chameleonseye/iStock Editorial via Getty Images

PayPal: 2025 Looks Like Another One To Forget

It's truly a year to forget for long-suffering investors of PayPal Holdings, Inc. (PYPL). The recovery in 2024 proved to be short-lived, as investors reassessed whether they could have been too ambitious with the valuation re-rating in PYPL, given the transformative changes that are undergoing in the fintech and payments marketplace.

It already had much to deal with, as it wrangles with the increasing slate of competitors vying for market share. These rivals run the gamut, ranging from big tech with walled garden credentials like Apple (AAPL), to encroaching e-commerce rivals seeing payments as a natural extension to their market expansion, such as Amazon (AMZN) and Shopify (SHOP).

And then we have core marketplace rivals such as Klarna, and Stripe, as they battle for market leadership. PayPal notched a relatively constructive growth in BNPL in the third quarter (+20% upside in BNPL TPV). Yet, it remains to be seen whether margin optimization in PayPal's earnings could be enough to help rein in the industry headwinds that have finally decoupled PYPL's confident ascent back in 2024, in contrast to the malaise that investors have had to manage this year, with the stock down >30% over the past year.

Back in October, I kept my faith in PYPL stock, thinking that the relative undervaluation was a disconnect and that the market had taken PYPL's fall way too far. I couldn't quite fathom why the market turned so drastically against the fintech leader's recovery in 2025, even as the overall market has continued to print new highs. However, it appears that these investors could have gotten it right on point here, following the recent conference that PayPal partook in, as CFO & COO Jamie Miller unveiled some worrying signs about the current state of consumer spending and sentiments.

PayPal: Consumer Headwinds Increasingly Somber

PayPal will look to invest "1 to 2 points of transaction margin dollars back" into the business, as it seeks to effectuate more robust consumer adoption and what it terms "habituation." I think this is something that could have surprised investors who have keenly followed PYPL's thesis for a while. Why?

Isn't PayPal a solid enough household name that it should have used 2024 to consolidate and then capitalized on 2025 as a year of revival to wind down those less profitable setups? Yet, management's commentary indicates that we might have to wait till 2026 or even longer, plausibly to ascertain whether the recovery is still panning out as anticipated? No good....clarity is now more murky, and investors are made to wait longer for the turnaround thesis.

Next, PayPal highlighted that stress sensors on consumer spending are starting to bite, one that I acknowledge that I should have paid more attention to. Such a cagey commentary amid what seems like a robust Black Friday shopping weekend suggests that PayPal's exposure to the lower and middle income could set back its outlook for 2026 when the company reports Q4 earnings early next year.

Management enunciated that the cautionary signals have led to a clear trend in "lower average order value," which has also impacted the accretion in its core branded checkout prospects. The discrepancy between the less affluent consumers and their wealthier peers has also led to fears about the "affordability crisis," and whether it could lead to adverse political ramifications when the midterms come into play next year.

