Fahroni/iStock via Getty Images

Daqo New Energy (NYSE:DQ) is a Chinese company among the leading global producers of polysilicon, a material used for solar panel manufacturing. The sharp polysilicon price decline between 2023 and 2024 negatively impacted both revenue and operating margins of the major players in the industry, resulting in a 57% YoY decline in DQ's revenue in the first 9m FY24 and a collapse in profitability, with net income margin falling to -19.79%, compared to 18.61% in FY23.

During 2024, polysilicon price stabilized between $4 and $5 per kg, but it does not yet show signs of recovery, likely driven by supply dynamics linked to increased global production capacity and declining demand for solar PV systems, factors that could persist into FY25.

Although the market is facing short-term challenges, I believe the projected long-term growth in demand for solar panels represents a structural driver for DQ, suggesting that revenue will accelerate again and margins will recover. Moreover, DQ has an extremely strong balance-sheet, with no debt and $2.3 billion in available cash as of September 2024.

Considering the expected recovery in polysilicon demand, the company's financial strength, and further consolidation in the industry, I assign DQ a "buy" rating, supported by a DCF analysis indicating an 80% undervaluation of its market price.

Polysilicon Supply and Demand Dynamics

Polysilicon is an essential material to produce crystalline silicon (c-si) solar cells, a technology used in 97% of the solar modules produced globally in 2023. The polysilicon supply chain is highly concentrated and dominated by Chinese companies, which contribute 93% of the 2.25 million ton (Mt) global production capacity and 80% of the 1.6 Mt production output in 2023. The same applies to demand, with China accounting for 63% of the new PV installations globally in 2023. These factors highlight the importance of Chinese companies in determining the price of polysilicon.

Production capacity increased by 71.6% in 2023, while demand growth slowed, leading to a supply-demand imbalance and a subsequent reduction in the price of polysilicon, ranging from $4 to $5 per kg in H2 FY24. The oversupply was primarily caused by the four major companies in the industry (Tongwei, GCL Technology, Daqo New Energy, and Xinte Energy) which have made, and continue to make, significant investments to increase their production capacity. One example is Tongwei, which has announced a $3.9 billion investment plan scheduled between 2024 and 2025, with the goal of building a 0.4 Mt annual polysilicon plant. Considering the investments made by the other three companies as well, this is expected to result in a total production capacity of 3.5 Mt by FY25 in China alone.

This development is likely to have a negative effect on polysilicon price between Q4 FY24 and FY25, partly due to high inventories that could further depress the selling price of the material. However, in the medium term, a price below the cost of production, even for tier 1 producers, is expected to result in many Chinese and Western companies exiting the market, leading to increased market consolidation and reduced imbalance between supply and demand.

Therefore, I consider it likely that the price of polysilicon will begin to recover between H2 FY25 and FY26. However, it should be noted that the oversupply condition is also partly due to demand-related dynamics. FY24 was characterized by a slowdown in the number of new installations globally, driven by rising interest rates and regulatory and policy uncertainty regarding incentives such as the PTC and ITC in the US. For this reason, the evolution of demand will also play a key role in the recovery of polysilicon price.

Business Overview

DQ is among the top 5 polysilicon producers in the world, with an expected output of about 200,000 metric tons (equivalent to 0.2 Mt) in FY24 and a production capacity of 0.35 Mt as of September 2024, holding a global market share of around 10%. As of December 2023, 60% of the company's production is dedicated to N-Type polysilicon, a percentage that continues to grow as N-Type requires a higher degree of purity than P-Type and is therefore increasingly used due to its ability to provide higher solar cell efficiency.

