jax10289

Dear readers/followers,

I've been a fairly heavy investor in Mercedes-Benz Group AG (OTCPK:MBGAF) for a number of years now. The company, like many automotive manufacturers in Germany that I also invest in such as Volkswagen AG (OTCPK:VWAGY) and Bayerische Motoren Werke Aktiengesellschaft (OTCPK:BMWKY), has been on a rollercoaster of ups and downs, since the company first moved head-first into going all-out EV, only to less than 2 years ago roll back these plans to bring about a more appealing overall mix of ICE and EV.

Mercedes-Benz is one of the most valuable car brands in the entire world. This is well-earned because Mercedes, at least historically, has built very premium and qualitative, well-loved cars. This is why I, personally, drive a Benz - my main driver is a 2019 S-Class, and this is my "dream car", and a car I intend to have for as long as I can keep it running, repaired, and insured. For someone like me who doesn't care about the racing spirit or driving fast, but more about comfort, a Benz is the perfect "driving machine".

What Mercedes and other companies are seeing in consumers, which is starting to shift things about, is a declining willingness to pay for premium cars and brands. While this is a general development for most automotive companies, it's very detrimental to Mercedes, which makes much of its margins from a small portion of its consumers - 15% of total sales for the car manufacturer. If this number were to decline further or the margins here were to change, the results for Mercedes could be an issue, and thus the share price. This is one of the things I am going to talk about.

Looking at the latest results, the upside, and the potential of Mercedes-Benz

There is a reason I own far more in stock in Daimler Truck Holding AG (OTCPK:DTRUY) than I do Mercedes-Benz. The car manufacturer, unlike the HVP, has not managed to "wow" me so far with its near-term plans.

I am not as positive about Chinese entrant brands as other analysts seem to be. In fact, I consider the likelihood of Chinese EV brands establishing a significant presence in Europe to be rather low - and I am backed up by sales numbers here (Source). Despite the excitement of these newer and cheaper products, I believe they will ultimately be weighted down by insurance costs, lack of dealer and support/service networks and other factors.

However, the downside in sales for Mercedes in China is very real. China is currently where Benz generates most of its revenue, with average revenue on a per-user basis significantly declining. While I don't think it's in any way the end of Benz, I do believe that the company will have to pay and invest much more to retain its brand identity and integrity in the face of rising competition - which translates, in my modeling, to larger costs here.

The latest results are a number of weeks old at this point. What I am looking at for Benz are the gross margin levels, the sales growth rates, and overall R&D cost. The company's investments in MB.OS is especially risky - and interesting - when the brand is trying to create its own OS.

There's also something to be said that, like with many European and Japanese manufacturers, 2024 is really just a transition year for the automotive market. The upgrades coming in the coming years, not only an upgraded electric CLA but a full-suite S-class upgrade in 2 years, are the things that should be considered as significant positives here.

Risks to the company are pricing power and the cost environment, with the latter coming under pressure due to new competition that on the surface offers a better value proposition. Personally, I would be dubious of a new entrant that offers brand X which supposedly has the "same premium value" as brand Y at a significantly lower price. My question would then concern where the new entrant has saved, and if it's really just all "lower margins". But it holds appeal for plenty of people.

I do not believe that Mercedes is regaining its lost market share in China - I believe the cost environment and the changing consumer tastes will see China become a smaller market, with the company once again forced to focus on a different mix. This is one of the reasons why my own PTs for Mercedes are lower than the market average.

