Getty Images

VICI Properties (VICI) is a no-nonsense stock that perfectly fits income-seeking investors who want stability, predictability, and preservation of capital.

Investors who are disappointed with the stock's returns over the past few years should rethink their strategy, as VICI isn't a stock for market-beating adventures.

For its purpose, low-risk 8%-10% shareholder returns, I still view VICI as a one-of-a-kind asset, which is why I continue to rate the stock a 'Buy.'

VICI's Growth Is Slowing As Management Maintains Impressive Prudency

There aren't many companies where highly cautious management teams are necessarily a good thing, but in VICI's case, I believe it's unquestionably important.

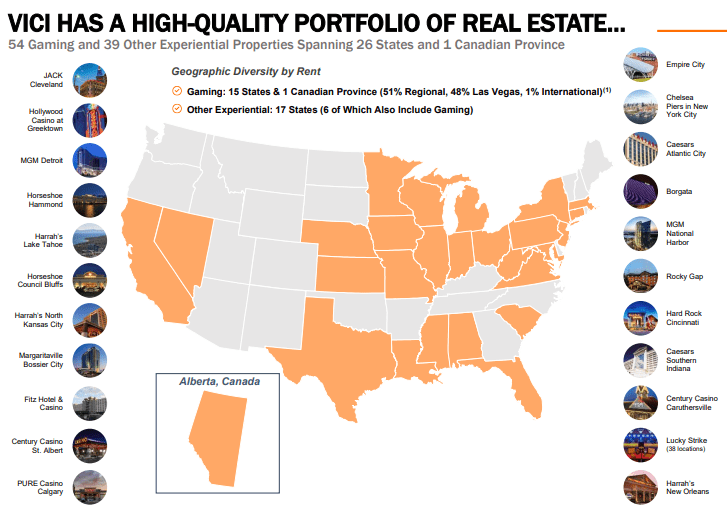

We're talking about a company that truly has an 'N of One' real estate portfolio, consisting of irreplicable assets, mainly across the Vegas strip.

VICI November Investor Presentation

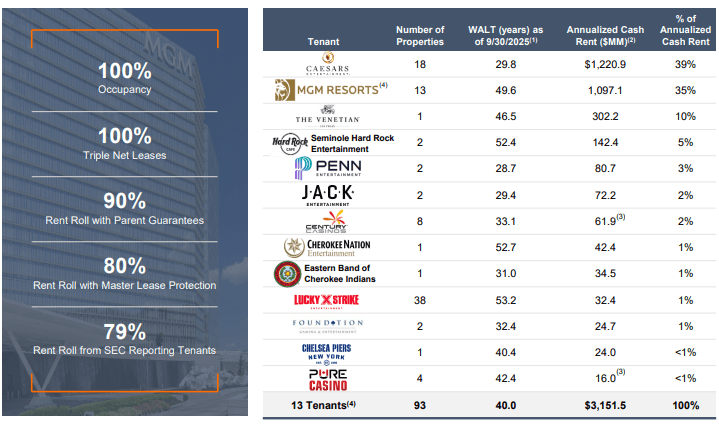

This unique portfolio of assets, unsurprisingly, draws an extraordinary group of tenants that are the best at what they do. Occupancy is almost always at 100%, rent has never been late, lease terms are long, and there are annual escalations in every one of them.

