Tatyana Berkovich/iStock Editorial via Getty Images

Introduction

Philip Morris International Inc. (NYSE:PM), the company behind the leading cigarette alternative IQOS and the leading oral nicotine products ZYN, announced its results for the third quarter of 2025 today.

I last covered Philip Morris in July after the company released its second quarter results, explaining why the underlying fundamentals remain very strong and that the fairly significant decline in the share price following the release of the results was primarily due to previously exaggerated investor expectations. After all, even after the decline, PM shares were trading at a price-to-earnings ratio of around 23 and a free cash flow yield of less than 4%.

In this update, I will share my assessment of Philip Morris' recently concluded third quarter, focusing on earnings adjustments (see my critical analysis of PM's adjustments), the development of the cigarettes and the smoke-free business, and overall profitability.

Philip Morris Q3 2025: Delivering As Expected

Philip Morris International’s latest earnings report was solid, and I’m inclined to say, as usual, given the tendency to deliver adjusted EPS ahead of estimates. Quarterly EPS came in at $0.14, or almost 7%, above expectations.

Adjusted EPS growth was a robust 17.3% year-over-year, although it should be noted that the weaker U.S. dollar had a positive impact of 4.2 percentage points. Earnings adjustments excluding currency effects were insignificant, at only $0.01 per share. On a consolidated basis, Philip Morris reported operating profit adjustments of $517 million, representing approximately 12% of actual operating profit, and attributable to amortization of intangible assets and an excise tax-related litigation charge in Germany. The difference between the impact of the adjustments on operating income and net income (per share) is largely attributable to dividend income from a now deconsolidated affiliate (Rothmans, Benson & Hedges Inc. in Canada, RBH), tax items, and fair value adjustments of equity investments.

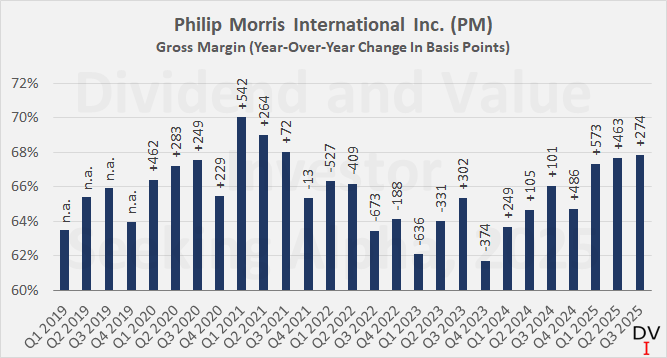

In terms of profitability, Philip Morris reported a further increase in gross profitability of 2.7 percentage points year-over-year to 67.8% (Figure 1). The sequential increase was much more moderate at only 18 basis points. The continued improvement is certainly encouraging, but I would say that, given the impacts from working capital movement, it makes more sense to review profitability after the full-year results are released early next year.

Figure 1: Philip Morris International Inc. (PM): Gross margin on a quarterly basis (own work, based on information from company filings)

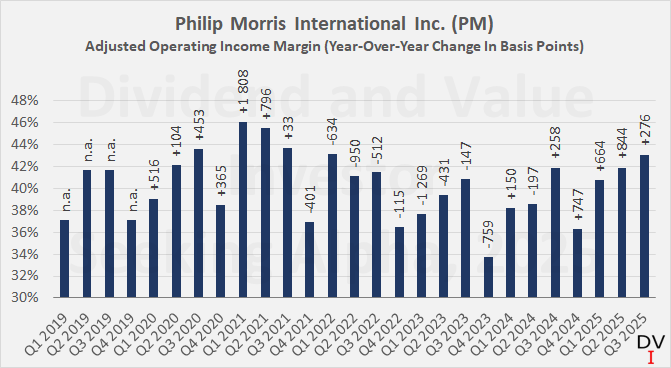

Adjusted operating profitability improved by 1.2 percentage points to 43.1% compared to both the previous quarter and Q3 of 2024 (Figure 2). Given the abovementioned adjustments affecting operating profitability, I maintain that Philip Morris' reported operating margin accurately reflects the company's underlying profitability.

Figure 2: Philip Morris International Inc. (PM): Adjusted operating margin on a quarterly basis (own work, based on information from company filings)

