Maks_Lab/iStock via Getty Images

Credo Technology Group Holding Ltd (CRDO) has kept soaring since early July 2025 despite my previous bearish call that cited significant overvaluation. It was a strong 70% rally, partially fueled by AI-related FOMO but also due to aggressive upward EPS revisions over the last few months. I have to give credit to the management because their track record of capitalizing on the data center boom is impressive. The AI momentum is also strong with a few large new AI infrastructure projects announced just recently. However, valuation analysis says that expectations are too high. I think that CRDO is likely to deliver strong earnings next week. However, this earnings season showed us that even Nvidia did not rally after its stellar past quarter's performance. I do not want to bet against the AI momentum again, meaning that waiting on the sidelines with a "Hold" rating is a prudent approach.

FQ2 2026 earnings preview

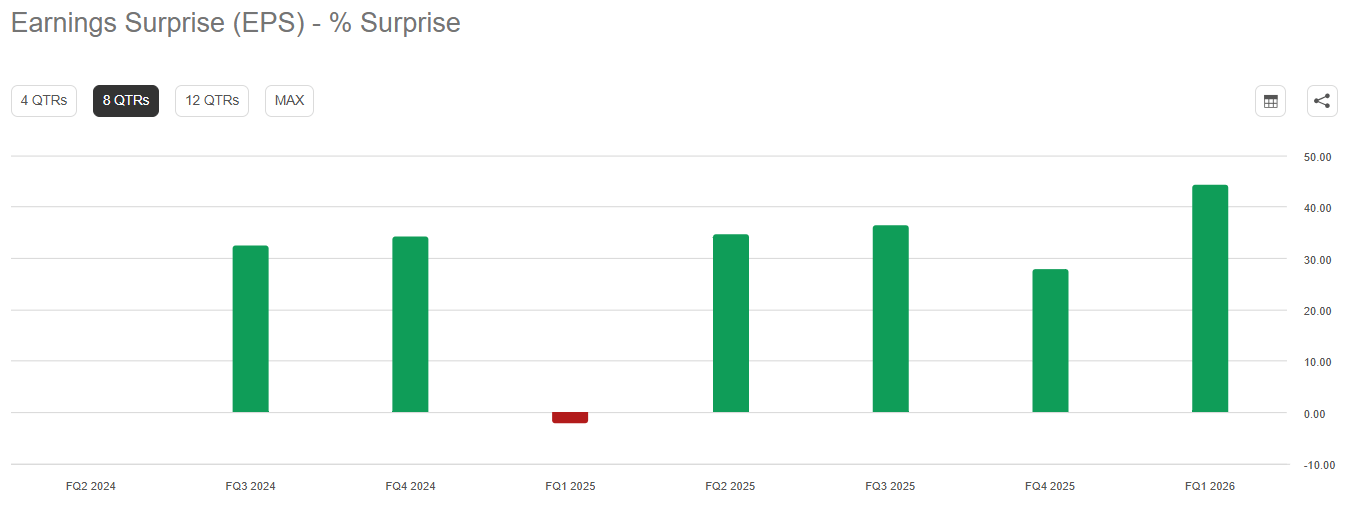

Credo releases its FQ2 2026 earnings on December 1st. The company does not have a very long earnings surprise record, but even with a relatively small sample there are some useful takeaways. The management is usually quite conservative in the EPS estimates because six out of eight last earnings releases were marked with 25%+ positive EPS surprises. Revenue surprises were also mostly wide over the same period. A company that can deliver large EPS and revenue surprises usually deserves strong investors' confidence, which is always good before the earnings release.

