bjdlzx

The last article on Tullow (OTCPK:TUWLF) (OTCPK:TUWOY) covered the debt burden because the stock price was not going anywhere until that debt burden got handled. The current management has really just been coming up with solutions to deal with that debt burden. To their credit, they have dealt with this issue through a combination of solutions that include growth in production. However, the issue remains. Until that debt burden is properly dealt with, I believe investors are better off with a company like Murphy Oil (MUR) that has no debt burden and has credible partners.

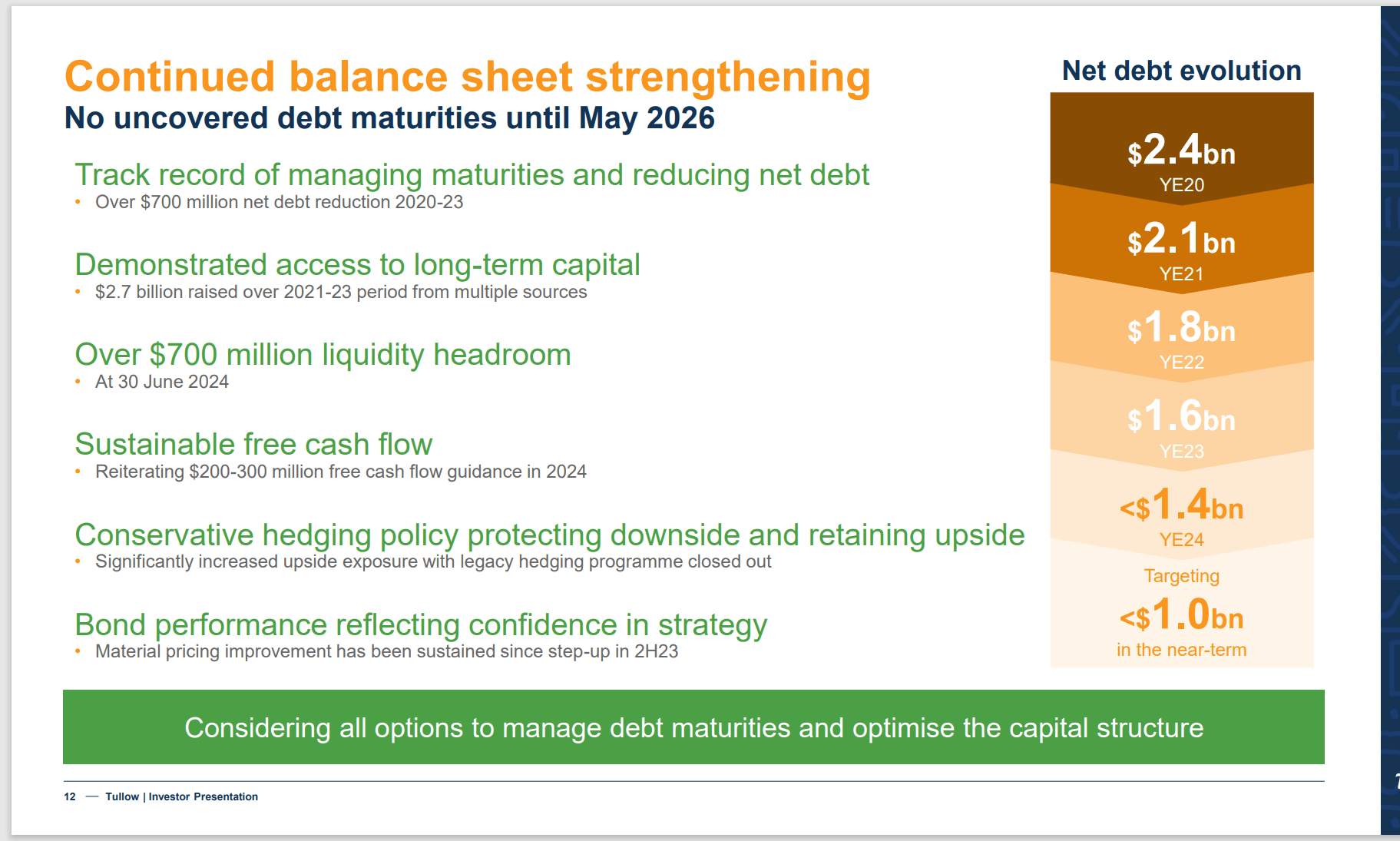

The latest earnings report has stated that the company has free cash flow to pay down debt assuming an oil price. Even if that goal is met, the debt will remain at $1.4 billion at the end of the year while free cash flow is a mere $200 million (very roughly).

