mariusz_prusaczyk/iStock via Getty Images

Description

Aya Gold & Silver (TSX:AYA:CA) is a mid-tier and pure-play silver producer with all of its mining assets located in the Kingdom of Morocco. The company's flagship asset is the Zgounder Mine, located in the Anti-Atlas mountain range. With a production of 8.6 million ounces of silver in 2024, Morocco is the 16th largest silver producer in the world, but the largest on the African continent. The largest silver mine in the country is Imiter, owned by Managem, a mining group with operations in eight African countries and listed on the Casablanca Stock Exchange.

Aya Gold & Silver Portfolio Overview (Q1-25 MD&A)

The Zgounder and Imiter mines are among a select class when it comes to ore quality and metallurgy, as some parts of their deposit contain native silver. In both cases, a proportion of the final product is in the form of 99.5% pure silver bars, which can result in much lower smelting or refining charges compared to products sold in the form of concentrate or doré bars. The further away the final product is from pure silver bullion, the higher the smelting charges are. It may look like a benign nuance, but as the numbers below illustrate, the impacts on operating margins can amount to a few percentage points.

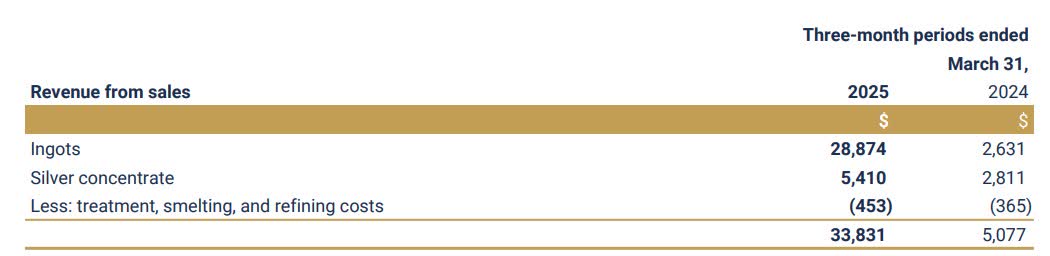

Throughout 2024, silver concentrate and silver ingots represented approximately 70% and 30% of Aya's sales, respectively. However, with the new Zgounder mill ramping up, management expects that only silver ingots will be produced and sold starting in Q2-25. According to regulatory filings, Aya was paid approximately 85% of the metal value with concentrate sales. In contrast, based on management's comments during the Q1-25 conference call, Aya expects higher realized prices relative to average spot prices in a given quarter. The company's strategy is to hold bullion inventory in Geneva while patiently offering physical metal on the ask side of the market.

We are very choosy on how we sell our silver because we have liquidity, we're well funded, so we don't need to rush. So we build inventory in Geneva. We have the silver available for a transaction and we sell it normally by moving the market up. We will price it above market and we wait for the market to move up and come and hit, the bid to come and hit our offer and we're offering metal. It's not paper silver, it's metal, it's identified as such and we normally beat the average of the month or average of the quarter. So if you look at the average realized price by Aya and compare that to the average silver price of the quarter, we beat it steadily. And that is being very disciplined in how we sell it. Aya Gold & Silver Q1-25 Conference Call

For the full year of 2024, Aya reported treatment, smelting, and refining costs of $3.0 million, representing 7.6% of total revenues. If we look at the Q1-25 numbers, those same costs amounted to $0.5 million, or approximately 1.3% of total revenues. As illustrated below, ingots represented ~85% of total revenues in Q1-25, and with the Zgounder mill still ramping up, ingot sales as a proportion of total sales should increase further in the coming quarters.

Q1-25 Sales Breakdown (Q1-25 MD&A)

To put Aya's metallurgy in perspective, MAG Silver (MAG) reported treatment, smelting, and refining costs of $35.3 million in 2024, or the equivalent of 5.6% of total sales. MAG discloses those numbers on a 100% basis, even though it owns a 44% interest in Juanicipio. As discussed in previous articles, the remaining 56% interest is owned by Fresnillo (OTCPK:FNLPF), and MAG is unlikely to be traded for much longer with Pan American's (PAAS) buyout.