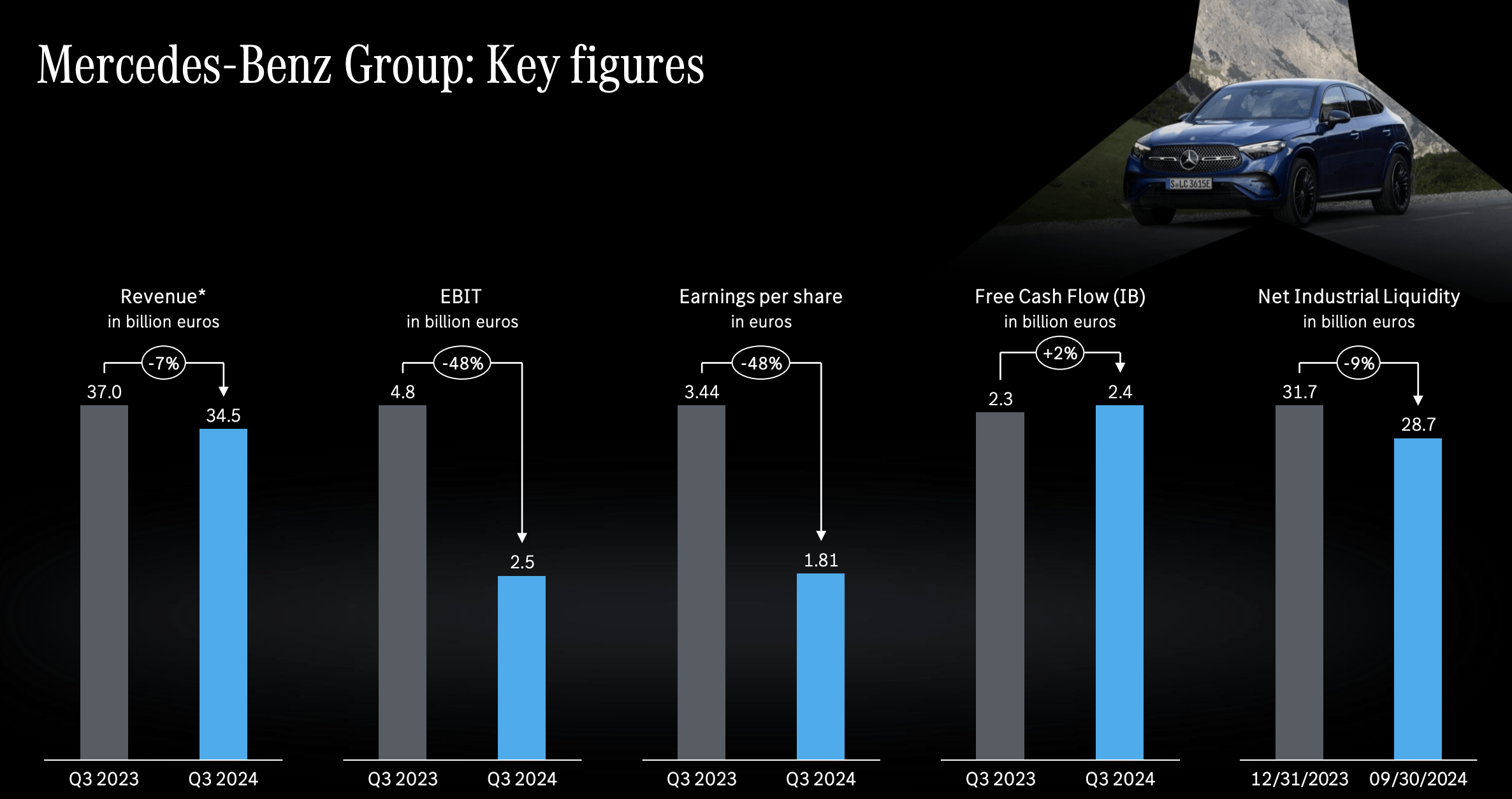

Mercedes Benz Company IR Presentation 3Q24 (Mercedes Benz Company IR Presentation 3Q24)

The latest results are 3Q24. This was not a good report or a set of quarterly results. Company sales were decent - solid for cars and vans - but China was the real sales culprit here. This resulted in slow margins, actually margin pressure, with the typical statement of "challenging market conditions".

On the positive side, the company continues to generate very strong cash flow, we're seeing improvements in automated driving tech, and the company is moving into vertical scalability with its new battery-recycling facility. Benz is also taking advantage of the company's poor valuation to execute billions of euros in buybacks - which is advantageous to shareholders, provided the company can rise from this.