Tullow Progress And Guidance To The End Of The Fiscal Year (Tullow Investor Presentation September 2024)

This management has clearly performed a minor miracle to remove as much debt as it has in the time it has been in control of the company. This definitely marks this management as above average. However, there is still more work to be done with that debt.

That makes this a company to watch from the sidelines. I would reiterate that the stock is probably not going anywhere significant until the debt ratio gets to where it needs to be.

Complications

Additionally, during the conference call, management reiterated their commitment to safety. Nonetheless, there were some safety incidents that each investor needs to review for themselves that were covered during the conference call. This company operates in a part of the world where worker protections are not exactly the same as they are in the rest of the world (whether or not a union is involved).

Management claims to have resolved the issues enough to keep most of them in the "minor" classification although one issue is being investigated. That fact alone may well mean much of this came about from issues not caught by the current management that were existing before this management took over. It can happen.

On the other hand, when company finances are on the "stretched" side, this is something that points to watching this company from the sidelines.

Stock Price Action

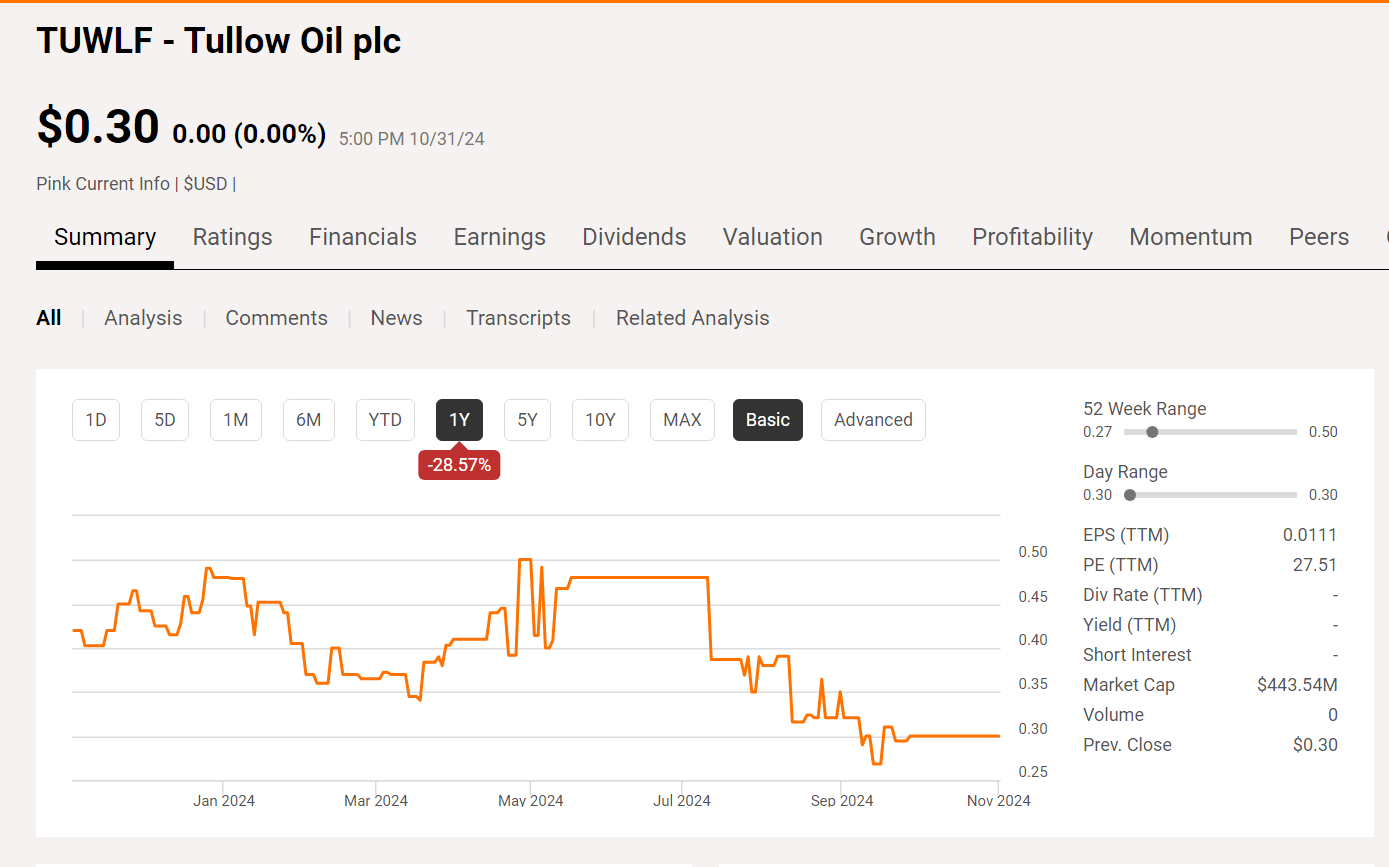

This is a company with a fair amount of stock outstanding. The low price of the stock means that a lot of volume is needed to move the stock. Since the market value is relatively low, that is certainly possible. Still, the movement lately is worth reviewing.

Tullow Common Stock Price History And Key Valuation Measures (Seeking Alpha Website November 3, 2024)

This stock price is likely more sensitive to current industry worries about weak commodity prices in the future due to the debt load. Servicing the debt is a cost that is often the difference between a low-cost competitor and one with a competitive disadvantage.

According to the website, my last article was published at $.42 per share, so the stock has now lost nearly 30% of its value as I am writing this. Low priced stocks are very volatile. Therefore, any investor needs to use patience and limit orders to either invest or divest this stock.

But between the stock price action and the concerns listed before, I probably would not consider investing in this stock at this time. As I noted before, I have tremendous respect for this management as I believe they are cleaning up one of the bigger messes that I have come across in some time. However, that very good job has not yet established a "buy" case because this has been a very big mess.

I personally believe that they have more than an average chance to get to the point where this will be a buy. But there is no need to get in early. This company could be badly hurt by a sustained period of low oil prices due to the debt load.