Fresnillo sells the totality of its production to Met-Mex for smelting, and refining. For the full year of 2024, Fresnillo recorded refining and treatment charges of $143.5 million, representing ~4% of the gross metal value. Notably, Fresnillo generates almost 60% of its revenues from the sale of various concentrates, which may partly explain why smelting charges look so high. Fresnillo: Juanicipio Standing Out Once Again

In short, the Zgounder mine is in a unique position when it comes to metallurgy. With a disciplined marketing strategy, Aya's realized prices should be slightly above average spot prices over a given period. On top, I would not be surprised if treatment, smelting and refining costs drop below 1.0% of sales in the coming quarter.

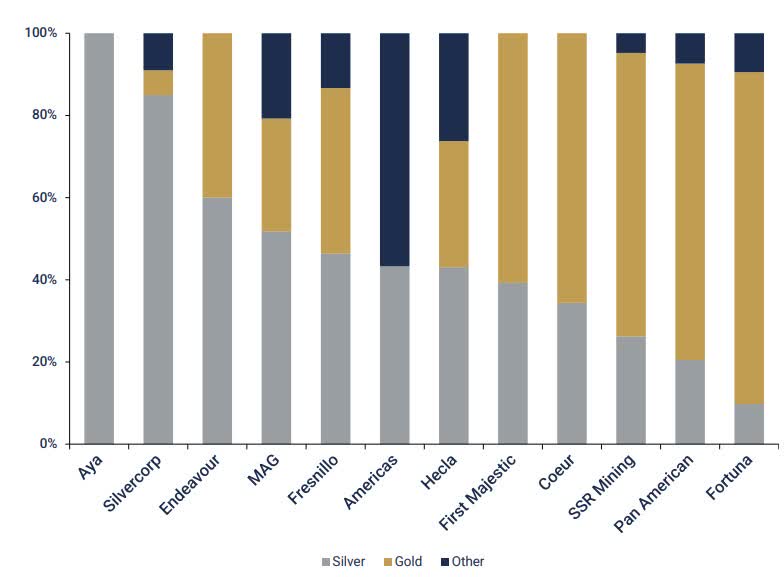

As illustrated below, Aya is the only pure-play silver miner that I am aware of. Fresnillo, MAG, and Endeavour (EXK) also offer exposure to silver, although it is diluted by a meaningful exposure to gold. As of today, I know very little about Silvercorp Metals (SVM), but I plan to research the company over the next few days.

Silver Miner Portfolio Overview (May 2025 Presentation)