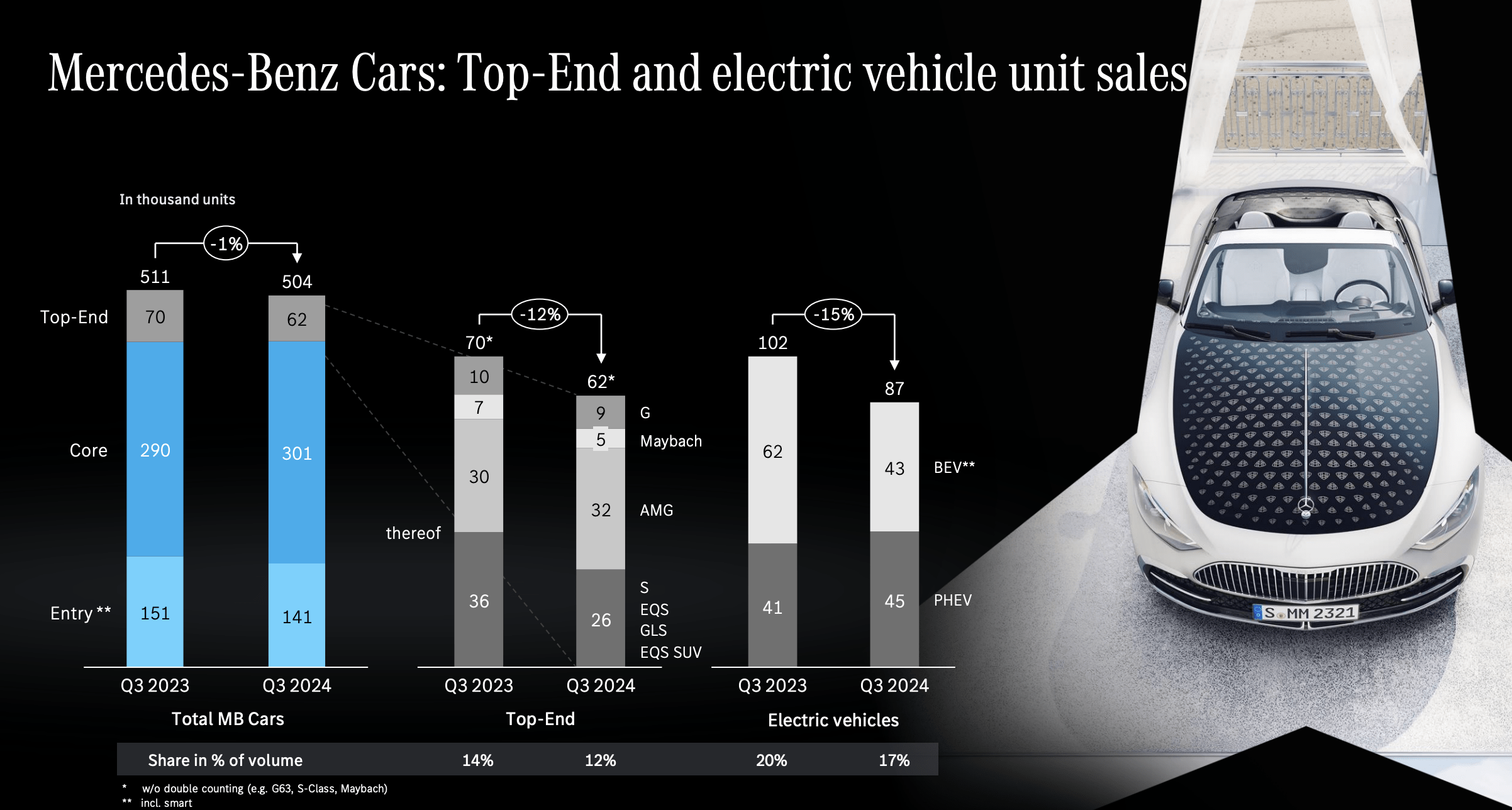

Mercedes Benz Company IR Presentation 3Q24 (Mercedes Benz Company IR Presentation 3Q24)

EBIT was mostly stable during the quarter, even if the only positive that could really be argued are the operational efficiencies in procurement and on the production side. Negatives included the unfavorable mix, negative pricing, product expenses, lower results, and issues in dealer support in China, as well as previous-year effects and changes in interest rates.

