malerapaso/iStock via Getty Images

It seems that the risks for the BDC sector (BIZD) just keep emerging one after another. In the space of less than 2 years, the sector has been pressured by falling base rates, compressing spreads, stagnant M&A markets, enormous supply of new entrants, and, recently, increased credit risks from Tricolor and First Brands bankruptcies and weakening SaaS businesses, which play a significant role in BDC portfolios.

As a result of these dynamics, the BDC index has dropped by ~23% in the past 12-month period. This is a huge drawdown.

On top of this, 12 BDCs have delivered negative news on the dividend front, where even such names as Golub Capital (GBDC) and Gladstone Capital (GLAD) were forced to make these painful decisions. In the context of the publicly traded BDC space that consists of ~55 players, the fact that 12 BDCs have cut their dividends in the past 12-month period is significant.

Moreover, I firmly believe that there will be many more announcing these kinds of news as they report the Q4 and/or Q1, 2026 figures. The logic here is simple: 1) BDC sector average base dividend coverage is 100% (i.e., no margin of safety), 2) balance sheets are fully leveraged across the board, providing no ammunition to grow, and 3) lower base rates and continued spread compression will just keep pushing the NII per share generation down.

Now, the fact that BDCs are effectively leveraged vehicles that lend to companies that cannot access cheap bank or public capital market financing, in combination with the aforementioned backdrop, which shows how violent the moves in the BDC sector can be, provides a strong ground for excluding BDCs from retirement income portfolios.

In other words, the risks that come with BDC investments are theoretically too high for prudent retirement investors or investors, who cannot afford to play around with the portfolio capital, which is meant for living expense coverage.

Personally, as a structural BDC bull, I would say that this is a fair characterization. However, I completely disagree with the notion that all BDCs are unsuitable for truly reliable and durable current income streams.

In this article I will now try to articulate how select BDCs have what it takes to be considered "sleep well at night" retirement picks. The two BDCs that I will highlight below would most likely be the picks that I would choose if I was forced to invite only two BDCs into my high and durable passive income portfolio.

Pick #1: Capital Southwest, 11.2% yield

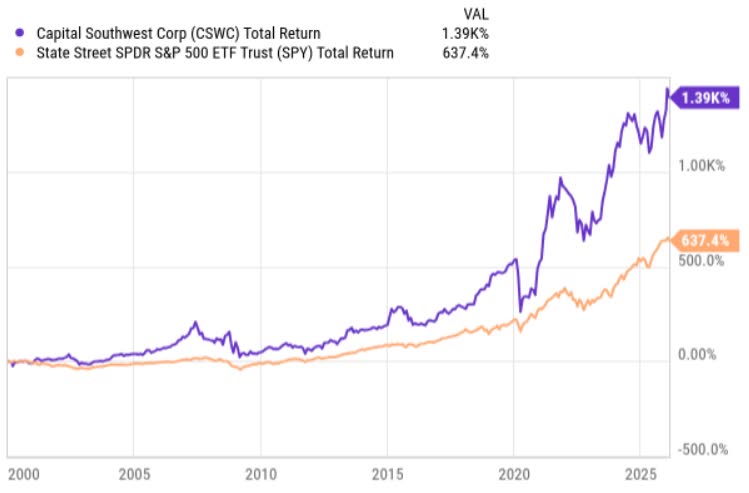

Capital Southwest (CSWC) is a BDC with one of the longest track records as a publicly traded vehicle in the entire BDC industry. It is, of course, nothing that moves the needle in the context of the overall investment case, but it at least allows us to take a look at how CSWC has performed in different market regimes.

YCharts

This chart is really powerful. It shows that CSWC has outperformed the booming S&P 500 (SPY) index and that despite several disastrous events such as the dot-com bubble, GFC, and COVID-19, the BDC has managed to preserve NAV and regular (and enticing) dividend distributions.

The historical performance is not a guarantee of future results, but it certainly puts things into the right perspective when making an argument that CSWC is just a private credit vehicle that is set for a blow-out when the next credit crunch happens.

Now, if we speak about the underlying fundamentals, then this is where the essence lies. And the first thing with which we have to start is the internal management component, which is the main reason why I have chosen CSWC as a buy-and-forget retirement income pick over Fidus Investment (FDUS) - similar to FDUS, at a lower multiple, but externally managed.

The value of internal management is that there is simply better alignment of interest between management and shareholders, and, importantly, the fee structure is more favorable for long-term investors, where, say, in the case of abnormal returns, we can avoid value-restrictive (double-digit) incentive fees that are similar to hedge fund models.