Zgounder Mill Expansion

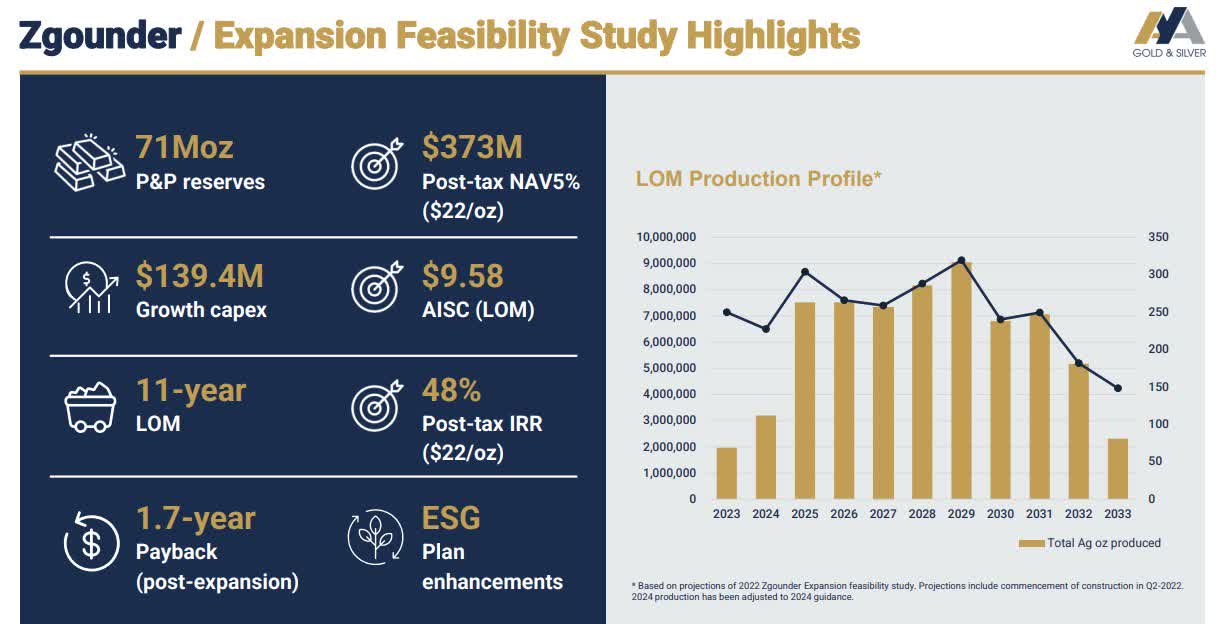

After the new Zgounder mill reached commercial production in December 2024, the mine produced 1.1 million ounces of silver in the first quarter of 2025. Following the earnings release, Aya's stock sold off sharply as cash costs came in at $18.93 per ounce, which is much higher than the all-in sustaining costs of $9.58 per ounce expected in the Feasibility Study released in February 2022. During the quarter, Aya encountered issues with the oxygen plant, which was operating below capacity, resulting in lower-than-expected recoveries. Labour costs should also diminish over the coming quarters after the mill ramp-up is completed.

Zgounder Expansion Highlights (May 2025 Presentation)

What impresses me the most about the Zgounder Project is its achievement on a $140 million budget. According to management, the price tag for a similar project could have been between $400 million and $500 million in North America. The regulatory and permitting processes would have been much longer, too. The pattern would also have been similar when it comes to labour and energy costs.

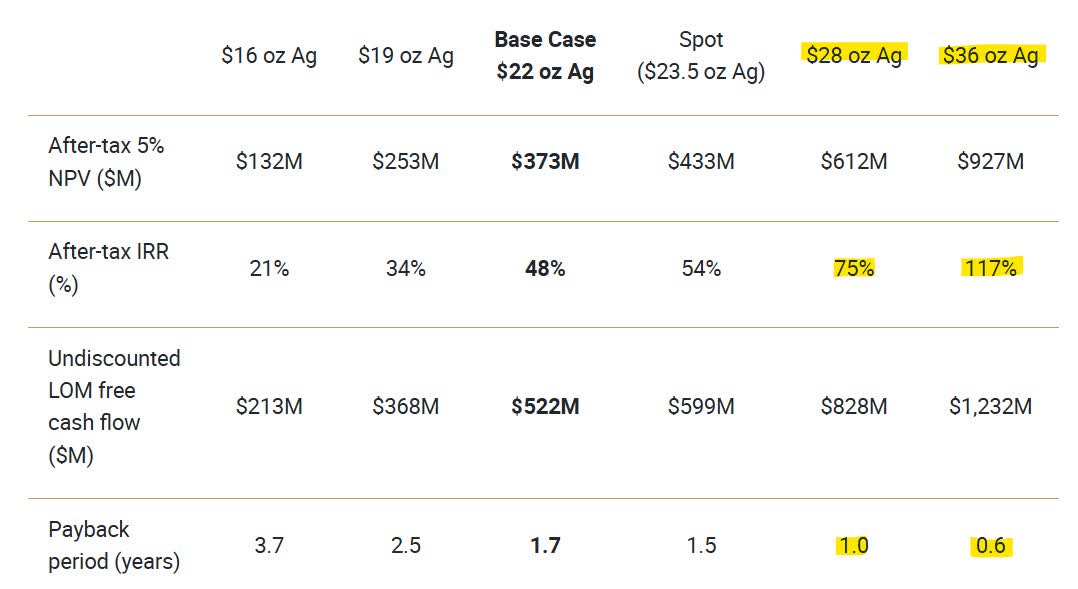

With low initial capital requirements and production costs, the payback period is expected to be around one year, with an after-tax internal rate of return estimated at 75% using a realistic silver price of $28.00 per ounce. As illustrated below, the project's after-tax IRR increases to 117%, and the payback period diminishes to just a few months using a silver price assumption of $36.00 per ounce.

