takayib/iStock via Getty Images

In our July 2025 article (here) when we last checked on the economic screws, we stated…

So far, tariffs have been repeatedly delayed — only around $20B/month has been collected — and net money-creation continues at a higher rate than last year. Although the BBB spending bill removes resources from the poor and gives them to the rich, the increased deficit-spending ($5T over 10-years) should support the stock market and keep the primary bull trend in place over the next year.

Six-months later, the tariffs have been running at twice what they were in July (~$40B/month) and DOGE has been disbanded with an estimate of ~$200B of cuts (here), far short of the $2T Musk predicted — since Government spending at this point is slightly higher year-over-year, the $200B in cuts must have been applied to other budget lines.

The BBB (Big Beautiful Bill) does not come into effect until the New Year and will bring tax-cuts of $4.5T over ten years with $2.3T of those benefits — more than half — going to the top 10% of earners (here). Tax cuts are the same as spending increases because they leave more money in the private sector, but if these tax cuts are balanced off by reduced spending in areas such as healthcare insurance subsidies, then the positive effect on the economy could be blunted.

These uncertainties make predicting the next 6-12 months in the economy much less certain, but in this article we will check on the current state of the "screws" that hold the economy together.

The Screws Holding the Economy Together

The first chart below is the BaR grid (from econ p.i.) dated June 27, 2025 and the second chart is the most recent dated December 19, 2025.

econ p.i.

econ p.i.

econ p.i.

econ p.i.

Notice that the MoC (mean of coordinates) has moved out of the expansion quadrant and into, while the WMoC (weighted mean of coordinates) and the LD (leading indicators) have both weakened their positioning. This means that the average of economic measures have weakened and are no longer growing. This screw is a little loose.

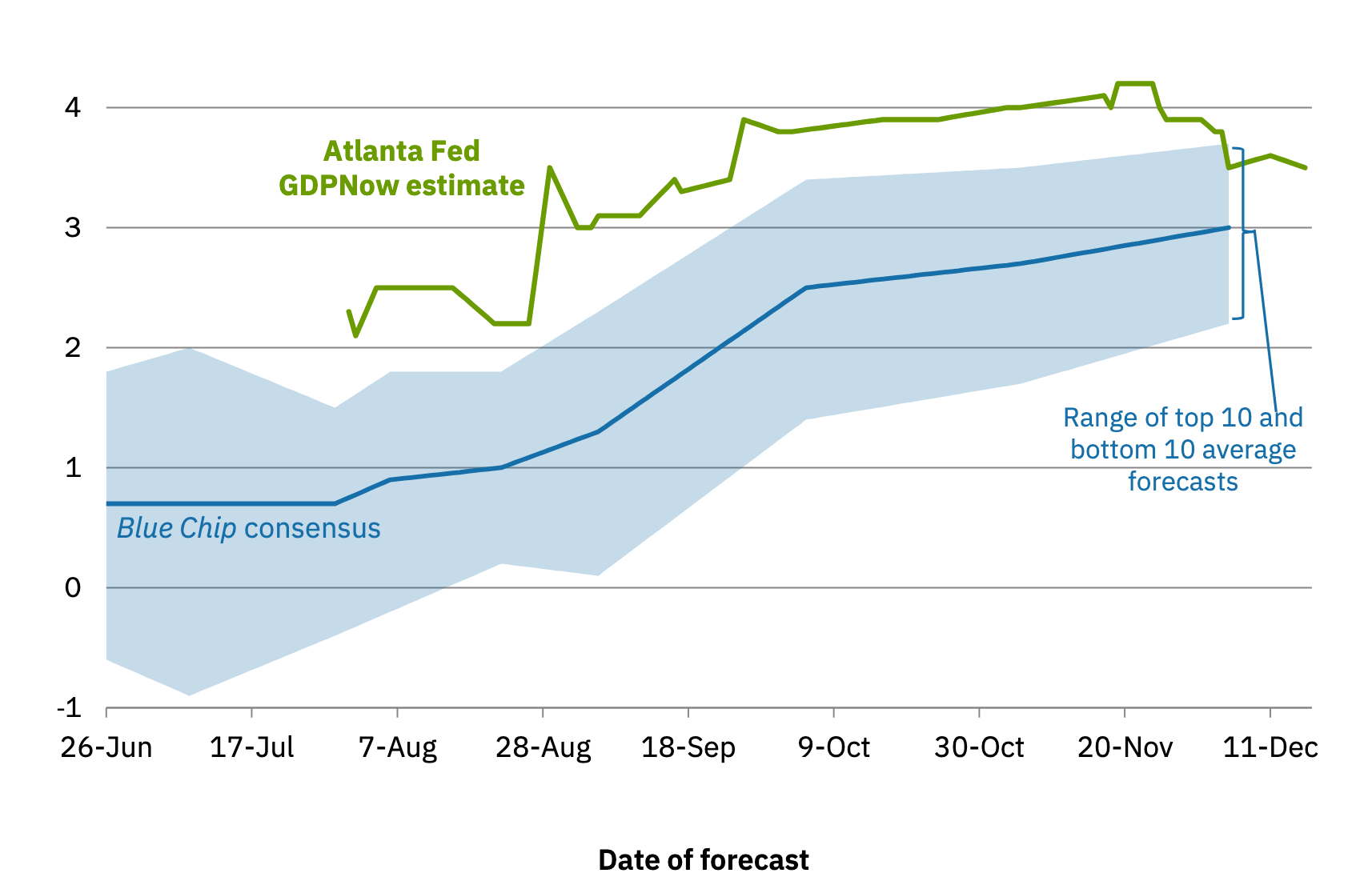

The GDPNow estimate of Q2 2025 is averaging 3.5% (compared to 2.5% last July). This screw is tight (chart below).

