Disclosure: I do not have a stake in $DUOL.

The Education Opportunity

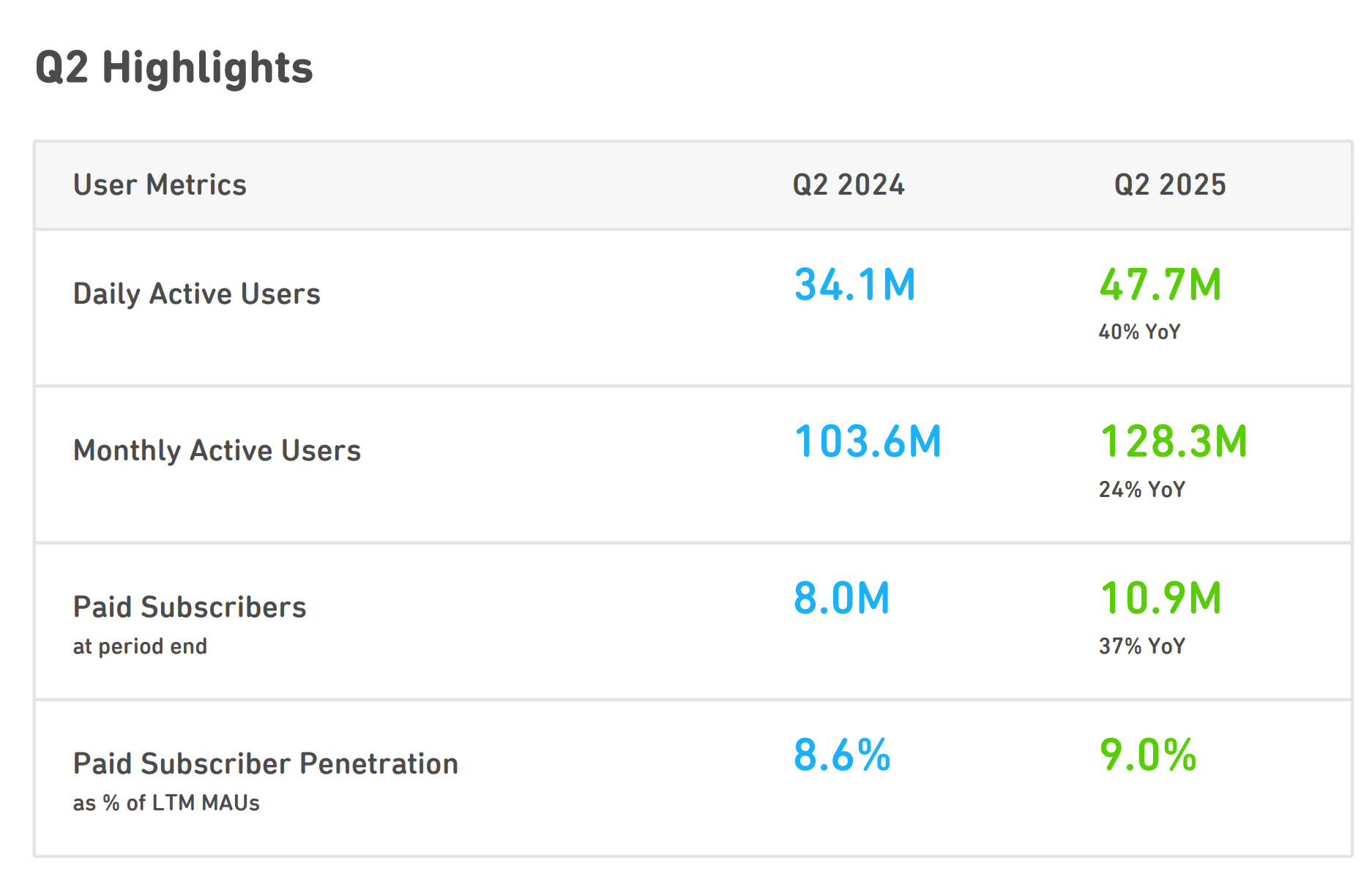

Duolingo finished 2024 with over 40 million daily active users, up 51% year-over-year, and generated $748 million in revenue. The company is perceived as just a language learning app, but it is building what could become the operating system for consumer education in the AI era. The company now has 10.9 million paying subscribers as of June 2025, converting roughly 9% of its monthly active user base into paid customers. That conversion rate is climbing while the absolute user base grows at rates that would make most consumer internet companies jealous. The stock has become one of the most interesting growth stories in public markets, especially given its relatively flat performance this year.

We’ll explore the bull and bear case in this deep dive, but here are the 3 pillars that the thesis relies on:

Pillar 1: The Gamification Moat Creates Unprecedented Engagement and Low-Cost Growth

Pillar 2: AI Integration Accelerates the Moat While Expanding Margins

Pillar 3: Category Expansion and Platform Vision Create Multiple Growth Vectors

Before we dive in, why did I even get interested in DUOL in the first place? There are two main reason:

