hold rating, which is essentially neutral, could be recessionary impacts in 2026. If an extended oil shock/geopolitical conflict generates a recession, U.S. airlines like this one could feel it, making my view overly positive, but if those conflicts turn out to be short-lived and by next week the major media is talking about ceasefire and oil returning to normalcy, we could see a return to confidence and making my view overly cautious. So, I think that macroeconomic trends will have the greatest weight of all the topics I considered today, and that happens to be the factor the airlines have least control over.

Conclusion

To conclude this follow-up today, I upgraded my prior Sell rating to a Hold, agreeing with much of the consensus as of Tuesday on this airline, and despite many concerns (unprofitable, high debt, etc.) there were silver linings in the clouds that I identified in my article this time around.

Although this is not a dividend income stock, the neutral thesis is betting on further capital growth rather than dividend income, and so for now it is a good time to fly in neutral gear as I wait and see if this airline can turn its numbers around after all.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.