GDPNow

Industrial Production of the United States has increased since the start of 2025. This screw is tight (chart below).

tradingeconomics.com

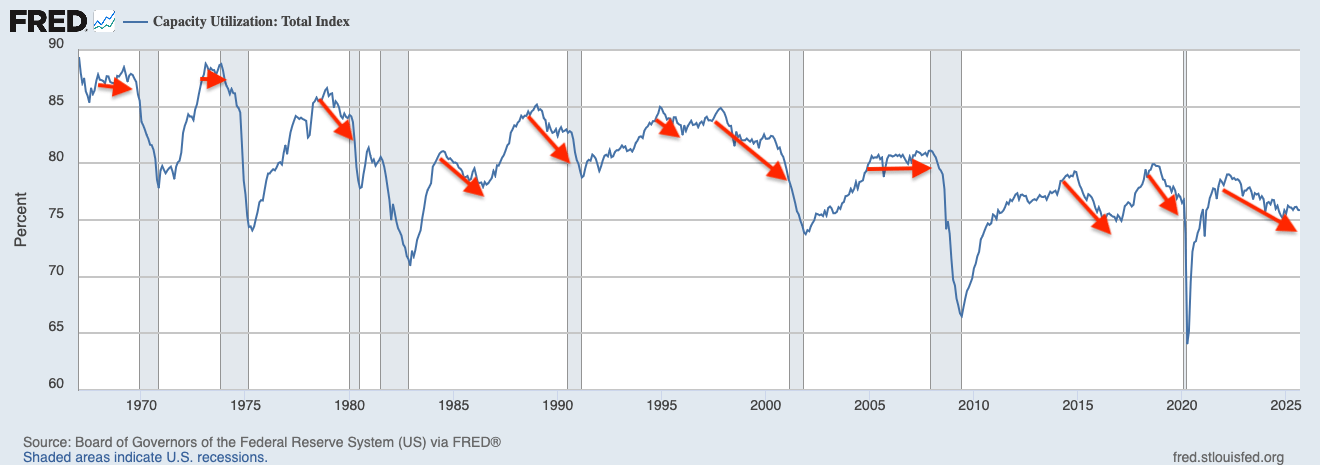

Capacity utilization either stalls or drops ahead of recessions. However, it is a necessary condition, not a sufficient condition for a recession; no recessions resulted following the drop in capacity utilization in 1985, 1995, 1997, and 2015. Capacity utilization has been decreasing, making this screw looser than we would like to see.

FRED

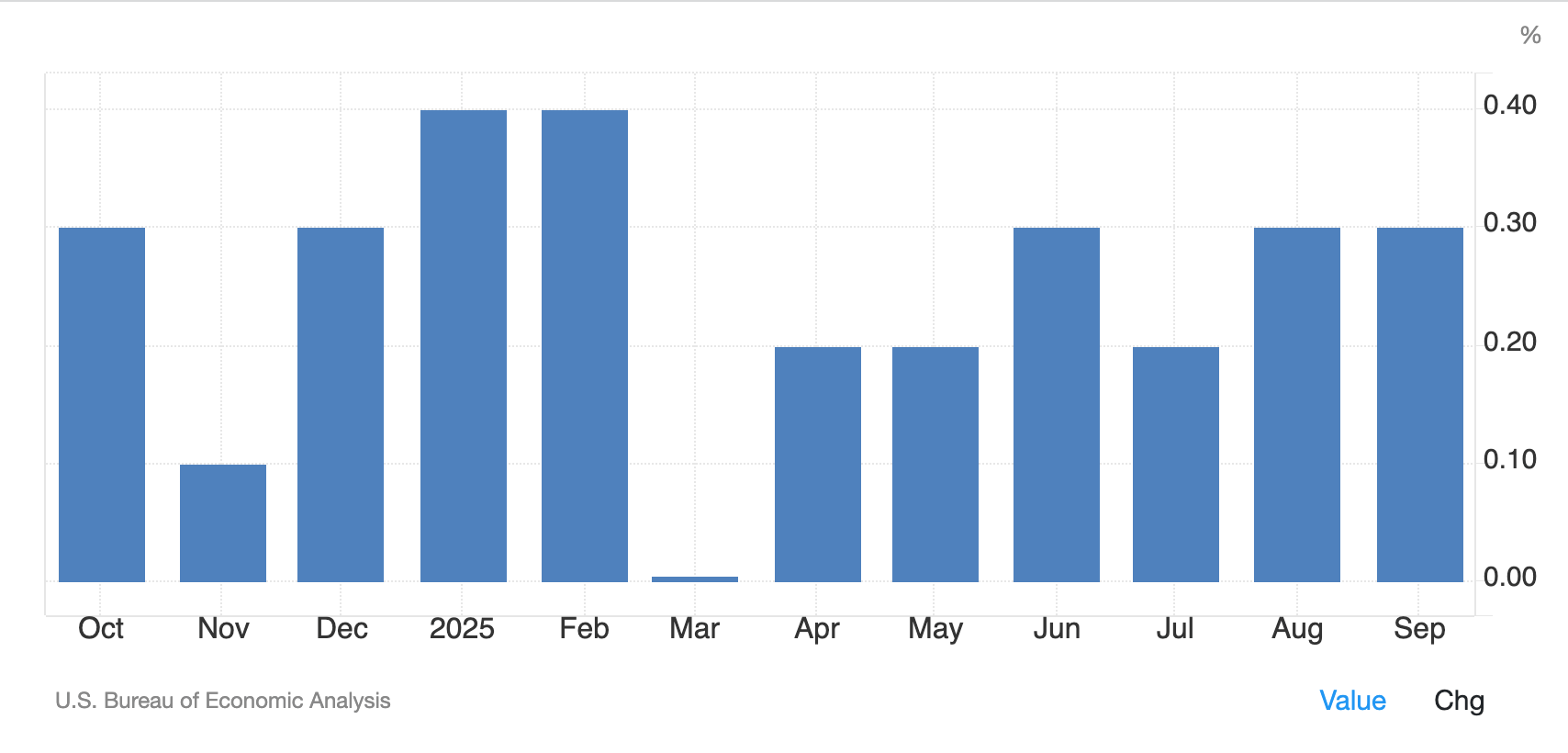

PCE (personal consumption expense), which is the Fed's preferred gauge of inflation, has been steady since June. This screw is tight enough (chart below).

