bjdlzx

Expand Energy (NASDAQ:EXE) came into being on the first day of business in the fourth quarter of fiscal year 2024. Therefore, the results reported are those of Chesapeake Energy (CHK) alone. In some ways, this helps the accounting aspect tremendously, as one quarter does not have to be "split" for reporting purposes. However, it would have been considerate of investors to discuss the pro forma combined returns of the two companies for the third quarter in the quarterly press release. The biggest problem for the new company is the expansion of its presence into the high-cost Haynesville Basin, combined with a lack of cost control and selling price maximization.

Earnings

The last article commented on how the company sold the profitable Eagle Ford operations to essentially expand the high-cost Haynesville operations through this merger to become Expand Energy. That trend continued into this quarter. The article (and several before it) the lack of a vigorous operational cost control strategy. That may be changing though as management appears to have noticed the cost situation. But more time is needed to be sure.

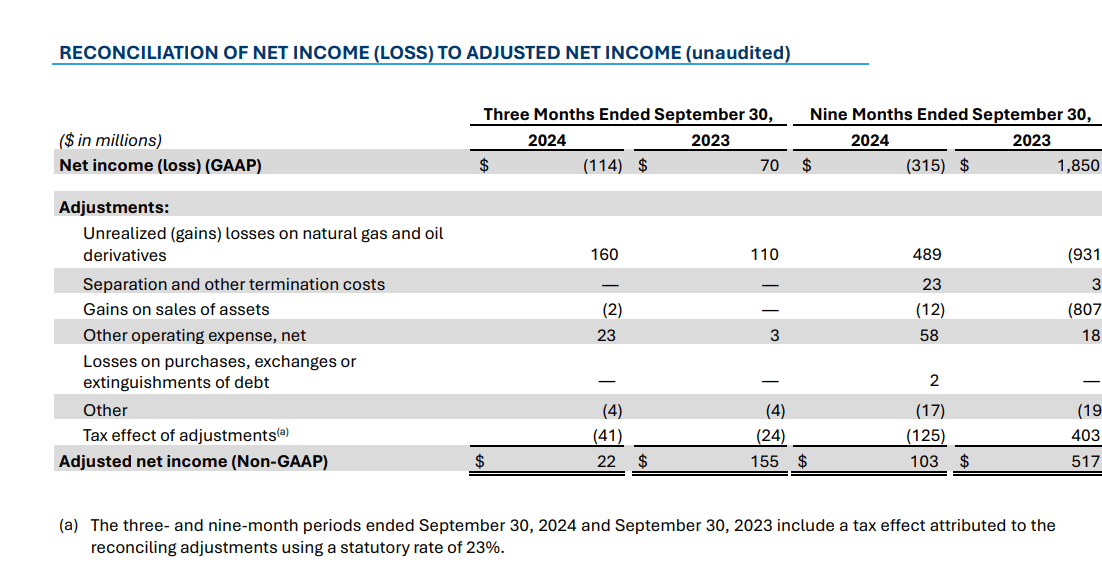

Expand Energy Adjusted Net Income Calculation And Comparison (Expand Energy Third Quarter 2024, Earnings Press Release)

The year-to-date net income (a non-GAAP measure) is positive. It should further be noted that unrealized gains or losses for derivative contracts really represent a forward sale of oil and gas prices. They do not represent actual cash gains or losses. Instead, it is an indication of an opportunity cost that is made to obtain a certain sales price at the expense of a possible better sales price to avoid the possibility of a worse sales price.

Even taking that into consideration, the performance is materially worse than the alternative of keeping the Eagle Ford properties and dumping the Haynesville operations. The Eagle Ford acreage is much more profitable than the Haynesville according to many operators, and that is likely to continue even when the ability to export expands to the levels anticipated by many. Of course, let's see how the future turns out.

If management is going to operate in a higher-cost basin (as the Antero Presentation referenced below frequently notes), then rigorous cost control is going to be needed. So far, there is little evidence of that.