VICI November Investor Presentation

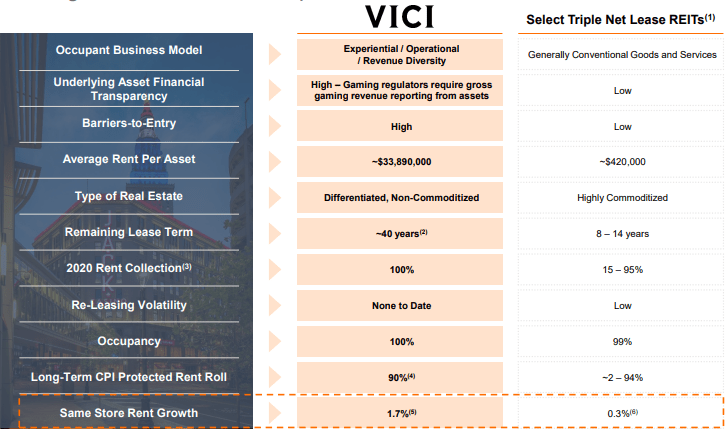

Simply put, VICI has arguably one of the safest and most predictable revenue streams in the world for the next few decades. However, this is both a gift and a curse.

VICI November Investor Presentation

When you already have a perfect portfolio, it's hard to add new assets to it without diluting its quality. Furthermore, after VICI's success, the experiential asset base has garnered more and more attention from other players, making valuations higher.

From the last earnings call:

We at VICI have been, are and will continue to be examining, evaluating and potentially investing in through our insight-driven approach, depending, of course, on our determination that these experiences have the investment attributes we rely on.

We are mindful, very mindful that at a time like this, it's more important than ever to identify as best we can the risks of oversupply, obsolescence and the other factors that can lead to real estate capital destruction. And through that identification process to determine what we will and will not invest in.

This is the perfect depiction of the strict screening that VICI's deal pipeline goes through. It also perfectly explains why it essentially dried out. VICI hasn't done a meaningful deal in a few years, and for an asset business like this, that means growth is hitting a wall.

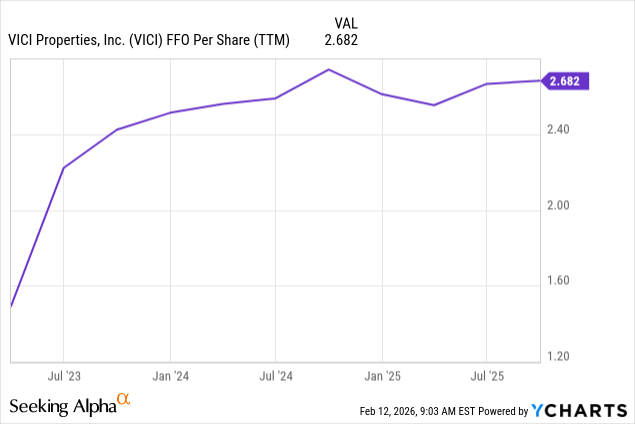

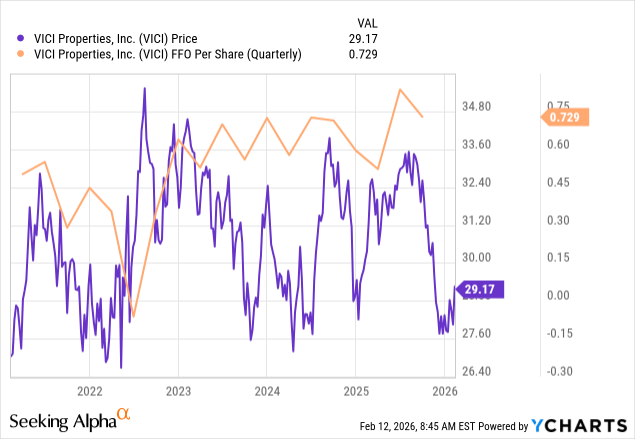

Indeed, FFO per share has been quite stable over the past few quarters, and there's not much on the horizon that signals change.

Ahead of its Q4 earnings due on February 25th, the number one thing to monitor, in my view, would be their deal pipeline and whether they have something meaningful on the table.

In November, they signed a $1.16 billion sale and leaseback transaction with Golen Entertainment, adding 7 gaming assets in Nevada. As always, they expect it to be immediately accretive to AFFO per share, so it'll be interesting to see how it supports their guidance for 2026.