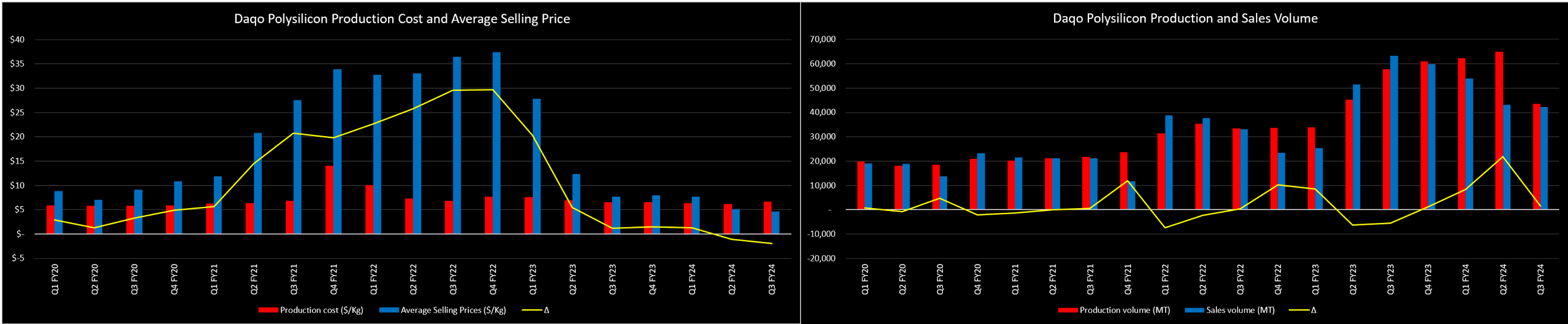

DQ SEC Filings, DQ Earnings Presentations and Author's Analysis

DQ's polysilicon production cost averages between $6 and $8 per kg and was $6.61 in Q3 FY24, compared to a price range of $4 to $5 per kg in the same quarter. This resulted in a lower production and utilization rate of about 50% in Q3 FY24, with the aim of minimizing losses caused by polysilicon price dynamics. Despite this, the imbalance between production and sales led to an increase in inventory, amounting to 20% of revenue as of September 2024, and a significant reduction in operating margins, which remained consistently in negative territory in the first 9m FY24.

In Q3 FY24, DQ reported better results than in Q2 FY24, because of countermeasures implemented by management to minimize costs. However, without effective improvement in polysilicon pricing, further gains in operating results are unlikely.