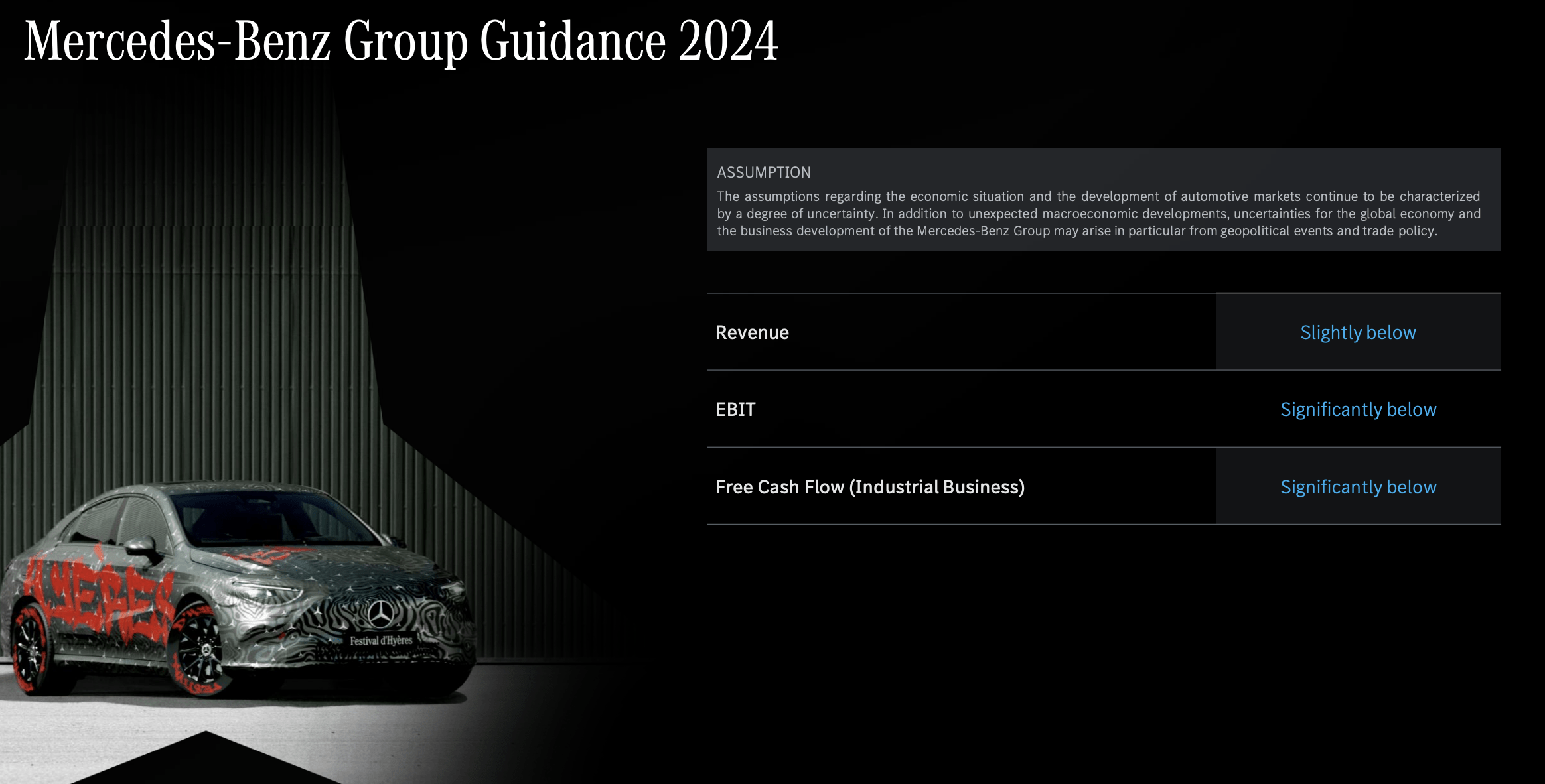

Vans saw less decline than cars, but it was still a decline both on the top and on the bottom line. The mobility segment continued along at a relatively stable rate, but the company's EBIT here wasn't great either, dropping 21% YoY. Guidance as it stands is a drop in 2024, with lower returns on sales, while at the same time seeing significant increases in the company's investments. The combination of these massive increases in spending while seeing a relatively pressured income and margin environment, have meant clear trends for Mercedes - namely negative ones.

That 2024 remains a problematic year is undoubted, including from guidance. But the question, like with its peers, becomes what comes out of this until 2028E.

Mercedes Benz Company IR Presentation 3Q24 (Mercedes Benz Company IR Presentation 3Q24)

The company is focusing marketing on new experiences and moments. I, personally, think they should more focus on ensuring that coming generations of cars give customers the sensations that we're used to from the S-class or other models, where I, personally, believe that sitting in and driving a Benz is actually substantially different from another competitor - even different from BMW. I do not think, for instance, that the Maybach SL Monogram will be a sales or profit driver for the business.

