In a report released today, Peter Lawson from Barclays maintained a Buy rating on Geron, with a price target of $4.00. The company’s shares opened today at $1.26.

Elevate Your Investing Strategy:

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Lawson covers the Healthcare sector, focusing on stocks such as Revolution Medicines, Nuvalent, and Arcus Biosciences. According to TipRanks, Lawson has an average return of 0.9% and a 45.16% success rate on recommended stocks.

The word on The Street in general, suggests a Moderate Buy analyst consensus rating for Geron with a $3.50 average price target, representing a 177.78% upside. In a report released on October 23, TD Cowen also maintained a Buy rating on the stock with a $4.00 price target.

Novo Nordisk has made a new offer to buy the obesity-focused biotech company Metsera, which Metsera now says is better than Pfizer’s updated bid.

Shares of Novo Nordisk NVO -1.49% ▼ are down after the Danish drug maker made a new offer to buy the obesity-focused biotech company Metsera MTSR +20.20% ▲ , which Metsera now says is better than Pfizer’s PFE -1.26% ▼ updated bid. In fact, Novo’s proposal values Metsera at up to $86.20 per share, or about $10 billion in total. That’s a 159% increase from Metsera’s stock price on September 19, right before Pharmaceutical firm Pfizer first made its offer. In comparison, Pfizer’s new bid values Metsera at $70 per share, which totals around $8.1 billion.

Elevate Your Investing Strategy:

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

According to their original deal, Pfizer now has two business days to make changes to its offer, or Metsera can cancel the agreement and accept Novo’s. However, Pfizer CEO Albert Bourla said that Novo’s offer breaks antitrust laws and likely won’t happen. Therefore, it doesn’t count as a better deal under the current agreement. Unsurprisingly, Novo disagrees and stated that the bid fully follows the law. More specifically, it believes that buying Metsera will help patients and shareholders by expanding its drug portfolio.

As a result, Pfizer has filed a second lawsuit against Novo and Metsera, accusing Novo of using unfair tactics to block Pfizer from buying the company. This battle shows just how important weight loss and diabetes drugs have become. Metsera, which is developing both oral and injectable treatments, is seen by Pfizer as a way to finally enter this fast-growing market after years of setbacks. Meanwhile, Novo Nordisk, a pioneer in the space, sees Metsera as a way to defend its position after losing ground to Eli Lilly LLY +0.24% ▲ and cheaper competitors.

Tesla plans a means to gift Full Self-Driving access, and faces the potential of a road surface that works like a Supercharger station.

Electric vehicle giant Tesla TSLA -4.10% ▼ knows that holiday shopping can be difficult. Even with all the alternatives we have these days, picking just the right present can be a tall order. But it has an idea, especially if you know a Tesla owner. This year, why not give the gift of Full Self-Driving (FSD)? The idea did not sit well with investors at all, and shares skidded down nearly 4% in Tuesday afternoon’s trading.

Elevate Your Investing Strategy:

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The idea is simple enough. Normally, FSD access comes with a subscription, or a hefty one-time payment. But now, people can offer up free FSD access for a range of time frames as though it were a Hickory Farms gift basket. Word from Tesla notes that the company plans to start up the gifting program ahead of Christmas, which means those who want to get something special for a Tesla owner in their lives can do so readily.

Tesla already offered gift cards, which could have been used for FSD service. But this is much more specific. FSD service is available for $99 per month, or for a flat fee of $8,000. The $99 monthly rate is a substantial savings over the original price of $199 per month, though Tesla has warned in the past that the rate could rise, especially the closer FSD gets to a complete release.

Every Road is a Supercharger

Meanwhile, the idea of turning roads into wireless charging stations for electric cars is on the rise, and another stretch of road has been converted accordingly. Electreon, backed up by the Vinci Group, took its act on the road and electrified a roughly one-mile stretch of road, allowing cars to drive down said road and recharge as they drove.

Electreon previously brought such efforts to Detroit, but the Paris stretch is significantly more advanced, reports note. Regardless, the idea of being able to fuel a vehicle by driving it on a particular stretch of road instead of trying to find a charging station is a powerful one. It is also one many drivers will likely enjoy seeing, particularly if such tools see broader use.

Is Tesla a Buy, Hold or Sell?

Turning to Wall Street, analysts have a Hold consensus rating on TSLA stock based on 14 Buys, 10 Holds, and 10 Sells assigned in the past three months, as indicated by the graphic below. After an 86.28% rally in its share price over the past year, the average TSLA price target of $395.54 per share implies 12.08% downside risk.