VICI's Growth Pipeline Remains Thin, As Tenant Base Expands

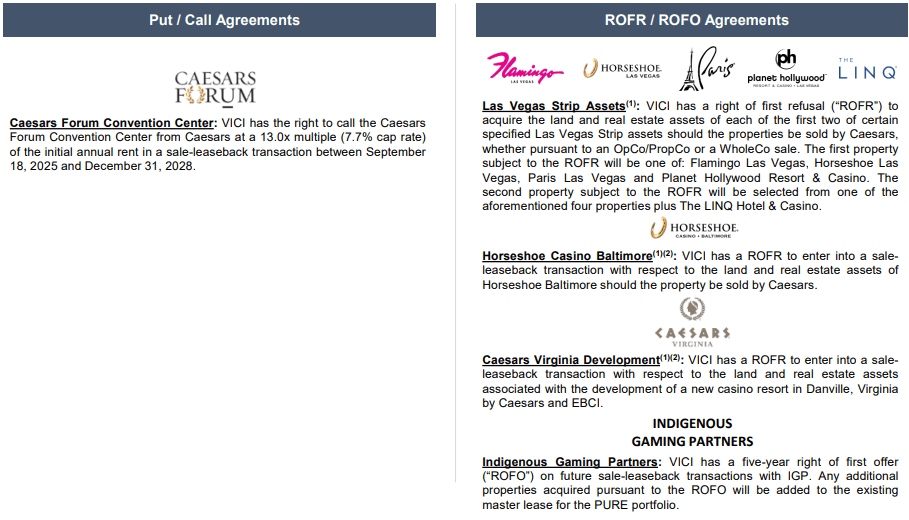

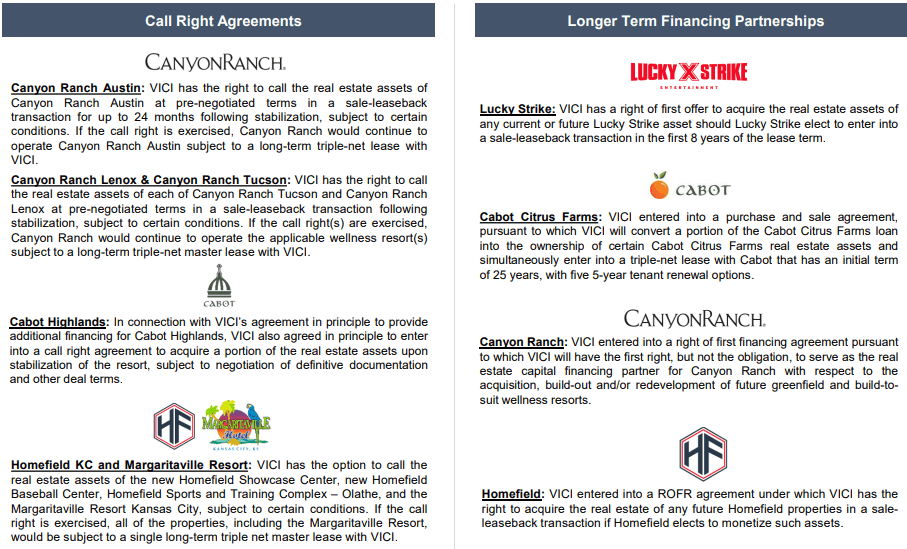

In Q3 and through 2025, VICI hasn't announced any major new deals. In addition, its option portfolio remained roughly the same. They hold an option on the Caesars Convention Center and the right of first refusal on several assets across the Strip, Horseshoe Baltimore, Caesars Virginia, and future Indigenous Gaming Partners deals.

VICI November Investor Presentation

VICI also has a call option for several assets from Canyon Ranch and Homefield KC, as well as additional financing opportunities with Cabo.

VICI November Investor Presentation

All in all, the once-exciting story of VICI as an aggressive accumulator of assets has subsided, and the stock performance followed.