tradingeconomics.com

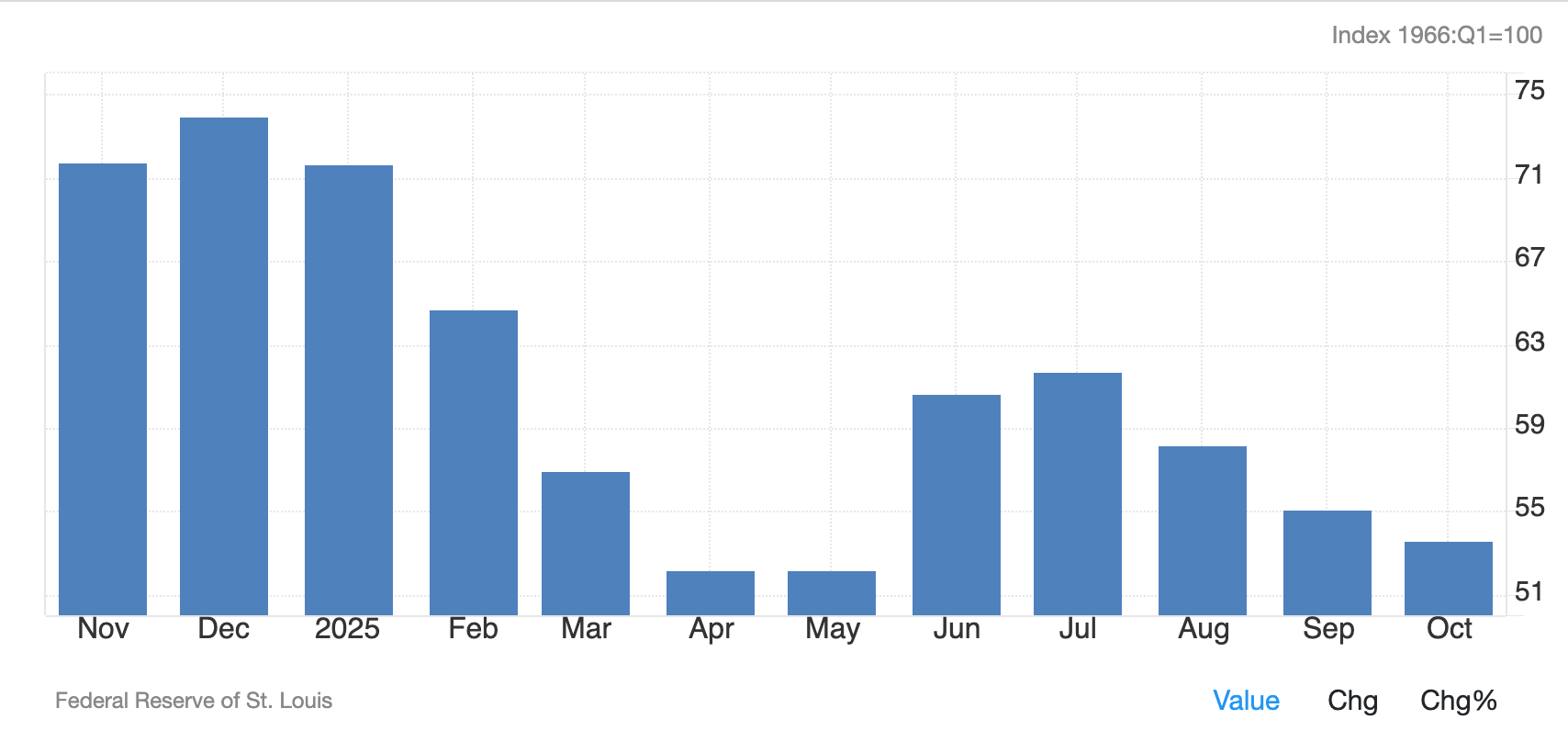

The University of Michigan consumer sentiment for the US has been trending lower since July. This screw is loose.

tradingeconomics.com

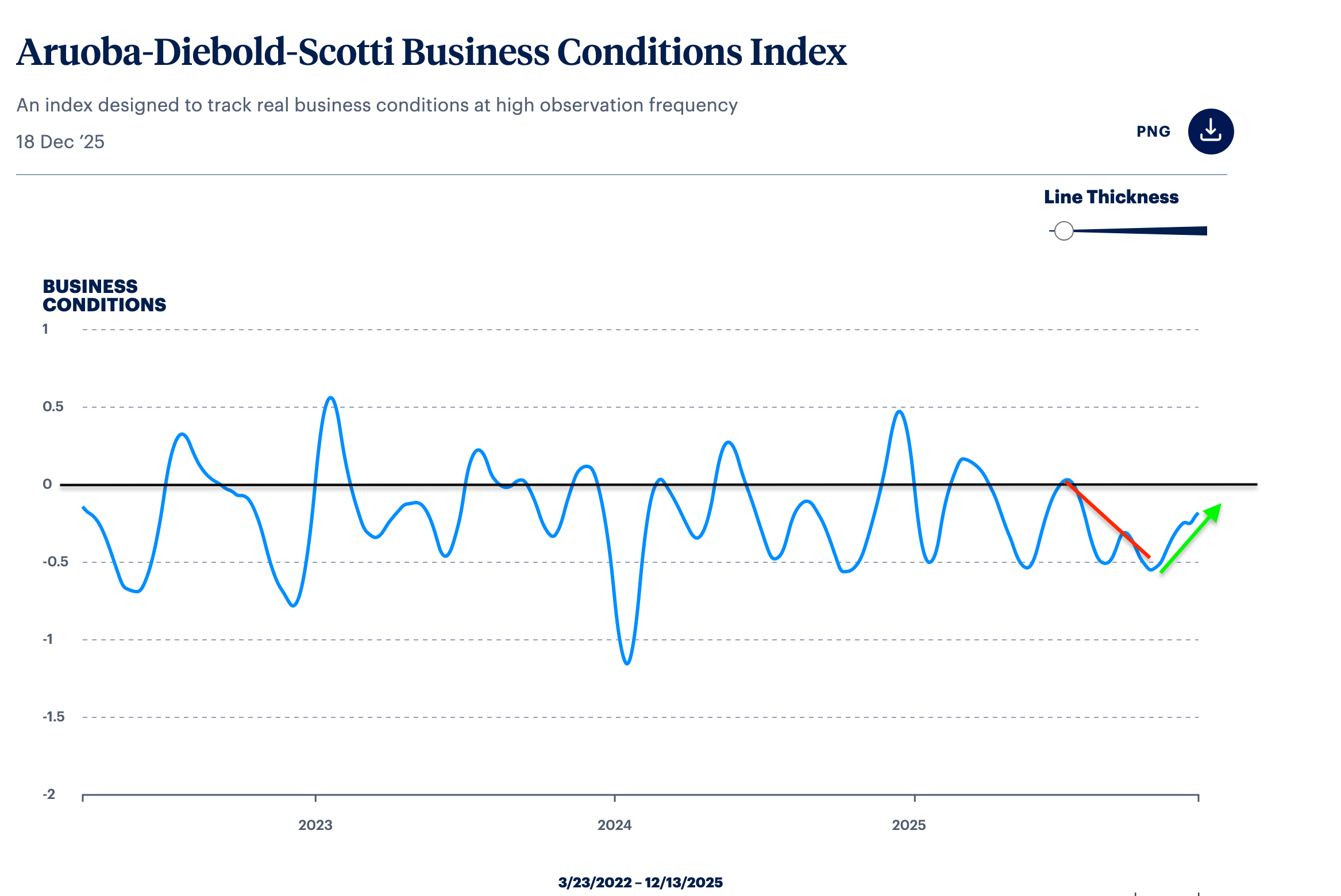

The Aruoba-Diebold-Scotti business conditions index is designed to track real business conditions at high frequency. The average value of the ADS index is zero. Bigger positive values indicate progressively better-than-average conditions, and bigger negative values indicate progressively worse than average conditions. The index shows that business conditions are still slightly worse than average, but have improved recently (green arrow) which makes it a tightening economic screw (chart below).

