hapabapa

I like to review and potentially buy closed-end funds, especially near year-end. Discounts can blow out, although I'm not sure why. This year, discounts on U.S. closed-end funds have been wide. Last year they have been wider. Through the middle of the year, discounts disappointed, but currently average discounts on these products are moving in the right direction. The BlackRock Innovation and Growth fund (NYSE:BIGZ) is interesting. This is an equity growth fund with a call overwriting strategy. There is an activist present, and it trades at a discount of over 10% to net asset value. The expense ratio is 1.55% with 1.25% of that being in management fees.

Last year I wrote this fund up as well. At the time, it traded at a ~15% discount to net asset value. The NAV may be understated slightly as well, which I'll get into in a bit. Since that time, it did well, returning 25.61%, although it was crushed by the S&P 500 (SPY) returning 34.01% over that same period.

Boaz Weinstein continues to push for change here, and it is a major position in the funds and hedge fund he manages, according to his firm's 13-f. Boaz also pushed to change the directors at this fund and is likely to continue pushing for changes that favor investors (see this interview). Over the past year, BIGZ has been part of the Blackrock discount management program. That's not been that successful as it appears. The fund's discount narrowed, but that's true for the entire space. The fund is trading at a discount to net asset value that's close to the average for U.S. focused equity funds ~10%. However, covered-call funds currently trade at an average of -6.7% to net asset value.

The fund isn't overwriting options very aggressively. It is writing call options on only around 13% of its portfolio. Typically, about 6.2% out-of-the-money. One reason the fund is perhaps conservative in writing options is that 23.8% in private investments.

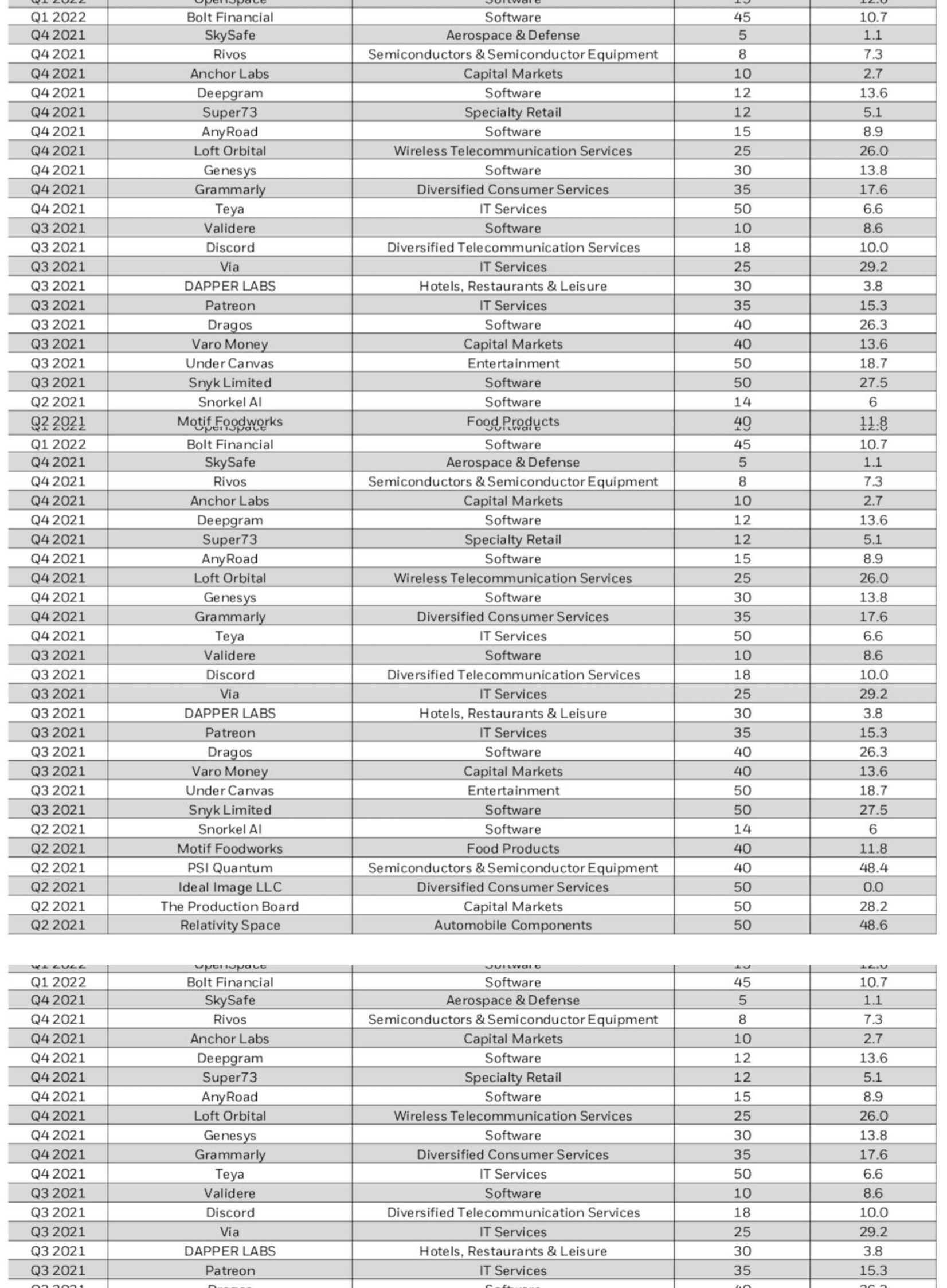

This table includes most of these private investments:

BIGZ private investments (Blackrock)

The values of these private companies aren't continuously updated like portfolios that are marked to market. This can be beneficial when valuations are falling but holds the net asset value back when private valuations are rising. During 2024 equity valuations have been rising. The private companies that could potentially go public can probably be considered mid-caps. Examples are Discord, PSI quantum and Patreon. Mid-cap growth stocks haven't kept up with the S&P 500, but what diversified index has?

Another way to look at a fund like this is that it's essentially a high fee mid-cap growth fund (like they're countless) but with stakes in Discord etc thrown in for free (because of the 10% discount).

I don't believe the lagging valuation updates likely make an incredible difference. As a whole, it seems likely to me that this portfolio is currently slightly undervalued. If the entire portfolio could be marked-to-market, NAV would potentially be a bit higher. In any case, the private holdings are down to ~23% from 26% last year. Decreasing the exposure to private will likely help the discount, even if the assets aren't undervalued. Investors have to factor in illiquidity premium on these. If the IPO market opens up again, which seems more likely after the latest U.S. presidential election, it could be a catalyst to reduce the private portfolio. In turn, that could free Blackrock up to make more meaningful changes to close the discount to net asset value. Massive tenders and other ways to return capital have the awkward side effect to increase the exposure to private.

The fund is also subject to an unusual contingent limited-term structure. Which sounds really complicated, but basically, there is a termination date for the fund set at March 25, 2033. That's still 8+ years away, but the discount should be gone by that time. It also puts pressure on the fund to forego/reduce private investments going forward, as it would be really awkward to be caught holding loads of private investments at a termination date.

To sum this up; 1) A covered-call fund at a ~10% discount is relatively attractive by itself. 2) There's a closed-end fund activist that built a huge position here and is actively pushing for change 3) Changes are already being implemented slowly but could accelerate if the IPO market opens up 4) Private valuations are potentially lagging the market. Like last year, I think it's still a buy.