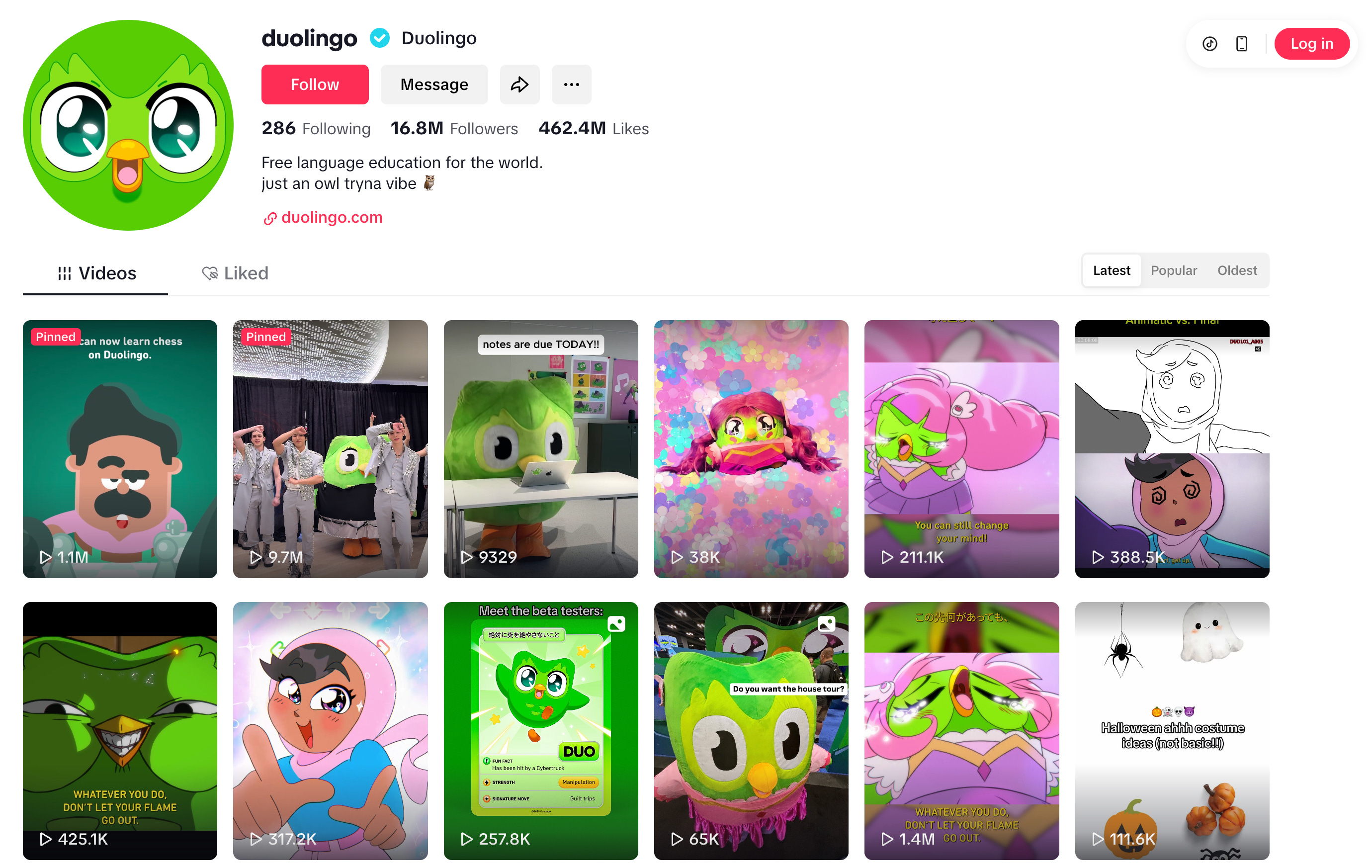

First, I have always been fascinated by their social media strategy. As a content creator myself, I constantly try to study how brands get distribution for their messages. Bringing a product into the world is not easy. Getting millions of people to consistently engage with that product’s content through apps like TikTok, which Duolingo has absolutely dominated in, is even harder. When I realized that their green owl mascot racks up hundreds of millions of views a month — it showed me the DNA of this company to generate attention for their product is resonating more deeply with the cultural zeitgeist and it might not just be a language learning app.

Second, I am in a stock draft competition with my friends. We started in June of 2025 and I ended up picking DUOL as my last pick. I picked it at the amazing price of $447, thinking I was getting a deal as it was down from $530 (I also did know their top line metrics were incredible in terms of growth) and then the stock tanked and now I am more curious about the pick I made. The rest of my mock ETF is below:

The Bull Case

The bull case for Duolingo rests on understanding that this is not an education company competing with Rosetta Stone or Babbel. This is a consumer internet company that happens to teach languages, and increasingly math and music, using the same psychological hooks that made social media and gaming addictive. The app’s gamification strategy, centered on streaks, leaderboards, and loss aversion mechanics, has driven engagement rates that rival social platforms. When you see someone check Duolingo at 11:58 PM to maintain their 400-day streak, you’re not watching education. You’re watching habit formation that generates predictable cash flows. I personally have friends that are addicted to making sure they continue their streaks and given I used to have a streak with a girl back in 7th grade on Snapchat (Samantha, if your reading this I still love you) I can understand how the gamification of those streaks result in sticky users. The company has figured out how to make learning feel like entertainment, which means they can charge for it like entertainment.

The transformation accelerated dramatically in 2024 with the rollout of AI-powered features. Duolingo Max, the premium tier priced at $30 per month or $168 annually, introduced AI features like Video Call with Lily and Roleplay scenarios powered by OpenAI’s GPT-4. These are not incremental improvements. These are features that fundamentally change what digital education can deliver. When a user can have an unscripted, adaptive conversation with an AI character that adjusts difficulty in real-time, you’re approaching the value proposition of a human tutor at a fraction of the cost. The company is using AI not just to create content faster but to deliver experiences that were previously impossible at consumer price points. That’s the unlock that Wall Street is starting to understand.