philadelphiafed.org

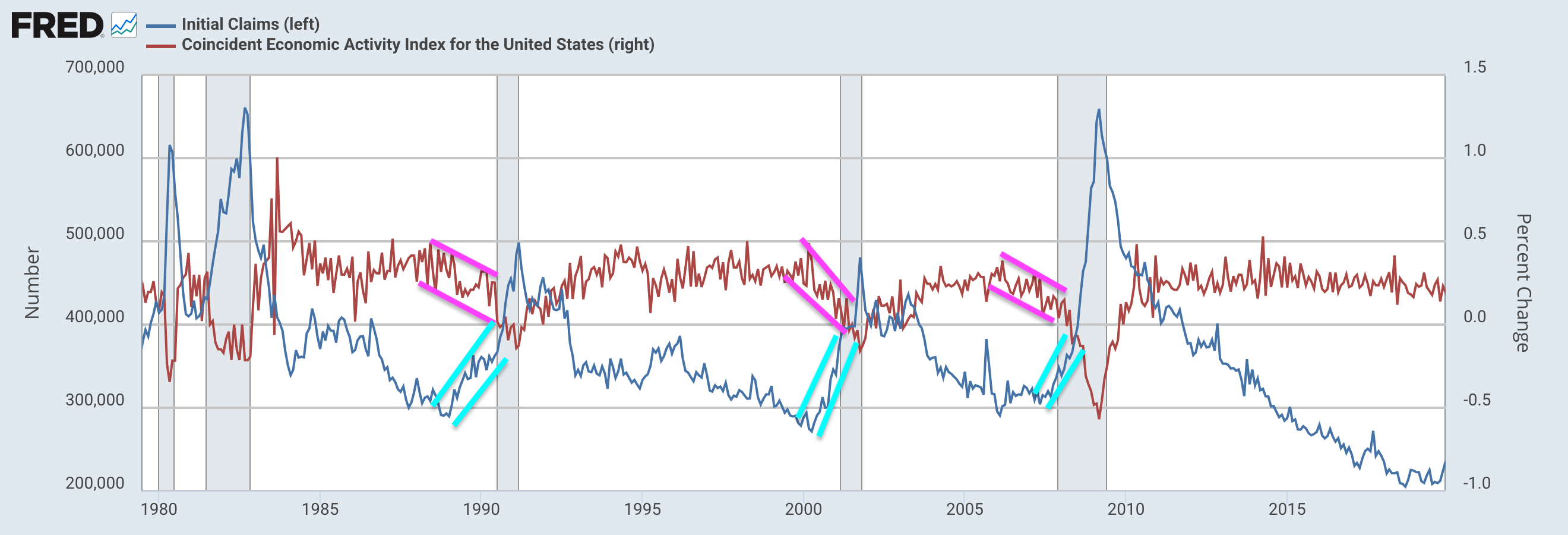

Initial jobless claims [blue] rise for a year ahead of recessions, while business activity [red] falls (chart below).

FRED

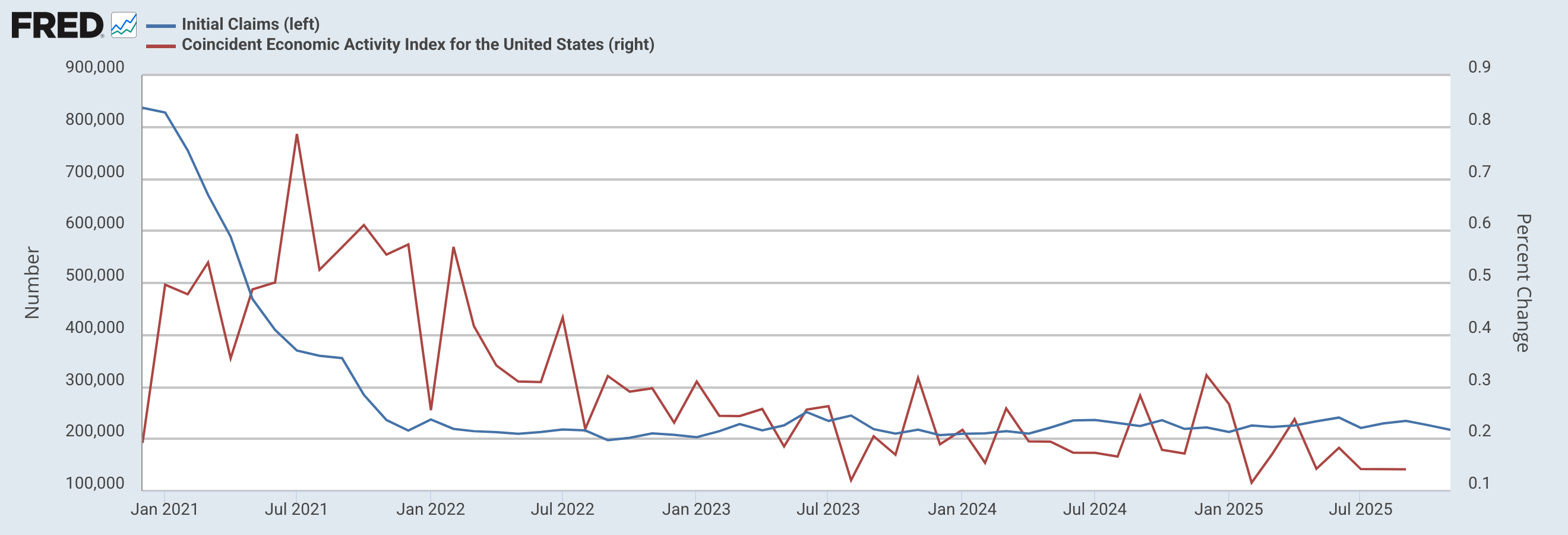

Since 2022, initial claims and business activity have been stable. These are both tight economic screws (chart below).

