Brandon Bell/Getty Images News

One of my favorite idioms in German must be "vom Regen in die Traufe," literally translated as "from the rain into the eave" and more loosely as from bad to worse. While we have been (unpublicized) negative on Tesla, Inc. (NASDAQ:TSLA) for a while, the coming end of federal EV tax credits as part of President Trump's recently signed Big Beautiful Bill, or BBB, has made a rough situation even worse in our view. With the discontinuation of $7,500 in buying incentives further exacerbating Tesla's already existing competitive pressures in the U.S. while it continued to lose market share in Europe and China, we struggle to see a positive near and mid-term future for Tesla and engage in a Strong Sell.

Firstly, Tesla has NOT been a good investment for more than 3 years. Following a meteoric rise before and shortly after the pandemic, shares currently trade roughly on par with late 2022 levels. Relative to the broader U.S. market, Tesla shares are off by almost 40 percentage points with a significantly higher volatility.

A lot of people are quick to point to Tesla's (arguably unrealistic) valuation multiples. Yet, the stock has always traded at such multiples, therefore we believe there needs to be a strong catalyst, or better, a set of strong catalysts for valuation to reach a breaking point.

In light of recent events, we believe those catalysts should be:

- A massively deteriorating outlook on future deliveries following the end of EV credits in the U.S. and market share losses in Europe and China,

- Continued gross margin deterioration amid high competition and building inventories and

- Further backlash towards CEO Elon Musk's political endeavors which have now effectively alienated both fringes of the U.S./European potential customer bases.

Essentially, we believe Tesla has turned from being the hypergrowth posterchild of the EV "movement," led by a charismatic and well-liked CEO, to just another mass market car manufacturer with the substantial added risks of a politically active CEO and a sky-high valuation that looks set to burst at some point.

Given the inherent difficulties in valuing Tesla according to traditional metrics, we refrain from a specific price target, yet we believe there could be a material downside from current levels over the next years. Key risks to our bearish thesis remain higher than expected growth in deliveries which could drive better gross margins as well as political development surrounding CEO Musk.

1/ The key argument behind our bearish stance on Tesla is that the company has entered a "post-growth" phase as deliveries have stalled and are likely to fall further in the midterm amid political backlash and ended EV credits in the U.S.

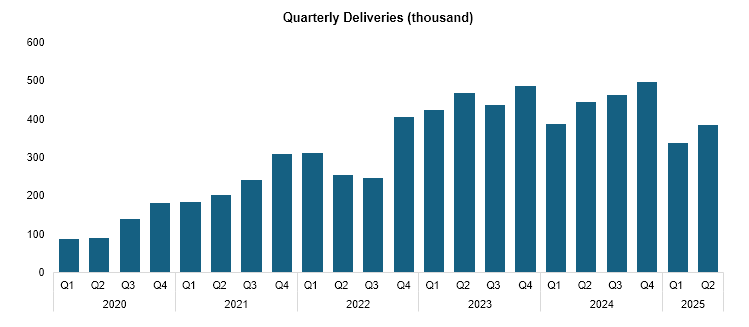

On a quarterly basis, deliveries peaked in late 2024 at almost 500k cars before falling sharply into 2025 with the most recent Q2 sales at 384k. Despite being up vs. Q1, Q2 deliveries were down almost 14% y/y, even higher than Q1's ~13% y/y drop. Deliveries also missed the consensus estimate of 389k vehicles (as per Seeking Alpha) which had already been revised downwards from 395k.

Company Information

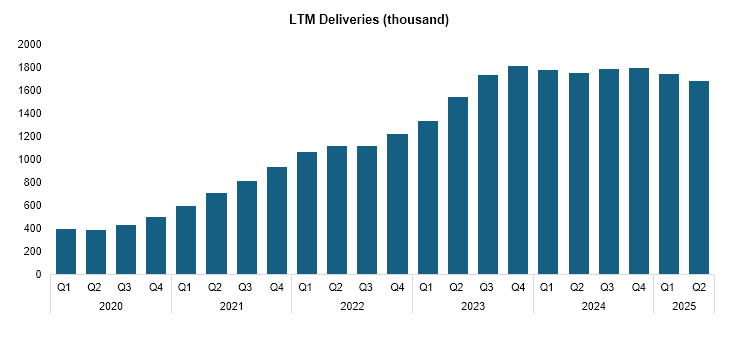

On an LTM basis, deliveries have continued their negative trend since late 2023, declining ~4% y/y vs Q1's ~2% decline and Q4 24's ~1% decline.