Zgounder Project Economics (February 2022 Press Release)

With an average annual production of ~6.8 million ounces over an 11-year mine life, the Zgounder Project is of similar size to Endeavour's Terronera Project, which entered wet commissioning in early May 2025. Once at full production, Terronera is expected to produce ~7.0 million ounces of equivalent silver after capital expenditures of around $230 million. Using a silver price assumption of $26.00 per ounce, Terronera's IRR is estimated at 34.6%, so about half of what is expected from Zgounder.

Once Zgounder reaches full production, Aya will also approach MAG in terms of production volume. For the full year of 2024, Juanicipio produced 23.0 million ounces of silver equivalent, of which 44% or 10.1 million ounces was attributable to MAG's shareholders.

In any case, the economic parameters from Zgounder's feasibility study certainly look great, but it is now time for Aya to support those numbers with tangible cash flows.

Boumadine Project

The second-largest asset in Aya's portfolio is an 85% interest in the Boumadine Project, also located in the Kingdom of Morocco. The remaining 15% interest is owned by the Office national des hydrocarbures et des mines, also known as ONHYM, a public institution with the mandate of developing natural resources inside the country's borders. Between 1950 and 1992, historical underground mining operations occurred on the property.

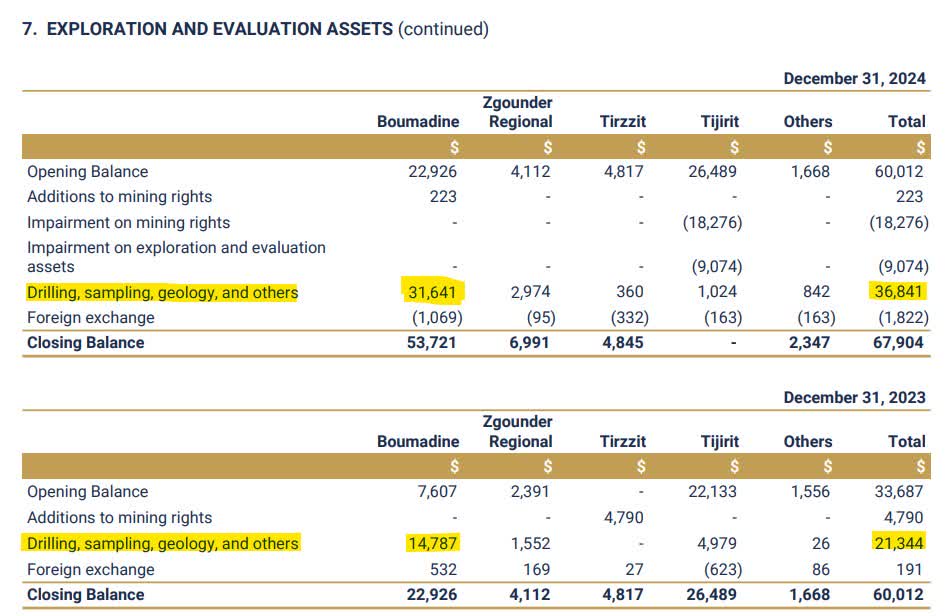

Over the last few years, Aya deployed a meaningful amount of capital to advance exploration on the property, notably with a 76,000-meter drilling program in 2023, followed by a 108,000-meter program in 2024. According to the company's guidance, another ~120,000-meter drilling program is planned for 2025. As illustrated below, Boumadine's drilling and other exploration expenses amounted to $14.8 million and $31.6 million in 2023 and 2024, respectively.