The financial profile supports the growth story in ways that separate Duolingo from most high-growth SaaS companies. The company operates at 73% gross margins while maintaining positive operating margins as of 2024.

This is a business that scales beautifully because incremental users cost almost nothing to serve. The freemium model creates a massive top-of-funnel, and the gamification engine converts free users into paying subscribers without traditional sales and marketing spend. Sales and marketing represented only 12% of revenue at $27 million, which is absurdly low for a consumer internet company at this scale. That efficiency comes from network effects and virality, not paid acquisition, which means the unit economics improve as the company grows rather than deteriorating like most consumer businesses.

The Gamification Engine That Prints Money

The core insight that Luis von Ahn (founder/CEO) and his team had in the early 2010s was that education technology had an engagement problem, not a content problem. There were plenty of ways to learn languages online. What didn’t exist was a product that made people want to come back every single day for years. The solution was to stop building education software and start building a game that happened to teach you things. Duolingo introduced streaks, rewarding users for learning daily, with the longer streak creating stronger psychological attachment. This one feature became the foundation of a business model that now generates three-quarters of a billion dollars annually.

The streak mechanic is deceptively simple but works on multiple psychological levels. At the surface, it’s a counter that goes up by one each day you complete a lesson. But what it actually does is transform language learning from an abstract long-term goal into a daily commitment with visible progress. Users offered a streak wager see a 14% boost in day 14 user retention.

The monetization flywheel works because gamification creates both free user engagement and natural upsell opportunities. Free users get limited “hearts” that represent mistakes they can make before having to wait or watch ads. Streak freezes allow users to protect their streak if they miss a day, but you have to earn or buy them. Once users have used up all their streak freezes, they can exchange in-app currency for new freezes, or purchase them directly, adding a new revenue channel. The app is training users to value the features they don’t have, which makes the subscription conversion feel like a natural upgrade rather than a hard sell.

From 2017 to 2020, Duolingo’s revenue jumped from $13 million to $161 million, growth driven substantially by its gamification strategy. That trajectory continued through 2024 as the company refined the balance between free and paid features. The key insight is that gamification doesn’t just drive engagement, it creates willingness to pay. When someone has a 300-day streak and runs out of hearts on day 301, they’re far more likely to subscribe than someone who just downloaded the app yesterday.

AI as the Moat Deepener

Alright, so let’s talk about AI because quite frankly — it may be the reason DUOL stock is flat YTD.

Duolingo began cutting contractor staff in 2024, stating that generative AI is accelerating content creation dramatically faster. The company discovered that AI could generate language learning content at a pace that humans simply cannot match. The use of large language models enabled Duolingo to generate 7,500 content units in 2024 compared to 425 in 2021. When you can launch courses in new languages or add advanced content in weeks rather than years, you create a moat that competitors cannot easily cross.

The AI advantage also goes far beyond content generation. Duolingo Max introduced Video Call with Lily in 2024, placing users into unscripted video conversations where they must respond in real-time without assistance. This feature uses GPT-4 to create adaptive conversations that adjust based on user responses. If you answer with simple, short responses, the AI matches that level. If you provide detailed answers, it escalates the complexity. This level of personalization was previously only possible with human tutors, and human tutors charge $30 to $100 per hour. Duolingo is delivering comparable experiences for $30 per month, unlimited usage. The unit economics of AI-powered tutoring are fundamentally better than human-powered alternatives.

The second major AI feature is Roleplay, which creates scenario-based learning where users take on roles in fictional situations. One early scenario places users in a café where they must order in Spanish, with the AI character Lily playing the barista. These scenarios are not scripted conversations where you select from multiple choice responses. You type or speak freely, and the AI responds contextually. This matters because the biggest gap in traditional language learning is the jump from classroom exercises to real-world conversation. The Explain My Answer feature rounds out the offering by providing on-demand explanations of grammar concepts when users make mistakes. The feature was adopted by 65% of users and increased course completion rates by 15%.

Building AI features that actually work in production at consumer scale is difficult and expensive. It requires massive amounts of training data, engineering talent, and iteration cycles. Duolingo benefits from the world’s largest language learning dataset, with over 103 million monthly active users generating engagement data. That data advantage compounds because every user interaction makes the AI better at personalizing content and predicting what users need. Competitors starting today would need to accumulate years of user data to match Duolingo’s AI capabilities, and by that time Duolingo will have moved even further ahead. This is a classic network effect moat where scale begets better product which begets more scale. Spotify, YouTube, Uber…all the network effect businesses that consumers love have this built in advantage and AI may help DUOL capitalize on it.

However, there have been some AI concerns around Duolingo.

The existential risk to Duolingo isn’t from language learning startups but from big tech platforms with distribution advantages and AI capabilities that could obliterate the market overnight.

Google is the most obvious threat given that Google Translate now handles over 100 billion words daily and has evolved from simple translation to conversation mode and real-time camera translation. The company could easily build a language learning product into Android, leverage YouTube’s massive library of educational content, and integrate it with Google Assistant for conversational practice. Google already has Bard and Gemini AI models that could power adaptive tutoring experiences, and they have user data from Search, YouTube, and Android that dwarfs what Duolingo has collected. If Google decided to bundle free language learning into its ecosystem the way it bundled Maps and Gmail, Duolingo’s freemium model collapses because competing with free against free eliminates the differentiation.

