Sashkinw

How far $1 million can go in retirement largely depends on how you invest that money. For one thing, if you put it all into the S&P 500 (SPY), then you’d be getting $12,100 annually, based on the current 1.21% dividend yield. If one needs more than that to fund living expenses, then they’d have to dip into their principal to make up for the shortfall.

While that may be an easy thing to do in a growth market, selling down an index fund can be tricky thing to maneuver in the volatile market that we find ourselves in now. Income investments can greatly buffer against market headwinds by providing investors with a steady stream of cash. In fact, BDCs and REITs are required to distribute 90% of their taxable income to shareholders lest they want to lose their tax advantages.

This brings me to the following two names, which currently carry yields in the 7% to 10% range. Both operate in different industries and are also diversified by owning a wide asset base. In this article, I highlight what makes each a solid ‘buy’ at present for great income and potential appreciation, so let’s dive in!

#1: Morgan Stanley Direct Lending (MSDL)

Morgan Stanley Direct Lending is a BDC that’s externally-managed by none other than the well-known investment firm, Morgan Stanley (MS). Like other large peers Ares Capital (ARCC) and Blackstone Secured Lending (BXSL), MSDL is focused on lending to the U.S. middle market. Like BXSL, MSDL also has a low base management fee of 1.0%, comparing favorably to the 1.5% of ARCC.