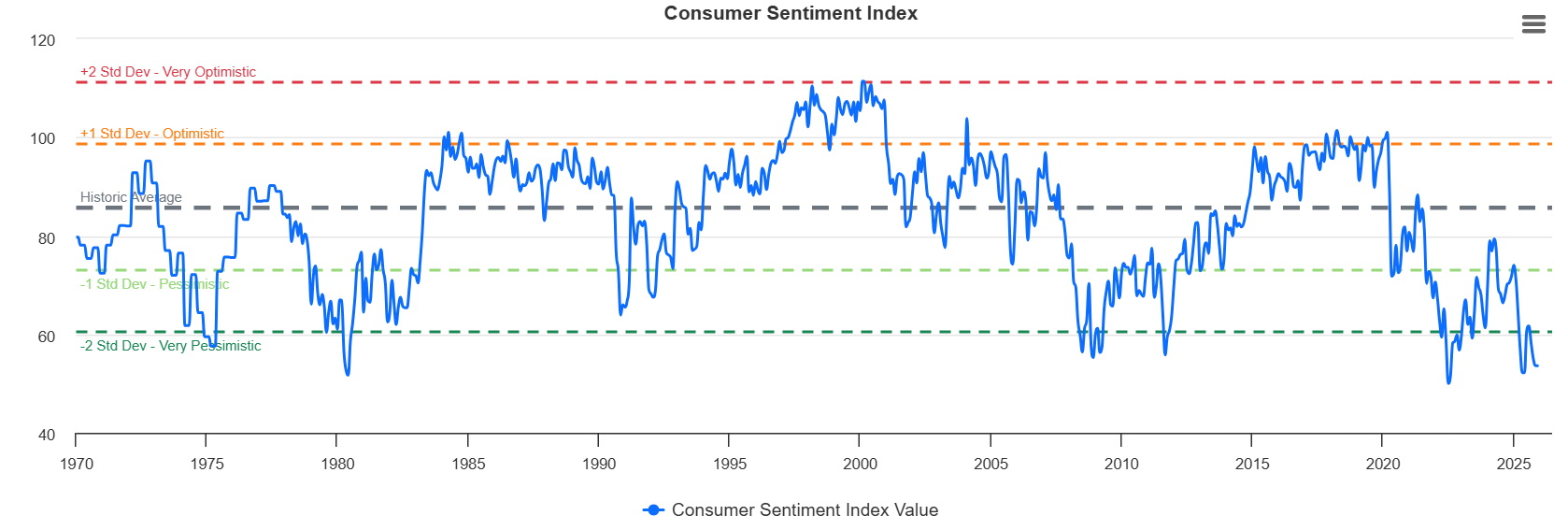

Consumer sentiment index (Current market valuation)

While these conjectures remain speculative, there is nothing along the lines of guesswork here when we take into account the clear pessimism reflected in the gloomy looking consumer sentiments index, printing levels that have deviated close to historic lows away from the long-term average. And with recent jobs reports not looking exactly sanguine, PayPal's business impact could linger on longer through 2026, even though a hard landing isn't my base case at the moment.