FRED

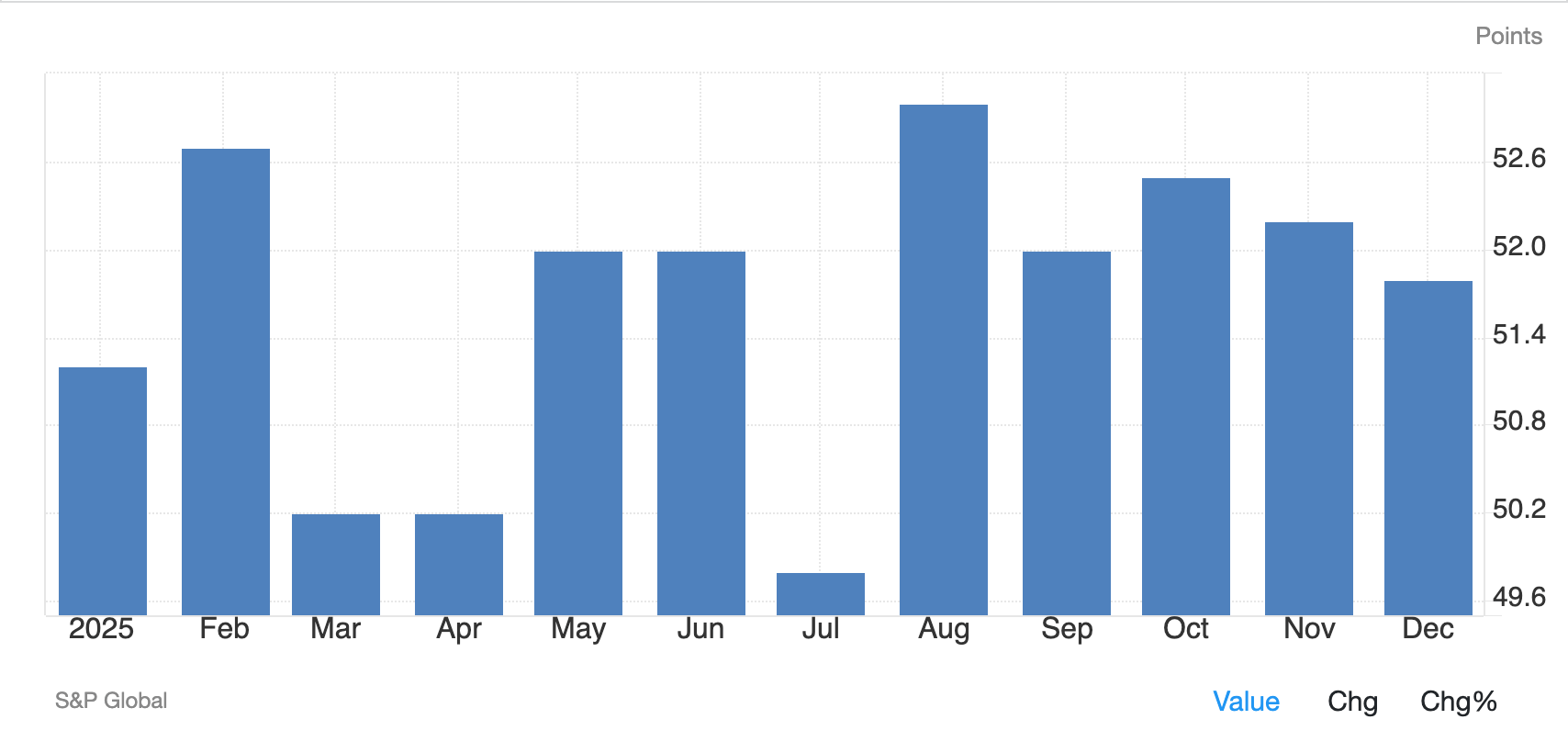

The Manufacturing PMI for the US continues to grow (above 50), but at a reduced rate over the past three months. This screw remains tight enough (chart below).

Tradingeconomics

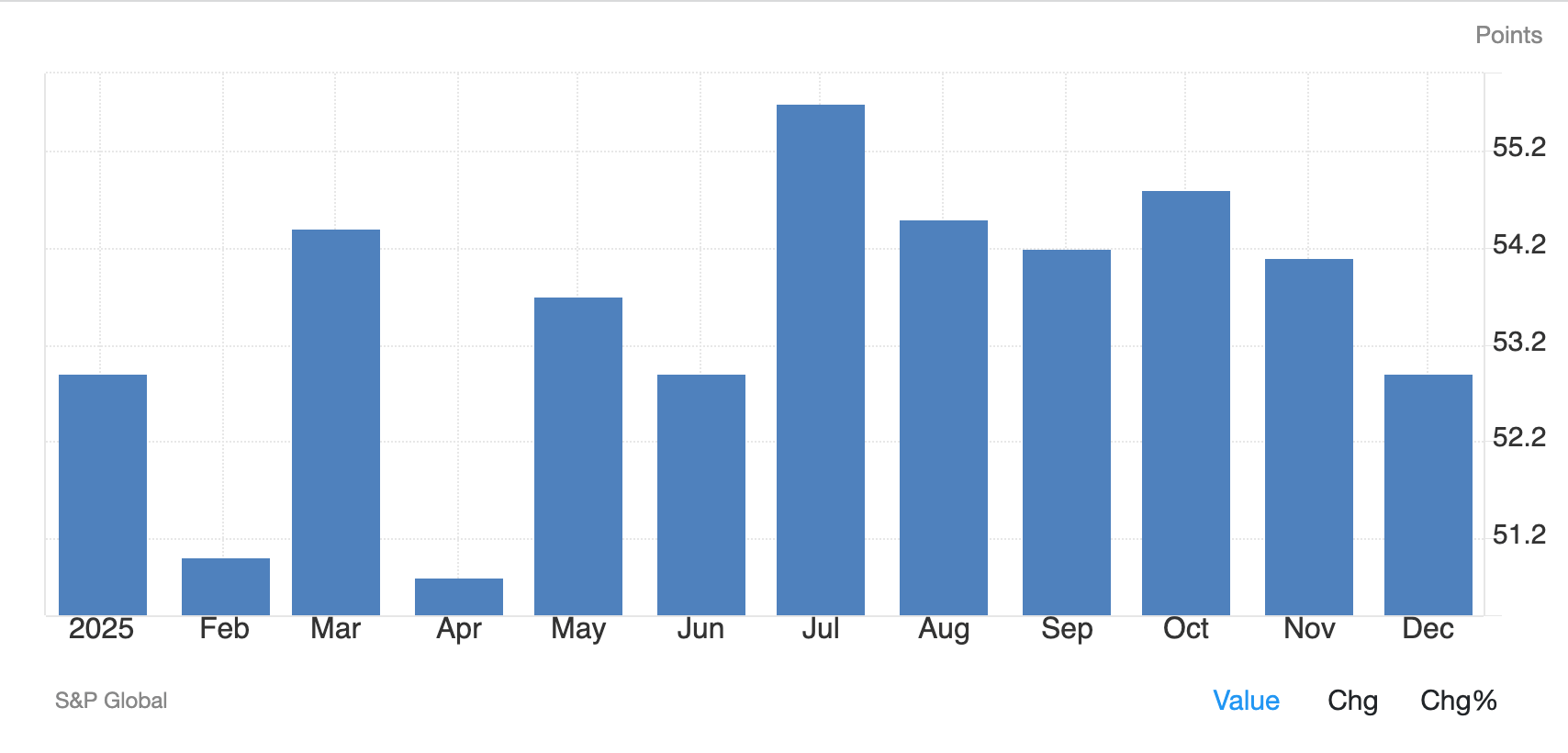

The Services PMI continues to grow (above 50), but at a reduced rate over the past three months. This screw is still tight enough, but getting looser (chart below).

