Daniel Grizelj

It’s been a while since I last covered Fidelity National Financial (NYSE:FNF) back in December 2021, highlighting how its business was hitting on both top- and bottom-line growth, while maintaining a strong balance sheet.

It appears that my ‘Buy’ thesis on the stock has worked out well, with FNF giving investors a 37% total return since my last piece, surpassing the 32% rise in the S&P 500 (SPY) over the same timeframe, thanks in part to robust dividend growth.

In this article, I revisit FNF including recent business results and forward outlook, and discuss why it remains an attractive buy at present, so let’s dive in!

Why FNF?

Fidelity National Financial is a leading provider of title insurance, mortgage services, and diversified financial services. Its two primary business segments include Title and F&G (Fidelity & Guaranty Life), which it acquired in 2020 and provides annuity and life insurance products. As shown below, FNF holds a #1 or #2 share in 38 states, making it the dominant Title insurer across the U.S.

Investor Presentation

Purchasing the insurer, F&G, was a strategic move for FNF, as its Title business is traditionally sensitive to higher interest rates due to potential for lower demand for mortgages when rates are high. However, the insurance side benefits from higher rates, as premiums can be invested in bonds with higher yields. This dynamic enables FNF to profit in all interest rate environments.

Meanwhile, FNF demonstrated strong Q3 2024 results, with the Title segment seeing a 6% YoY operational revenue growth to $2.0 billion. This segment also maintained an industry-leading adjusted pre-tax title margin of 15.9%, though it did drop by 30 basis points from the prior year period. This was driven by steady title performance on the commercial side, while refinancing volumes declined from a daily average of 1,800 last year to 1,500.

On the F&G side, gross sales grew by an impressive 39% YoY to $3.9 billion, and it achieved record assets under management of $63 billion. This represents a robust 20% increase over the prior year period. This was driven by traction in diversified product offerings, which contributed to margin expansion.

Looking ahead, the F&G arm is expected to continue AUM growth and see expanding profitability through its diversified new business platform as it continues to scale. Plus, management expects higher commercial volumes this year as the office sector begins to transact alongside continued strength in industrial and multifamily sectors.

On the profitability front, management continues to guide for an attractive pre-tax title margin in the 15% to 20% range in the near-term, with a focus on investing in technology to drive long-term profitability, as noted below during the last earnings call:

Our technology initiatives are a key focus for investment and deployment across our operational footprint. We continue to build on our pioneering work over the last decade in instant decisioning and automated underwriting, without diminishing the coverage or value of our insurance product. At the same time, we are enhancing our customer experience throughout the transaction, while giving special attention to mitigating risk and fraud.

On the AI front, our high-quality curated data and single platform have allowed us to standardize, automate and use machine learning AI tools in many aspects of our business over the last 15 years. In turn, this has reduced the cost and time lines of the title search and exam process while preserving the coverage and value of our insurance product.

Importantly, FNF carries a strong balance sheet with a BBB credit rating and stable outlook from S&P. This is supported by a reasonably low debt-to-capital ratio of 28.9%, sitting within management’s targeted range of 20% to 30%.

FNF currently yields a respectable 3.4% and the dividend is well-covered by a 47% payout ratio. It also comes with a high 5-year dividend CAGR of 9.9% and 13 consecutive years of growth. Management has noted that it views the $550 million annual dividend as being sustainable.