Company Information

Company Information

The key factor for stagnating/falling sales has been Tesla's international markets in our view, namely Europe and China.

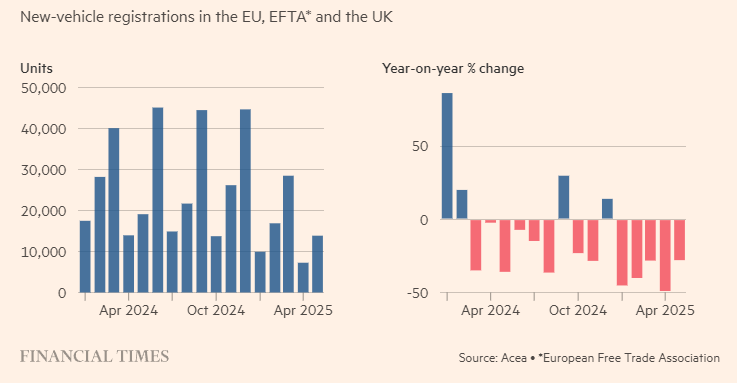

In Europe during May, Tesla vehicle sales on the continent fell by ~28% vs the prior year, marking the 5th consecutive quarterly decline despite the revised Model Y being available since early March.

Financial Times

At the same time, overall BEV sales grew by 27% and total car sales were up ~2% y/y. While Tesla does not officially report their European delivery figures as part of their financials, we believe June's and July's ACEA (Association des Constructeurs Européens d'Automobiles) registration figures should all but confirm another disastrous quarter in Europe.

Statista

Similarly to Europe, Tesla is also materially losing market share in China, as of 2025 the world's single largest market for EVs. During Q2, Tesla delivered around 128k vehicles in the country, around 4% below Q1 numbers and down 12% y/y according to the China Passenger Car Association.

CnEVPost

As noted by EV news website Electrek, sales fell despite the full availability of the new Model Y whose rework had been believed to have temporarily dented Q1 delivery numbers. It also notes that Tesla had been running record discounts on both the Model 3 and Model Y with 0% financing corresponding to around a $3,000 to $4,000 discount depending on the specific model.

Since early 2021, Tesla's average market share in China monthly registrations has fallen from the high teens to high single-digits as the industry has scaled up rapidly (total BEV new registrations grew ~33% y/y in June as estimated by CnEVPost).

Looking forward, we believe Tesla's market share will continue to fall as domestic competitors launch further models, many of them directly targeting the Model Y. Among the Model Y's likely fiercest competitors are the Xiaomi Corporation (OTCPK:XIACF) YU7 and the XPeng Inc. (XPEV) G7, both launched to great success during June/early July, with the YU7 gathering over 200k preorders within minutes. While preorders and reservations should always be taken with a grain of salt, last but not least due to Tesla claiming over 1 million orders for its Cybertruck only to then sell below 50,000 actual models after release, we believe Tesla's position becomes more and more tricky as an increasingly patriotic Chinese marginal customer switches to cheaper domestic brands not associated with Elon Musk's political endeavors.

CnEVPost

While Tesla's sales and market share had held up reasonably well in the U.S. compared to China and Europe, the end of $7,500 in federal EV tax credits as part of the Trump administration's Big Beautiful Bill will likely put strong pressure on domestic sales. While it could raise short-term vehicle turnover during Q3, we believe sales could drop materially in Q4 after the changes take effect on Sep 30.

Notably, while the original form of the bill that passed Congress had the incentive expiring only by the end of the year, the Senate pushed the deadline forward, potentially also due to Musk's recent fallout with the Trump admin.