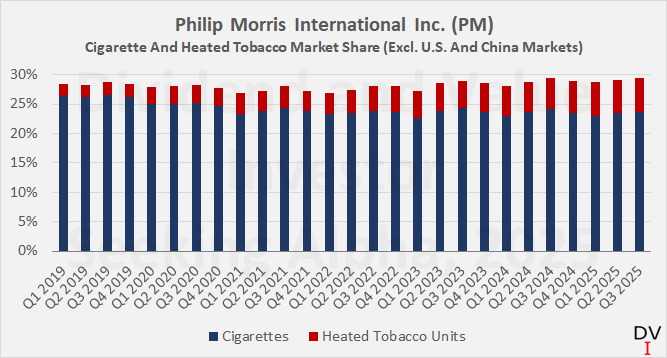

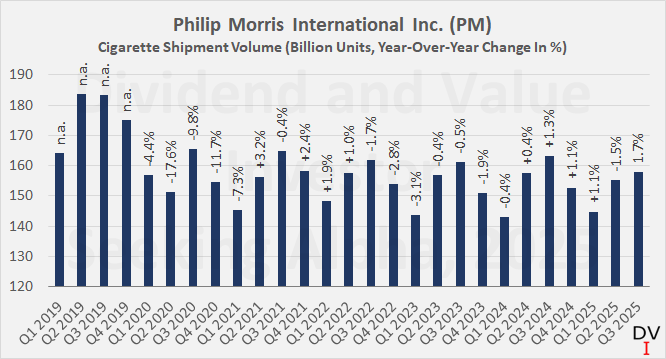

The business continues to perform as expected, and although traditional cigarettes are clearly not a focus for most Philip Morris investors, I still think it is worth noting that the company continues to maintain its market share despite pressure on consumers’ disposable income and the focus on premium brands (Figure 3, blue bars). Cigarette shipment volume declined 3.2% year-over-year but increased 1.7% quarter-over-quarter (Figure 4), outperforming its competitors, although I should add that a peer group comparison is difficult, if not impossible, due to their very different market presence.

Figure 3: Philip Morris International Inc. (PM): Cigarette and heated tobacco market share excluding U.S. and China on a quarterly basis (own work, based on information from company filings)

Figure 4: Philip Morris International Inc. (PM): Cigarette shipment volume on a quarterly basis (own work, based on information from company filings)

As shown in Figure 3 above (red bars), heated tobacco is naturally playing an increasingly important role, but the continued increase in market share (+10 basis points compared to the previous quarter, +50 basis points compared to the previous year, Figure 2, red bars) was largely expected.

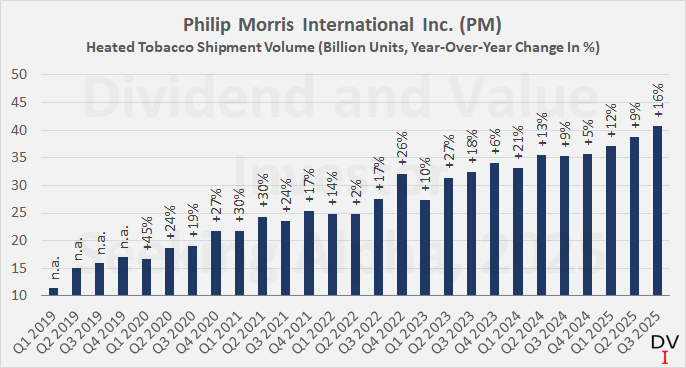

Combined with the decline in cigarette volume, Philip Morris estimates a 0.8% decline in industry volume. Given that heated tobacco is one of Philip Morris' growth drivers, this sounds negative, but it must be remembered that this segment is still significantly smaller volume-wise (22% volume contribution but 40% net revenue contribution), and it is therefore much more difficult to offset the decline in cigarette volume. Nevertheless, I was very pleased to see that heated tobacco shipments in the third quarter of 2025 were up 16% year-over-year, one of the strongest growth rates in the last two years:

Figure 5: Philip Morris International Inc. (PM): Heated tobacco shipment volume on a quarterly basis (own work, based on information from company filings)

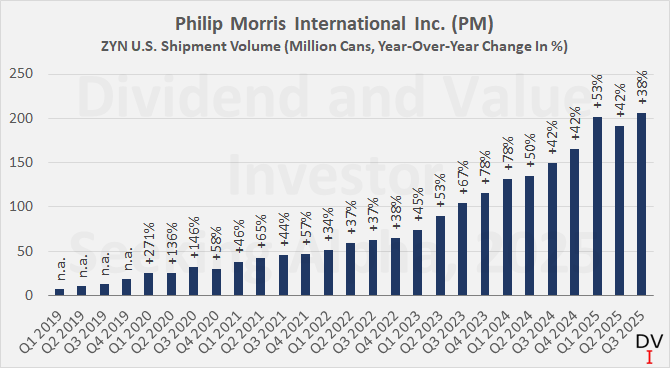

If we include nicotine pouches - Philip Morris' second growth driver - in the equation, volume growth becomes positive at +0.7% compared to Q3 2024. ZYN continues to grow strongly, but there are signs of a modest slowdown, which should also be seen as a sign that competition (especially British American Tobacco p.l.c., (BTI, BTAFF)) is not asleep. Nevertheless, volume growth of 38% in the U.S. (Figure 6) remains very respectable, although I would not be surprised if market sentiment continues to shift further toward British American Tobacco and slightly away from Philip Morris.