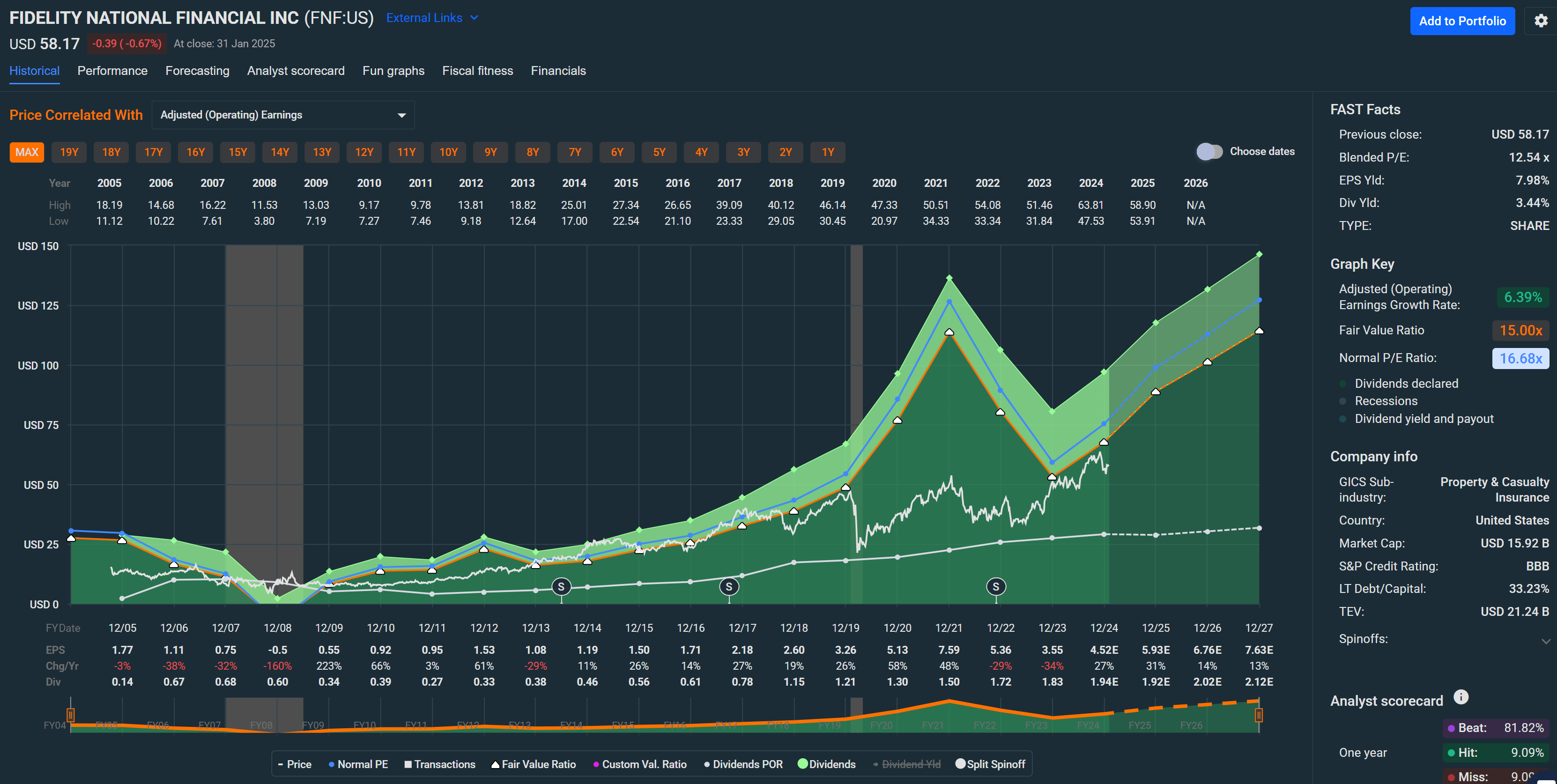

Lastly, I continue to see value in FNF at the current price of $58.17 with a forward PE of 12.8, sitting below its historical PE of 16.7, as shown below.

Seeking Alpha

Analysts estimate EPS to grow at a robust 17% to 29% over the next two years, driven by F&G AUM expansion, enhanced profitability from technology investments, and increased transaction activity across commercial title sectors, as noted earlier. As such, FNF appears to be undervalued with growth catalysts on the horizon.

Risks to the thesis include potential for a real estate downturn, which could negatively affect the title insurance business. Moreover, volatility in interest rates could negatively impact investment returns on the F&G side of the business. Lastly, the potential for regulatory changes, such as the proposal to remove title insurance from requirements of lenders for specific loans during the Biden administration, introduces uncertainty to the sector. However, that risk is mitigated at present due to Trump opposing this plan.

Investor Takeaway

Fidelity National Financial remains an attractive investment, supported by its dominant position in the title insurance market and the strategic diversification provided by its F&G annuity and life insurance segment. It’s demonstrated resilience and growth across its Title and F&G business lines.

FNF’s ability to thrive across interest rate environments, combined with its focus on technology investments and AI-driven efficiencies, positions it well for sustained profitability. Plus, it carries a solid balance sheet and a well-covered 3.4% dividend yield.

With a forward PE sitting below its historical average, FNF appears undervalued, offering significant upside potential driven by AUM growth, industry-leading margin, and commercial sector recovery. As such, income and growth investors may do well by layering into FNF at its current discounted valuation.

Read The Full Report on iREIT+Hoya

iREIT+HOYA Capital is the premier income-focused investing service on Seeking Alpha. Our focus is on income-producing asset classes that offer the opportunity for sustainable portfolio income, diversification, and inflation hedging. Get started with a Free Two-Week Trial and take a look at our top ideas across our exclusive income-focused portfolios.

With a focus on REITs, ETFs, Preferreds, and 'Dividend Champions' across asset classes, members gain complete access to our research and our suite of trackers and portfolios targeting premium dividend yields up to 10%.