panumas nikomkai/iStock via Getty Images

Last December, I initiated my coverage on Applied Digital Corporation (NASDAQ:APLD) with a strong buy rating due to its potential to emerge as a leading provider of HPC AI data centers. Since then, the stock is down 58% as a result of delays to its multi-billion lease agreement with a US hyperscaler, leading to higher cash burn.

Seeking Alpha

The stock’s drop was exacerbated by its recently announced Q3 FY 2025 earnings due to underwhelming revenue growth in its cloud services segment. At the same time, Applied Digital announced that it’s exploring opportunities to sell its cloud services segment, as part of its strategy to transition into a REIT in the future.

Despite this, I believe a sale of the cloud services segment could provide the company with ample cash to continue building out its Ellendale campus, which presents the biggest revenue opportunity thanks to demand from hyperscalers’ for data center capacity. In light of this, I’m reiterating my strong buy rating for Applied Digital, but lowering my price target to $47 by mid-2028, to account for the reduced revenue from the sale of the cloud services segment and the transition to a REIT, which still implies 1255% upside from current levels.

Q3 Overview

In Q3 FY 2025, Applied Digital reported 22% YoY revenue growth from $43.3 million to $52.9 million, driven by 220% growth in the cloud services segment from $5.5 million to $17.7 million, offset by a 7% decline in the data center hosting segment from $37.8 million to $35.2 million. While the growth in the cloud services segment may appear significant, it was a 36% sequential decline due to technical issues in moving GPU capacity from single-tenant reserve contracts to a multi-tenant on-demand model. Per management in the Q3 earnings call, these issues were resolved in the first or second week of March, which could see this segment generate revenues at a similar rate to Q2 during Q4.

In terms of costs, Applied Digital showed impressive cost management during Q3 as it reported a gross margin of 7.1% compared to -8.6% in the prior year.

At the same time, SG&A costs declined 24.3% YoY from $30 million to $22.7 million, meaning that they represented 43% of revenues in Q3 2025 compared to 69.3% last year. Accordingly, the company’s operating loss improved by 65.8% YoY from $55.4 million to $18.9 million, at an operating margin of -35.8% compared to -127.9% in the prior year, a sign of improving efficiency.

In terms of cash flow, Applied Digital reported $5.9 million in operating cash flow, a substantial improvement from $52.3 million and $75.9 million in operating cash outflow in Q1 and Q2 2025, respectively. Meanwhile, CapEx reached $257.5 million in Q3 as the company ramps up its efforts to complete the build out of its Ellendale data center, compared to $171 million and $54.8 million in Q2 and Q1, respectively. As such, the company’s cash burn increased from prior quarters as free cash outflow came at $251.6 million in Q3 compared to $223.3 million and $130.7 million in Q2 and Q1, respectively.

As for its balance sheet, Applied Digital exited Q3 with a cash balance of $68.7 million and had restricted cash of $185.5 million, including $154.1 million in funds for construction and $31.3 million in letters of credit. Meanwhile, the company has $689.1 million in total debt, of which $679 million are long-term debt, $386.1 million of which matures in FY 2027, bringing its net debt position to $434.9 million. Therefore, it is crucial for the company to finalize the lease agreement with the hyperscaler for its Ellendale data center in the near-term in order to deal with the debt mountain maturing in FY 2027.

REIT Transition

For the first time since announcing its strategic shift to building and leasing HPC data centers, Applied Digital’s management mentioned a future transition into a REIT, in the Q3 earnings call. According to this new strategy, the company has authorized the sale of its cloud services segment.

The company’s decision was driven by potential data center customers viewing this segment as a competitor, which has been a “point of friction” in negotiations, per management in the Q3 earnings call. In my opinion, this decision comes at an opportune time to capitalize on CoreWeave’s (CRWV) recent IPO. Currently, Coreweave is trading at a 4.96 sales multiple and Applied Digital’s management reiterated that they see the cloud services business to be a $110 to $120 million business.

At the midpoint of management’s expectations, and CoreWeave’s valuation, the cloud services segment could be sold for $570 million. These funds would provide the company with enough capital to continue building out its portfolio of HPC data centers, while minimizing its exposure to debt financing, reducing its interest expenses in the process.