Seeking Alpha

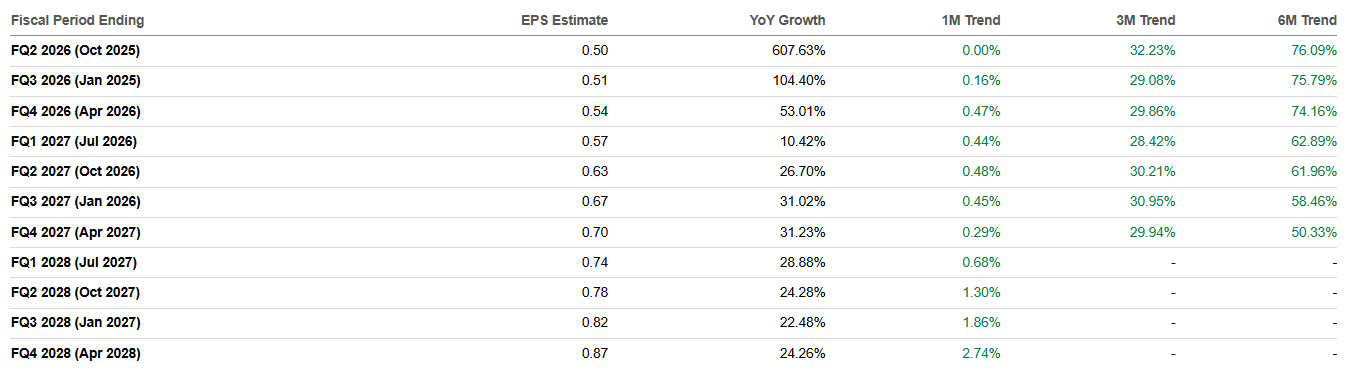

Besides investors' confidence, CRDO also has confidence in Wall Street analysts before the upcoming earnings release. Earnings revisions were all double-digit upgrades over the last three months, which is not only for FQ2 2026 but for several quarters ahead as well. The most impressive part is that CRDO's EPS is expected to soar by triple-digit percentages for two quarters in a row. The fact that CRDO's revenue and EPS are expected to maintain double-digit growth over the next several quarters indicates Wall Street's confidence in the company's ability to capitalize on the data center boom.

Seeking Alpha

And I have to say that Wall Street's confidence in Credo's ability to capitalize on AI tailwinds is not from thin air. CRDO has been absolutely brilliant in driving revenue growth over the last four quarters by accelerating YoY growth from 64% in FQ2 2025 to staggering 274% in FQ1 2026. The best part for investors here is that it was not just growth at all costs but profitable growth. The operating leverage is certainly there with the operating margin improving from -11.7% to 27.2% between the aforementioned quarters.

Seeking Alpha

Furthermore, despite revenue soaring by 64% YoY in FQ2 2025, for the upcoming earnings release a 226% YoY revenue growth is projected. It is impressive because usually it is difficult to accelerate growth that much when the comparative number has already spiked. As we know from the previous earnings call, Credo's ability to capitalize on AI tailwinds is mostly due to the active cable [AEC] product line, which is in high demand for data centers. The recent licensing agreement with the Siemon Company regarding AEC patents looks promising because it solidifies the value and proprietary nature of this technology. Among the positives for CRDO are also broader market recognition and potential for increased market penetration. With these favorable factors emerging as a result of the licensing agreement deal, I think that Credo's ability to capitalize on AI tailwinds has strengthened.

Industry-wise, the last few days confirmed that the most notable AI players are still aggressive in their AI infrastructure expansion plans. For example, Amazon is considering investing another $15 billion in a new data center-related project in Northern Indiana. Elon Musk's xAI is expected to close the new $15 billion funding round soon with the proceeds expected to be allocated in AI hardware as well. Developer of another popular LLM, Anthropic, also has ambitious plans to increase its computing capacity in the foreseeable future. Therefore, AI tailwinds are still strong, and I expect it to positively affect CRDO's revenue guidance for the full FY2026.

Besides headline numbers, I would also recommend investors pay attention to the key profitability ratios dynamic. As I mentioned before, gross and operating margins were expanding quite aggressively over the last few quarters. If CRDO continues demonstrating expansion of these metrics in FQ2 2026, it will highly likely add more confidence to investors. However, if there are signs that margins are not expanding or expanding slowly, it might be a warning sign indicating that CRDO's business model has achieved its full operating leverage potential. Margin dynamics is also crucial in terms of Credo's cash flow generating capacity because any business faces a moment when organic growth slows down, and having strong cash generating capacity is crucial to accumulate a strong financial position that can be potentially utilized for prospective M&A.

Overvaluation offsets fundamental brilliance

CRDO rallied by around 230% over the last twelve months and by 130% year-to-date. CRDO bulls enjoy strong momentum, which is always a bullish factor. However, there is always a very subtle line between healthy optimism and overly high expectations. When I look at Credo's valuation ratios, I think that we are more in the "overly high expectations" area.