Overall, we believe Tesla's U.S. topline growth story becomes a doubtful question for the marginal buyer. With Musk having effectively alienated both fringes of the political spectrum, Tesla will rely more and more on politically agnostic buyers seeking an unemotional and efficient purchase. Financial incentives in the form of EV credits have likely strongly benefitted sales in this customer segment, yet with those now gone Tesla's U.S. domestic sales could take a material hit from Q4 onwards.

Overall, we calculate Tesla's FY25 vehicle deliveries falling by ~20% y/y based on annualized YTD figures. Considering recent weakness in Europe and China as well as U.S. sales potentially falling off a cliff in Q4 due to expiring tax credits, we argue there could be more downside.

Company Information, WSR Estimates

2/ While less significant for Tesla's valuation than topline growth, we also note that (automotive) margins continue to trend down with the current buildup of inventories likely becoming a further headwind to pricing. During Q1 25, Tesla reported a 14.3% gross margin for its automotive segment (including services) which, while still excellent for a carmaker was down 240bps y/y and 260bps below FY24. It also continues a longer downtrend which saw margins peaking above 25% in 2021 and 2022.

Company Information

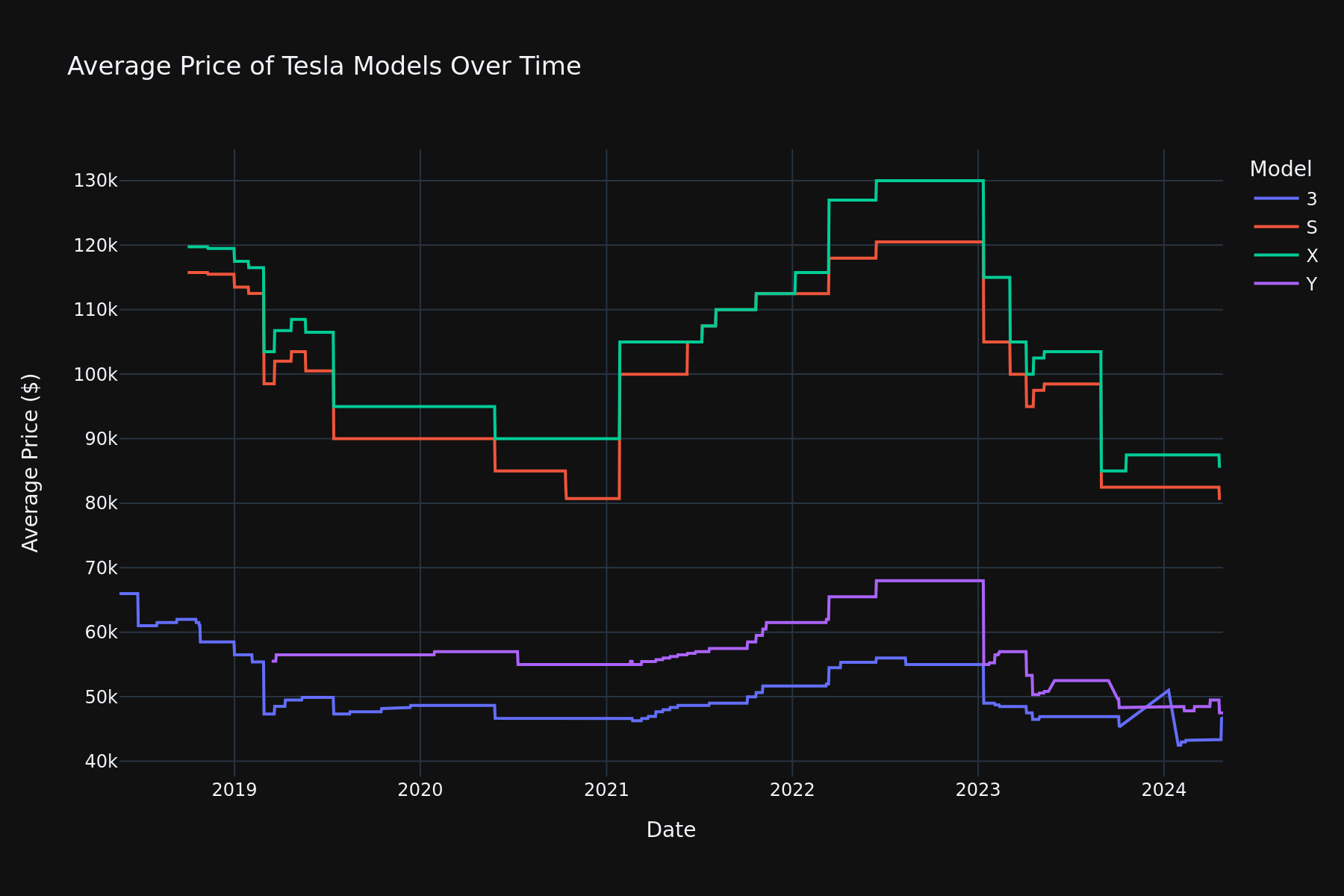

With the manufacturing cost base largely fixed, we believe this is largely explained by higher competitive pressure, forcing Tesla to slash prices across models. The best-selling Model Y for example starts at around $45,000 in the U.S., significantly below pandemic-era prices of ~$55-70k.

SkillsAI