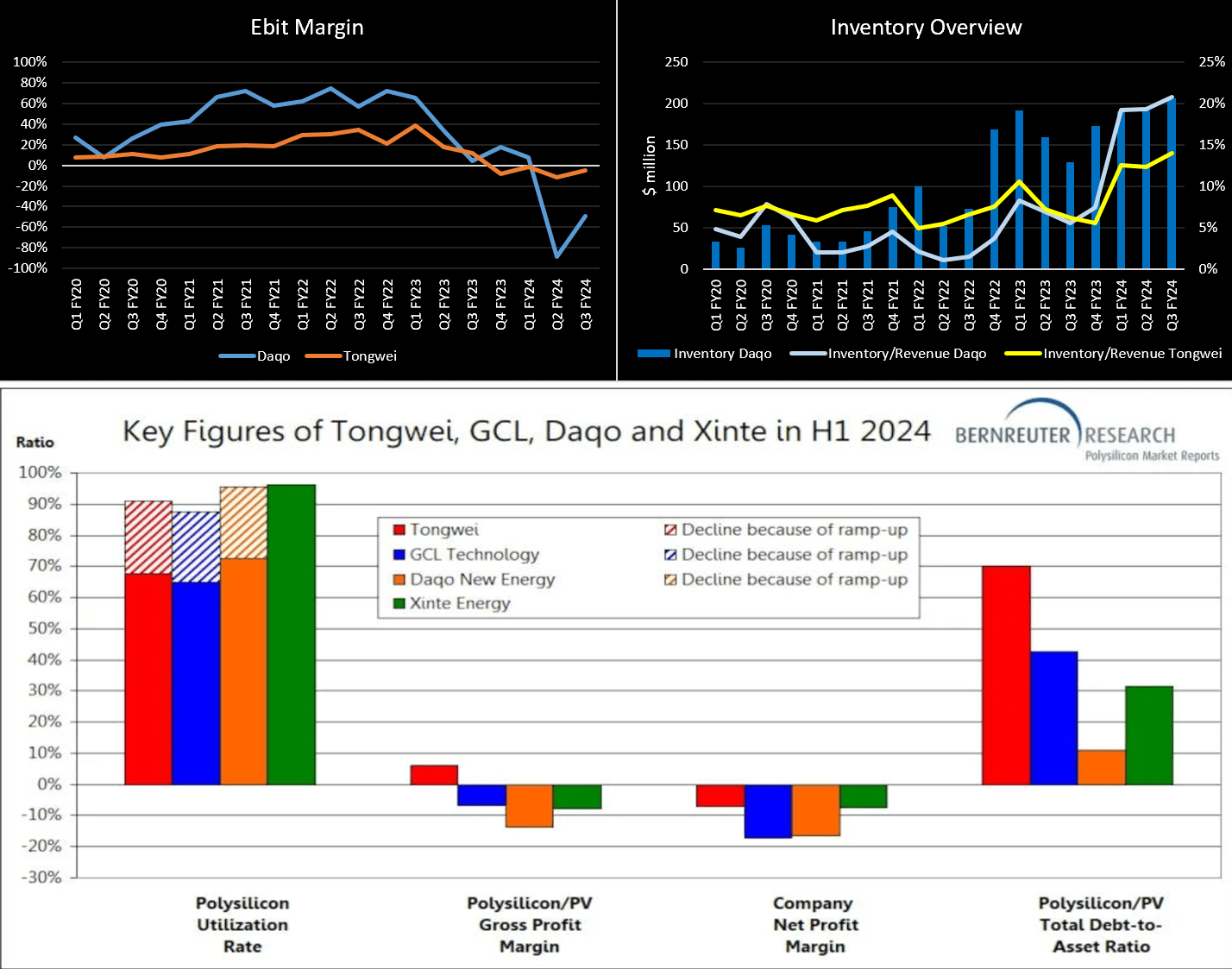

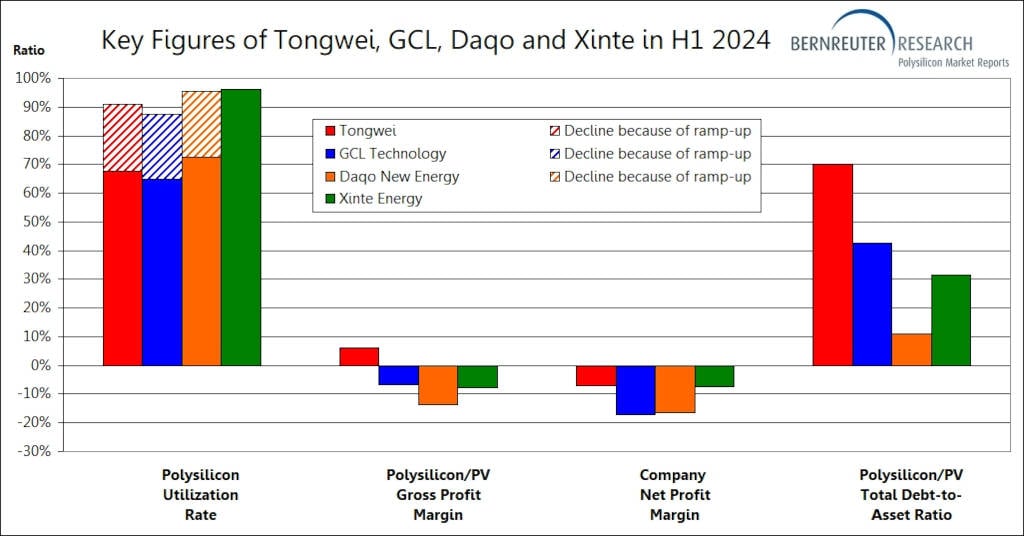

DQ SEC filings, Tongwei Financial Reports and Bernreuter Research

Bernreuter Research's analysis shows how the same dynamics outlined above affect other industry leaders, except for Tongwei, which, despite producing at a loss as evidenced by its negative net income margin in H1 FY24, continues to increase its market share. Nevertheless, the Chinese giant is also characterized by a more leveraged financial structure than DQ, which has a much stronger balance-sheet.