Tradingeconomics

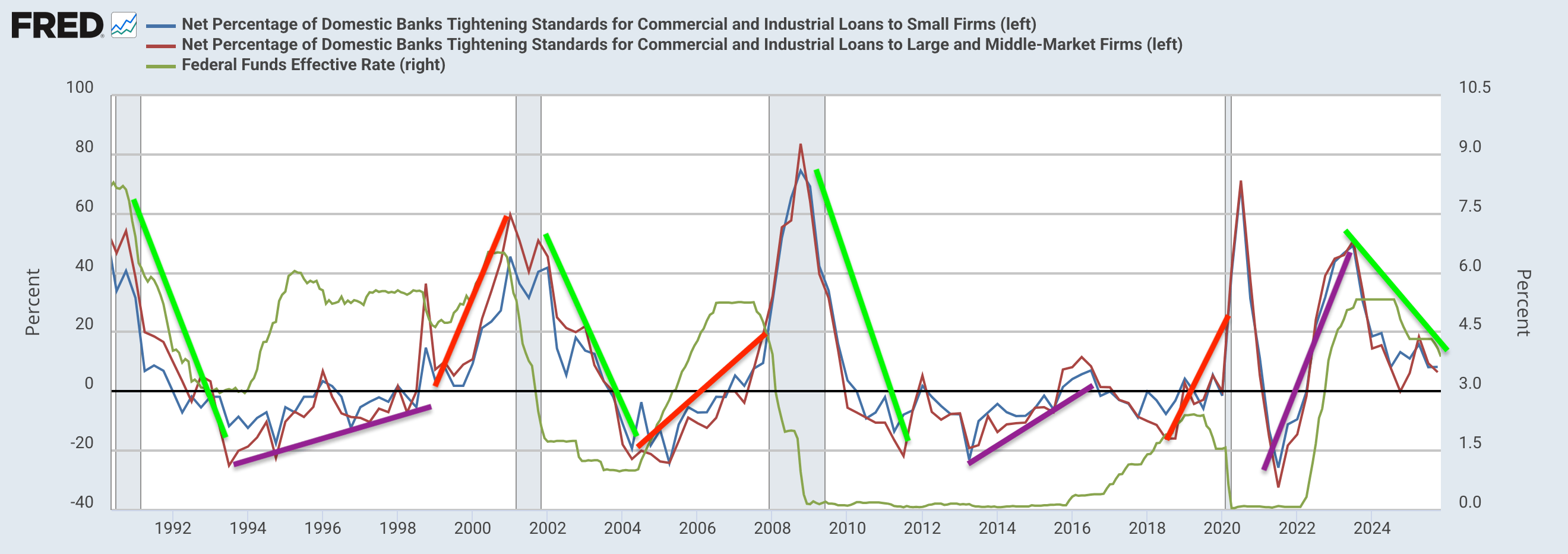

Banks tightening lending-standards always precedes recessions (red-lines below), but tightening lending-standards does not always lead to recessions (purple-lines below); e.g., 1994-1999 and 2014-2016, and 2021-2022. Lending-standards continue to be relaxed (green-line below). This screw is tight.

FRED

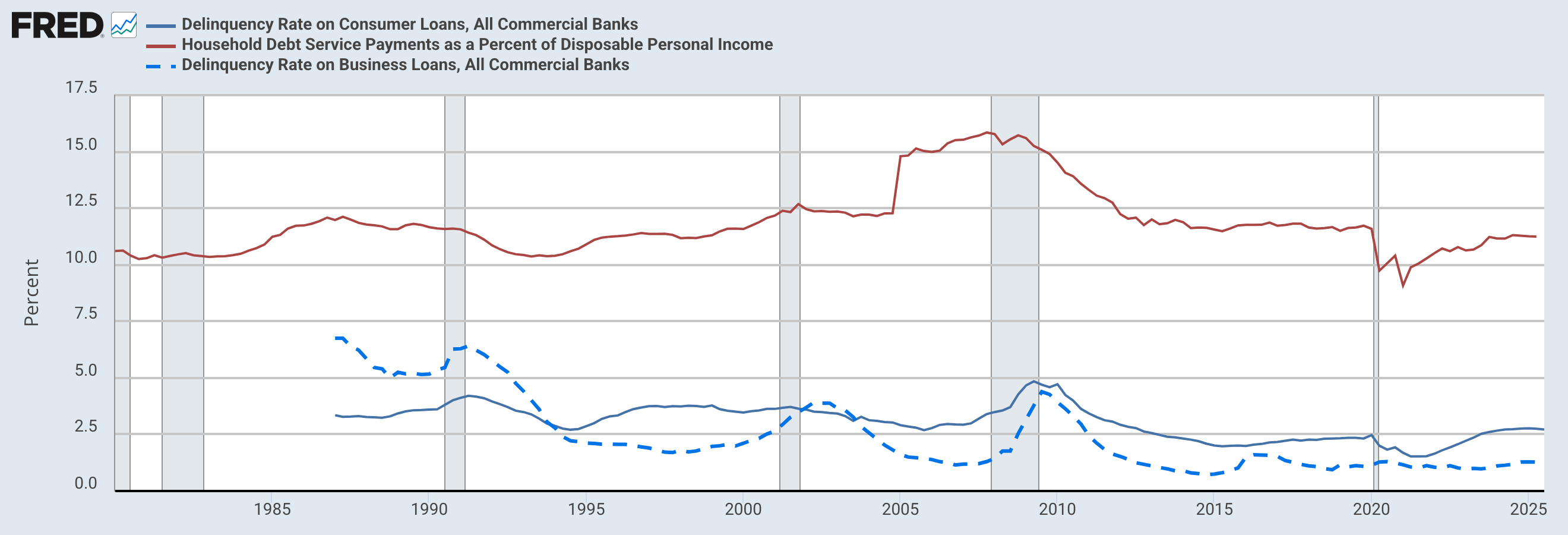

Recessions occur when loan delinquency-rates are rising, and when Household debt service as a percent of disposable income becomes elevated. Currently, both measures are just above historically low levels. This screw is tight.