Even Perplexity is getting into this game…

Apple represents a similar threat through its ecosystem control and recent AI investments. The company could integrate language learning into iOS as a native feature, use Siri for conversational practice, and leverage the education infrastructure it already built for schools. Apple has 2 billion active devices and could push language learning to every iPhone user through software updates, creating instant distribution that Duolingo spent a decade building organically.

OpenAI and ChatGPT present a different kind of threat that’s already materializing. Users can have free-form conversations in any language with ChatGPT right now, getting instant corrections and explanations without paying Duolingo’s $30 monthly Max subscription. The conversational AI that Duolingo licenses from OpenAI is available directly to consumers for $20 monthly through ChatGPT Plus, and the free tier is good enough for basic practice. Microsoft’s integration of AI into its products through Copilot means language learning tools could appear in Office, Teams, and Windows as ambient features rather than destination apps.

Meta has Llama models that power AI across Facebook, Instagram, and WhatsApp, platforms with 3 billion users who could access language learning without leaving apps they already use daily. Amazon could integrate language learning into Alexa for voice-first practice that happens during daily routines rather than dedicated study sessions.

Now, I am not fully convinced that the AI argument within big tech is enough to kill Duolingo. Could it result in the average person maybe not using DUOL and choosing to use another device or application they already have?

Yes.

However, the counterargument is that big tech lacks Duolingo’s focus on engagement design and gamification, and their attempts at education products have mostly failed because they optimize for features rather than habit formation. Google launched YouTube Learning and it went nowhere. Apple’s education initiatives haven’t moved the needle.

These companies are good at building technology but terrible at understanding the psychology of consumer behavior that makes someone open an app at 11:58 PM to maintain a streak — that is hyperspecific to Duolingo and one could make the argument about that being the true moat of the business, the same way Spotify continues to beat Apple Music because Spotify deeply cares about music more than Apple does even both have the same content on their platforms. The real question is whether Duolingo’s engagement moat is deep enough to survive if big tech decides language learning is strategic and throws meaningful resources at the problem with distribution advantages that Duolingo can never match.

The Subscription Model That Compounds

Duolingo operates a freemium model where roughly 91% of users pay nothing and 9% pay for premium subscriptions. This sounds like the company is leaving money on the table, but it’s actually the optimal structure for maximizing long-term value. The free tier serves two critical functions. First, it creates a massive user base that generates data, network effects, and virality. Second, it acts as an extended free trial that qualifies users before conversion. Someone who uses Duolingo for free for six months and builds a 180-day streak is far more likely to convert and retain as a paying subscriber than someone who pays upfront before experiencing the product. We know this playbook very well: I personally didn't pay for YouTube premium for a decade, got hooked, and now I can’t imagine life without it. If you are investing in a business long term, you want that dynamic on users and if DUOL can continue converting people into paid, you likely will see the sticky part of their moat increase their operating leverage.

As of December 2024, approximately 9% of monthly active users were paid subscribers, with paid subscriber penetration increasing significantly since the subscription launch in 2017. That 9% conversion rate is climbing slowly but steadily, and it’s worth understanding why this matters more than it might seem. In a freemium model, conversion rate times average revenue per user equals your monetization efficiency. Duolingo has been increasing both variables simultaneously. The company launched Duolingo Max at a higher price point than Super Duolingo, which increased ARPU among subscribers who upgrade to the premium tier. Meanwhile, the core Super Duolingo subscription has been converting free users at higher rates as the product improves and users become more engaged.