For this reason, internally managed BDCs tend to trade at a premium to externally managed peers. Granted, it might not be the best setup for investors, who are looking for superior gains in the short to medium-term, but when the investment horizon is, say, 10+ years, the internal management factor should support alpha performance (or at least greater stability).

Furthermore, another driver for my preference towards CSWC is the fact that the BDC is equity-biased with a focus on lower middle market businesses, where the competition from the mushrooming private credit supply is inherently lower. For larger money managers, it really does not make sense to dedicate their resources to ~$5 million ticket-size funding, while their underlying portfolio is measured in billions. This dynamic introduces an important moat (or shield) around CSWC's business model, which, practically, manifests itself via higher and more stable spreads.

Now, speaking of the equity bias, I think that it is a huge benefit if a BDC has taken equity co-investments on top of standard loan injections. The equity component, by definition, comes with higher return potential, especially if the holding period is long enough. But more importantly, the equity exposure carries a negatively correlated return factor to traditional loan investments. For example, as the base rates go down, loan investments tend to yield less, thereby resulting in an NII yield compression. Conversely, for equities, lower yields result in higher valuations and a better environment to find traction in the market for successful monetization. Namely, equity investments, which for CSWC account for 9.1% of the total portfolio, can smooth out the return profile and neutralize the negative effects from non-accruals.

Finally, what I really value in CSWC is that it has consistently maintained a conservative leverage profile like now - at 1.07x (debt to equity), while the sector average is closer to 1.22x. This has two benefits: 1) lower sensitivity to potential downside risks, and 2) ability to go on offense when the time is right without entering speculative financial risk territory.

Pick #2: Trinity Capital, 13.2%

Trinity Capital Inc. (TRIN) is just like CSWC, an internally managed BDC, which is automatically a huge positive for long-term investors, who deploy capital for smooth and gradual compounding.

In fact, let me say that finding an internally managed BDC is not that easy or common, as there are only 4 such publicly traded vehicles available out there. I'm not including PhenixFIN (PFX) in the conversation, which is a different beast - i.e., different business model, tiny market cap, and, importantly, value-destructive historical profile (e.g., more than 60% down in the past 10-year period).

Now, the main difference between CSWC and TRIN lies in the investment strategy or scope, which is much wider and more diverse for TRIN:

TRIN Investor Presentation Q3, 2025

TRIN has really built a diversified ecosystem of various lending and equity (warrant) co-investment opportunities, where equipment finance and asset based lending have recently gained a more pronounced momentum. Exactly these two areas have experienced significant growth in the past couple of years - mainly due to lower downside (better protection due to underlying collateral) and expanding CapEx within many asset-intensive businesses.

What the presence of multiple investment avenues brings to the table as well is the ability for TRIN to access a wider and larger origination universe from which to really select the best risk-adjusted investments.

We can see how this has borne fruit for TRIN in the context of portfolio and earnings quality. For example, as of Q3, 2025, TRIN had one of the lowest PIK shares in the entire sector - i.e., at 0.9% of the total income, while for the sector, the metric was 7.9%. Similarly, TRIN has only 2.5% of its portfolio (at cost) linked to non-accruals, while for the sector it is closer to 4%.

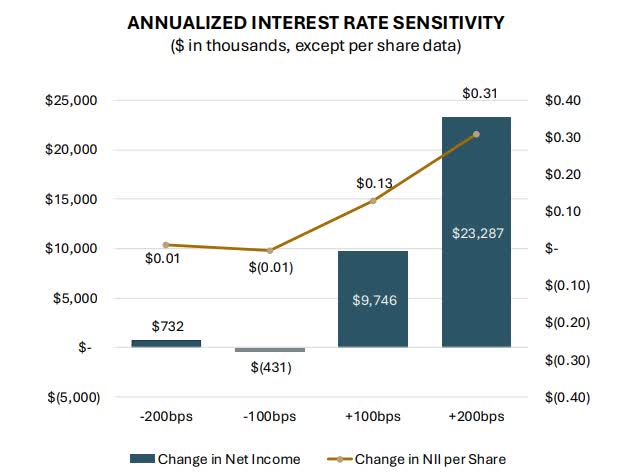

Another area, where TRIN's position of being able to cherry pick the most attractive investments has played out nicely is interest rate management.

Here comes an interesting chart:

TRIN Investor Presentation Q3, 2025

Because of the favorable interest rate floors, TRIN is in a unique position to avoid negative pressures from lower base rates, while almost any other BDC in the sector is forced to deal with the consequences (i.e., NII per share going down due to lower SOFR).

In a nutshell, I would certainly include TRIN in my "2 BDC retirement income portfolio" alongside CSWC for durable and stress-free income returns as well as long-term compounding.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.