FRED

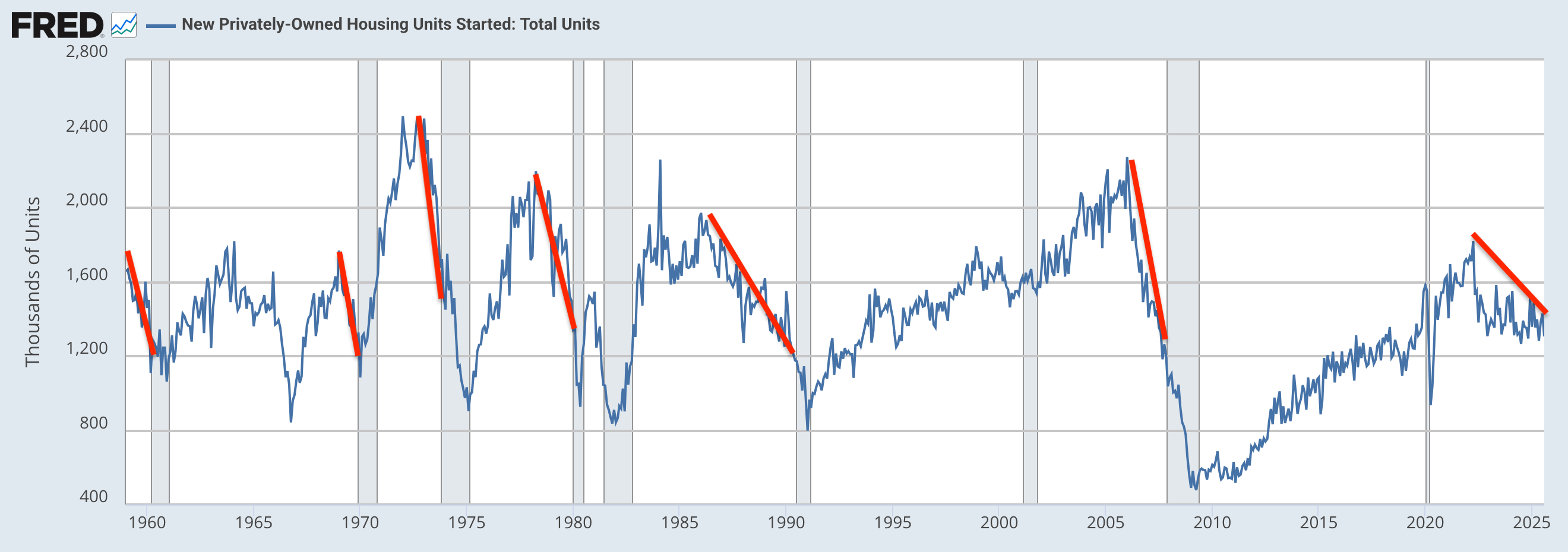

Recessions are always preceded by at least two-years of falling housing starts. Housing starts have been falling since 2022. This screw is loose.

fred

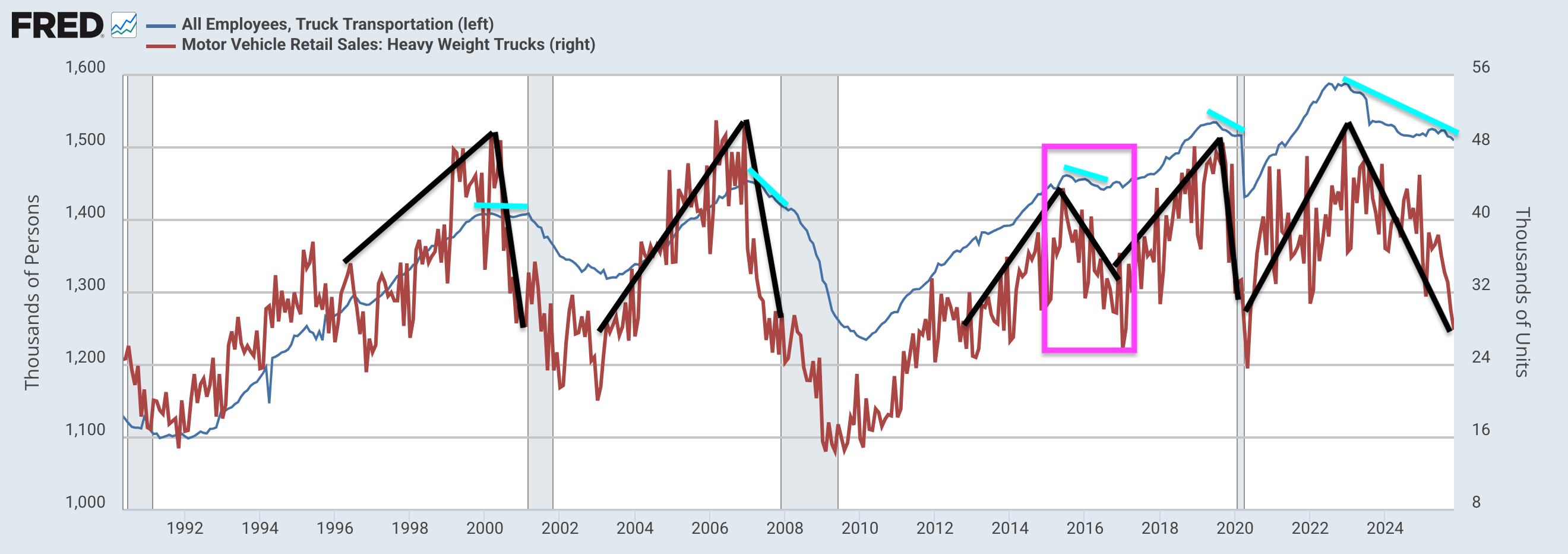

Truck transport employment (blue-line below) stops growing or declines, and heavy truck sales (red-line) collapse for more than a year ahead of recessions — the exception being 2015-2017 (pink-rectangle below). Truck transport employment has come down from the all-time highs of 2023 (blue-highlight) and truck sales have dropped below the up-trend line (black). This is a dangerously loose economic screw.

FRED

Corporate profits tend to decline (red), sometimes for years, ahead of recessions. Profits continue to rise from the pandemic lows. This is a tight screw.

FRED

The Most Important Screw of All

Money drives both the economy and the stock market, but most people simply do not understand what money is or where it comes from.

Money can be anything that we agree is capable of releasing real-resources, like labor and materials. It is not a physical entity, and today's money is not fixed to anything physical; Richard Nixon took the US dollar off the gold-standard in 1971. The US dollar is created by Congressional spending-laws, and is destroyed by taxation: by the way, taxation is what forces everyone in the US to use the US dollar as currency. Taxpayers need to earn US dollars before they can pay their taxes. Taxpayers cannot create US dollars — that would be counterfeiting. All US dollars are created by Government spending. The Federal Government is "self-funding."