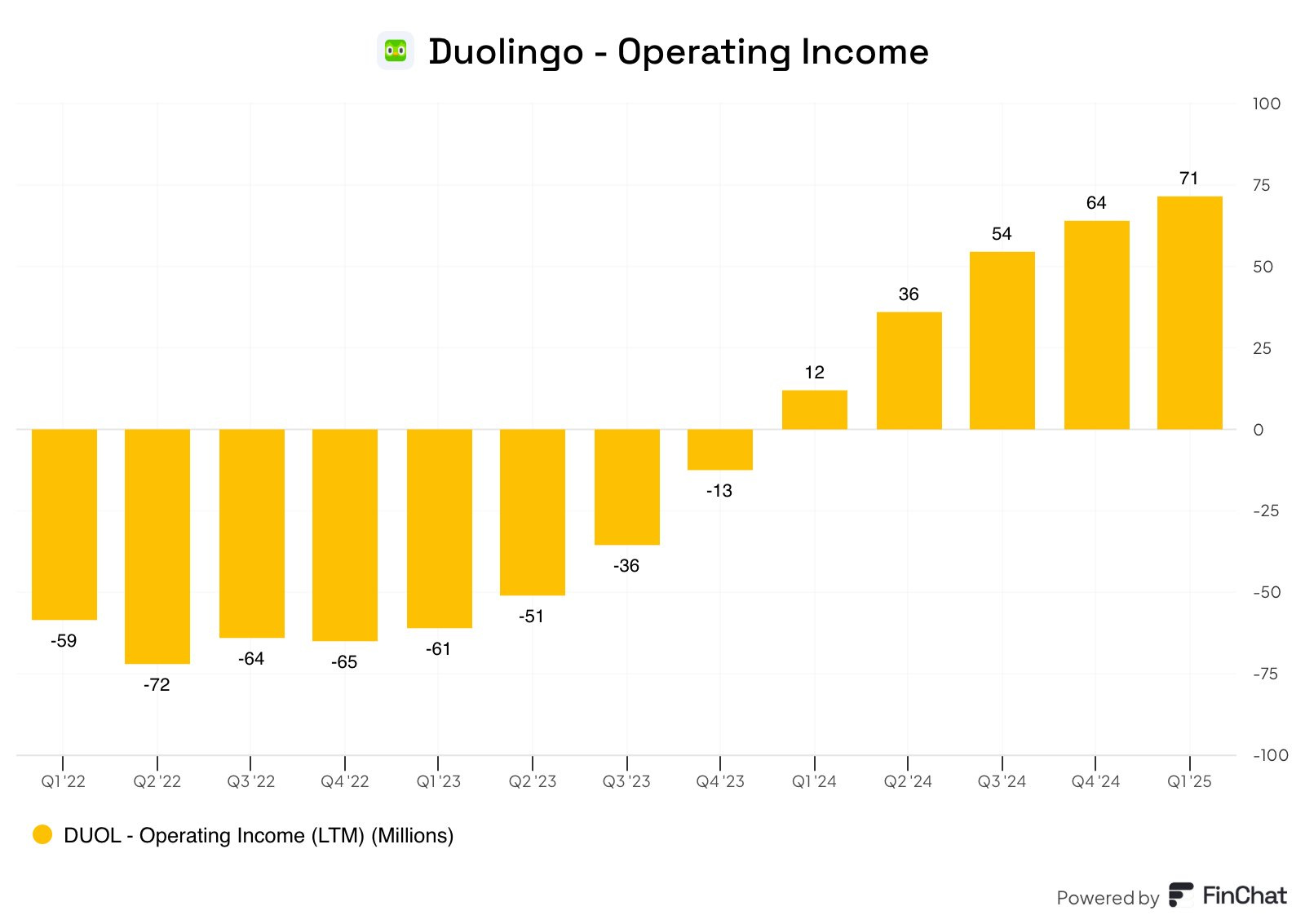

The margin story around AI is also underappreciated for the company. In 2024, Duolingo achieved 25.7% Adjusted EBITDA margins. The company has stated it will invest more in AI and Video Call features in 2025, which may moderate margin expansion slightly, but the long-term trajectory is clear. AI allows Duolingo to deliver more value to users without proportionally increasing costs. A human tutor requires human labor for every interaction. An AI tutor costs essentially nothing per interaction after the fixed cost of building it. As usage scales, the marginal cost approaches zero while the value to users remains high.

The subscription revenue dynamics are particularly attractive because they compound. Duolingo reached 4.8 million paid subscribers at the end of March 2023 and grew to 10.9 million by June 2025. That’s more than doubling the subscriber base in roughly two years. Revenue compounds faster than subscriber growth because existing subscribers stick around while new ones get added. The cohort behavior shows that users who subscribe tend to remain subscribed for years, which creates a growing base of recurring revenue. This is why Duolingo’s revenue growth has been so consistent even as the company scales. The subscription model creates predictability that advertising-based models cannot match.

The Data Moat That Nobody Talks About

The most underappreciated aspect of Duolingo’s competitive position is the data advantage they have built over more than a decade. The company collects engagement data from 130 million monthly active users, and this data is not just volume, it’s structured learning data with labels. When a user completes an exercise, Duolingo knows whether they got it right or wrong, how long it took, what mistakes they made, and what they did next. That’s the raw material for training AI models that personalize education. Competitors cannot replicate this data set without first acquiring similar user scale, which takes years.

More users generate more data. More data makes the AI better at personalizing lessons and predicting when users will struggle or succeed. Better personalization increases engagement and learning outcomes. Higher engagement drives more users through word-of-mouth and retention. The cycle reinforces itself, and the advantage grows over time. This is not a theoretical moat, it’s observable in the product. Duolingo’s AI can predict with high accuracy which exercises a specific user will find challenging and adjust difficulty accordingly. That prediction capability comes from analyzing millions of similar users over years. A competitor starting today would be operating blind by comparison.

The proprietary algorithms that Duolingo has built on top of this data represent intellectual property that is defensible even without patents. The company’s mobile application is protected by multiple IP rights including copyright, patents, utility models, and trade dress protection, though core gamified learning concepts are difficult to patent comprehensively. The real IP is not in the gamification mechanics, which can be copied, but in the specific implementations that come from years of A/B testing and machine learning. Duolingo runs hundreds of experiments per quarter, each one generating insights about what makes users engage and learn better. That institutional knowledge is embedded in the product and cannot be easily reverse-engineered.

The long-term implication is that Duolingo gets better faster than competitors can catch up. Every year the gap widens because Duolingo has more data from more users doing more lessons.

Unit Economics That Could Actually Work

The economics of Duolingo are radically different from traditional education companies because the marginal cost of serving an additional user approaches zero. With 73% gross margins, the platform scales efficiently as its user base expands. When a new user downloads the app and starts a Spanish lesson, Duolingo incurs almost no incremental cost. The content already exists, the servers have capacity, and the AI models are already trained. This is the software scalability advantage in its purest form. Compare this to a traditional language school where every new student requires classroom space, instructor time, and materials. Duolingo can add millions of users with minimal cost increase.

The customer acquisition cost structure is what separates Duolingo from most consumer internet companies. With 90% organic user growth and sales and marketing at only 12% of revenue, Duolingo minimizes acquisition costs as virality replaces paid marketing spend. This is extraordinary. Most consumer apps spend 30% to 50% of revenue on sales and marketing just to keep growing. Duolingo spends 12% and grows faster than most of them. The reason is that satisfied users tell other people to try the app. The gamification creates social sharing moments. The brand has become culturally relevant, particularly among younger users. All of this creates organic growth that doesn’t require paid acquisition spend.