Exploration Assets (2024 Annual Report)

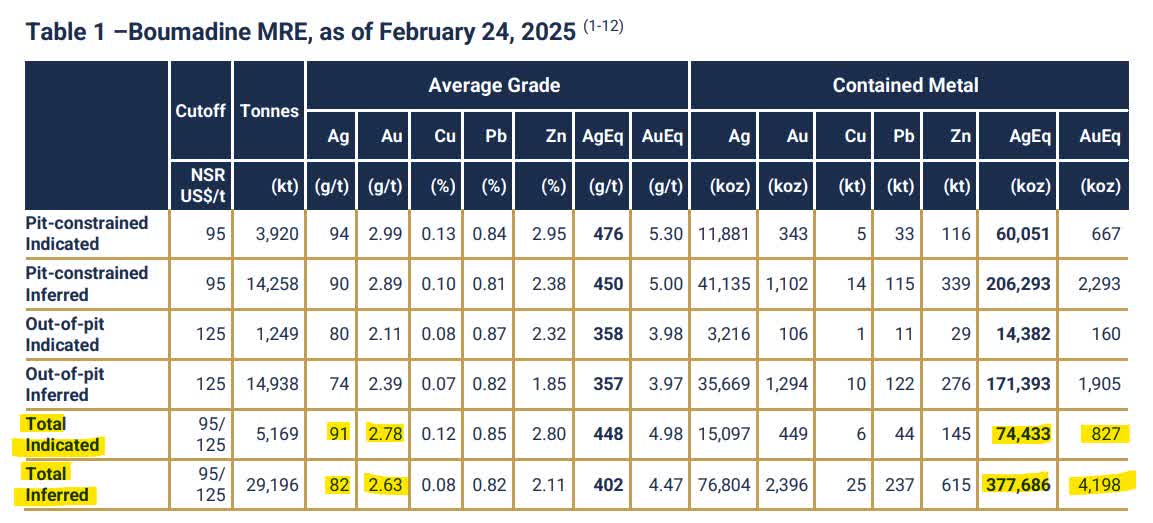

After investing almost $50 million in exploration over the last two years or so, Aya reported an updated mineral resource estimate on the project in February 2025. The revised estimates include 74.4 million silver-equivalent ounces in the indicated category and 377.7 million silver-equivalent ounces in the inferred category. Whether it is in the indicated or inferred categories, silver itself accounts for only 20% of total silver equivalent ounces, highlighting Boumadine's meaningful exposure to gold, lead and zinc.

Boumadine Mineral Resource Estimate (2025 Mineral Resource Estimate)

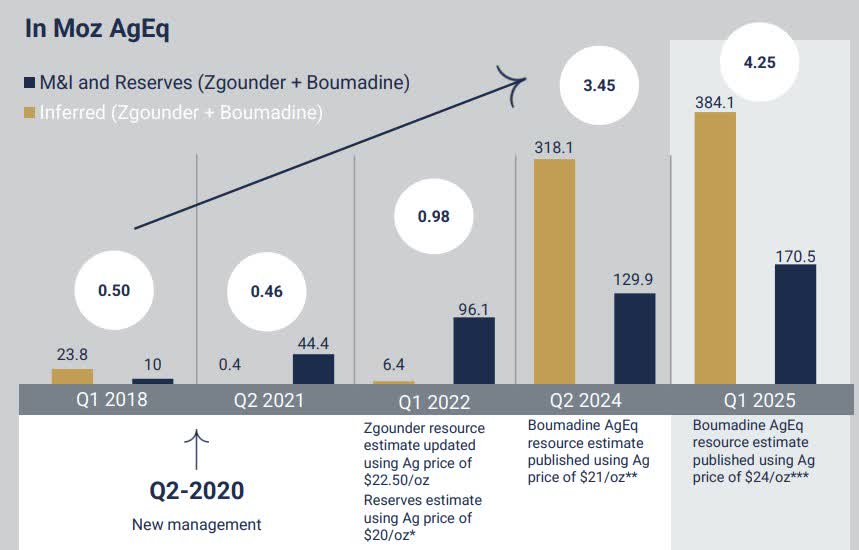

Aya has done a good job growing Boumadine's resources, but considering the project's early-stage nature and the amount of capital deployed towards exploration, reinvestment risks are real. Once in full production, Zgounder will generate meaningful free cash flows, of which a significant proportion will be reinvested in the Boumadine Project.