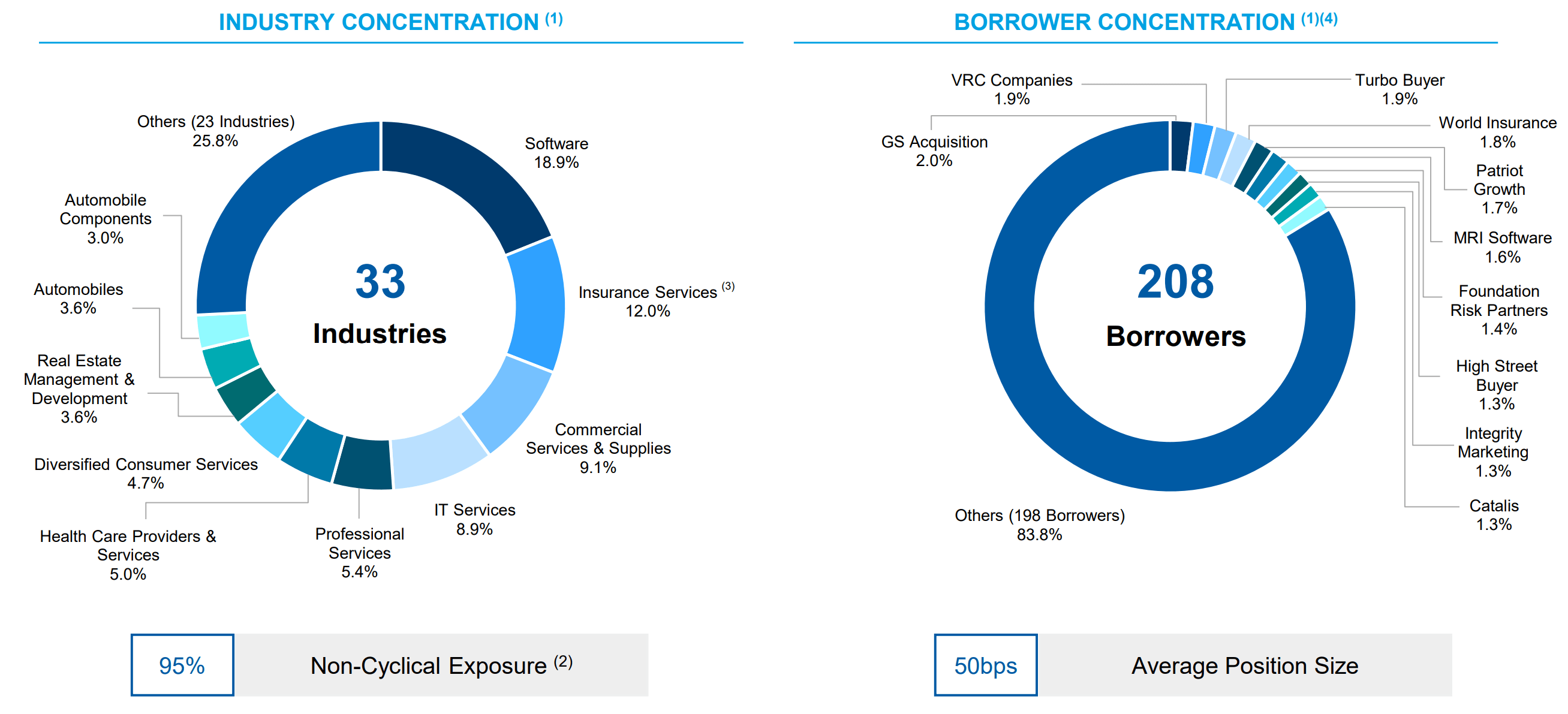

MSDL focuses on industries that are non-cyclical, which represent 95% of portfolio value, and have low capital requirements. Its investments have solid equity buffers to protect MSDL’s debt instruments, as reflected by the weighted average loan-to-value ratio of 40%.

Moreover, 96.5% of MSDL’s loans are in the safer first lien secured debt category, which stand first in line for recovery of capital in the event of a borrower default. Its portfolio companies are well-diversified by industry, with software, insurance, commercial services and IT Services making up just under half (49%) of portfolio value. The average hold size sits at just 0.5% of portfolio total and no single investment makes up more than 2%, as shown below.