The conversion funnel from free to paid is where the unit economics really shine. Because free users are pre-qualified through engagement, the users who convert to paid subscriptions have already demonstrated commitment. They’re not impulse buyers who cancel after the first month. The company reported paid subscribers totaling 9.5 million at quarter end in Q4 2024, an increase of 43% from the prior year quarter. That subscriber growth is accelerating as the product improves and the free user base expands. The key insight is that every improvement to the free product simultaneously improves retention of free users and increases conversion to paid because more people build habits with the app.

The Duolingo Brand

Duolingo has achieved something that most companies spend billions trying to manufacture and fail. It has become culturally relevant in a way that transcends its core product. The Duo owl mascot, created in 2011, has become a cultural phenomenon that resonates especially well with millennials and Gen Z users. The character has taken on a life of its own through memes, social media, and viral marketing campaigns. The viral marketing campaign where Duo owl fakes his own death generated 17 billion impressions globally without significant media spending. This is earned media that money cannot buy, and it creates brand awareness that drives organic user acquisition at scale.

The brand strength shows up in concrete metrics. Brand awareness grew from 49% to 53% between February 2024 and January 2025, with conversion from awareness to consideration reaching 83% compared to the 73% competitor average. These numbers indicate that Duolingo is not just well-known, it’s well-regarded. People who know about Duolingo are substantially more likely to actually try it compared to competing language learning products.

The long-term value of brand strength is that it creates defensibility independent of product features. Competitors can copy gamification mechanics. They can build AI tutors. They can offer free tiers and subscriptions. What they cannot easily copy is the cultural capital and brand awareness that Duolingo has accumulated over more than a decade. Duolingo leads its category in the US with 53% brand awareness, sitting 24 percentage points above its nearest competitor. That lead compounds because brand leaders get disproportionate attention, which drives more word-of-mouth, which strengthens brand position further. This is a flywheel that is very hard to stop once it reaches critical mass.

How Duolingo Expands to Everything

The thesis that Duolingo is just a language learning company misses the bigger picture. The company has built an engagement engine and a brand that can be applied to any subject that benefits from daily practice and spaced repetition. Duolingo Math was announced in August 2022 and merged into the main app in 2024, with Duolingo Music released in October 2023, and chess lessons in beta launched in April 2025. These expansions are not random product experiments. They are testing whether the Duolingo formula of gamification plus AI can work in categories beyond languages.

The early results suggest the formula is portable. Math and music are subjects where traditional education has similar problems to languages. Students need consistent practice over long periods. The gap between knowing concepts and applying them fluently requires repetition. Motivation is a challenge because progress is gradual. These are precisely the problems that Duolingo solved for languages using gamification and adaptive learning. The same mechanics that keep someone practicing Spanish vocabulary every day can keep them practicing multiplication tables or piano scales. The psychology of habit formation and small wins is universal across learning categories.

The market opportunity in adjacent verticals is substantial. Duolingo operates within a $115 billion direct-to-consumer language learning market and an even larger $220 billion education market overall, with current revenue of $748 million representing just 0.65% of the direct-to-consumer segment. The expansion into math, music, and chess represents an attempt to capture additional share of that broader education market. Each new subject adds potential users who might not have been interested in language learning but want to learn math or music. The cross-selling opportunity also exists where someone learning Spanish might add math for their child or pick up music as a side interest.

The operational advantage of category expansion is that it leverages existing infrastructure. Duolingo doesn’t need to build a new app or brand for math and music. These subjects live within the main Duolingo app and benefit from the existing user base, brand awareness, and product features. The AI infrastructure that powers language learning can be adapted to other subjects. The gamification mechanics transfer directly. The subscription model is identical. This means the incremental cost of entering new categories is far lower than if Duolingo had to start from scratch, which improves the unit economics of expansion.

The long-term vision is that Duolingo becomes a consumer education platform rather than a language learning app. If they execute successfully, a user might turn to Duolingo for any subject they want to learn in a casual, self-directed way.

Competition and Moat Durability

The language learning market is fragmented with numerous competitors ranging from traditional software like Rosetta Stone to newer apps like Babbel to informal platforms like YouTube channels. The key insight is that Duolingo is not really competing with these on the same axis. Rosetta Stone sells expensive software with offline capabilities but lacks engagement features. Babbel offers structured lessons but doesn’t have the gamification or AI capabilities that Duolingo has built. YouTube is free and comprehensive but requires self-motivation and provides no structure. Duolingo occupies a unique position that combines free access, structured curriculum, gamified engagement, and AI-powered personalization. That combination is difficult to replicate.

The moat comes from multiple sources working together. Duolingo’s moat is driven by strong economies of scale, a powerful brand, and growing network effects, with 73% gross margins and AI-powered content creation enabling efficient scaling. Economies of scale mean that Duolingo’s costs per user decrease as the user base grows, which allows them to invest more in product development than competitors can afford. The brand moat means users default to Duolingo when deciding to learn a language rather than researching alternatives. Network effects come from data advantage and social features that make the product better as more people use it. These moats reinforce each other to create a competitive position that is defensible from multiple angles.