{kind=link}

Financials Snapshot

DQ SEC Filings and Author's Estimates

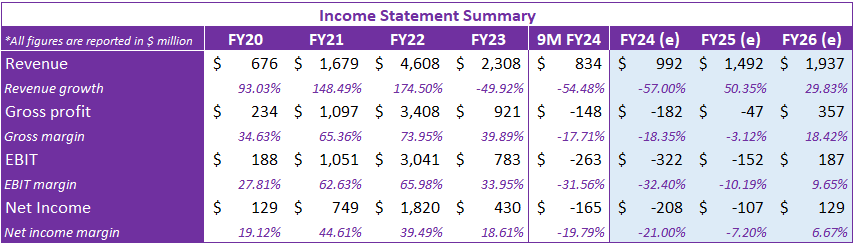

The polysilicon price collapse had a severe negative effect on DQ's financial results. In the first 9m FY24, revenue fell 54.5% YoY, accompanied by a drop in operating margins. The EBIT margin of -31.56% and net income margin of -19.79% reflected a sharp decline compared to 33.95% and 18.61%, respectively, achieved in FY23.

In Q4 FY24, I expect lower revenue and margins than in Q3 FY24 due to seasonal trends, as confirmed by the outlook provided by management, which estimates production output between 31,000 and 34,000 metric tons of polysilicon. For FY25, however, I anticipate a return to growth, especially from H2 FY25. In fact, in the first half of the year, the high level of company inventories, coupled with uncertainty regarding the incentives provided by the Inflation Reduction Act in the US, could act as countervailing factors to polysilicon price growth.

