Tony Anderson/DigitalVision via Getty Images

Introduction

On Holding AG (NYSE:ONON) is a Swiss-founded company, originally specializing in running footwear with the use of modern technological solutions to allow athletes of all levels to perform at their highest potential. ONON uses sustainable materials alongside modern manufacturing methods and distribution models, which has allowed them to reach customers all around the world. I believe ONON to be performing at a high level and that this is just the beginning of their growth, indicating the company to be 'Hold'.

Investment Thesis

On Holding AG (NYSE:ONON) has emerged as one of the fastest growing footwear brands in the world, riding a wave of premium branding, athlete partnerships, and product innovation. Despite short-term volatility caused by tariff threats and a premium valuation, ONON’s growth trajectory, margin profile, and brand equity position it as a high-quality long-term compounder. While the stock is currently priced for near-perfection, ONON still offers an attractive entry point for investors with a long-term horizon — particularly on any pullbacks.

Financials

ONON reported Q1 2025 revenue of CHF 727 million, up 43% year-over-year — beating consensus estimates by ~CHF 46 million (about 6%). Given that this is the fourth consecutive quarter of growth, it's safe to say this performance is not a one-off. To continue, TTM gross margin is sitting at 60.6% which is higher than competitors such as Lululemon (LULU), Deckers (DECK) and Nike (NKE) who sit at 59.3%, 57.9% and 42.7% respectively). For ONON, this is in line with management's targets, which will create confidence in leadership from an investor perspective and increase stock stability.

At the end of June, ONON closed at $52.05 per share. EPS for Q1 2025 was reported at $0.23 which beat expectations by 4.5%, signifying strong earnings growth. After having a strong start to 2025, a press release from May stated ONON expects to continue this global demand, subsequently aiming to reach at least 28% growth on a constant currency basis which, would be equal to CHF 2.86 billion at current spot rates.

On a global perspective, ONON captures approximately 2% of the market share of the athletic footwear market. This market is still largely held by well-known players such as Nike and Adidas, holding 18%–35% and 9%–25% respectively, depending on which category of shoe you look at. If we take the U.S. alone, ONON holds approximately 6.6%, again behind Nike and Adidas. On a retailer basis, in DICK'S Sporting Goods (DKS), for example, ONON sales increased to 12% while Nike's sales here dropped to 32%.

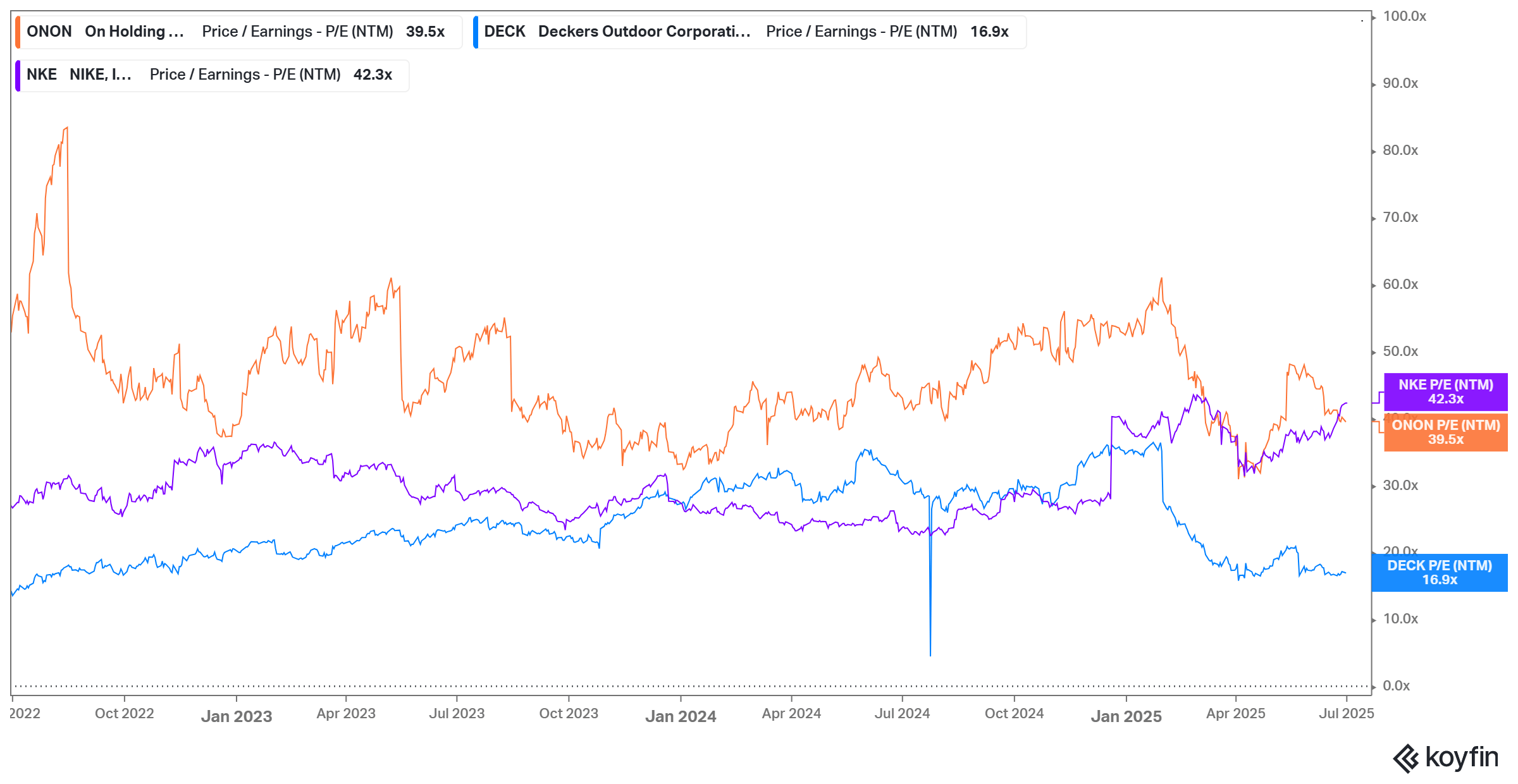

Take a look at the comparative snapshot below:

A Bullish Argument

Diversification

ONON, backed by the well-known former tennis player Roger Federer, has grown to be more than just a running shoe. Over the life of the company we have seen product diversification from the first running shoe into more casual footwear, clothing across a range of sports, and sporting accessories.