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

That is quite a large move for Super Micro, a key player in the AI hardware boom. SMCI’s long-term average post-earnings move is -3.39%, which reflects a decline.

What to Watch in the Report

In SMCI’s upcoming report, investors will likely be watching for commentary on the timing of its $12 billion design win backlog and progress toward its ambitious full-year revenue guidance of at least $33 billion.

Also, traders will keep an eye on the company’s gross margins to see if they remain steady or face further pressure due to product mix or rising competition. Management’s commentary on margin trends in the upcoming quarters will be in focus.

Lastly, investors are watching for updates about the rollout of Super Micro’s new liquid-cooled systems and upgraded chips from Nvidia NVDA -3.14% ▼ and AMD AMD -2.51% ▼ . Slowing demand or rising competition in the AI server space could trigger volatility in the stock.

Analysts’ Expectations from SMCI’s Q1 Results

Wall Street is expecting SMCI to report earnings of $0.38 per share, down from $0.75 in the same period last year. Also, analysts project revenues of $5.83 billion, compared with $5.94 billion in the year-ago quarter.

It must be noted that last month, the company disclosed preliminary Q1 revenue of about $5 billion, below its initial $6 to $7 billion guidance and analysts’ consensus estimates.

Is SMCI a Good Stock to Buy?

On TipRanks, SMCI stock has a Hold consensus rating based on four Buys, seven Holds, and three Sells assigned in the past three months. Meanwhile, the average Super Micro Computer price target of $45.33 implies a 5.82% downside risk from current levels.

