Enez Selvi/iStock via Getty Images

Fastenal Company (NASDAQ:FAST) reported the company’s Q2 results on the 14th of July. The industrial and construction supply distributor showed solid sales momentum amid a turbulent macroeconomic backdrop, continuing Fastenal’s strong track record of consistent earnings growth. Good growth in contracts continues to boost Fastenal’s forward outlook, meanwhile tariffs’ impact could increasingly pressure Fastenal’s gross margin.

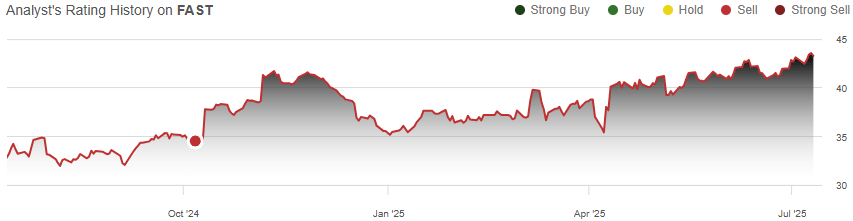

I remained at a Sell rating in my previous October 2024 article on the stock, titled “Fastenal: Resilience Is Overshadowed By Steep Valuation”. Since, the stock has only got more expensive with a 26% total return, outpacing the S&P 500’s return of 9% in the same period.

My Rating History on FAST (Seeking Alpha)

Fastenal Q2: A Solid Result Amid Subdued Industrial Activity

Fastenal reported a strong second quarter. Revenues reached $2080 million with 8.6% year-on-year growth, $12 million above Wall Street’s consensus estimate. The EPS came in at $0.29, one cent above Wall Street’s expectation.

After very subdued growth in previous quarters, the Q2 report now more confidently turned Fastenal closer to the company’s long-term growth rate - the quarter continued to reaccelerate Fastenal’s growth as the daily sales rate improved significantly to an 8.6% level. Driving the growth, Fastenal’s total contract count improved by 9.5% year-on-year, and the shift towards higher-value customer sites aided growth especially well as customers spending above $10 thousand monthly increased significantly. The on-site strategy continued to gain momentum, looking to carry growth in upcoming quarters as well. Safety supplies showed an especially good 10.7% growth in the daily sales rate, while other categories grew at a slower pace.

FAST Q2'25 Investor Presentation

Notably, the macroeconomic backdrop still hasn’t aided Fastenal, making the quarter’s growth reacceleration especially good. The U.S. manufacturing PMI has stayed subdued amid tariff concerns during the quarter, and industrial production has similarly stayed quite low. The macroeconomic backdrop pressured especially fastener sales and MRO-related fasteners only showed quite slow 3.4% growth in the daily sales rate. In terms of end markets, non-residential construction showed the worst growth at 3.0%.

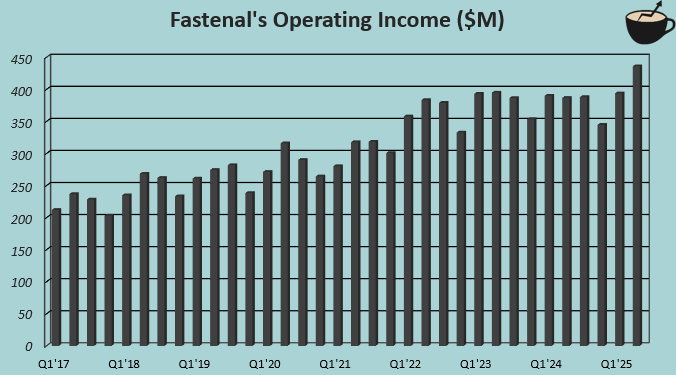

On top of improved sales, Fastenal showed strong profitability in Q2 – operating income grew by 12.7% to a record high of $436 million, showing an 80 basis point gain in the operating margin of 21.0%. The majority of margin expansion was gained through sales leverage, meanwhile, the gross margin also showed a 20 basis point increase to 45.3%. Overall, I believe that the Q2 report more confidently returned Fastenal to solid earnings growth.