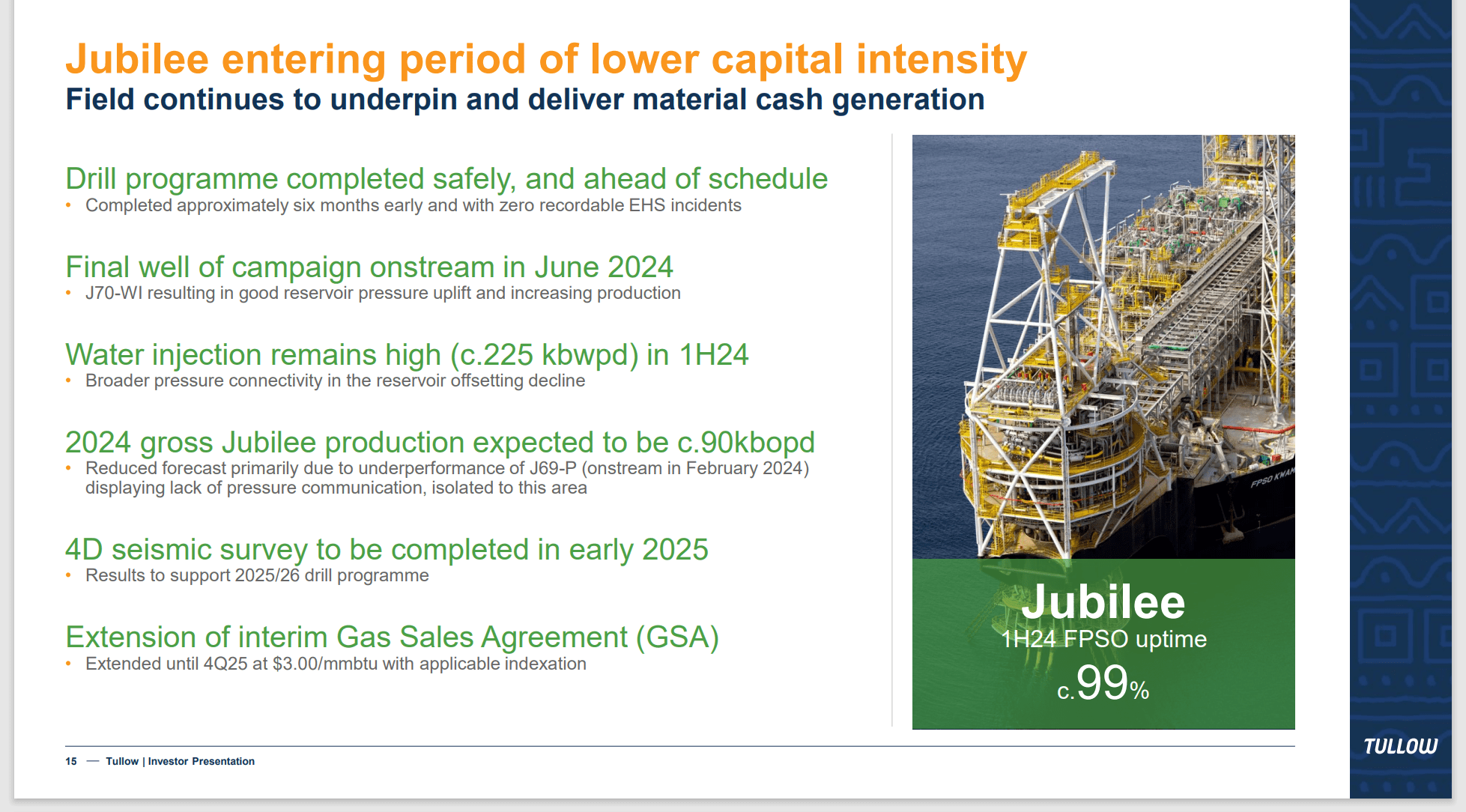

Jubilee

The major income producing asset for this company is the Jubilee field.

Tullow Update Of The Jubilee Field (Tullow Corporate Presentation September 2024)

Next year could well feature the ability to produce more free cash flow because the capital needs could well be lower. Drilling may begin again towards the end of fiscal year 2025. But that is far from certain.

A huge multiyear capital project was completed that resulted in a major cash inflow for the next several years. Now what the company needs is something like that from any of their other fields.