Basin Reporting

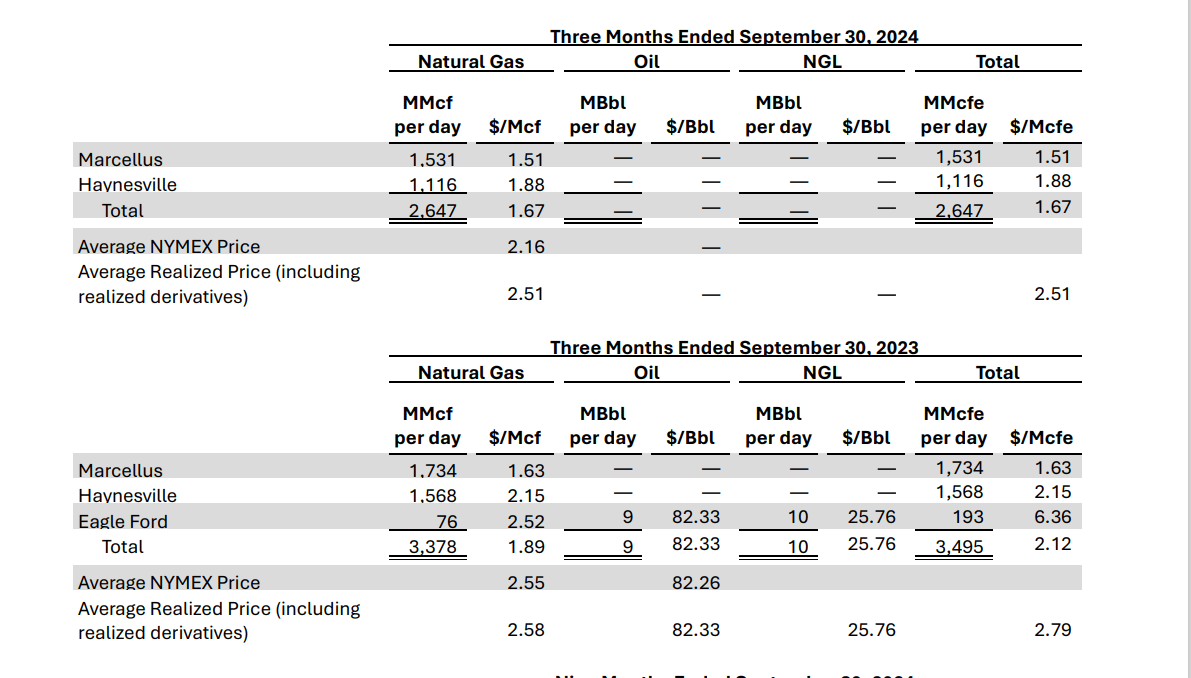

Comparative Basin Reporting shows the story.

Expand Energy Third Quarter 2024 Production Comparison (Expand Energy Third Quarter 2024, Earnings Press Release)

As shown above, even the Eagle Ford natural gas price received was far better than anywhere else. The combined price per MCF was far above what the company could obtain much of the time for its natural gas operations.

All that needed to be done was control the costs of the Eagle Ford operations. I follow many operators that report rock bottom costs from the Eagle Ford acreage, often comparable to Permian acreage production costs. That would provide badly needed cash flow and profits that likely would exceed what is currently being reported.

It should be noted that the company is shutting-in Haynesville production despite the better pricing shown above, due to the cost of that production. The Haynesville is the "swing basin" in that it is most sensitive to weak natural gas pricing. It therefore often decreases production to bring supply and demand into balance.

Now the company has the chance to show that when the natural gas cycle begins the inevitable recovery, this company will report above-average profitability to make up for the losses. However, given the past lack of emphasis on operations, I do not like the immediate chances. That could change in the future, however, as operations seem to be getting more attention.

Natural Gas Prices

One of the big hindrances to decent profitability is the prices received for production.

Expand Energy Prices Received Guidance (Expand Energy Corporate Presentation Third Quarter 2024)

As is clearly shown above, the company is setting expectations that it will receive less than NYMEX pricing. But competitors have long gotten around such parameters to post better than NYMEX pricing.

As a side issue, if the above slide is the guidance, then the investment grade debt rating and low debt levels are almost mandatory. Companies like this really cannot handle much of a debt load due to the cyclical nature of the cash flow.