Investor Presentation

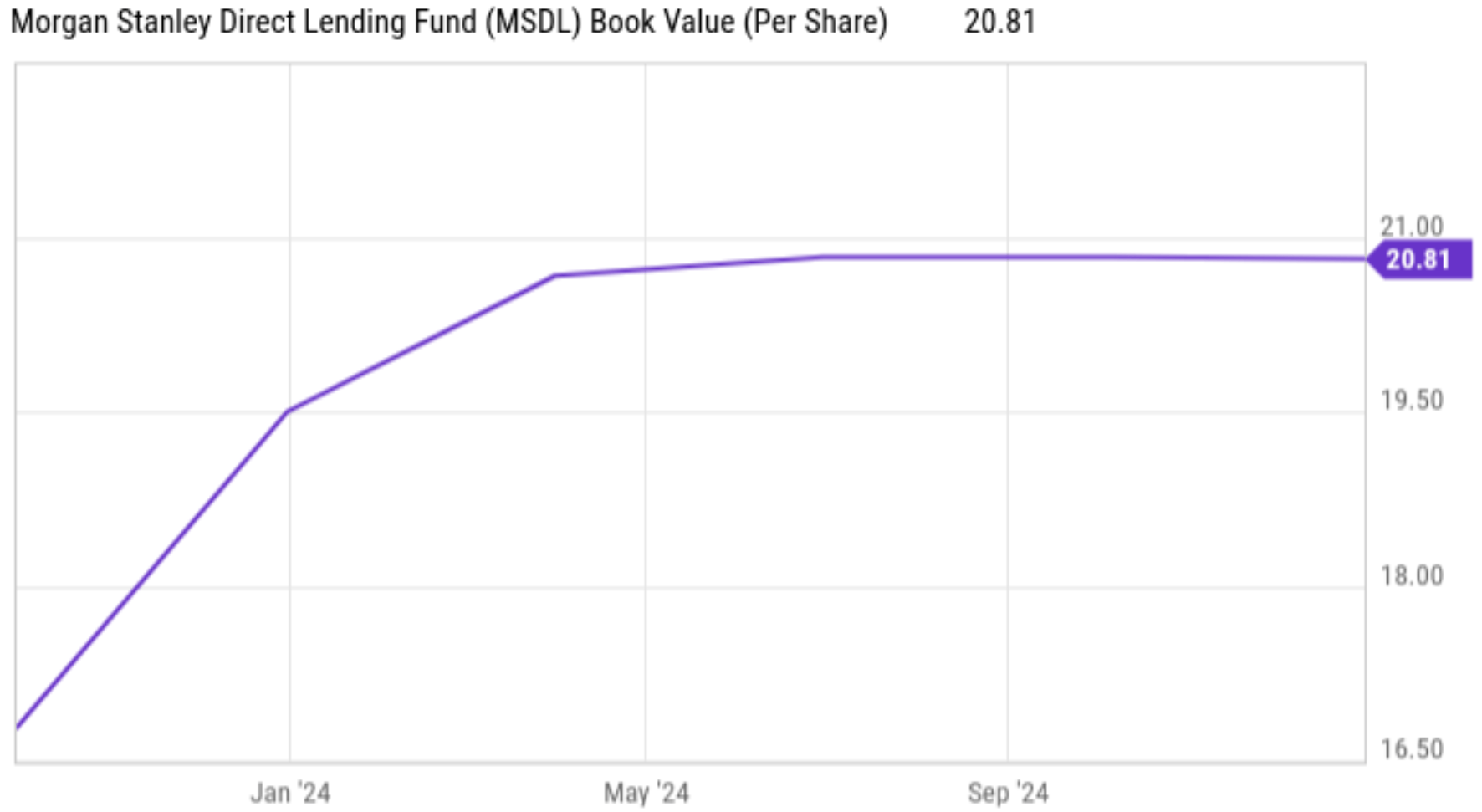

MSDL demonstrated steady financial performance its Q4 2024 results, with NAV per share remaining steady at $20.81, which is down by just $0.02 on a sequential basis. As shown below, NAV per share has remained stable since the middle of last year, after rising from the ~$16.50 at inception in 2023.

YCharts

Q4 Core NII per share came in at $0.57, which is down by $0.05 on a sequential basis due entirely to the interest rate cut during this time. Nonetheless, NII still provided 114% coverage over the $0.50 quarterly dividend rate. MSDL committed $188 million in new investments during Q4 with a net funded deployment of $144 after adjusting for repayments. At the same time, MSDL generated a respectable portfolio yield of 10.4% at cost.

Portfolio credit remains solid with a very low non-accrual rate of just 0.20% at portfolio cost. The percentage of investments with internal credit ratings of 1 or 2 stood at 98.3%. This is on a scale from 1-4, with 1 being the highest quality. At the same time, the percentage of the portfolio with internal ratings of 3 and 4 sits at 1.7%, which is 20 basis points lower compared to 1.9% in Q2, as shown below.

Investor Presentation

Looking ahead, MSDL is well-positioned to make opportunistic investments as it carries a safe debt-to-equity ratio of 1.08x, sitting well below the 2.0x statutory limit for BDCs. Management sees potential for improved deal flow this year with the return of leveraged buyout activity, as noted during the recent earnings call:

Shifting to deal volumes, it was constructive to see a modest pickup in LBO activity during 2024 and private credit remains the funding source of choice for LBOs. Prospectively, we believe that activity will continue to accelerate due to the combination of anticipated deregulation, healthy public and private financing markets, significant private equity, dry powder and aging sponsor portfolios.