The switching cost question is worth addressing because it’s a potential weakness. Most friction comes from adapting to a new platform’s interface and structure rather than true financial or technical constraints, resulting in limited pricing power and some competitive vulnerability. A user can download Babbel or Memrise at any time and start learning. There’s no contractual lock-in beyond a monthly subscription, and many competitors offer free tiers as well. The real switching cost is psychological rather than financial. A user with a 500-day streak is not going to abandon that progress lightly. Someone who has spent months learning with Duolingo’s interface and methodology would find it jarring to start over with a different system. These psychological costs are real but harder to quantify than traditional switching costs.

Valuation

Duolingo trades at $330 per share as of October 17th 2025, giving it a market cap of roughly $14 billion. The Q2 2025 results showed the business firing on multiple cylinders with revenue hitting $252 million for the quarter, representing 41% growth year-over-year. The company raised full-year guidance to $1.01 billion to $1.02 billion, up from prior expectations of $987 million to $996 million. That puts the stock at roughly 13.7x forward revenue, which is down from the 15x to 20x multiples the stock commanded earlier in 2025 when shares briefly touched $544 before pulling back. The multiple compression happened despite accelerating fundamentals, which creates an interesting setup for investors trying to decide if this is expensive or cheap.

The Q2 results provide updated inputs for modeling the business forward. Daily active users hit 47.7 million, up 40% year-over-year, while paid subscribers reached 10.9 million, up 37% year-over-year. The DAU to MAU ratio improved to 37.2%, which is a substantial increase from the 32.9% ratio a year earlier and indicates deepening engagement across the user base. ARPU grew 6% year-over-year, driven primarily by mix shift toward higher-priced tiers like Max and Family Plans rather than base price increases. The gross margin came in at 72.4% in Q2, expanding 130 basis points sequentially from Q1 despite the rollout of AI features. Adjusted EBITDA margin hit 31% for the quarter, and the company raised full-year EBITDA margin guidance to 28.75% at the midpoint. These are the metrics of a business that is scaling efficiently while maintaining high growth rates.

The framework for valuing Duolingo needs to account for the multiple growth vectors working simultaneously.

First is subscriber growth, which is running at 37% year-over-year and shows no signs of slowing given that DAU growth of 40% provides a leading indicator for future subscriber conversions. If paid subscribers grow from 10.9 million today to 25 million by 2030, that’s a reasonable trajectory given current conversion rates and the expansion of Max availability.

Second is ARPU expansion, which is being driven by mix shift to premium tiers rather than price increases. If ARPU grows from roughly $78 annually today to $110 by 2030 through continued migration to Max and Family Plans, that would represent 7% annual growth. Those two inputs alone get you to $2.75 billion in subscription revenue by 2030. Add another $400 million from the English Test, ads, and other sources, and total revenue reaches $3.15 billion.

The margin story is where Duolingo separates from most high-growth companies. The business is already generating 31% adjusted EBITDA margins while growing 40%, and management has demonstrated operating leverage across the income statement. AI costs, which were feared to compress margins permanently, came in lower than expected in Q2 and are declining as efficiency improves. The company is also testing direct web checkout that bypasses Apple’s 30% app store fee, instead paying roughly 2% to payment processors like Stripe. That change alone could add several hundred basis points to margins over time as it rolls out. If adjusted EBITDA margins expand to 35% by 2030, which seems achievable given the fixed-cost nature of the business, that would generate $1.1 billion in EBITDA on $3.15 billion in revenue.

The valuation math from here depends on what multiple you assign to 2030 EBITDA. If the market values Duolingo at 25x EBITDA in 2030, which would be reasonable for a business still growing 20% to 25% at that scale, you get to a $27.5 billion market cap. That implies roughly 2x upside from today’s $14 billion market cap, or about 15% annualized returns over five years. The bull case is that margins expand more than expected as AI costs decline and direct checkout scales, getting EBITDA margins to 40% by 2030. In that scenario with $1.26 billion in EBITDA at 30x multiple, you’re looking at a $37.8 billion market cap or 2.7x from current levels, which would be roughly 22% annualized returns, likely beating the S&P.

The bear case is that user growth slows faster than expected, max adoption disappoints, and competition from free alternatives pressures pricing. If revenue only reaches $2.5 billion with 28% margins by 2030, that’s $700 million in EBITDA. At 20x multiple, you get a $14 billion market cap, which is flat to today and represents zero return over five years. The current valuation at $330 per share seems reasonable rather than cheap or expensive. The stock has pulled back 39% from the May 2025 highs despite fundamentals continuing to improve, which suggests the market is discounting either growth deceleration or increased competition. The Q2 results showed neither of those concerns materializing.

This is the part that I think the bulls should be happy about — so far the market has discounted the stock from its highs due to various concerns, but almost nothing in the actual results shows a mapping of those concerns to reality. Until I see a meaningful connection between the mainstream concerns and the numbers, its hard to take those concerns seriously.

DAU growth of 40% exceeded expectations, bookings beat by a healthy margin, and profitability expanded more than anticipated. The guidance raise for both revenue and margins indicates management has confidence in the trajectory. The risk is that I’m underestimating competitive threats from big tech or overestimating the sustainability of 35% to 40% subscriber growth. But at 13.7x forward revenue for a business growing 40% with 30%+ EBITDA margins and positive cash flow, the setup looks more attractive than most high-growth software companies trading at similar or higher multiples with worse fundamentals.

The comparison to historical valuations of category winners is also important to look at:

Netflix traded at 10x to 15x revenue for years during its high-growth phase and delivered multi-bagger returns from those levels as it proved out the streaming model.

Spotify has never commanded premium multiples due to margin structure (record labels taking a majority of the margin) but Duolingo doesn’t have that problem.