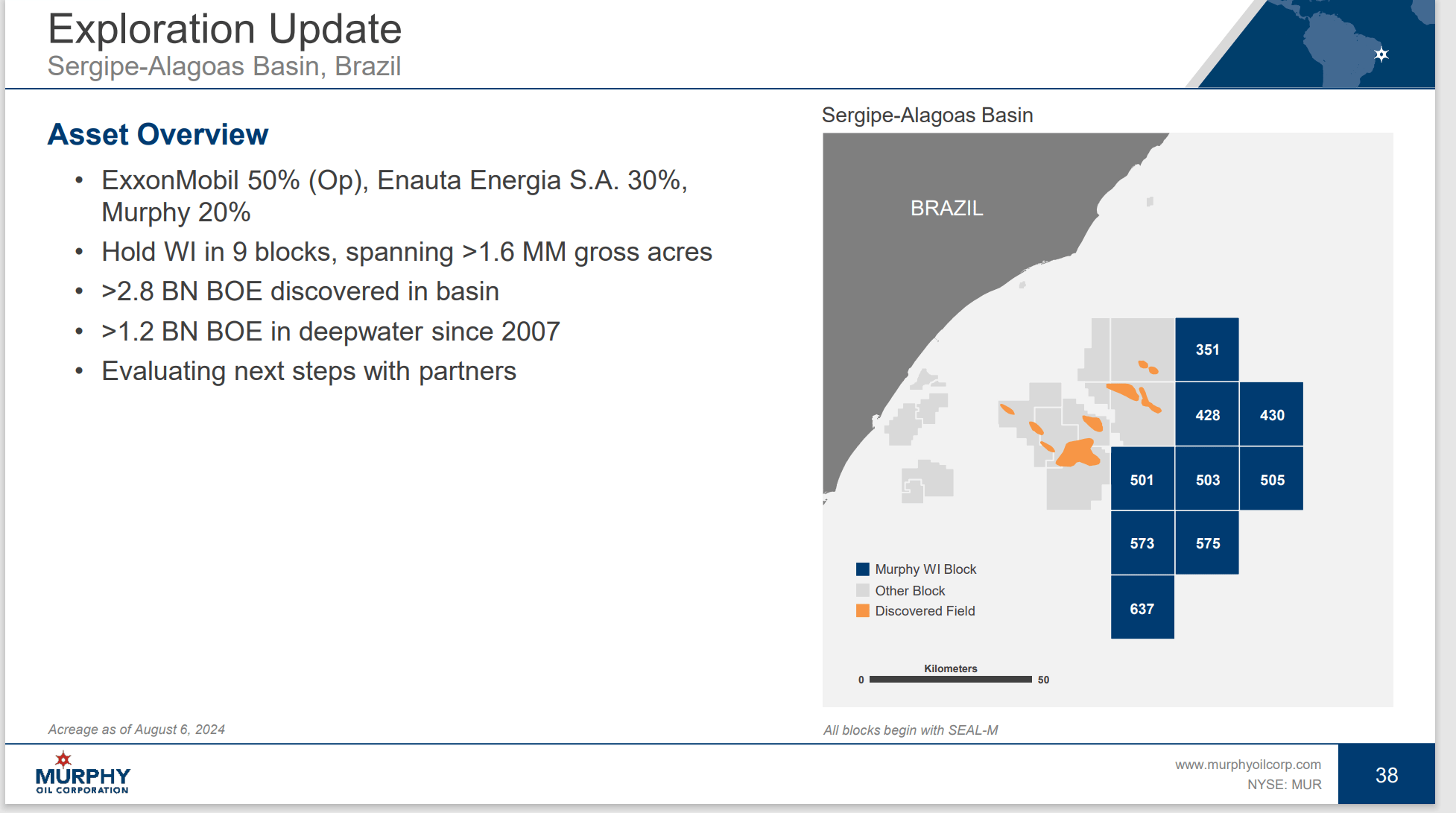

Why Murphy Oil

Murphy oil has a far lower debt ratio than is the case with Tullow. This gives the company a lot more flexibility to take advantage of opportunities and find partners.

Murphy Oil often has some well-known partners as operators. These partners often give the company an advantage when bidding on acreage.

Murphy Oil Update Of Brazil Partnership With Exxon Mobil (Murphy Oil Corporate Presentation September 2024)

Having Exxon Mobil (XOM) is often a huge advantage over the partners that Tullow has had. While a partnership with Exxon Mobil is no guarantee of success, many times, Exxon Mobil has found oil that is not all that significant to a large company but is very significant to a company the size of Murphy.

The latest example here is the Exxon Mobil partnership with Hess (HES) that found oil in Guyana. My latest article on that can be found here.

Murphy has a lot of other "name" partners. More importantly Murphy has balanced the risks of offshore exploration and development far better than Tullow has.

That last statement mostly applies to the management that came before current Tullow management. But it is also a small company risk in that they often do not have the resources to pay for the talent that can handle relatively large offshore projects properly. The smaller the company is, the more this risk presents itself.

This is probably where Tullow management is heading the company towards as the debt reduction proceeds. However, there is a lot of "cleaning up" that needs to happen first.

Summary

Clearly, Tullow management has come concerns that will keep management very busy for the next couple of years. Tullow has made tremendous progress since I first began following the company. However, that progress does not yet add up to a buy.

Instead, I would consider selling any Tullow stock I have and using that money to buy Murphy Oil. Murphy Oil is far more financially healthier, and it partners with some well-established companies.