PayPal: Yet, Fundamentals Stay Robust And Resolute

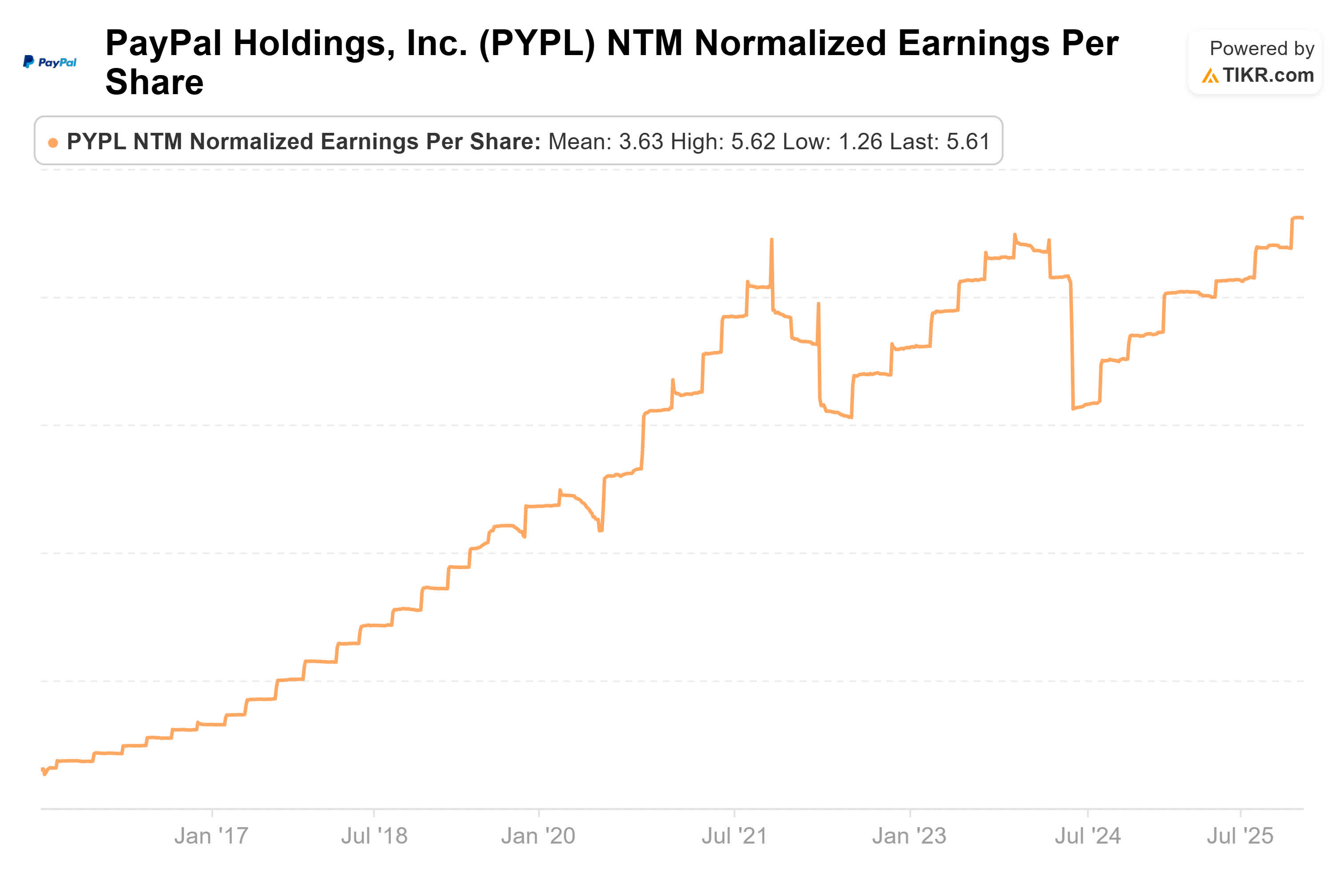

PayPal estimates (TIKR)

Yet, the salient question that I thought investors should ask is whether PayPal's earnings profile is going to slide down to new lows. From what I had gathered from PayPal's conference, it doesn't appear to be the case. Management highlighted its record in delivering robust free cash flow of $6B to $7B in the past couple of years, while having also declared a dividend back in Q3. Therefore, I thought PayPal's decision to invest more aggressively isn't predicated on weakness, but a show of strength in its underlying financials and the outlook through 2026.

Nevertheless, I'm not about to argue with the market and make the clarion call that the market is wrong. As investors/analysts, we should always maintain humility in our analysis and assessment, and try to glean useful insights from the market's perspective into PayPal's afflictions.

I think the market could be baking in more trouble brewing ahead for PayPal's consumer and merchant ecosystem, if the unemployment and jobs reports continue to flag increased risks, worsening the already torrid-looking consumer sentiment updates.

Yet, I think the silver lining here is that PayPal's robust FCF through 2027 (>$7.5B) provides credence to my narrative that these tough times shall pass, as long as the Fed plays ball through the end of 2026. With the current National Economic Council Director Kevin Hassett lining up as the hot favorite to replace Jerome Powell as the next Fed chair, I think we can suggest that Hassett should be broadly aligned with Trump's penchant for lower interest rates.

I think the market will likely skew in favor of a less hawkish Fed than worrying about one where the Fed's independence could be eroded. The market has reasons to believe that the FOMC is beyond one man/woman's decision or proclivities, even though raised dissent could also send shockwaves through the market. Despite that, the market still expects the Fed to cut rates by >3x through the end of 2026, which could help provide some helpful scaffolding for the pessimistic consumer, as merchants prepare cautiously for the effects to percolate through their businesses next year.

Buy Or Sell PYPL Stock?