Author's Calculation Using TIKR Data

Tariff Impact Could Intensify After Q2

Fastenal’s margin performance was still strong in Q2 as the company’s gross margin slightly improved. Yet, the current tariff landscape could increasingly affect the bottom line after the quarter. The company sources a significant share of products from China to the U.S., facing a massive 95% total tariff on steel and aluminum imports and 55% on other imports. Such a massive tariff is likely to drastically increase Fastenal’s sourcing prices from the country, meanwhile other sourcing countries also face differing tariff levels. At an inventory turnover rate of approximately 2.5, there’s an approximately 5-month average delay in the sourcing prices to show up in Fastenal’s results, and the newly added February-June tariff policies likely haven’t yet shown up in the gross margin to a significant degree. Higher product costs should show up increasingly in H2 results.

While the tariff impact is likely to be material at first, I believe that Fastenal should ultimately mitigate a good part of the tariffs. The company has noted its contracts to allow pricing increases, and Fastenal has already begun to adjust prices - Fastenal increased product pricing by approximately 140 to 170 basis points in Q2 to offset tariffs, and expects to execute additional pricing actions going forward. The pricing increases and good gross margin stability so far underline good pricing power, meanwhile Fastenal is working to mitigate tariffs further through sourcing diversification.

Fastenal’s Valuation Remains Too Expensive

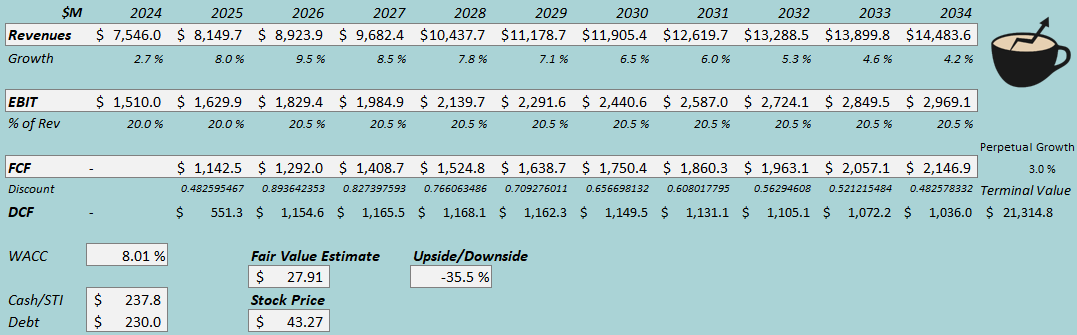

I updated my discounted cash flow (DCF) model assumptions for Fastenal for a fair value estimate. The model again underlines Fastenal’s significantly expensive stock.

As Fastenal’s growth is already reaccelerating despite the subdued industrial activity, I have slightly raised my revenue growth expectations. I now estimate a 2024-2034 CAGR of 6.7% and 3% perpetual growth afterward as Fastenal continues to expand its contract count. Pricing increases should now also provide a short-term boost to revenue growth.

While tariffs seem likely to slightly pressure margins, I ultimately expect Fastenal to shift the impact into pricing. I still assume the EBIT margin to ultimately stabilize at 20.5% and that Fastenal converts after-tax earnings quite efficiently into free cash flow.

DCF Model (Author's Calculation)

The estimates put Fastenal’s fair value at $27.91, 36% below the stock price at the time of writing – at a forward P/E of 39.6, the stock is simply too expensive. Fastenal would need to grow at a materially accelerated pace for the stock to be a worthy investment.

The fair value estimate is up from $24.81 previously when adjusted for Fastenal’s recent stock split.

CAPM

The DCF model uses a cost of capital [WACC] of 8.01%, derived from a capital asset pricing model:

CAPM (Author's Calculation)

I still don’t expect Fastenal to use a noteworthy amount of debt as financing over the long term. For cost of equity, I use the 10-year bond yield of 4.43% as the risk-free rate. The equity risk premium of 4.62% is Professor Aswath Damodaran’s most recent July estimate for the US. Seeking Alpha now estimates Fastenal’s beta at 0.72. With a liquidity premium of 0.25%, the cost of equity and WACC both stand at 8.01%.

Takeaway

Fastenal reported solid Q2 results, as revenue growth reaccelerated despite subdued industrial activity. Sales leverage also boosted Fastenal’s margin level. Going forward, meanwhile, the growth outlook is good, tariffs act as a notable short-term headwind to margins as Fastenal is looking to gradually shift tariffs into pricing. The stock remains too expensive, and as such, I remain with a Sell rating for Fastenal.