Seeking Alpha

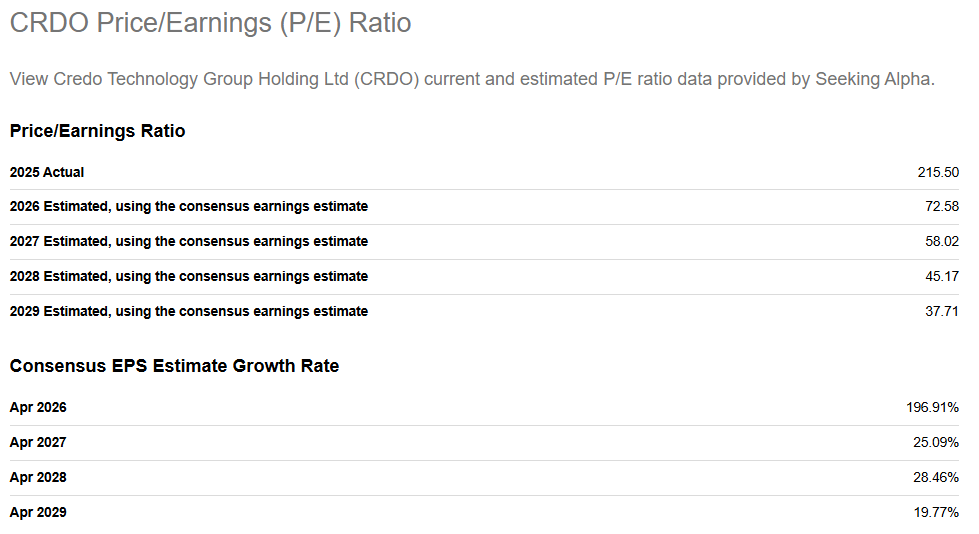

Of course, with CRDO's aggressive revenue and EPS growth, high TTM and 1Y forward multiples are perfectly fine. Since the calendar Q3 earnings season revealed that tech giants are willing to invest more in AI infrastructure during calendar year 2026, CRDO's elevated FY2027 forward P/E ratio estimate of 58 is also fine. However, the EPS growth rate is expected to moderate as the rule of large numbers will start working against Credo given that the numbers were soaring over the last several quarters. It is just the basic math suggesting that it is far easier to deliver EPS growth when the comparative EPS is just a few cents [like in FY2024]. But because quarterly EPS numbers are expected to grow aggressively over the next few quarters, the comparatives will grow around tenfold in FY2027 compared to FY2024 levels.

Furthermore, the financial strength of tech giants is not infinite and it is highly uncertain whether they will continue ramping up data center investments after calendar 2026. I think that the forward FY2028 P/E ratio estimate of 46 reflects that data center buildout will continue growing aggressively dollar-wise, which is an extremely risky bet. These expectations are highly likely mostly linked to optimistic expectations around the global data center spending spree because CRDO is a pure AI play at the moment as the company's business mix is mostly concentrated in generating revenues from data centers. Thus, CRDO's growth potential significantly depends on the strength of data center tailwinds.

Finally, last week Nvidia released stellar Q3 earnings with wide revenue and EPS beats and quite aggressive guidance. Nevertheless, the market cap of the world's largest company declined slightly over the last week. That might indicate that AI-related optimism is near peak levels at the moment.

Factors against upgrading

Actually, given Nvidia's weak share price performance after the earnings release might mean that I should better stick to the bearish rating. I am upgrading the rating to a "Hold" because CRDO's revenue growth keeps accelerating aggressively. However, there is no guarantee that Mr. Market expects Credo's revenue to accelerate even faster. Moreover, with extremely high valuation ratios like CRDO has, even a double-beat against consensus estimates does not guarantee that the stock will avoid a post-earnings sell-off.

The post-earnings sell-off risks are also high because of the massive rally CRDO delivered over the last twelve months. A 230%+ capital gain for the ones who bought last November might be too tempting to miss out on such an opportunity to book large profits.

Seeking Alpha

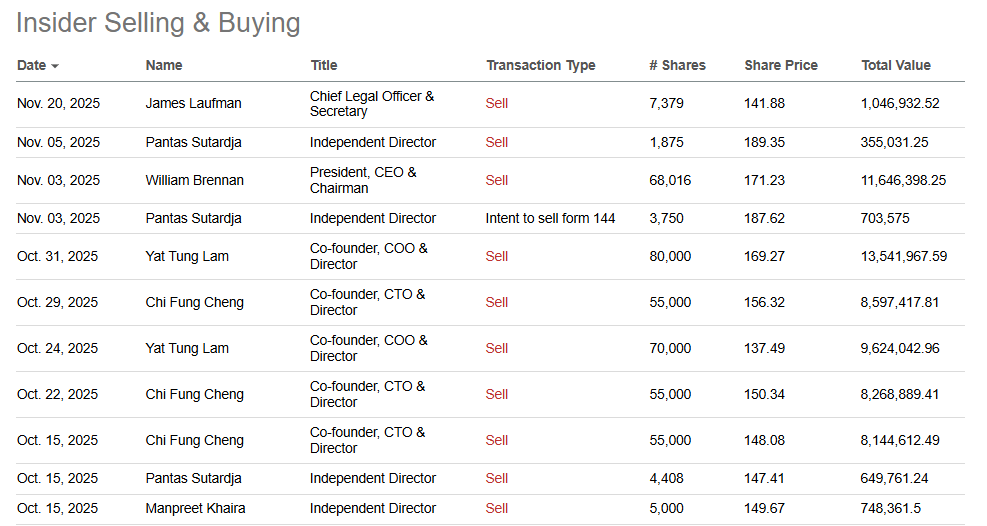

Moreover, insiders have been selling quite actively in October and November, which is another warning sign before the upcoming earnings release. Active insider selling is particularly warning in CRDO's case because it is not a company that has aggressive stock-based compensation, which means that insiders are not getting many shares as remuneration.

Bottom line

To conclude, I am upgrading CRDO to a "Hold". Betting against accelerating revenue growth amid AI momentum was a big mistake last time. The company's fundamentals are strong, and it can capitalize on the data center boom as well. However, I think that aggressive insider selling and generous valuation offset all the positives.