DQ SEC Filings and Author's Analysis

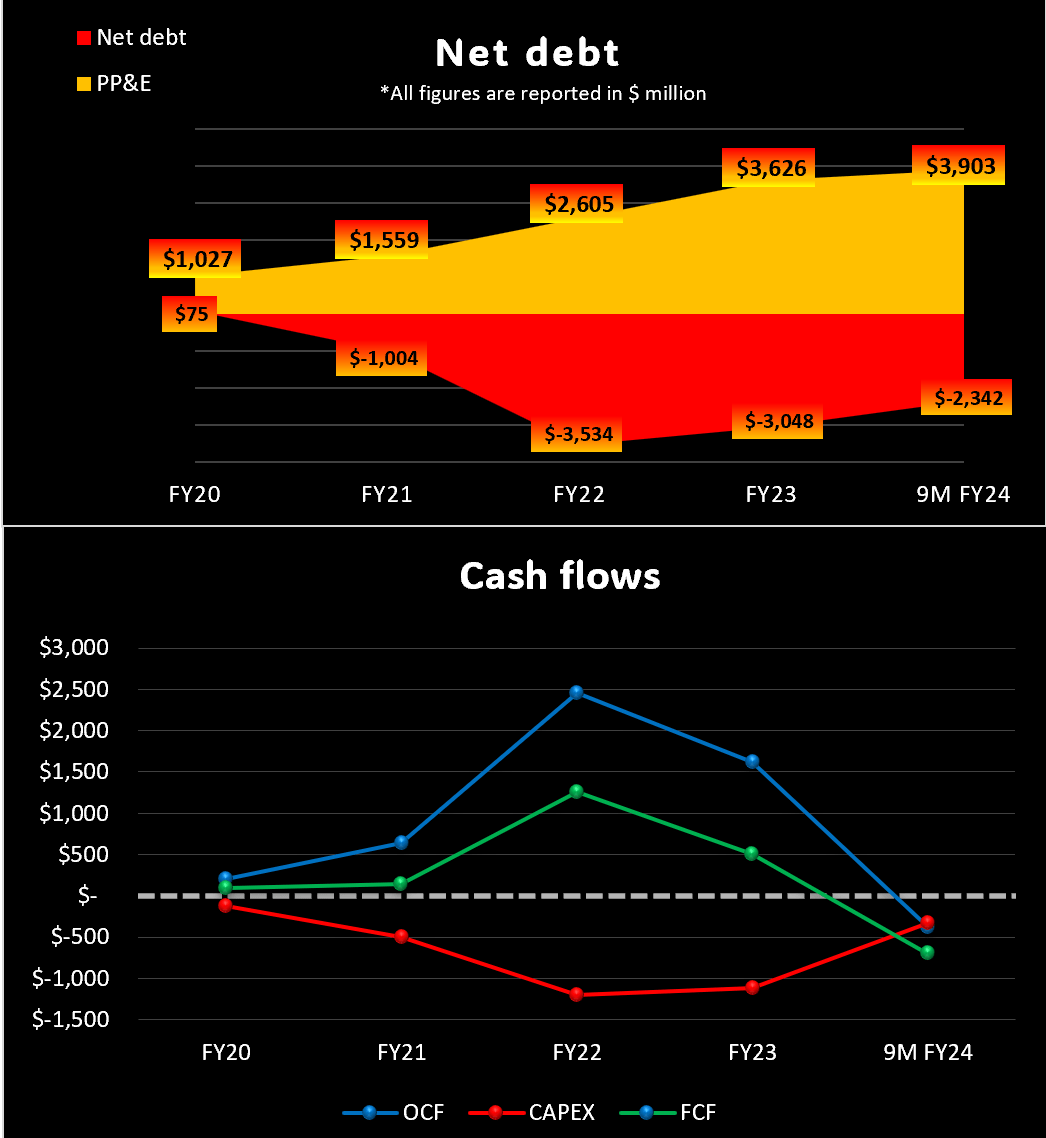

On the balance-sheet side, DQ appears to be a very solid company with a net cash position of $2.3 billion, higher than its current market cap, and PP&E of $3.9 billion. Although DQ recorded a negative OCF of $376 million in the first 9m FY24 due to the factors previously discussed, it is historically characterized by high internal cash generation and positive FCF despite significant investments aimed at increasing its production capacity. For these reasons, I expect a return to positive FCF by FY26, partly driven by a reduction in CAPEX resulting from the market oversupply, which discourages the construction of new production facilities in the short term.

Furthermore, the large amount of cash on hand can partly be allocated to shareholders, as evidenced by the $100 million share buyback program announced in July 2024, set to be executed by June 2025.

Main Risks

The high concentration of solar panel manufacturers implies that DQ has a high concentration of revenue. In FY23, the company's top 3 customers accounted for 64.4% of revenue.

As of December 2023, DQ directors owned 28.9% of the company. This concentration of ownership may give them significant influence over the company's activities.

DQ's operating results are highly dependent on the evolution of polysilicon price and global demand for solar panels.

The new Trump administration and uncertainty regarding tax incentives under the IRA could lead to a slowdown in the growth of new PV installations, resulting in a decline in demand for solar panels and, consequently, polysilicon. The imposition of tariffs on Chinese products could also have a negative impact on DQ's economic performance.