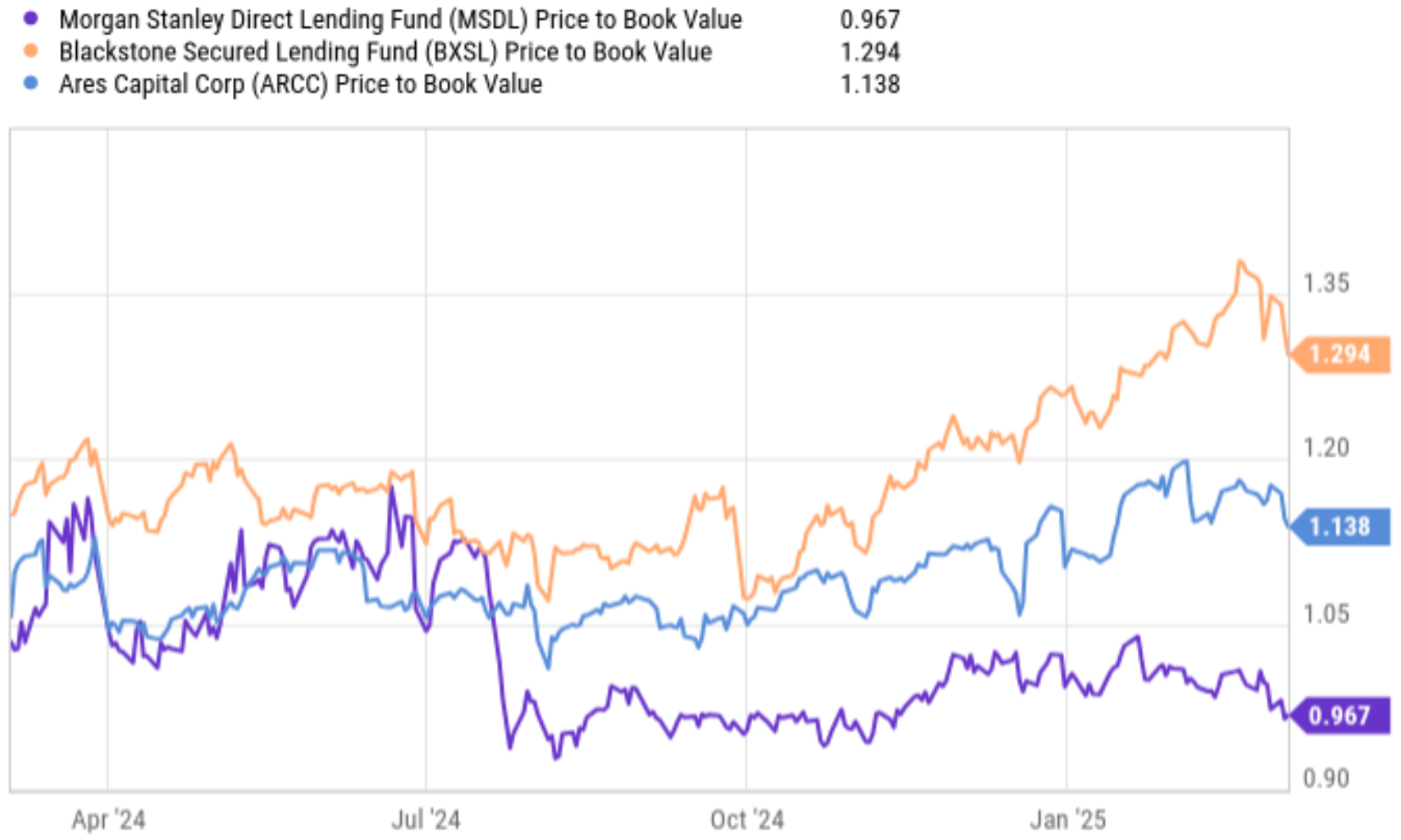

Turning to valuation, MSDL appears to be attractive at the current price of $20.13, which equate to a price-to-book value of ratio of 0.97x. This compares favorably to peers ARCC and BXSL, which carry P/Book ratios of 1.14x and 1.29x, respectively, as shown below. With a 10% dividend yield that’s well-covered by NII, robust portfolio credit and a strong balance sheet, MSDL appears to be a solid high income investment at present.

YCharts

#2: Broadstone Net Lease (BNL)

Broadstone Net Lease is a REIT that specializes in owning and acquiring single-tenant commercial properties. At present, it has 765 properties across 44 U.S. states and 4 Canadian provinces. BNL’s portfolio is comprised of 60% Industrial (by annual base rent), 31% Retail, 6% Office, and 3% Clinical Surgical.

The portfolio is also diversified across 202 tenants in 55 industries, with the top 10 tenants comprising just 22% of ABR. In similar fashion to that of net lease giants like Realty Income Corporation (O) and W. P. Carey (WPC), BNL has long weighted average lease term of 10.2 years and 2% annual rent escalators.

BNL delivered steady 2024 results, with 99.2% occupancy at year-end and AFFO per share growing by 1.4% YoY to $1.43. While this may not seem high, it’s notable because BNL was able to achieve growth amidst portfolio repositioning efforts. This included reduction of clinical / surgical assets from 9.7% at the end of 2023 to 3.2% at the end of last year.

This repositioning could have resulted in negative AFFO per share growth, yet growth was positive as BNL re-deployed capital to its core focus on industrial and retail assets. Over the past year, BNL made 405 million in total investments including $234 million worth of acquisitions, $115 million in build-to-suit developments, and $52 million in recycling capital (from the aforementioned recycling of medical-related properties). At the same time, BNL executed 7 lease rollovers with a 112% weighted average recapture rate and a new lease term of 9 years. This highlights the in-demand nature of its properties.

