LETFs: Structural Arbitrage & The Mathematics of Decay

Why 3x Leverage is Mathematically Flawed (and the 2.0+ Sharpe System That Exploits It)

Hello!

Welcome back. Today, we will be looking further into a topic that I wrote about in the past: volatility decay. Also known as beta slippage or volatility drag, this is a neat concept that helps us understand the structure of the market.

In my opinion, it is crucial for everyone to understand this, as this concept (or similar concepts) appear(s) in all markets.

At the end, I will share a strategy that has a Sharpe ratio of over 2. Let’s get into it.

Recap

In my first post on this topic, LETFs: Volatility Decay & Optimal Leverage, I explained how LETFs utilize derivatives and daily rebalancing to amplify daily index returns. We broke down the mechanics of "volatility decay," demonstrating mathematically how choppy markets erode capital and why this drag accelerates with higher leverage.

Despite common warnings against holding LETFs long-term, we introduced research on "Optimal Leverage," which suggested an optimal leverage (that was not 1x!) for historical US markets.

In my second post on this topic, LETFs: Dual Strategies for Smarter Leverage, I examined two leveraged ETF strategies. The first strategy used LETFs to construct a leveraged variation of the traditional 60/40 portfolio. While this portfolio delivered exceptional gains from 2009 through 2021 aided by negative stock-bond correlations, the strategy suffered losses in 2022 when rising interest rates caused both asset classes to decline simultaneously.

The second strategy in the post amplified outperformance relative to the benchmark (S&P 500) by capitalizing on lower prices during drawdowns.

All About Returns

Today, we are going to stick with analysis in the U.S. equity markets. A common assumption in the markets is that the returns for a stock are normally distributed. This is a core assumption of the Black-Scholes model. As I have written about before, we know that this assumption is incorrect, due to negative skew and positive kurtosis (leptokurtic). While there are clear errors with this assumption, let’s assume that the returns for a given stock or ETF are roughly normal for this post.

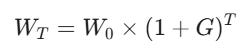

In finance, your wealth at time T (WT) is not the sum of your daily returns; it is the product of your daily growth factors. If xi is your return on day i (e.g., +0.05 or -0.02):

This is, in essence, compounding, We want to find the single rate G (Geometric Growth) that represents this messy path:

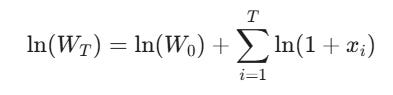

We can then take the natural logarithm (ln) of both sides:

Because ln(a * b) = ln(a) + ln(b), the product turns into a sum:

If we ignore the starting wealth, we are simply left with the summation of the log returns (ln(1+x)).

But, why do we use ln(1+x)?

If you have a discrete return x (like +10%), the ln(1+x) calculates the continuously compounded return required to achieve that same result. For example, if a stock appreciated 10%, the continuously compounded return would be 9.53%, as ln(1.10) = 9.53%. Therefore, ln(1+x) transforms the discrete return into its continuous equivalent.

This is helpful as wealth accumulation is a multiplicative process, but statistical tools (like mean and variance) work best on additive processes. The logarithm is the tool that converts the former into the latter, and this makes them mathematically elegant for computers and researchers.

Additionally, it helps us model the behavior of the underlying stock, as it imposes symmetry. For example, if stock XYZ is at $100, and has a 10% increase on day 1, and a 10% decrease on day 2, the stock price is not back to $100. Rather, it is at $99. The geometric returns would be 9.53% and 10.53%, respectively.

Geometric returns impose symmetry as equal up and down moves in geometric return space force the underlying stock back to its starting value. This symmetry is what allows us to model the 'drag' effectively. It reveals that a -10% loss hurts more than a +10% gain helps.

Taylor Series

In this part, I will give a refresher on Taylor series and how it connects to the concept of vol decay.

A Taylor Series approximates any complex, curved function (like a logarithm or sine wave) using a sum of simple polynomial terms (like x2, x3, x4).

The general formula for approximating a function f(x) near a point a is:

As we saw above, we care about Geometric Growth, which is governed by logarithms. Therefore, we can use a Taylor series to approximate the the function ln(1+x). I won’t do all the math out (as it is difficult in Substack), but this is the final approximation to two derivatives.

We approximate at 0 as daily returns are close to 0 and you want to approximate as close to the majority of your data points as possible (once again, assuming a roughly normal distribution of returns). A return of 0% is roughly the mean return on any given day for the S&P 500. 1

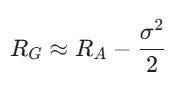

Now, this is something that is interesting. The -(x2/2) term is our volatility decay, itself. The full term says your realized compounded return is your average return minus half your variance.

In formal finance terms, volatility decay creates a divergence between the Arithmetic Mean (simple average) and the Geometric Mean (compounded growth).

The approximation formula for this relationship is:

Does this look familiar? This is the exact formula we just derived, but explicitly showing the divergence between the geometric mean and the arithmetic mean. This means that the higher the volatility (sigma), the lower your realized compound return (RG) will be relative to the average daily return.

Deriving the Levered Formula

Now, let’s connect this all to LETFs. Simplistically, LETFs multiple each underlying daily return by some leverage multiple. As you all know, I do not view volatility decay as some evil spirit that justifies the avoidance of LETFs, as all stocks and ETFs display some sort of volatility decay.

Instead of trying to avoid volatility decay, we should find the optimal leverage (0.5x, 1x, 2x, 5x, 100x?) given that volatility decay not only exists, but rises exponentially with our leverage ratio.

The paper that I shared in this post came up with an optimal leverage through various backtests, but there is an elegant mathematical solution that verifies its findings.

In this mathematical optimization, we want to maximize the Geometric Growth Rate, not the Arithmetic Mean. However, before we solve for optimal leverage, we need to derive the levered formula.

The return of your levered portfolio (RL) is the risk-free rate plus the leveraged excess return:

RL = r + f (Rm - r)

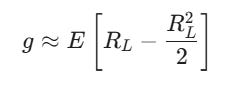

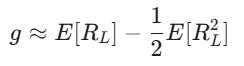

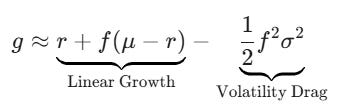

Rm is the market return, r is the risk-free rate, and f is the leverage. To find the Geometric Growth (g), we take the expected value (E) of the log return:

g = E [ ln(1 + RL) ]

Then, taking our Taylor approximation from above (x-(x2/2)), we can substitute:

And then simplify:

1) The linear term is simply expected return:

E[RL] = r + f*(µ- r)

2) Now, onto the squared term (E[RL2]). We need to square the levered return formula (from above). For small time intervals, the risk-free rate part becomes negligible when squared compared to the volatility, so we approximate RL = f * Rm for the variance term.

RL2 ~= Rm2 * f2

In statistics, E[X2] = variance - (E[X])2. For short time periods (like daily), the mean squared (E[X])2 is tiny compared to the variance, so E[X2] ~= σ2.

E[RL2] ~= σ2 * f2

3) Now, we can substitute the prior steps into the geometric equation.

And, there we go. That is the geometric return for the levered portfolio. It took a bit to get here, but now the fun part comes. In the next section, we will find the optimal leverage formula, and showcase the strategy.

Optimal Leverage

To find the optimal leverage, we take the derivative of the geometric growth with respect to leverage (f) and set it to zero: