Alistair Berg/DigitalVision via Getty Images

Introduction.

My research indicates that I find companies with interconnected business models particularly interesting such as Amazon and Mercado Libre and Hilton. The business model of Booking Holdings INC (NASDAQ:BKNG) aligns with my investment criteria. The general public views Booking as a booking website for rooms but I believe it offers many more features.

The main advantage of Booking stems from its broad selection of services accessible through its platform. The platform allows users to reserve accommodations and dining spots and enables them to book flights and hotels together in one transaction. The company plans to introduce vacation activity ticket booking through its app if it achieves its targets. The combination of various services within the platform makes it an essential tool for people who travel.

The main objective of this research is to study the business operations of Booking Holdings INC in detail. The analysis will focus on identifying growth drivers and demonstrating how this company surpasses its market competitors. The research includes a thorough financial assessment and market valuation analysis to understand Booking's market standing.

Based on this analysis, my recommendation for Booking Holdings is a Hold. I contend that after a period of adverse situations for the sector and a subsequent extraordinary recovery, the tourism industry may be reaching a ceiling. This suggests that the share price of Booking, as well as other companies in the sector, could enter a phase of equilibrium rather than continuing its pronounced growth. Throughout this thesis, I will detail the factors that support this perspective of market normalization.

Business model

Booking Holdings (BKNG) operates as a global intermediary in the travel industry through its five core brands: Booking.com, Priceline, Agoda, KAYAK, and OpenTable. While its strategic goal is to be the primary, all-encompassing destination for travelers' needs, the company's financial core is its online accommodation booking service. This segment, which connects consumers with hotels and other lodging options, is the dominant driver of the business, accounting for 89% of total revenue.

Booking Investor Relations

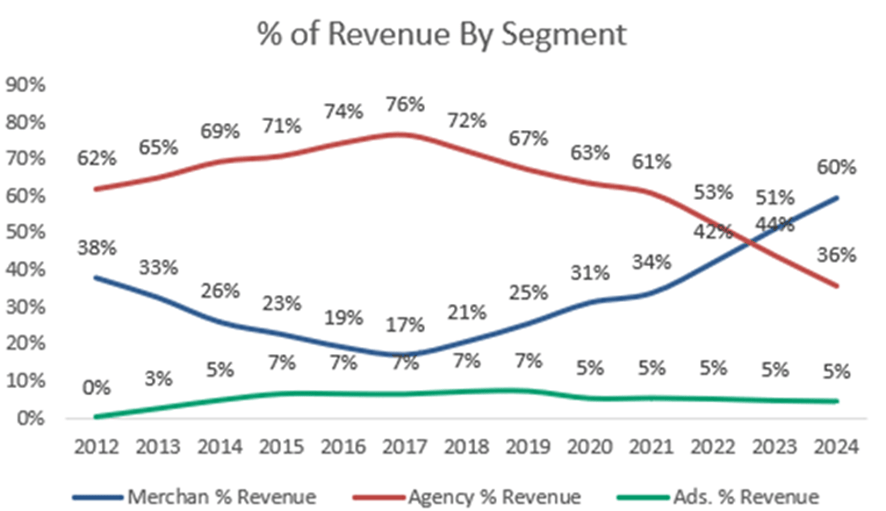

To generate this accommodation revenue, Booking utilizes two primary operational models: the agency model and the merchant model. The agency model, which represents 80% of Booking's worldwide sales and is prevalent in Europe's fragmented hotel market, functions by taking a 10-15% commission on reservations where the customer pays the hotel directly upon arrival. In contrast, the merchant model, more common in the United States, involves Booking purchasing blocks of hotel rooms at a discount and reselling them to customers. Under this model, the customer pays Booking directly, and the company earns a higher margin of 20-30%.

Miguel Dabán (Seeking Alpha)

Beyond its core accommodation business, Booking has strategically expanded its ecosystem with several supplementary services. These include dining reservations and restaurant management tools through its OpenTable platform, significant advertising revenue generated from KAYAK's metasearch engine, and the sale of various travel insurance products that protect both travelers and accommodation hosts.

These ancillary services are fundamental to Booking's "connected trip" strategy. While they currently generate less revenue than accommodation bookings, their purpose is to create a seamless, integrated travel experience. By allowing users to plan an entire vacation—from flights and car rentals to hotel stays and dinner reservations—within a single platform, Booking increases user loyalty, creates additional revenue streams, and strengthens the overall value proposition for both consumers and business partners, encouraging repeat usage of its services.

How cyclical tourism and inflation affect the business

The business operations of the company face dual challenges from tourism cycles and rising inflation rates. The business model foundation requires a thorough examination of the essential long-term factor that affects this company. The tourism industry shows clear cyclical patterns according to my research, which also demonstrates how economic conditions and inflation rates affect its operations.

The current inflationary period has caused travel expenses to rise throughout the industry. The rising costs affect multiple areas of the industry because airline operators must pay more for fuel while new aircraft deliveries remain scarce, and hotels raise their rates because of high occupancy and operating expenses, and tourists face additional taxes that increase their total expenses.

The COVID-19 pandemic created an unprecedented disaster for the tourism industry. The World Tourism Organization (UNWTO) reports that international tourist arrivals dropped by 67 million during the first quarter of 2020, while tourism directly employed between 100 and 120 million people worldwide, faced job loss. The World Tourism Organization (UNWTO) provided these statistics to demonstrate the starting point for the tourism industry's remarkable recovery process.

The European tourism sector shows strong recovery trends according to Eurostat statistics. The European Union (EU) reached its 2019 tourist activity participation rate of 65% in 2023 after tourism activities dropped to 52% during the pandemic year 2020.

The travel industry faces multiple challenges, yet consumers show unexpected resistance to cutting back on their travel plans. The travel industry reports that customers maintain their interest in traveling and demonstrate a willingness to invest more money in their trips despite current economic uncertainty. The United States saw a 14% increase in spring travel expenses during 2025 compared to the previous year. The post-pandemic consumer behavior shows a preference for experiences over material possessions because they now value experiences more than physical items.

The total market shows better resistance to a light recession, according to Booking, because of this development. The company faces challenges because of the specific types of trips that customers choose to book. The rising inflation creates two distinct market segments, which present opportunities for OTAs to serve customers who focus on budget-friendly and mid-range options. The OTAs excel at serving this customer base because they offer price comparison and extensive inventory selection, which appeals to customers who make their decisions based on cost. The tourism industry has demonstrated outstanding recovery from pandemic difficulties and inflationary pressures, yet my research indicates this exceptional growth pattern will not persist. The industry will transition from its current high-growth phase into a mature stage, which will produce stable and predictable expansion rates.

For Booking, these macroeconomic trends are not merely contextual; they directly impact its revenue model and key financial metrics. For instance, inflation that drives up hotel rates directly benefits Booking's agency-driven model. Since its commissions are a percentage of the gross booking value, higher rates automatically translate into higher absolute commission revenue. Furthermore, the consumer shift towards budget-friendly options plays directly to Booking's competitive strengths. Its platform excels at aggregating the fragmented supply of independent and mid-range hotels, attracting price-sensitive travelers who rely on its comparison tools. This directly drives key metrics like 'Room Nights Booked' and solidifies its market share against the direct booking channels of major hotel chains.

Why Booking is ahead of its rivals

The online tourism industry features Booking as one of its most recognizable companies. The market contains multiple competitors beyond Booking since it operates as a single entity. The market shows strong competition through multiple companies that achieve significant growth rates. The global market includes two major players, Airbnb (NASDAQ: ABNB) and Expedia Group (NASDAQ: EXPE) while the United States hotel market faces additional competition from major chains Hilton and Marriott.

The analysis of Airbnb represents my first point of interest. The business structure of Airbnb matches Booking because they operate without owning any real estate properties. The company achieves its competitive edge through its intermediary position, which enables it to connect hosts with guests. The company operates with minimal fixed costs because of this strategy, which I consider highly effective. The main distinction between Airbnb and other platforms, according to my analysis, is the ability for hosts to invite guests to stay in their shared apartment. The ability to share an apartment with guests provides cost-effective options, but I believe many users, including myself, would avoid this arrangement because it involves staying with unknown people.

The business model of Booking matches Airbnb in every way, so I believe Booking outperforms Airbnb in all aspects. The business models of Booking and Airbnb share identical characteristics, which leads me to believe Booking leads the market with superior advantages and faster development. The platform allows users to plan their entire vacation through Booking because it generates more revenue streams and provides a complete trip planning solution from a single platform.

360Hotel Management

The Expedia Group operates through a complex business model because it maintains ownership of multiple brands, which include Expedia.com, Hotels.com, Vrbo, Trivago, and additional brands. The business model of Expedia Group operates identically to Booking because it unites the merchant model with the agency model through room purchases and commission-based intermediary services. The application allows users to book flights and cars in addition to hotels, which provides Booking and Expedia Group with equivalent advantages for trip planning through a single platform.

The identical business model of Booking and Expedia Group leads me to question why I would choose Booking over Expedia Group. The world's largest hotel booking website exists under the Booking brand. The majority of users who plan vacations automatically visit Booking as their first choice for booking accommodations. I use Booking for all my hotel bookings because the platform provides an effortless user experience, and I have never encountered any issues during my travels. The platform serves numerous users who share my experience.

My primary objective in this paper was to demonstrate Booking's dominance as the first travel platform people choose for trip organization because this position appears nearly impossible to challenge. Users who depend on Booking for their travel needs will not likely switch to alternative platforms even when faced with superior competition because they trust their current platform. The combination of trust and established habits creates this situation. The extensive customer base of Booking creates an unbeatable market advantage, which makes it nearly impossible for new booking websites to succeed in the market. The company has secured automatic consumer trust, which functions as an unbreakable barrier for new competitors to enter the market. The industry undergoes a complete transformation because of artificial intelligence advancements.

How artificial intelligence is transforming the industry

Booking Holdings dedicated itself fully to the "Connected Trip" initiative during 2025 because it enables customers to reserve multiple travel services from a unified booking platform. The company has achieved a low double-digit market share for its combined booking service, which shows annual growth exceeding 30%. The company achieved its highest flight booking growth during the second quarter of 2025 with a 44% increase.

The implementation of generative artificial intelligence stands as a fundamental competitive advantage for the company. The company works on its own AI-powered "travel model" while partnering with OpenAI to let ChatGPT access its travel data for planning purposes. The system enhances user satisfaction while it streamlines operations and decreases the expenses needed for customer support.

The presentation included a significant point about Booking creating its development of an AI-powered "travel model" system. The company plans to create proprietary technology that will deliver customized search results and predictive travel recommendations through conversational interfaces, although no specific timeline or technical details were provided.

The company continues to develop its AI-based solutions, which include virtual agent customer service through vBeyond, while focusing on building proprietary technology for improved search experiences.

The industry faces both obstacles and new possibilities because of this ongoing development process. The new interfaces require companies to determine how to organize product and destination details and which content types will work best for these interfaces.

Artificial intelligence integration in tourism operations has revolutionized the way products get presented to customers and distributed to the market. The industry needs professionals to develop content that appeals to the core reasons why people travel. AI creates a dual benefit for customers because it delivers instant responses and eliminates the need for human assistance during support interactions. Booking.com demonstrates its leadership in this transformation through its partnership with TikTok which enables users to make direct accommodation bookings from the social media platform.

Financial analysis

The story of Booking Holdings showcases how a company can survive major challenges through effective execution. The analysis shows how the company faced an extreme financial crisis during the pandemic in 2020 before showing an unexpected fast recovery throughout the following years.

The company achieved pre-pandemic levels in 2022 and then expanded its operating margins while improving efficiency during 2023 and 2024. The company achieved its highest revenue and earnings per share records while maintaining solid growth at a more moderate pace. The company has maintained its positive business model performance throughout 2025.

The company achieved 9% growth in room nights to 1.1 billion during fiscal year 2024 while gross bookings increased 10% to $165.6 billion and revenue expanded 11% to $23.7 billion compared to 2023. The company achieved higher profitability growth than revenue expansion through its disciplined cost management, which resulted in a 17% increase in adjusted EBITDA to $8.3 billion.

StockOpine´s

The positive business performance maintained its upward trajectory during the second quarter of 2025. The company achieved better-than-expected results through its 8% increase in room nights and 13% growth in gross bookings, reaching $46.7 billion, and 16% revenue expansion to $6.8 billion. The company achieved a 28% increase in adjusted EBITDA, which reached $2.4 billion. The European and Asian markets showed the highest growth rates, but the United States market experienced the lowest expansion because of decreased average daily rates and shorter guest stays.

The company achieved its strategic goals through these essential operational performance indicators.

Alternative Accommodation segment bookings increased by 10% during Q2 2025, thus reaching 37% of total room nights. The segment shows strong competition against Airbnb through its expanding market share.

The mobile app and direct website of the company maintained their position at mid-fifties percentage levels throughout the year while showing annual growth. The company depends less on paid advertising because of this essential metric, which leads to improved long-term profitability.

The second quarter of 2025 saw connected trip transactions, which included multiple services such as flights and hotels, reach a "low double-digit share" of total transactions while showing more than 30% annual growth.

The company's fast-growing Connected Trip service proves the effectiveness of its strategy, which extends past basic cross-selling practices. The combination of services through bundling enables Booking to develop complex products that enhance customer retention. The complete package booking process leads to higher customer retention rates because customers tend to return for their next trip, which decreases acquisition expenses while boosting their lifetime value (LTV). The company gains access to more detailed customer data through service bundling, which enables advanced personalization and strengthens customer loyalty.

Valuation

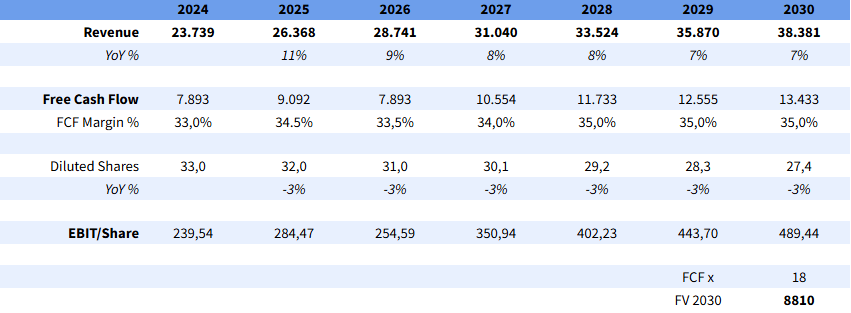

The financial reports show Booking Holdings' ability to handle different crisis successfully. The free cash flow ((FCF) method stands as my preferred valuation approach because the company produces substantial liquidity. The business model of Booking, which involves charging customers before paying hotels, enables the company to maintain high cash flow margins and reduce its expenses and debt levels.

The tourism industry has returned to normal after the pandemic, but I predict Booking will keep its revenue growth between 7% and 8% annually. The company's share buyback program drives my valuation because it leads to revenue growth while the sector recovers from its pandemic impact.

Author's calculations

The company spent $1.8 billion on share repurchases during Q1 2025 before allocating $1.3 billion in Q2 2025. The remaining $24.6 billion authorization shows management intends to use it for shareholder value return and stock price enhancement. The combination of revenue stability and share repurchase program makes me confident about the company's future performance.

My projections indicate Booking will reach $8,810 in 2030. This price target suggests a long-term upside potential of over 60% from current levels. However, and this is the key point of my thesis, my final recommendation is a Hold. This decision is based on a risk assessment: I am not willing to endure the short-term dangers to achieve that theoretical long-term return. As I have argued, I firmly believe the tourism sector has hit a ceiling, which introduces significant uncertainty about future growth rates. Furthermore, I consider the stock to be somewhat overvalued at present, reflecting post-pandemic optimism, and it needs a period for its price to equilibrate. Therefore, I prefer to wait for a safer entry point before committing capital, despite the attractive long-term potential the mathematical model displays.

Conclusion

In conclusion, my analysis demonstrates that the strength of Booking Holdings extends beyond its scale as an intermediary. The company has successfully transformed itself into an integrated travel ecosystem, where its "Connected Trip" strategy and investments in artificial intelligence are not just growth initiatives but the very foundation of its durable competitive advantage. This combination, along with the immense trust users place in its brand, creates a barrier to entry that I consider extremely difficult for competitors to overcome.