On top of this, they've got a large amount of geographic expansion to go into markets like India, LatAm, and China. So in terms of the TAM ahead, I have no worries about ONON's lack of growth opportunities.

D2C Business Model

Furthermore, direct-to-customer (D2C) now makes up 38.1% of revenue and management hope to increase this further with more stores to be put in place each year. Increased revenue from a D2C business model means ONON has more control over it's branding, pricing, margins, and customer experience whilst also generating far more data. It can also lead to more predictable revenue and in turn more accurate forecasting due to reduced reliance on wholesale partners. As an investor, an increase in D2C can mean higher margins leading to more profitability, so ONON's push towards a D2C approach is very welcomed by investors.

Global Ambassadors and Eco-Consciousness

ONON is currently affiliated with some of the top athletes across both tennis and running / athletics, having partnerships with 3x Grand Slam champion Iga Swiatek, Kenyan track star and 2x Gold medalist Hellen Obiri, USA's Olympic medalist Yared Nuguse as well as many more. The use of global ambassadors can accelerate brand awareness and credibility, especially if the ambassadors go on to be successful. When Hellen Obiri won the Boston marathon wearing ONON shoes, this spoke immensely to the credibility of the technology of the shoes and demonstrated their ability to create elite performance.

Outside of the sporting world, ONON has partnered with Global style icons such as Zendaya and FKA Twigs. Zendaya, specifically, has been part of the launch campaign of the Cloudsurfer 2 and Cloud 6. These partnerships appeal to the company's fashion – conscious consumers wanting to avoid 'fast-fashion', making a statement towards how ONON values the climate and environmental stability. The Gen Z consumers have a significantly increased focus on fast fashion than previous generations. Therefore, if a brand can't show it is eco-conscious, it risks losing key market share.

Risks to the business

1. Tariff Exposure and Supply Chain

Currently, 90% of ONON’s shoes are made in Vietnam and 55% of sales come from the U.S. which, has proposed tariffs of up to 46% on imports from Vietnam. There is currently a 'pause' which is due to expire on 9th July. If tariffs are fully imposed, this could cause gross margins to contract significantly and, in turn, prices will rise, which will could negatively impact purchasing patterns. Fortunately, ONON has pricing power and is intending to raise prices anyway, with minimal demand loss expected. For example, management has been raising prices (upwards of $10 per pair) and seeing no demand sensitivity thus far.

2. Foreign Exchange Risk

During the first quarter of 2025 net income fell by 38% solely due to foreign exchange losses (CHF 77m gain last year vs. 15m loss this year). Although FX affects will change as an inherent risk of working with foreign currencies, such big FX swings can be unpredictable and impactful on YoY earnings. Of course, FX gains and losses are a business risk that is inherent in any multinational company and should not deter investors away. Rather, investors would benefit more from focusing on operating metrics (EBIT and EBITDA) rather than net income.

3. Overdependence on Footwear

Currently, ONON shoes are making up 93.7% of revenue, which is a significant reliance on one revenue stream. Take the Cloudmonster, for example, one of ONON's most popular lines, if this were to suddenly flop or face severe supply chain issues, this could have a significant impact on revenue. However, we know that ONON has been expanding their products into apparel and sports other than running, and this diversification will be a huge counter to any overdependences on footwear lines.

Valuation

Relative to peers (NKE and DECK), ONON is trading way above DECK, and slightly below NKE following NKE's recent run up. ONON deserves a premium, way above DECK (6.4%) who have been struggling for growth lately relative to ONON who are growing at 43%. The only area where DECK is stronger is in terms of profitability, who actually have stronger EPS estimates in FY 2025 vs ONON, however, in FY 2026 ONON are expected to grow their earnings considerably faster.

Koyfin

In terms of assumptions, ONON is expected to hit $1.05 in EPS by FY 2026, which would mean they're growing earnings at a rate of 41%. Therefore, for them to hit a stock price ~30% higher than today ($67), they'd need to trade at a Fwd PE of 64x which considering earnings growth of 41% seems on the higher side, though not completely unrealistic.

I think ONON is a very strong business, however, in investing you need to buy quality businesses and buy them at good valuations and I don't think the current ONON valuation gives investors a solid amount of margin for error. Therefore, if I were to buy ONON I'd definitely be waiting for a pullback into the mid- to low-$40s range where the margin for error moving forward then makes a lot more sense.

Conclusion

As I mentioned, I think ONON is a strong business, and they're a very strong competitor to the big players like NKE and Adidas. The numbers speak for themselves, and it's clear they're innovating quick, and meeting the consumers' expectations today. However, the PE multiple ONON is trading at is arguably on the higher end, and I think it's best to wait for a pullback slightly into at least the mid-$40s.

With that being said, I'm going to initiate a "Hold" rating on ONON for now, and perhaps update my rating if ONON does pullback.