By selling off this segment, Applied Digital vision of transitioning into a REIT would be possible since it will be mainly focused on operating its Bitcoin hosting and HPC data center segments, both of which fit into a REIT structure. In fact, management stated in the Q3 earnings call that the company may look to add more Bitcoin capacity along with HPC capacity, an endeavor that I expect to see demand from Bitcoin miners due to Bitcoin’s current prices.

In my opinion, Applied Digital’s new strategy is mainly driven by its partnership with Macquarie Asset Management. This partnership is a $5 billion perpetual preferred equity financing facility, with investment vehicles of funds managed by Macquarie, for the company’s HPC business. According to Applied Digital, Macquarie’s committed funds provide the majority of the funds needed to build more than 2 GW of HPC data center capacity.

At the same time, partnering with an institution as Macquarie validates Applied Digital’s HPC data center plans due to Macquarie’s reputation as a major financial institution. As is, management stated that Macquarie is aiding its negotiations with customers for the lease of the Ellendale data center, which may alleviate customer fears over Applied Digital’s ability to execute on its targets.

Revenue Projections

With Applied Digital exploring opportunities to sell off its cloud services business, I’m updating my revenue estimates for the company through FY 2028.

Cloud Services Segment

Starting with the elephant in the room, the cloud services segment generated $71.3 million in revenue YTD. As the technical issues that hindered the segment’s revenue generation during Q3 are now solved, I expect the segment to return to the same rate as Q2.

This could see the segment generate around $99 million in FY 2025.

Additionally, I expect the sale of this business to occur in Q2 FY 2026, at least, which could see this segment generate around $27.7 million in revenue in Q1 2026.

Data Center Hosting Segment

Per Applied Digital’s latest 10-Q filing, its 286 MW Bitcoin mining facilities are operating at full capacity and generate around $35 million in quarterly revenue. Accordingly, I’m estimating this segment to generate around $140 million in annual revenues, unless Applied Digital leases more capacity or renews its leases at a higher price.

HPC Data Center Segment

As for the HPC data center segment, Applied Digital is yet to realize revenues from this business as it continues to prepare the first building at the Ellendale data center to start operating soon. In the Q3 earnings call, management stated that the first building will be ready to generate revenues in Q4 CY 2025, or Q2 FY 2026. Meanwhile, the company expects the second building to be ready for operations at the end of Q2 CY 2026, or Q4 FY 2026, and the third building to be ready in Q1 CY 2027, or Q3 FY 2027.

With that in mind, my estimates assume the first building to generate revenues from Q2 FY 2026 and the second building to generate revenues in Q4 FY 2026. I’m also estimating the third building to start generating revenues in the second half of FY 2027.

My estimates are also based on the per MW pricing of the initial lease announcement of $2.2 million per year, as shared in my previous coverage on Applied Digital.

Accordingly, my revenue estimates for the HPC data center segment through FY 2028 are as follows.

By adding my estimates for all segments, my revenue estimates for Applied Digital through FY 2028 are as follows.

Valuation

Based on my revenue estimates, I believe Applied Digital as a bargain at its current share price of $3.44. At this valuation, the company has an EV of $1.2 billion, which translates to the following EV/sales multiples through FY 2028.

In comparison, data center REITs Equinix (EQIX) and Digital Realty (DLR) are trading at the following EV/sales multiples.

By applying the average EV/sales multiple of both REITs to my revenue estimates for Applied Digital through FY 2028, my price target for the stock is as follows.