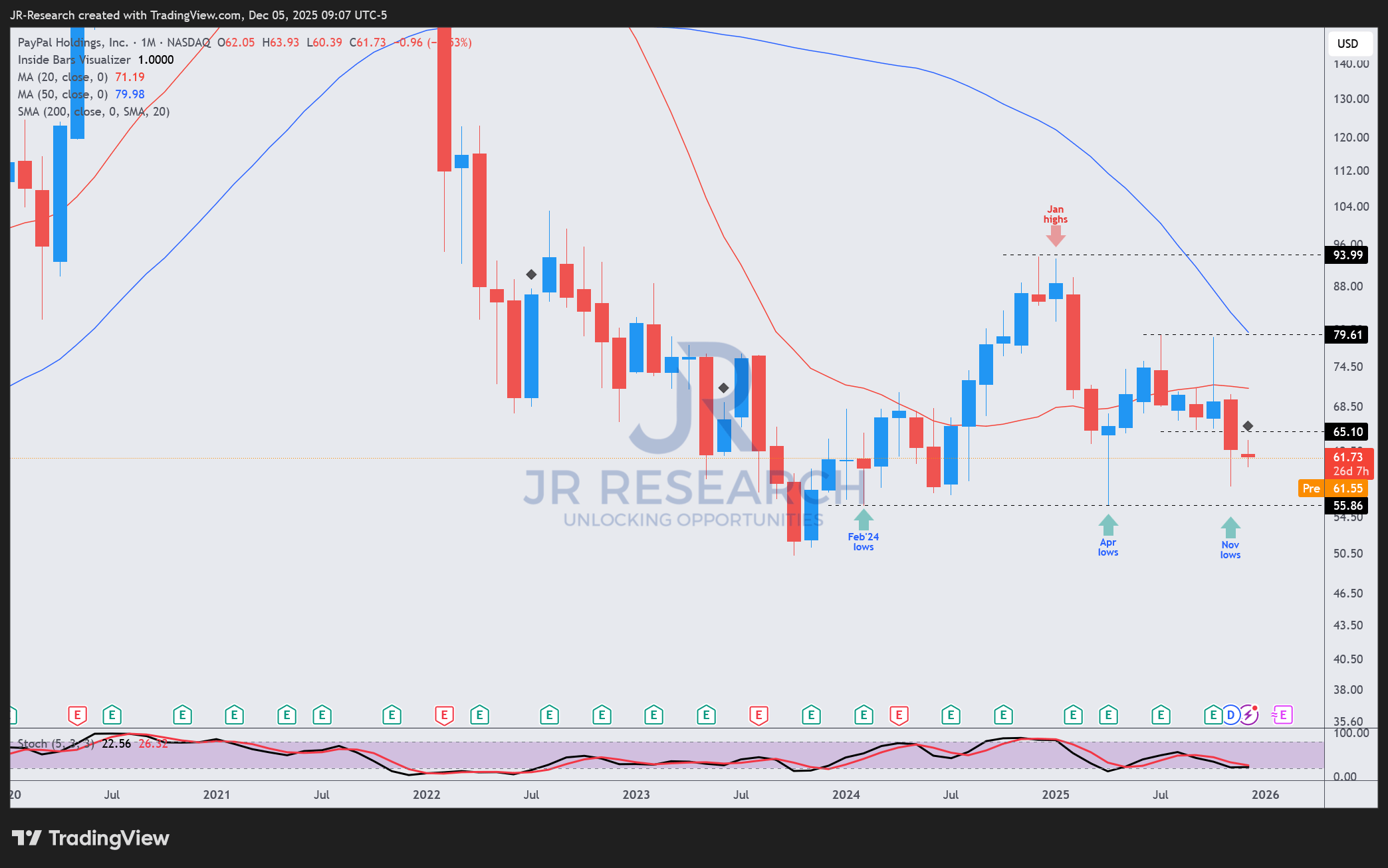

PYPL price chart (monthly, long-term) (TradingView)

If we dissect the buying sentiments in PYPL's long-term chart, I believe it's sufficient for me to say that while the underperformance has been somewhat frustrating, there's a robust support level over the $55 zone. It's noteworthy that the level has held resoundingly since early 2024, although little did I expect the market to make a round trip back close to those levels through November 2025.

However, if we take into account the fact that PYPL's forward earnings multiple of 11x is even lower than the financial sector's (XLF) forward P/E of 16x, has the market turned too downcast for its own good? PayPal is still printing 438M active accounts as of Q3, augmenting my narrative that its sticky ecosystem isn't showing glaring signs of falling apart. It has also rounded up the less profitable businesses in unbranded, and charted a more aggressive path in its core branded opportunities.

While the recent partnerships in Agentic commerce with Perplexity and OpenAI may not yet yield clear results in the near term, they also show that PayPal is acting quickly to seize the initiatives with the leading LLM companies, while walled garden peers like Amazon dither in favor of their in-house tech.

PayPal's ecosystem could be further diversified, as it attempts to bridge the gaps of its relatively stagnant active accounts base (but still sticky) with the rapidly growing 800M+ active users that OpenAI reportedly accrued.

Therefore, I believe dip buyers should be looking to return more favorably as it inches closer to that $55 support level, after realizing that such steep pessimism doesn't seem justified after all. Of course, a worse consumer outlook through 2026 could set investors back further, but it's not as if the current sentiments aren't bad enough already, skewing the risk/reward in favor of a reversal from here.

Rating: Maintain Buy.