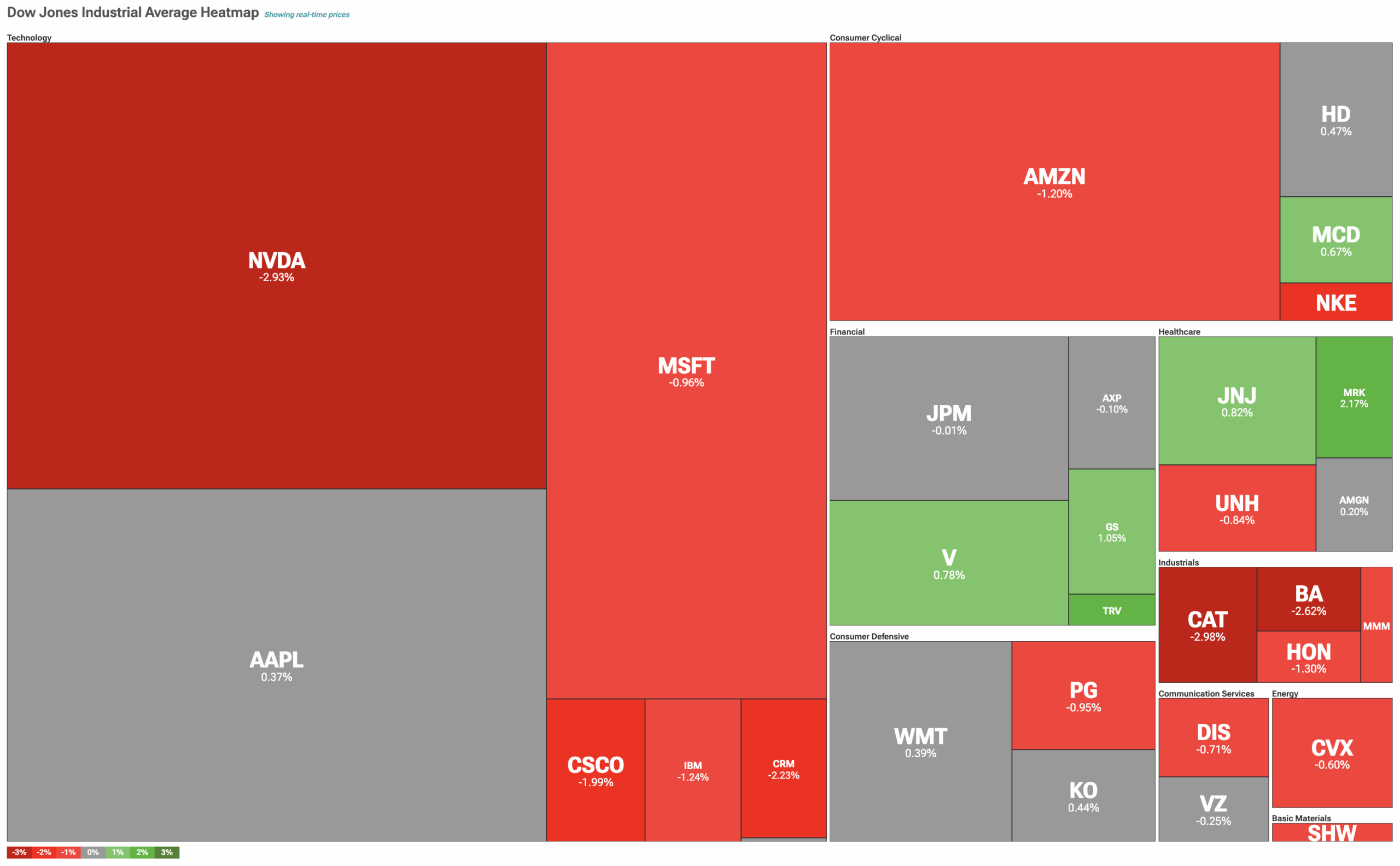

The Dow Jones (DJIA) is trading lower on Tuesday, led by losses in the tech sector amid growing concerns over elevated valuations.

Elevate Your Investing Strategy:

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Investors are also digesting warnings of a pullback from Goldman Sachs GS +0.99% ▲ CEO David Solomon and Morgan Stanley MS +0.66% ▲ CEO Ted Pick. “It’s likely there’ll be a 10% to 20% drawdown in equity markets sometime in the next 12 to 24 months,” Solomon said at the Global Financial Leaders’ Investment Summit in Hong Kong. At the same time, Solomon noted that drawdowns are normal during positive market cycles and that they allow investors to reassess their portfolios.

Speaking from the same summit, Pick said that investors should welcome a 10% to 15% drawdown as long as it isn’t “driven by some sort of macro-cliff effect.” He added that the market will place a greater emphasis on companies with strong earnings in 2026, resulting in “greater dispersion.”

Meanwhile, President Trump has called for an end to the filibuster rule as the government shutdown ties a record length of 35 days set in late 2018 and early 2019. “TERMINATE THE FILIBUSTER NOW, END THE RIDICULOUS SHUTDOWN IMMEDIATELY, AND THEN, MOST IMPORTANTLY, PASS EVERY WONDERFUL REPUBLICAN POLICY THAT WE HAVE DREAMT OF, FOR YEARS, BUT NEVER GOTTEN,” Trump said in a Truth Social post.

The filibuster is a Senate rule requiring most legislation to secure 60 out of 100 votes to pass, giving the minority party significant influence. Removing the filibuster would let bills pass with a simple majority in the Senate and could increase the likelihood of the government reopening. Republicans currently hold 53 seats in the Senate.

On prediction platform Polymarket, the odds of the shutdown extending to November 16 and beyond sit at 39%. The chances of the shutdown ending between November 8-11 and November 12-15 both hold odds of 22%.

The Dow Jones is down by 0.42% at the time of writing.

Which Stocks are Moving the Dow Jones?

Let’s pivot to TipRanks’ Dow Jones Heatmap, which illustrates the stocks that have contributed to the index’s price action.

Nvidia NVDA -3.10% ▼ is leading all tech stocks to the downside, despite Jefferies raising its NVDA price target to $240 from $220 on strong AI demand. That comes as hedge fund manager Michael Burry disclosed a short bet on the semiconductor leader. Salesforce CRM -2.31% ▼ and Cisco CSCO -2.10% ▼ are also trading lower.

Furthermore, all five industrial stocks are trading lower. Caterpillar CAT -3.11% ▼ is the worst hit, shrugging off a price target hike to $581 from $506 by UBS.

Elsewhere, Merck MRK +1.33% ▲ is in the green after the company announced $700 million in experimental cancer funding from Blackstone BX -0.91% ▼ . Amazon AMZN -1.40% ▼ is trading lower, although the e-commerce leader is still up by about 8% during the past week.

DIA Stock Moves Lower with the Dow Jones

The SPDR Dow Jones Industrial Average ETF DIA -0.59% ▼ is an exchange-traded fund designed to track the movement of the Dow Jones. As a result, DIA is falling alongside the Dow Jones today.

Wall Street believes that DIA stock has room to rise. During the past three months, analysts have issued an average DIA price target of $528.57, implying upside of 12.21% from current prices. The 32 holdings in DIA carry 30 buy ratings, two hold ratings, and zero sell ratings.