Own Calculations

Technical Analysis

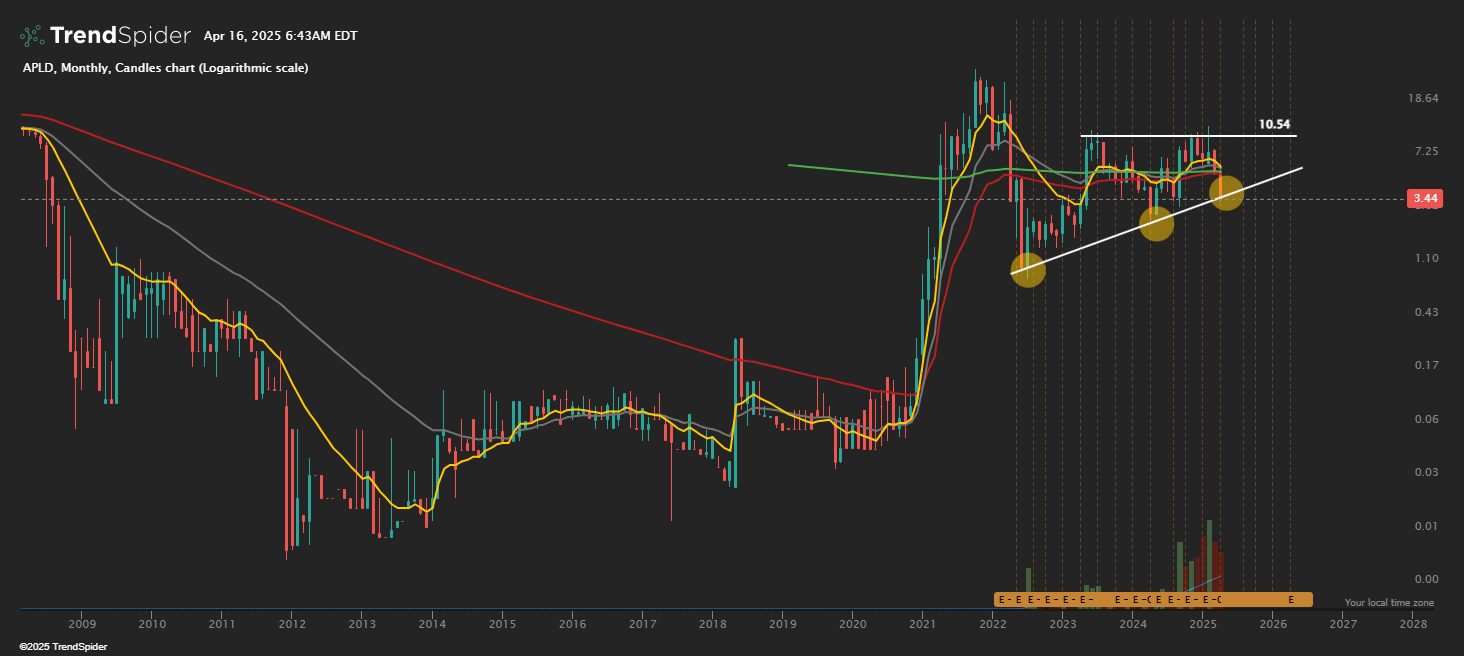

TrendSpider

Looking at the TrendSpider chart above, Applied Digital appears to be in a bullish triangle pattern on the monthly chart. Currently, the stock is testing the lower trendline of the pattern, a level that has seen the stock previously run to test the resistance level at $10. As such, if Applied Digital maintains the lower trendline as support, I expect the stock to rebound near the $10 mark to test its resistance, which offers around 200% upside from the current stock price. Possible catalysts that could help Applied Digital retest the $10 resistance include the announcement of the lease agreement with a hyperscaler for the Ellendale data center and the sale of the cloud services business if the sale price is near my estimate, in my opinion.

Risks

Risks to my bullish thesis on Applied Digital include additional delays to announcing the lease agreement for the first building of the Ellendale data center. As mentioned earlier, the company needs to start generating free cash flow before FY 2027 when $$386.1 million of its debt matures. Therefore, additional delays to announcing the lease agreement could continue to pressure the stock price.

Another risk to consider is the recent tariffs imposed by the Trump administration. While the tariffs won’t impact the first building of the Ellendale data center, construction costs of the 2 additional buildings could increase substantially due to the tariffs. As is, management stated in the Q3 earnings call that its data center CapEx is between $30 to $50 million per month, and the added costs brought by the tariffs could see the company’s cash burn accelerate significantly.

Conclusion

In conclusion, I remain bullish on Applied Digital despite the delays in announcing the lease agreement for its Ellendale data center. With the first building near completion, I expect the lease agreement to be announced in the second half of 2025, especially with Macquarie involvement with the company, which validates its plans, in my opinion. Moreover, I expect Applied Digital to receive around $570 million from the sale of its cloud services segment, which will provide the company with much-needed liquidity to reduce its exposure to debt financing. After accounting for the loss of revenue from the cloud services segment, I’m reiterating my strong buy rating for Applied Digital at its current depressed valuation, while lowering my price target to $47 by mid-2028, implying 1255% upside from current levels.