Mercedes Benz Company IR Presentation 3Q24 (Mercedes Benz Company IR Presentation 3Q24)

When I update on Mercedes, I look at the commoditization of the brand, which I view as a negative. And it's clear that the company wants to avoid this further as well, given its focus on increasing ASP, or average sales price. Whenever the company talks, however, about reducing input or material costs, I can only hope that this does not come at the expense of quality - because if history has shown us anything, you cannot over time shine dirt/garbage and call it gold.

The company's message out of 3Q24, for 2024, and going forward is that they are repositioning the company for more profitable growth. This is good. This is welcome. But I hope it comes with a focus backward rather than looking to the sides of where some companies currently are. The company is doing "subtle" things, but that really shows you how important these things are to consumers.

This includes the Mercedes star. How many consumers want a luxury Mercedes without an upright Mercedes star? Very few, apparently (including me) - so the company makes a big deal about now including an upright star.

Mercedes Benz Company IR Presentation 3Q24 (Mercedes Benz Company IR Presentation 3Q24)

Such a small thing, but important. It's all about KYC - Know your Customer - and not the banking way.

Let's look at the valuation and upside for the company.

Mercedes Valuation - a long road, but an attractive price at below €57/share

That Mercedes-Benz is in a slump, of that there is no doubt. The company has at least 2 years of issues to work through before I believe we can see a clear picture of where the company wants to be - even if its current strategic focus gives us some ideas. The move away from going "Full EV" very soon is also a confirmation of the company listening to the market more than before, and gives me faith in the future here.

To be clear with you, I'm not a fan of EVs - and this shapes my opinions on the automotive industry. I can see their use in some environments, but where I live and for my purpose, I could not drive or use the current iterations of the platform. I follow the development with interest and see where this takes the industry.

Mercedes's fundamentals are beyond solid. A rating. Less than 37% long-term debt to capital. A yield that even at the 2024E estimated level is at over 7%. A sales decline that's very clear, yes, but a stabilization that to me is equally clear in 1-3 years.

The company's market cap should be more than €60B. I do not believe the current valuation to be in any way reflective of the value here. At below 6x P/E, the company trades significantly below its long-term average, and this is where I like to invest.

At the current company strategy and valuation & position, it does not really matter to me the time it will take to recover. This is because the company is, to me, considered extremely cheap here. Any delay in recovery means that I will only be able to buy more cheaply. Even the lowest targets by the 22 analysts following Mercedes-Benz here puts the company at around €50/share, with up to €105/share possible. The average target is just south of €70/share, and this denotes at least a 22% upside. I believe the company's upside is almost double that over time. Still, out of 22, 14 analysts are either at a "Buy" rating or an "Outperform" rating - so this is a strong positive in terms of analyst targets.

I give the company a share price target of €85/share. This includes a significant 15% discount due to what I view as deteriorating market conditions and future trends in China, which I don't think all other analysts are including. I believe the shift back to value-over-volume will gain traction with consumers, provided the company also brings back some quality seen in previous generations of products - I've driven the latest iteration of the EQS for a week, and I was not impressed. I forecast better gross margins, but the uncertainty in the model here is the share of EVs, which are dilutive to margins overall. But generally speaking, I see gross margins bouncing back up in 2025E alongside other metrics, which should support a bit of recovery here.

For that reason, I consider the sub-€60/share prices to be the "trough" here, and that means that to me, it's time to invest.

My thesis is as follows.

Thesis

- Mercedes is one of the most qualitative and premium car companies out there. It owns some of the most desirable cars and brands on the planet, and despite some of its recent pushes in my view going in the wrong direction, I believe at heart the company remains a qualitative automotive business with a lot of forward potential.

- The company is currently addressing its profitability by improving step by step, and hopefully executing on its more improved mix and strategy going forward.

- In any future scenario, I view Mercedes-Benz as undervalued here, and that is why I give the company a "BUY" rating and consider it cheap. Out of all automotive in Germany, this one is one of the more attractive ones - and I am planning to expand my position in it going forward.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fulfills 3 out of 3 quality indicators, and 2 out of 2 valuation indicators. That means 5/5 "stars" here, which is enough for an attractive thesis for the company. Based on this, and a valuation target of €85/share where I see a risk/reward-adjusted upside that's attractive enough for me. I give the company a "Buy" rating as of December 2024.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

The company discussed in this article is only one potential investment in the sector. Members of iREIT on Alpha get access to investment ideas with upsides that I view as significantly higher/better than this one. Consider subscribing and learning more here.