Boumadine Historical Mineral Resource (May 2025 Presentation)

On a personal note, I find the Zgounder Mine highly attractive to gain exposure to spot silver prices. If the numbers included in the feasibility study can be reproduced in the real world, Zgounder would become my second favourite asset in the silver mining industry, after Fresnillo's Juanicipio and in front of Endeavour's Terronera mine. However, my main source of skepticism surrounding Aya is capital allocation, and more precisely, the reinvestment of Zgounder's free cash flow into an early-stage exploration property.

Conclusion

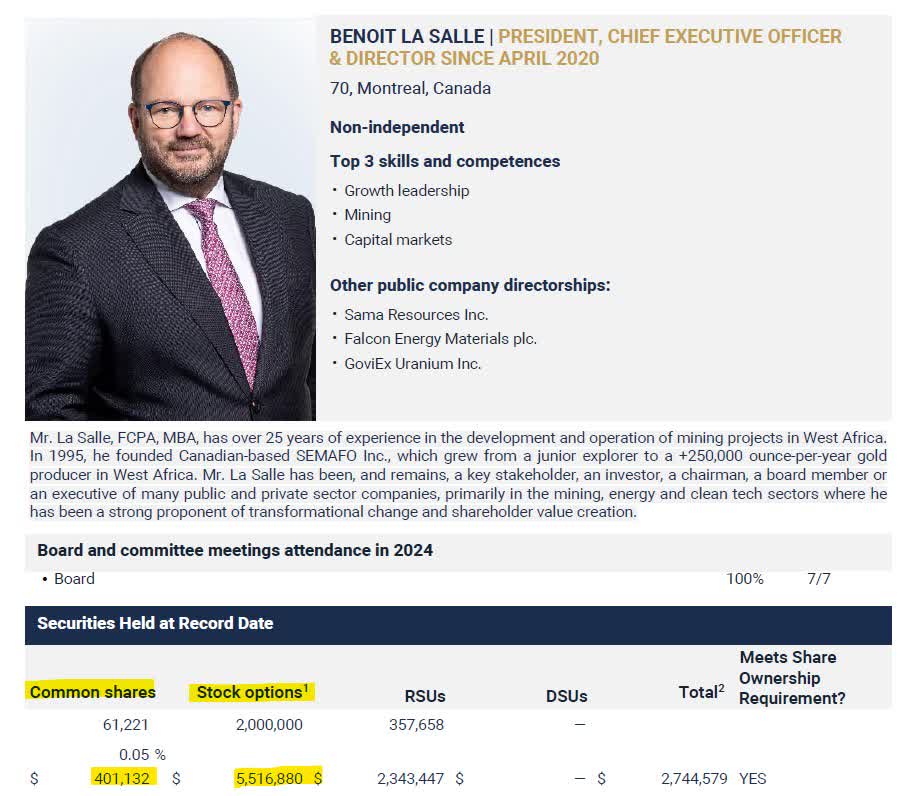

Benoit La Salle, Aya's president and chief executive officer, had prior success in West Africa after founding SEMAFO in 1995. The company evolved from a junior explorer to a gold miner producing over 250,000 ounces per year. In August 2012, after the announcement of operational challenges at the Mana Mine in Burkina Faso, Mr. La Salle announced that he was stepping down from his role as president and CEO. SEMAFO's story ended in March 2020 when Endeavour Mining (EDV:CA) announced an all-stock buyout offer valued at CAD$1.0 billion.