It is important to note that I do not arrive at this hypothesis because I consider the latter company's business activities to be weaker. Rather, I believe that investors have learned to appreciate that British American is anything but a conventional cigarette company with a portfolio of backward-looking smoke-free alternatives.

Figure 6: Philip Morris International Inc. (PM): ZYN U.S. shipment volume on a quarterly basis (own work, based on information from company filings)

Overall, and as evidence of continued strong pricing power across all three segments (cigarettes, heated tobacco, and oral nicotine products), Philip Morris reported organic net revenue growth of 5.9%, resulting in $10.8 billion for the quarter, which was largely in line with consensus estimates.

Looking ahead to the full year, Philip Morris left its organic net revenue growth guidance unchanged at 6% to 8%, once again demonstrating that quarterly results should not be overinterpreted.

The guidance for cigarette and smoke-free product shipment volumes was maintained, as were expectations for operating cash flow and capital expenditures. However, the previous guidance for operating cash flow of “more than $11.5 billion” did not include dividend income from the now deconsolidated Canadian affiliate, suggesting now weaker underlying operating cash flow. However, the corresponding dividend income is unlikely to make a significant contribution to operating cash flow: Multiplying the contribution of $0.10 to EPS by 1,556 million shares outstanding would amount to approximately $156 million, or approximately $137 million when offset by the $16 million in costs associated with implementing the RBH plan (and ignoring an insignificant tax benefit).

In terms of adjusted EPS, Philip Morris International has raised its guidance slightly from a range of $7.43–$7.46 to $7.46–$7.56, with the underlying GAAP EPS guidance increasing by $0.12 to $0.15 (see page 4 of the 8-K filing for further details).

Overall, I see no reason to change my previous free cash flow assessment and, therefore, my expectations for continued deleveraging. By the end of next year, Philip Morris expects a leverage ratio of 2x adjusted EBITDA, which seems realistic, especially assuming continued weakness in the U.S. dollar (see my previous article for details), but implies continued significant earnings and cash flow growth, as well as a moderation in investments.

As far as cash returns to shareholders are concerned, it should be noted that management remains prudent and does not currently repurchase shares. This makes sense not only in light of the still high level of debt ($47.3 billion at the end of the second quarter, 2025 10-Q3 not yet available), but also, of course, in view of the far from cheap valuation. Even after taking into account management's updated EPS guidance and the mid-single-digit decline in share price at the time of writing, PM shares are still trading at a price-earnings ratio of over 20.

That said, I certainly welcomed the 8.9% dividend increase announced a month ago, despite the consequently smaller room for debt repayment. While in my last assessment, I estimated Philip Morris’ debt repayment capacity at $1.5 billion annually, the latest dividend increase reduces it to well below $1 billion. That said, in view of the continued solid growth and expected moderation in capital expenditures, I wouldn’t say that the increase was imprudent.

Conclusion - An Increasingly Constructive Valuation

Philip Morris International's delivered solid results for the third-quarter result, in my view. The company's cigarette portfolio remains resilient, while heated tobacco products and, in particular, oral nicotine products (especially ZYN) continue to grow strongly.

At first glance, the less than 1% year-over-year growth in shipping volume seems weak if we disregard the contribution from the individual segments. Philip Morris' smoke-free portfolio grew by almost 17% in volume in the third quarter but contributed only 22.4% to total volume. At the same time, cigarette volume, which accounts for more than 77% of total volume, declined by “only” 3.2%. Against this backdrop, I think it says a lot that net revenues of smoke-free products accounted for more than 40% of total net revenues.

Earnings adjustments were acceptable, and I therefore maintain that the adjusted operating margin of 43.1% – 1.2 percentage points higher than in the third quarter of 2025 – actually reflects the underlying operating performance well.

Frankly, I cannot understand the market's (once again negative) reaction after what was undoubtedly a solid earnings report. Admittedly, with a forward price-earnings ratio still above 20, PM shares are far from cheap, but I maintain that Philip Morris International is more than just an ordinary cigarette manufacturer. The company is broadly diversified (in terms of products, brands, and regions), well managed, highly cash-generative, and has concrete growth prospects, unlike several non-tobacco companies in the consumer staples sector, which face ongoing challenges in terms of sales volumes and, depending on the industry, even margin pressure (e.g., the meat, confectionery, and spirits industries).

If the market value of PM shares continues to decline, I could well imagine returning to at least reinvesting my dividends, while I see little reason to buy other highly valued consumer staples companies with very limited growth prospects, as I explained in my previous article. With a price-earnings ratio of 18 or less, which corresponds to a share price of around $130, I would feel comfortable returning to reinvesting dividends (or outright purchases here or there). At this price, I would lock in what I consider to be a safe starting dividend yield of 4.5%, which I think is a reasonable starting point, especially against the backdrop of continued expected annual dividend increases.

Thank you very much for reading my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.