While average selling prices have been roughly stable since 2023, with the end of U.S. EV tax credits worth $7,500 from Q4 onwards, we believe Tesla could be forced to initiate price cuts to stabilize deliveries and sell off building inventories. We note that during both Q1 and Q2 deliveries fell short of production numbers by a cumulative 50k vehicles.

Company Information

With prices for used Teslas also continuing to fall, i.e., a used Model Y's most recent average sales price in March 2025 was around 17% lower vs. a year prior, we could also see the possibility of used car sales cannibalizing new vehicle sales, putting further pressure on delivery numbers and thus ultimately pricing and margins.

Used Model Y avg US selling price (Forbes)

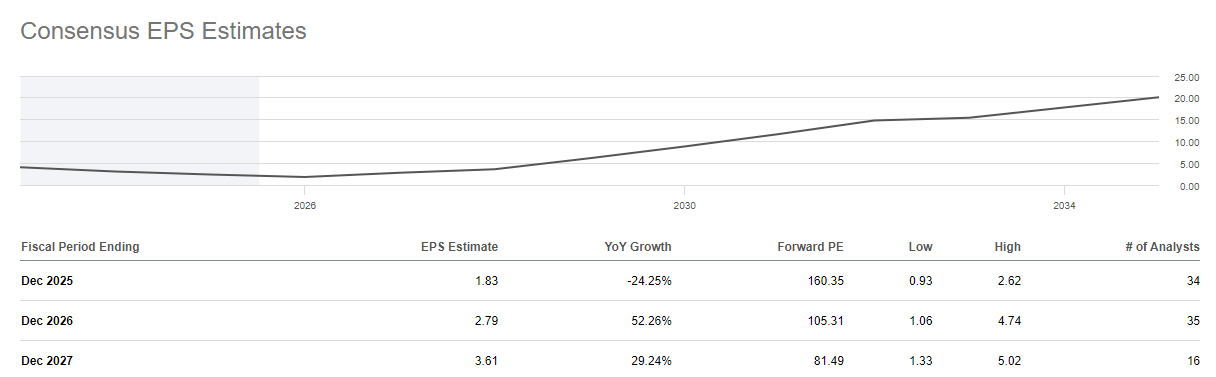

Still, consensus sees 2025 as merely a bump in the road with EPS expected to grow by 50%+ in 2026 and almost 30% in 2027, implying current P/E ratios of 105x and 81x respectively. We disagree and would expect material cuts to estimates over the course of H2 2025 and early 2026 as the market digests a potential 20% y/y fall in deliveries and the further decline in margins that will likely accompany it.

Seeking Alpha

With competition and pricing pressures stronger than ever, we find it hard to justify a future where Tesla will be able to recover (automotive) margins in a meaningful amount while topline growth also remains subdued. Excluding high shots like the Cybertruck (which as of current looks to be insignificant commercially), the company now operates almost exclusively in the mass market. As opposed to 10 or 5 years ago, this mass market for EVs is now well established and highly competitive with several competitors offering better manufacturing quality and features at a lower price point. Add to that a politically active CEO that continues to popularize, and we believe Tesla stock should best be avoided.