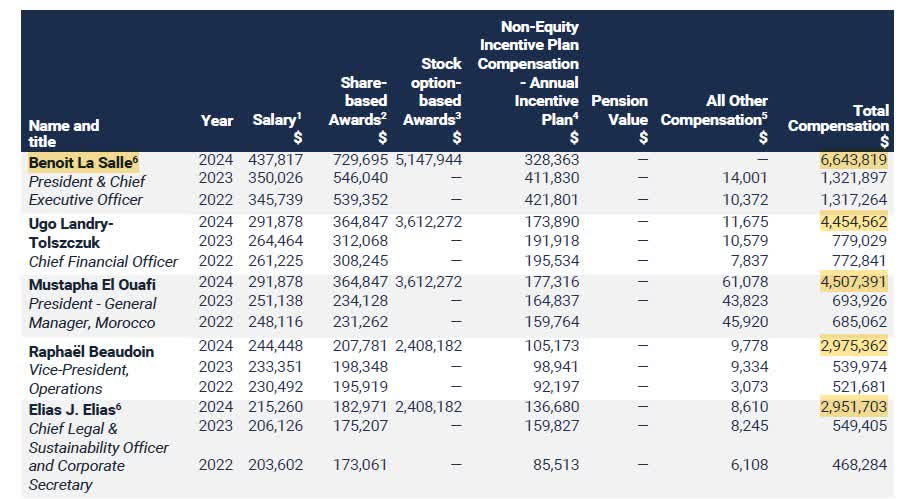

Just a few weeks later, in April 2020, Mr. La Salle was appointed as Aya's president and CEO. Following Aya's reorganization and SEMAFO's buyout, many former SEMAFO executives joined Aya's team. In a way, Aya's story in Morocco could be seen as a sequel to SEMAFO's story in West Africa, a kind of SEMAFO 2.0. However, I was surprised to discover that Mr. La Salle owns only ~60,000 shares of the company he leads, which is quite small relative to his 2.0 million stock options and ~360,000 RSUs.

Benoit La Salle Profile (2024 Management Information Circular)

On top of a generous compensation, Aya also disclosed in its most recent financial statement the payment of management and consulting fees of approximately $100,000 per month to Group La Salle, a company owned by Mr. La Salle.

Related Party Transaction (Q1-25 Financial Statement)

When we look at Aya from the standpoint of minority shareholders, the picture is slightly different, as they receive no compensation for sitting on the board of directors, no stock options, no management and consulting fees and no salary. In fact, the only way for minority shareholders to make money is via a higher share price or through dividend payments. At the end of the day, what kind of power can small shareholders like you and me have?

Management Compensation Table (2024 Management Information Circular)

Unfortunately, with Boumadine's early-stage nature and the large capital requirements associated with its development, minority shareholders may not fully taste the free cash flows from Zgounder. I feel like it is often the case with mining; minority shareholders rarely taste the fruits of their investment. When something is indeed successful, the money is poured back into other projects. The problem is that we all know how difficult it is to compound capital in mining. Instead of compounding, I would prefer a model of redistribution, and I will take care of the compounding myself. In today's market, this strategy seems increasingly rare, or even non-existent.

For the company itself and for the people in positions of control, it may make perfect sense to reinvest Zgounder's free cash flows into an early-stage exploration project. In fact, developing the precious metal mining industry in Morocco may be part of a deal with the local government to obtain permits. Even if no deal of this kind were signed, what message would it send to Morocco's government if Aya were to return most or even all of Zgounder's cash flows back to its foreign shareholders?

My 'Hold' rating reflects my optimism regarding Zgounder's free cash flow generation, but also my concerns about the reinvestment risks associated with the Boumadine Project. As a minority shareholder seeking exposure to silver prices, I want to minimize exploration and development risks as much as possible. At the end of the day, there are no agency risks associated with owning the metal itself; there is no management team between my capital and the assets purchased. Before accepting the presence of a third party in the equation, I want to make sure our financial interests are aligned.

I will continue to follow Aya's story closely in the upcoming quarters. Before upgrading my 'Hold' rating, I would have to gain additional conviction on Boumadine's near-term development potential. Additionally, Zgounder still has to replicate in the real world the economic parameters included in the project's feasibility study. It is time to show in the real world what was on paper just a few quarters ago.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.