The closest analog might be Match Group during its dating app dominance period, which traded at 15x to 20x revenue while growing 30% to 40% with improving margins. Duolingo is growing faster than Match was at comparable scale and has better unit economics.

The valuation today prices in continued execution but doesn’t give the company much credit for category expansion into math, music, and chess, or for the potential of Max to drive significant ARPU expansion as adoption scales. If those initiatives work, the upside case materializes. If they don’t, the stock probably trades sideways for a while but the core language learning business provides a floor on valuation given its cash generation and market position.

Risks

Every investment has risks, and Duolingo has several that deserve consideration. The first is execution risk around AI features. The company has bet heavily on AI as a differentiator, but generative AI is moving fast and unpredictably. If OpenAI or other providers change pricing, terms, or API access, it could disrupt Duolingo’s product roadmap. The company is also dependent on third-party AI models rather than building proprietary models, which means they don’t fully control a core piece of their technology stack. If competitors get better access to AI or if AI becomes commoditized, the advantage could narrow faster than expected.

The user growth question is another risk that investors worry about. Duolingo grew daily active users 51% in 2024, but maintaining that growth rate becomes harder as the base gets larger. There are only so many people in the world who want to learn languages on their phones. The expansion into math and music addresses this by broadening the addressable market, but those categories are unproven. If growth in core language learning slows and the new categories don’t gain traction, the company could face a growth deceleration that compresses valuation multiples. The market prices high-growth companies on future expectations, so any miss on growth could be punished disproportionately.

The monetization risk is about whether Duolingo can keep increasing the percentage of users who pay. The current 9% conversion rate from monthly active users to paid subscribers is good but not exceptional. Many freemium companies get to 10% to 15% conversion over time. If Duolingo cannot move the conversion rate higher, then growth becomes entirely dependent on adding more free users rather than monetizing the existing base better. The risk is that the company has already converted the users most willing to pay, and the remaining 91% are permanently free users who will never subscribe regardless of what features get added. This would cap monetization potential and limit margin expansion.

The final risk is valuation sensitivity. Duolingo trades at a premium multiple reflecting high growth expectations. If the company executes perfectly and meets expectations, the stock might deliver market returns. If they exceed expectations, the stock could outperform significantly. But if they disappoint on any key metric, the valuation compression could be severe.

Final Takeaways & Why I Don’t Have A Position

Duolingo has built something rare in consumer internet. The company combines organic growth, strong unit economics, brand strength, and a product that genuinely helps people learn. The gamification engine creates engagement that rivals social media while teaching useful skills. The AI integration is making the product better at a rate that competitors cannot match. The expansion into new categories creates multiple paths to sustained growth. The financial model generates cash while growing fast, which gives the company strategic flexibility. These elements work together to create a business that should compound value over time.

However, I am not making the investments for several reasons:

I personally do not like being long the idea of learning languages. As important as I think it is for humans to speak multiple languages, I think there are other businesses that have the same network effect and power laws that DUOL have that operate in much more important categories. One example is Robinhood. Democratization of financial opportunity is far superior, to me, than learning a language. The valuation in DUOL is not compelling enough to feel it is so discounted against other businesses with similar models that operate in important categories. Now, I know they are expanding beyond languages, but again the overall TAM is not as compelling — music, math, chess are all important…but none compare to TAMs for other consumer products that I feel could be greater (Uber for transportation, Netflix for content, Robinhood for finance). The opportunity DUOL has is gigantic, I just personally don’t want to be long that opportunity as I think other TAMs are more important.

I don’t love the AI narrative that overhangs the stock. Now, let me be clear: I do not think this stock will be flat over the coming years and it likely will outperform the market. I just think that any narrative around AI making language learning easier from big tech is not enough to kill Duolingo, but it could be enough to put a strain on the stock performance. I’m not willing to deal with that overhang on my investment. Everyone will always have some narrative overhang on their stocks, you have to pick and choose which ones you can live with.

The thesis is not that Duolingo will grow in a straight line or that execution will be perfect. The thesis is that the company has built structural advantages that compound and create a defensible position in consumer education. The network effects from data get stronger as more users join. The brand becomes more entrenched as cultural relevance increases. The engagement mechanics get refined through continuous testing. The AI capabilities improve as the data set grows. These advantages create a flywheel where success breeds more success, and the gap between Duolingo and competitors widens over time.

The risks are real and should not be dismissed. Competition from free alternatives could pressure pricing. User growth could slow as penetration increases. AI could become commoditized. Execution on new categories could disappoint. Valuation multiples could compress if growth decelerates. Any of these scenarios would hurt returns. But the base case is that Duolingo continues executing at a high level, growing users organically, converting more of them to paid subscribers, expanding margins, and entering new categories successfully. That base case justifies current valuation and offers upside if the company exceeds expectations, even if I am not making the investment today.

For investors who believe in the long-term shift to digital education and the power of habit-forming products, Duolingo offers a way to express that view with a company that has already proven the model works at scale. The question is not whether people will learn online, but which companies will capture that value. Duolingo has a decade head start, a brand that resonates globally, and product advantages that compound over time. That’s the setup for sustained value creation if the execution continues at the current level.

Thank you for taking the time to read the deep dive — truly appreciate your time and let me know your thoughts in the comments and what other companies you’d like me to dive into!

I hope Samantha sees this

Looking forward to next months deep dives hopefully PayPal gets one a lot of people do not understand the company and refuse to give a chance because of some experience they had years prior to current management very misunderstood with a terrible narrative