Seeking Alpha

That aside, VICI did announce it has a new tenant, the fourteenth one. MGM Resorts, the operator of the assets VICI acquired when it bought MGM Properties, signed a deal to sell its Northfield Park operations to Clairvest Group (CVTGF).

Clairvest is a private equity firm with ownership interest in 36 gaming assets. We don't have a lot of information about their specific gaming arm, but we do know that VICI's management said the deal reflects a higher coverage ratio on rent. Also, VICI said Clairvest has a strong track record in North American gaming.

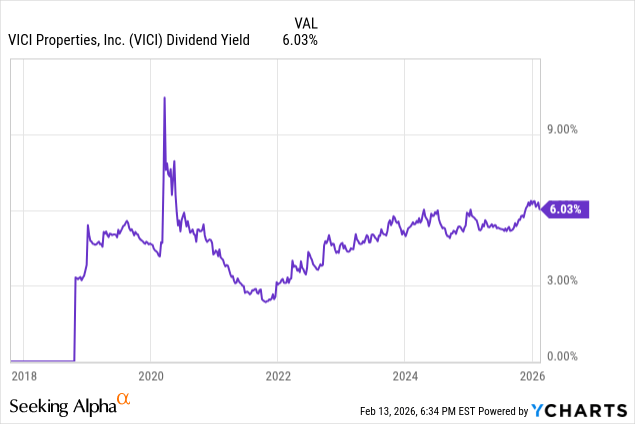

Yield Is At Multi-Year High, And So Is The Value

At $29.3 per share, VICI provides a record 6.2% forward dividend yield, which is roughly a 215 bps spread over the 10-year treasury.

Unlike a treasury bill, though, VICI is consistently increasing its dividend payout every year. Over the past five years, they've raised dividends by 7.0% annually. The last increase was a bit lower, at 4%.

Seeking Alpha

Bottom line, investors can effectively put this portion of the total shareholder return in pen, about 6% annually. It doesn't end here.

Valuation At Multi-Year Low

A REIT like VICI should be valued based on the adjusted funds from operations it generates. In simple words, that's the cash flow its business produces.

VICI Q3'25 Supplemental

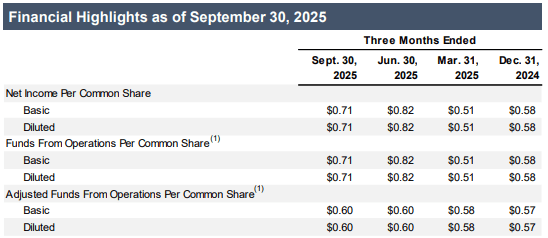

In Q3, AFFO per share was $0.6, in line with Q2, and up 5.2% from December.

VICI Q3'25 Supplemental

VICI is guiding for $2.37 AFFO per share in 2025, which means it expects to exit the year at a similar quarterly pace of roughly $0.6.

Assuming no growth in 2026, we get to a forecast of $2.4 in AFFO/share, which would mean the current price of $29.3 reflects a 12x multiple.

For several years, VICI's stock price tracked its FFO, but we can see a clear divergence in the past few months. This could be explained by some concerns over Las Vegas tourism, and slowing growth, as VICI maintains a prudent approach to acquisitions.

Still, I think it's safe to say that the 12x multiple is a floor for a company like VICI. As such, we should add 2%-4% annual AFFO per share growth to the total shareholder return calculation, and that assumes no multiple expansion.

Conclusion

VICI is a know-what-you-own story. If you're looking for a multibagger, you should look elsewhere. But, if you're looking for a steady stream of very decent income, and 8%-10% annual shareholder returns, this is the right place.

We don't know when, but once treasury yields drop, VICI will become an even more attractive asset, and that should further enhance the TSR equation over the long term.

All in all, I believe VICI has a place in the majority of portfolios, and I reiterate the stock at a 'Buy.'