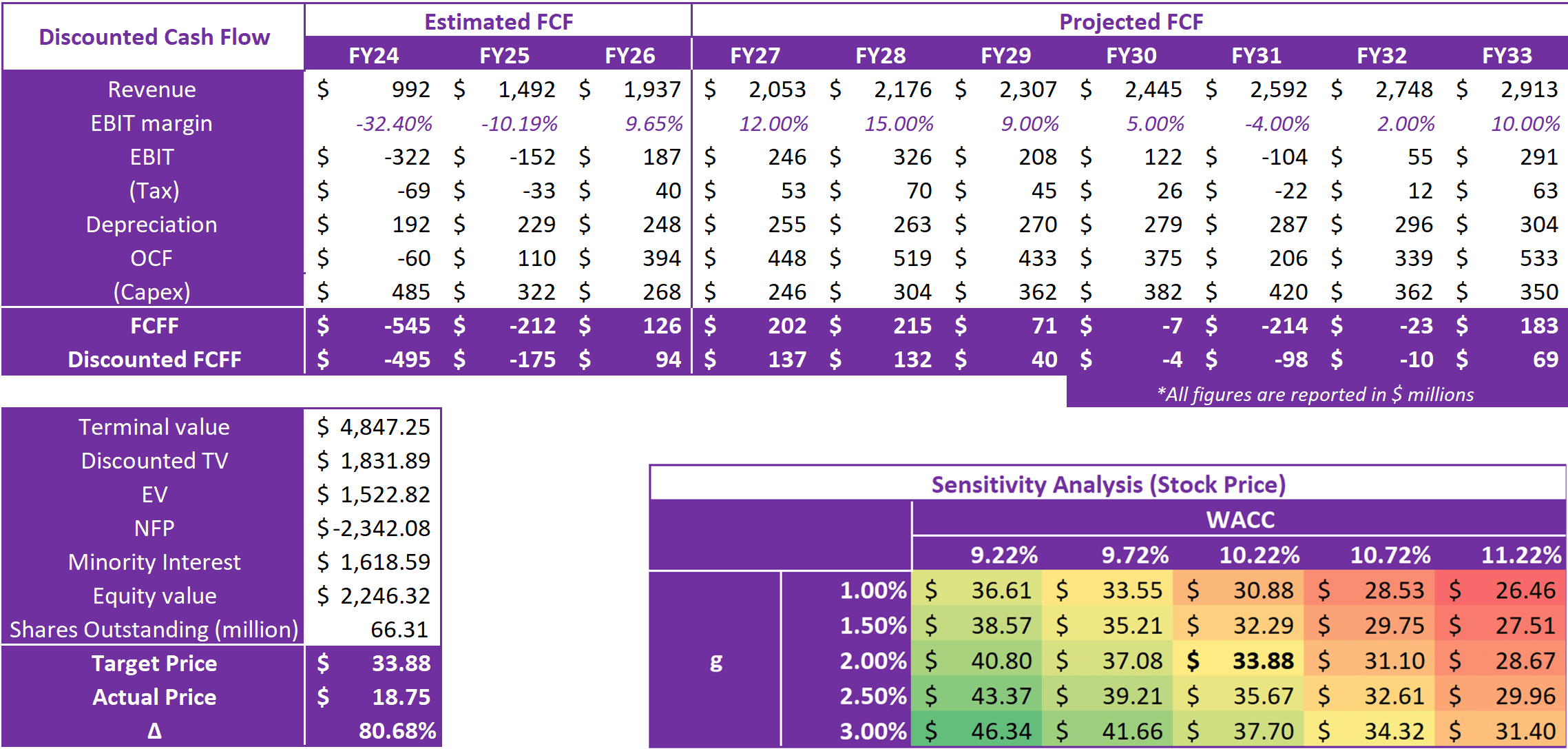

Discounted Cash Flow

To attribute a valuation to DQ, I performed a three-stage DCF. I made an estimate of the expected values of revenue, EBIT margin, CAPEX, and depreciation for FY24, FY25, FY26. I made a projection of these values for the period between FY27 and FY33, finally calculating the terminal value. This analysis returned a target price of $33.88 per share, which is about 80% higher than DQ current market price. To determine this value, I made the following assumptions:

Volatile EBIT margin to consider the cyclical pattern of the polysilicon price.

Beta was obtained using the Chinese unlevered beta of "Semiconductor" industry reported by Professor Aswath Damodaran, subsequently calculating levered beta based on DQ D/E ratio. A value of 1.46 was derived.

Growth rate (g) of 2%.

Risk-free rate of 2%, based on 10-year Chinese government bond yield.

Equity risk premium of 4.6% was obtained from Chinese ERP provided by Aswath Damodaran. Cost of equity of 10.22% derived from a CAPM model.

WACC of 10.22%.

Author's Analysis and Estimates

Take-Away

DQ is among the leading global producers of polysilicon, a material characterized by structural demand growth driven by the expansion of new photovoltaic installations. Although the current polysilicon price dynamics have led to a collapse in the company's revenue and operating margins, I believe that a more balanced supply and demand in FY25 could result in a price recovery, making the company extremely undervalued, as confirmed by the DCF analysis, which indicates an 80% undervaluation compared to the market price. The evolution of demand for solar panels and the imposition of additional tariffs under the Trump administration remain the two most important risk factors to consider, but they are not sufficient to change my view on the company. For these reasons, I assign Daqo New Energy a "buy" rating.