As the last article noted, in Guyana, Tullow drilled a well in Guyana (actually 2) and both came up with sour crude that is exceptionally expensive to process. As a result, the company gave the acreage back to a partner and has now moved on.

Meanwhile, Exxon Mobil has been drilling one light oil well after another. This points up the advantages of partnerships with a lot of resources. As a result, I have covered Hess outperforming much of the industry for some years now because of the growth of Guyana production.

For this reason, I suspect that Murphy Oil would probably do better for investors because this management has a far better track record in the offshore business.

Risks

Tullow still has a relatively large amount of debt when compared to the cash flow. It is far better than it was when I first began covering the company. Current management gets credit for that improvement. But the issue is that the debt situation still needs to improve more.

Because of that debt load, a severe and sustained commodity price downturn would hurt Tullow far more than it would Murphy Oil.

When one considers that commodity pricing in the future is very low visibility and very volatile, that makes Tullow a high-risk idea.

The management that is cleaning up the mess they found at Tullow is unusually talented and very resourceful. A loss of any of the key executives could prove to be very damaging to the future of the company until those issues are resolved.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

I analyze oil and gas companies like Tullow and related companies in my service, Oil & Gas Value Research, where I look for undervalued names in the oil and gas space. I break down everything you need to know about these companies -- the balance sheet, competitive position and development prospects. This article is an example of what I do. But for Oil & Gas Value Research members, they get it first and they get analysis on some companies that is not published on the free site. Interested? Sign up here for a free two-week trial.