phive2015/iStock via Getty Images

Investment thesis

Shares of Perion (NASDAQ:PERI) reacted negatively to Q4 results and FY25 guidance, a trend that has become common for the past several quarters. While I acknowledge the outlook for this year was underwhelming, as its larger revenue contributors continue to face revenue declines, I do see some positives that help me maintain my confidence in the investment case for PERI stock. Perion's three growth areas continue to perform well, and management's Perion One strategy looks promising. However, as the Search business and Open Web continue to decline going forward, it will put pressure on top-line growth. Nevertheless, with the current market cap nearly equal to the net cash position and strong FCF generation expected this year, I still find the risk-reward attractive and maintain my Buy rating.

Key takeaways from Q4 results and FY25 guidance

While Q4 results showed total revenue and adjusted EBITDA down 45% and 71%, respectively, they came in within management's guidance. However, investors need to dig deeper to understand the underlying dynamics given the drastic changes that have taken place in recent quarters. Search Advertising revenue of $25.5 million was down 78% year over year following the loss of Microsoft (MSFT) Bing as a customer. Given that Search Advertising is no longer a priority for Perion, I will not focus on this going forward.

Q4 Earnings Presentation

Turning to Perion's other business segment, which is Advertising Solutions, it had revenue of $104.1 million, which was down 13% year over year. A headwind impacting Advertising Solutions has been the lower Open web video revenue, which was down 61% year over year, as shown above. While this weakness is partly attributed to lower demand from customers, it is also because management has down-prioritized it in favor of its faster-growing areas.

The three growth areas going forward for Perion remain CTV, Digital Out-of-Home ("DOOH"), and Retail Media. Growth for these in Q4 was 10%, 57%, and 34%, respectively. I expect all of them to continue to put up strong numbers in 2025, as they each benefit from industry tailwinds in CTV, DOOH and retail media, which should help lift overall growth as they gradually become a larger portion of total revenue.

With Open web still representing 58% of Advertising Solutions revenue in Q4, declining revenue here will continue to weigh on topline growth despite strong growth elsewhere. Based on management guiding for 80% of FY25 revenue of $410 million at the midpoint, expected from Advertising Solutions, this translates to $328 million in Advertising Solutions revenue, and implies a 3% year-over-year decline versus FY24.

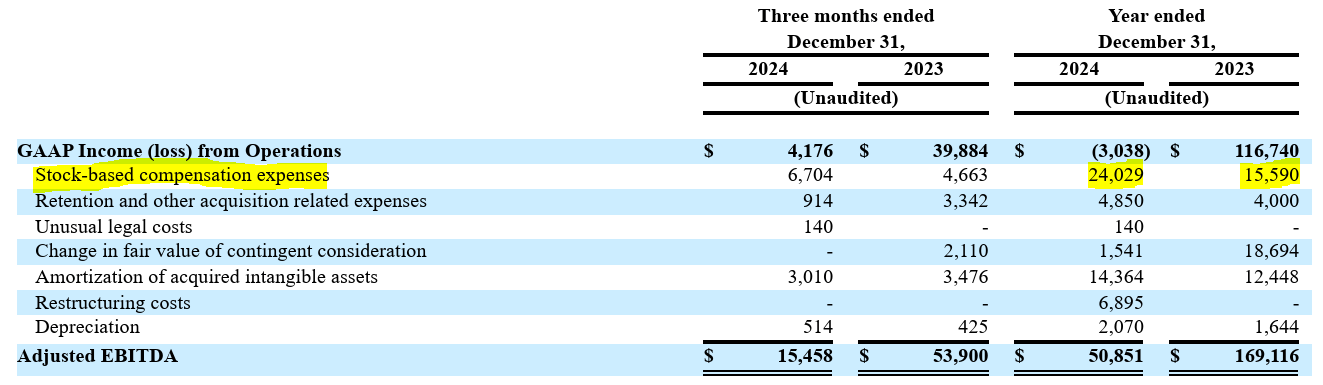

Despite the drastic drop in Search revenue and modestly lower Advertising Solutions revenue expected for FY25, Adjusted EBITDA guidance of $41 million at the midpoint shows that efficiency measures and headcount reductions are helping to protect margins. While Adjusted FCF in FY24 of $16.6 million was well below Adjusted EBITDA of $50.9 million, it was impacted by unfavorable working capital related to the Microsoft Bing contract and the acquisition of Hivestack. For FY25, investors can expect FCF to closely track Adjusted EBITDA, a trend that consistently occurred in prior years.

What makes me stay bullish on the stock

While there were limited positives to be taken from the Q4 results, apart from the performance of the three growth businesses, the biggest factor that makes me stay positive on the stock is its valuation. With $373 million in cash and no debt, Perion's net cash position represents nearly 93% of the current market cap of just over $400 million.

It is not difficult to argue that the profitable Advertising Solutions business, which is expected to generate $328 million in revenue for FY25, should be worth at least 7% of the current market cap or $30 million. Even conservatively, I would value this business at a Revenue multiple of 1, as it should have steady state margins of close to 10%. When added to the value of its cash, this implies a total value of $700 million, or $14.8 per share.

Q4 Earnings Presentation

While the market remains skeptical with respect to execution by management, especially given the missteps that occurred last year, I see the Perion One strategy as being a promising move. Through Perion One, all of its offerings, which include CTV, DOOH, retail media, social, and open web, would be brought under a single platform solution. This would make its product offering stronger while also reducing marketing costs. As a part of this strategy, I also agree with the move that management is making to down-prioritize open web in favor of its growth segments, given that open web is a crowded space where Perion has less differentiation. Highlighting the significance of Perion One on the earnings call, its CEO stated:

The role of Perion One is to solve the complexity of omnichannel advertising and provide a unified AI-driven advertising infrastructure that deliver precision, efficiency, and measurable results.

While I am encouraged by the fact that the company has the right ingredients in place to make this strategy work, I do acknowledge that there is execution risk here. However, at the current valuation, investors are not being asked to pay up for this, which makes the risk-reward setup compelling.

Risks to consider

Investors need to realize that a return to top-line growth in 2026 depends heavily on the company's three growth businesses continuing their current momentum. The remaining business lines are gradually shrinking and will remain a headwind to overall revenue growth.

Meanwhile, given the fact that Perion's massive net cash position represents a substantial portion of the current market cap, prudent capital allocation is crucial to increase shareholder returns. Given that significant capital is being deployed towards share repurchases, with management's commentary suggesting that the main focus will be on delivering organic growth under Perion One, I think it is less of a concern that the cash will be spent inefficiently.

Q4 Financial Report

Another concern I have been sharing in my previous writeups is related to the company's stock-based compensation ("SBC") expenses, which increased significantly in FY24. Due to the resulting dilution, the company's shares outstanding are only marginally lower, despite spending $46.9 million on buybacks during 2024. If I do not see SBC expenses leveling off in the coming quarters, especially with revenue declining, I will become more concerned.

Conclusion

Though Perion's guidance for 2025 was underwhelming, I remain positive on the company due to the strong performance of its three fast-growing areas in CTV, DOOH, and Retail Media. The Perion One strategy appears promising, and the current valuation shows that the market remains skeptical with regard to management's ability to execute on their plan. I see limited downside from current levels due to the massive cash position and therefore maintain my Buy rating as the risk-reward remains favorable.