Net spending is the difference between nominal-spending and taxation. If the Government spends (creates) more US dollars than it taxes back, then we say it has a deficit; it has deposited more money in private bank accounts than it has taxed back.

Government deficit = private surplus

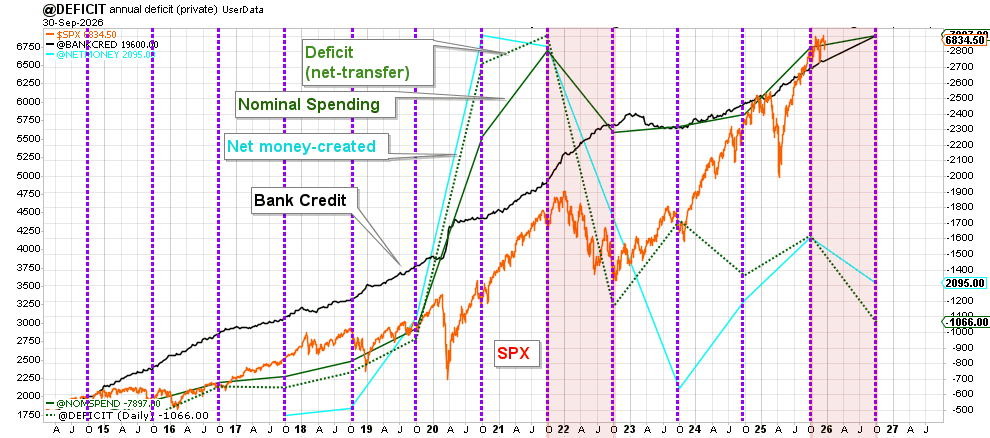

Government deficits correlate positively with the SPX (chart below). This makes sense, since bigger economies (and higher stock markets) require more money in the system.

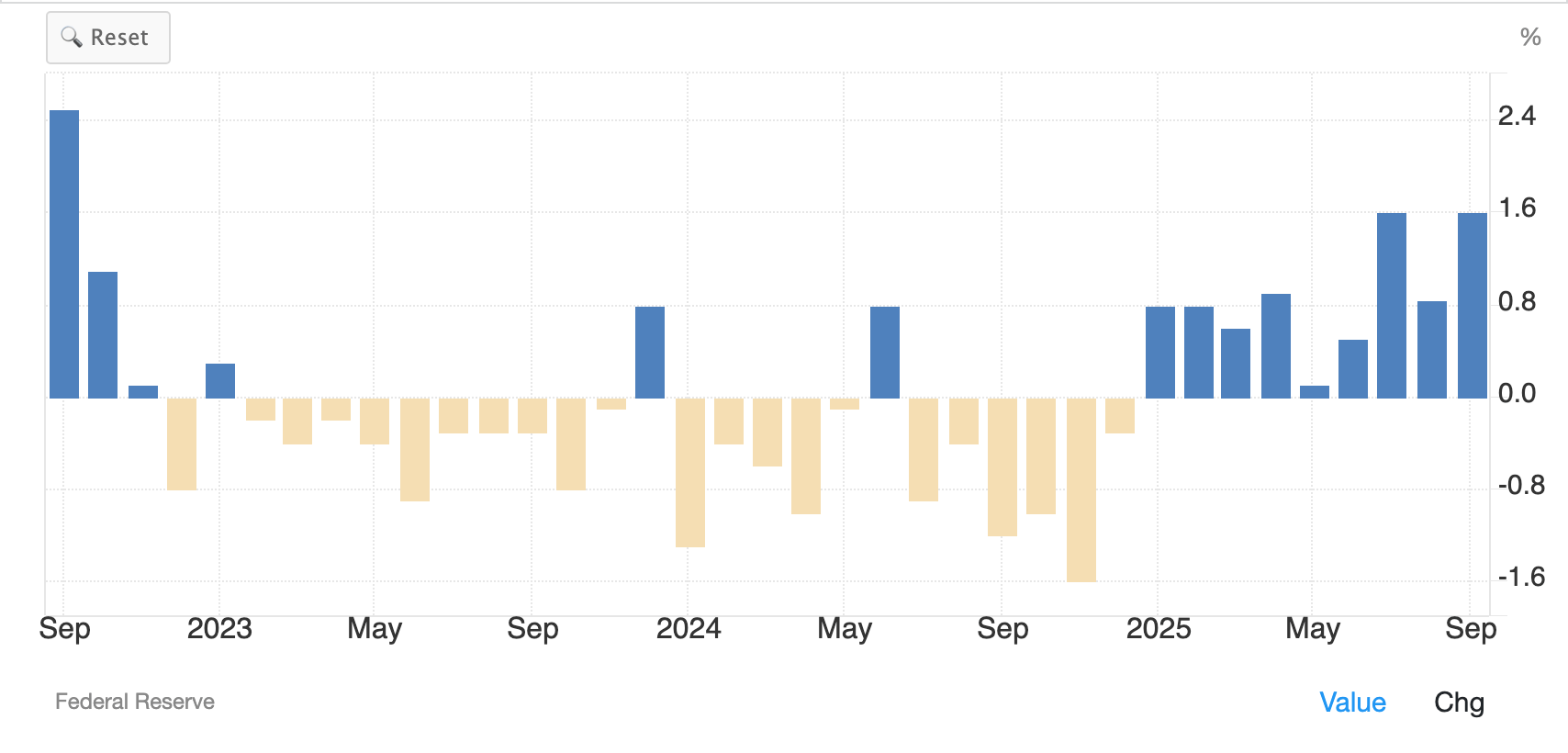

So far, the fiscal-2026 (started October 1, 2025) annualized run-rates of the deficit and of the net money-creation (which includes bank credit creation) are lower than in any year since 2022 (chart below).

This is a loose screw, but it is still early in the fiscal-year and the BBB takes effect in the new calendar-year with a potential $5T increase to the money supply (by way of tax-cuts), and if the tariff taxes are stopped or (better yet) refunded, then the improved fund-flows would tighten the "deficit-spending screw" which would support the economy and the stock market.

ANG Traders, stockcharts.com

In conclusion, 60% of the economic screws are tight, and as long as the BBB's tax-cuts take effect in January, many of the loose screws will tighten — starting with net money-creation — making a recession in the next 6-12 months unlikely. However, if the deficit and net money-creation continue to slow, then the economy and the stock market will stall and recession and a bear market become more likely.

Investors can stay long the stock market through technology ETFs such as SOXX, AIQ and XT, as well as broad spectrum ETFs such as SPY and QQQ.