Management is guiding for AFFO per share of $1.47 at the midpoint of range for the full year, representing 3% growth from last year. This is supported by a robust acquisition plan of $500 million with a focus on industrial properties. Moreover, BNL has $227 million in committed built-to-suit projects that are expected to add $17.6 million in incremental ABR. Management plans to add at least $500 million to the build-to-suit pipeline this year. These projects have targeted stabilization in 2026-2027 and initial cash yields in the 7.5% range with 3% annual rent escalators.

This is supported by a strong balance sheet with BBB/Baa2 credit ratings from S&P and Moody’s. BNL also carries one of the lowest leverage ratios in the net lease sector with a net debt to EBITDA ratio of 4.9x. It has over $900 million in available liquidity and has no plans to raise equity this year.

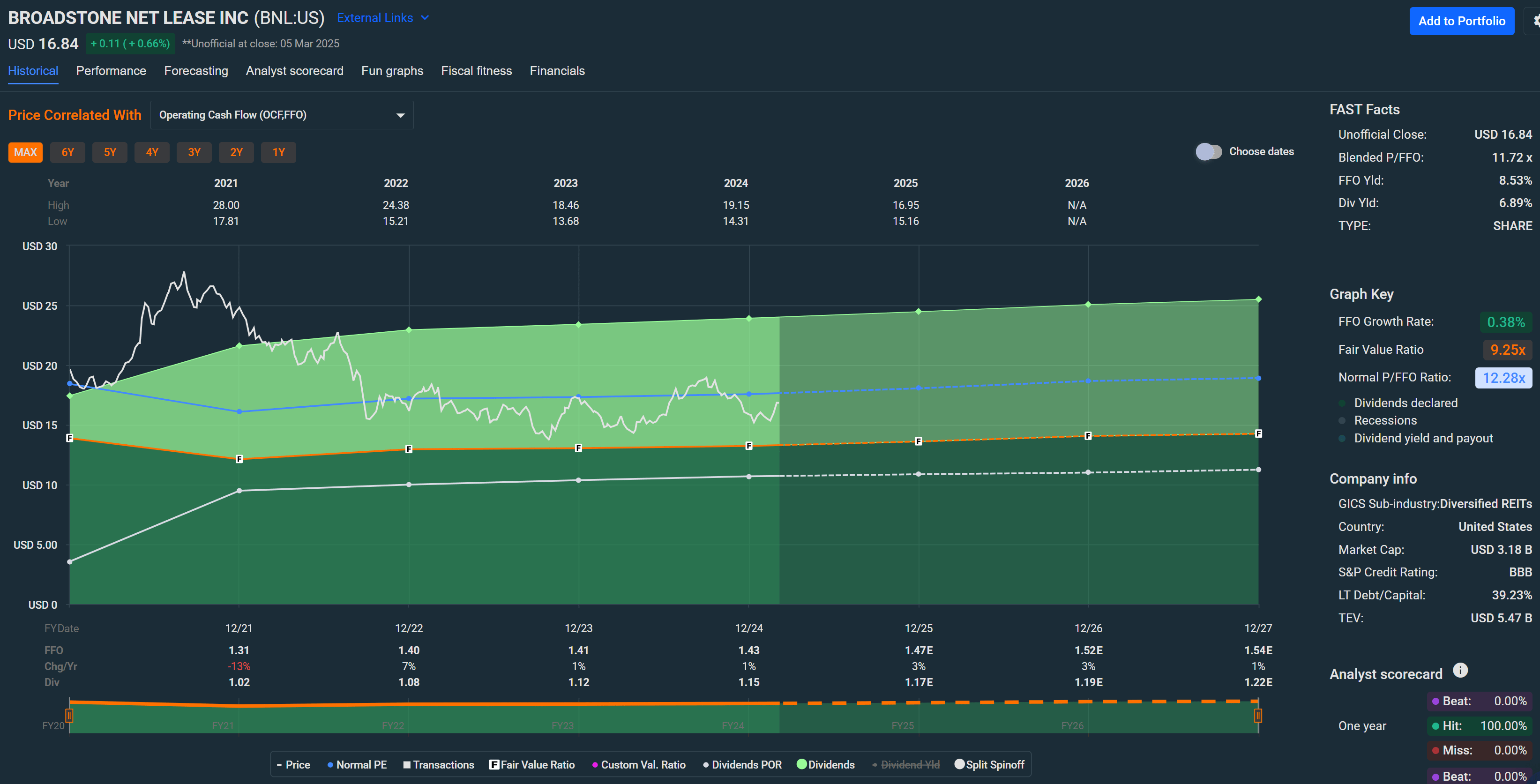

Importantly for income investors, BNL currently yields an attractive 6.9% and the dividend is well-covered by a 77% payout ratio. BNL is also attractively valued at the current price of $16.84 with a forward P/FFO of just 11.0. This sits below its normal P/FFO of 12.3, as shown below. BNL’s valuation also compares favorably Realty Income and W.P. Carey’s forward P/FFOs of 13.4 and 13.3, respectively.