Stay ahead of macro events with our up-to-the-minute Economic Calendar — filter by impact, country, and more.

Wall Street expects DoorDash to top earnings per share and revenue in Q3 2025, even as they see its Deliveroo acquisition as a pipeline for future growth amid intensifying market competition.

Food delivery company DoorDash DASH +0.31% ▲ is preparing to reveal its third-quarter 2025 results tomorrow. Heading into the results release, Wall Street remains upbeat about DASH stock.

Elevate Your Investing Strategy:

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But what is expected from the company, which is seeking expansion through its $3.9 billion acquisition of British online food delivery company Deliveroo (GB:ROO)?

Analysts’ recent assessments on DASH stock provide clues about what Wall Street expects from DoorDash. For instance, Goldman Sachs analyst Eric Sheridan expects DoorDash’s acquisition of Deliveroo to fuel its future growth — although the acquisition is also anticipated to result in a short-term impact on DoorDash’s EBITDA margins.

Moreover, Sheridan anticipates that the total dollar value of all orders placed on DoorDash’s app will continue to exceed analysts’ estimates, like it has done in previous quarters.

Chipping in, UBS analyst Stephen Ju believes that DoorDash can continue to count on the demand for online food delivery that has persisted since the post-COVID-19 period. Ju also sees consumer demand for convenience further driving growth in the medium term.

It is important to note that DoorDash is not resting on its laurels. It is now testing driverless food delivery in partnership with Alphabet’s GOOGL -2.14% ▼ Waymo, the U.S. tech giant’s autonomous driving subsidiary.

Across Wall Street, analysts are currently bullish on DoorDash’s shares, with 26 Buys and eight Holds issued over the last three months. Consequently, DASH holds a Strong Buy consensus rating.

There is a distressing change in the air at Home Depot, both inside and out.

The aisles at home improvement giant Home Depot HD +0.63% ▲ , much like any other hardware store, have often felt laden with purpose. These are places where inspiration lives, as long as you have the cash, the talent, or some combination of both, to realize that potential. But these days, the sentiment is changing a bit, and Home Depot is working to understand this new feeling. Investors remain reasonably confident, as shares notched up fractionally in Tuesday afternoon’s trading.

Elevate Your Investing Strategy:

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Back in July, when Home Depot had its second quarterly earnings report, it noted that traffic in its stores was starting to drop. Granted, there was a gain in overall sales, but many regarded that as a function of higher prices than it was an increase in customers. The small drop in customer count was offset by the rise in prices.

And Home Depot has been fighting against the need to raise prices, working with suppliers and cutting expenses to try and hold the line. But some price bumps were likely inevitable, and the customer—already feeling tapped out after a simple grocery store run—is cutting back accordingly. A recent interest rate drop has helped, of course, but this tepid drop has so far proven little help. So Home Depot is left with rising prices, frightened customers, and a market that is looking increasingly inhospitable for all but the most basic of sales.

Protest After Protest After Protest

And then, a flood of protests fired up, with news out of several cities talking about rallies at Home Depot locations all over, you guessed it, illegal immigration. Multiple events fired up in the last few days, and all of these aimed at a combination of the federal government and Home Depot.

In East Lansing, protesters gathered for the “ICE Out of Home Depot” rally, which looked to “…honor immigrant workers who have been detained by ICE on Home Depot properties.” Pittsburgh saw a similar rally. And finally, Savannah, Georgia saw a rally as part of the “Disappeared in America Weekend of Action,” which focused on—you guessed it again—ICE raids at Home Depot locations.

Is Home Depot a Good Long-Term Buy?

Turning to Wall Street, analysts have a Strong Buy consensus rating on HD stock based on 19 Buys and six Holds assigned in the past three months, as indicated by the graphic below. After a 5.43% loss in its share price over the past year, the average HD price target of $446.30 per share implies 17.2% upside potential.

Anthropic, the AI startup backed by tech giants Amazon and Google, has significantly raised its growth forecasts.

Anthropic ANTPQ), the AI startup backed by tech giants Amazon AMZN -1.43% ▼ and Google GOOGL -2.14% ▼ , has significantly raised its growth forecasts. It now expects up to $70 billion in revenue by 2028, compared to just $5 billion this year, according to The Information. The company believes that businesses will drive this growth by using its AI models through APIs (Application Programming Interfaces). Anthropic even predicts that its API revenue in 2025 will be about twice as much as OpenAI’s.