FAST Graphs

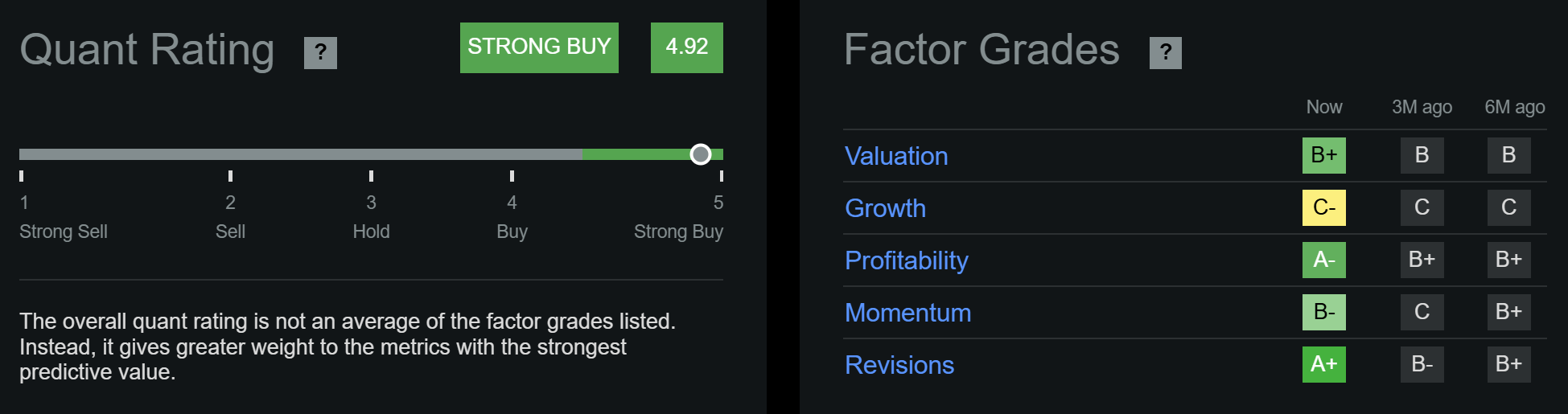

With a near-7% dividend yield and forward guidance for 3% FFO/share growth along with a potential for reversion to mean valuation, BNL could deliver potential market-beating total returns. As shown below, SA’s Quant rates BNL as a ‘Strong Buy’ with a score of 4.9 out of 5, with A and B scores for Valuation, Profitability, Momentum, and Analyst Revisions.

Seeking Alpha

Investor Takeaway

Morgan Stanley Direct Lending and Broadstone Net Lease are both attractive high income investments with attractive yields and strong operating fundamentals. MSDL focuses on middle-market lending with a primarily first-lien loan portfolio. It carries a well-covered 10% dividend yield and benefits from its low leverage and stable credit quality.

Meanwhile, BNL has a well-diversified property portfolio with long lease terms, a solid balance sheet, and a near-7% yield. This is supported by stable AFFO growth and strategic portfolio repositioning. Together, MSDL and BNL present a balanced income-focused strategy to help investors navigate market volatility while generating high income returns.

Read The Full Report on iREIT+Hoya

iREIT+HOYA Capital is the premier income-focused investing service on Seeking Alpha. Our focus is on income-producing asset classes that offer the opportunity for sustainable portfolio income, diversification, and inflation hedging. Get started with a Free Two-Week Trial and take a look at our top ideas across our exclusive income-focused portfolios.

With a focus on REITs, ETFs, Preferreds, and 'Dividend Champions' across asset classes, members gain complete access to our research and our suite of trackers and portfolios targeting premium dividend yields up to 10%.