Elevate Your Investing Strategy:

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Separately, the firm’s Claude Code tool is also growing fast, as it’s reaching nearly $1 billion in annualized revenue, up from $400 million in July. Overall, Anthropic’s revenue is expected to hit nearly $7 billion this year, with new forecasts indicating $15.2 billion in 2026 and $38.9 billion in 2027. Unlike OpenAI OPAIQ), which doesn’t expect to generate positive cash flow until 2030, Anthropic aims to turn profitable by 2027 with $3 billion in free cash flow, and possibly $17 billion in 2028.

OpenAI, in comparison, expects to burn through $35 billion in 2027 and nearly $47 billion in 2028, largely due to its high computing costs for research and development. In addition, Anthropic expects its gross profit margin to swing from -94% last year to 50% this year, and to 77% by 2028. However, if free users are included in the cost calculation (as OpenAI does), margins would be lower at -109% for last year, 47% for this year, and 75% by 2028. Even then, these numbers are close to top-performing software companies, which usually have margins above 70%.

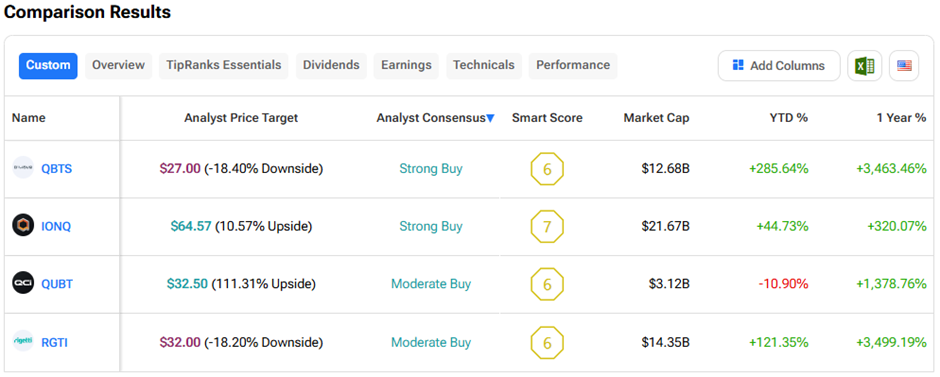

IONQ, RGTI, QBTS, and QUBT are trending lower after Canadian rival Xanadu announced plans for a Nasdaq listing.

Shares of American quantum computing firms, including IonQ Inc. IONQ -6.70% ▼ , Rigetti Computing RGTI -5.44% ▼ , D-Wave Quantum QBTS -6.10% ▼ , and Quantum Computing QUBT -9.14% ▼ , are trending lower after Canada’s Xanadu announced plans for a U.S. listing. Xanadu is a photonic quantum computing firm, which claims its technology offers several advantages over competitors.

Elevate Your Investing Strategy:

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Xanadu is planning to go public in early 2026 on the Nasdaq stock exchange via a $3.6 billion special purpose acquisition company (SPAC) deal after completing a merger with blank-check firm Crane Harbor Acquisition Corp. CHAC +2.65% ▲ . The company expects to raise nearly $500 million from the SPAC deal.

What Sets Xanadu Apart?

Xanadu is building quantum computers using light particles, called photons, to perform calculations. In contrast, IonQ uses trapped ions, while Rigetti relies on superconducting qubits that require extremely cold temperatures to maintain quantum states. On the other hand, D-Wave uses quantum annealing with superconducting qubits optimized for solving specific optimization problems, making its approach different from universal quantum computing.

Xanadu claims its photonics approach offers key advantages:

Operates at room temperature

Easier to manufacture

Flexible error correction

Modular design

Scalable through optical networking

Fast processing speeds

Compatibility with existing telecom systems

Xanadu’s quantum computer, called the X-Series, is the first photonic quantum computer accessible on the cloud. The company believes its technology can scale up to one million qubits by connecting multiple quantum systems using optical networking.

Furthermore, Xanadu has created error-resistant photonic qubits called GKP states directly on a chip. These qubits allow the system to correct its own errors, improving stability and reliability. This breakthrough brings quantum computing closer to practical, large-scale applications that can operate at room temperature.

Currently, Wall Street has assigned a “Strong Buy” consensus rating to D-Wave Quantum and IonQ, with IONQ offering greater upside potential of the two.

{kind=link}

{kind=link}