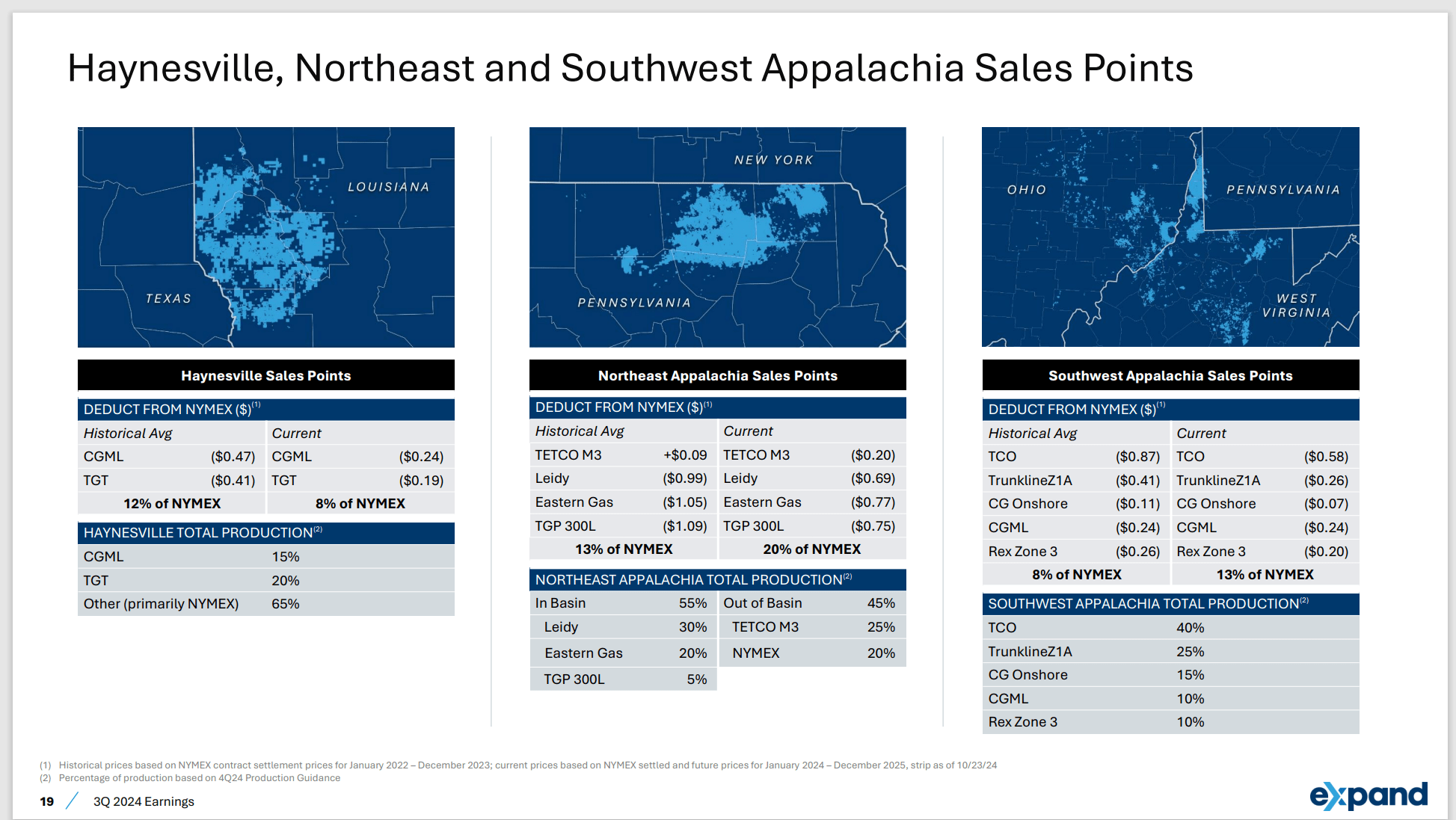

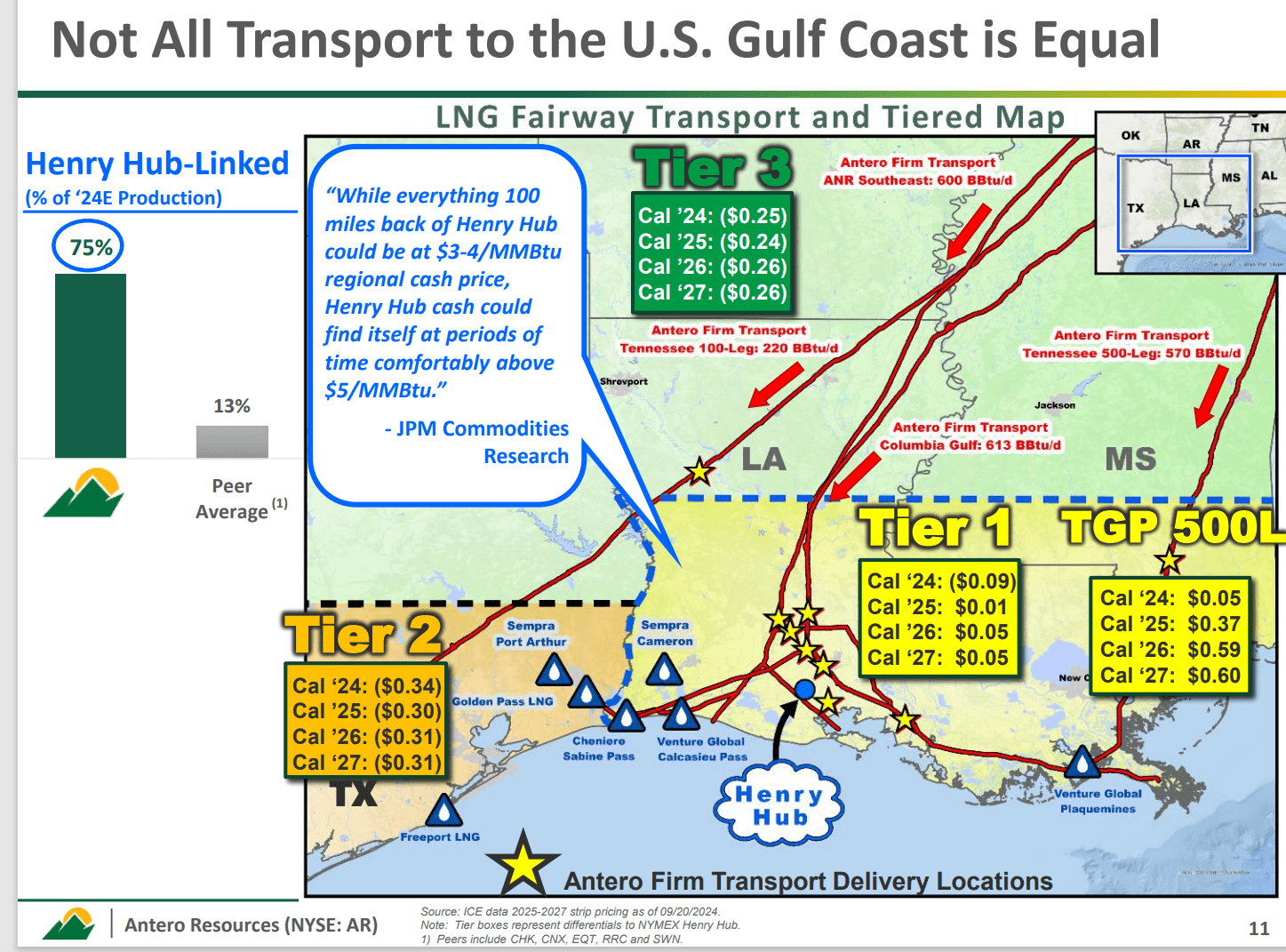

Antero Resources Natural Gas Export Pricing Considerations (Antero Resources Natural Gas Fundamentals September 25, 2024)

As Antero Resources (AR) demonstrates in their presentation, there is a big variance in pricing depending upon where the market for the natural gas is, even though most of what is shown above is for export. Clearly, some of those locations are showing a gain, and it is management's responsibility to get that gain for shareholders.

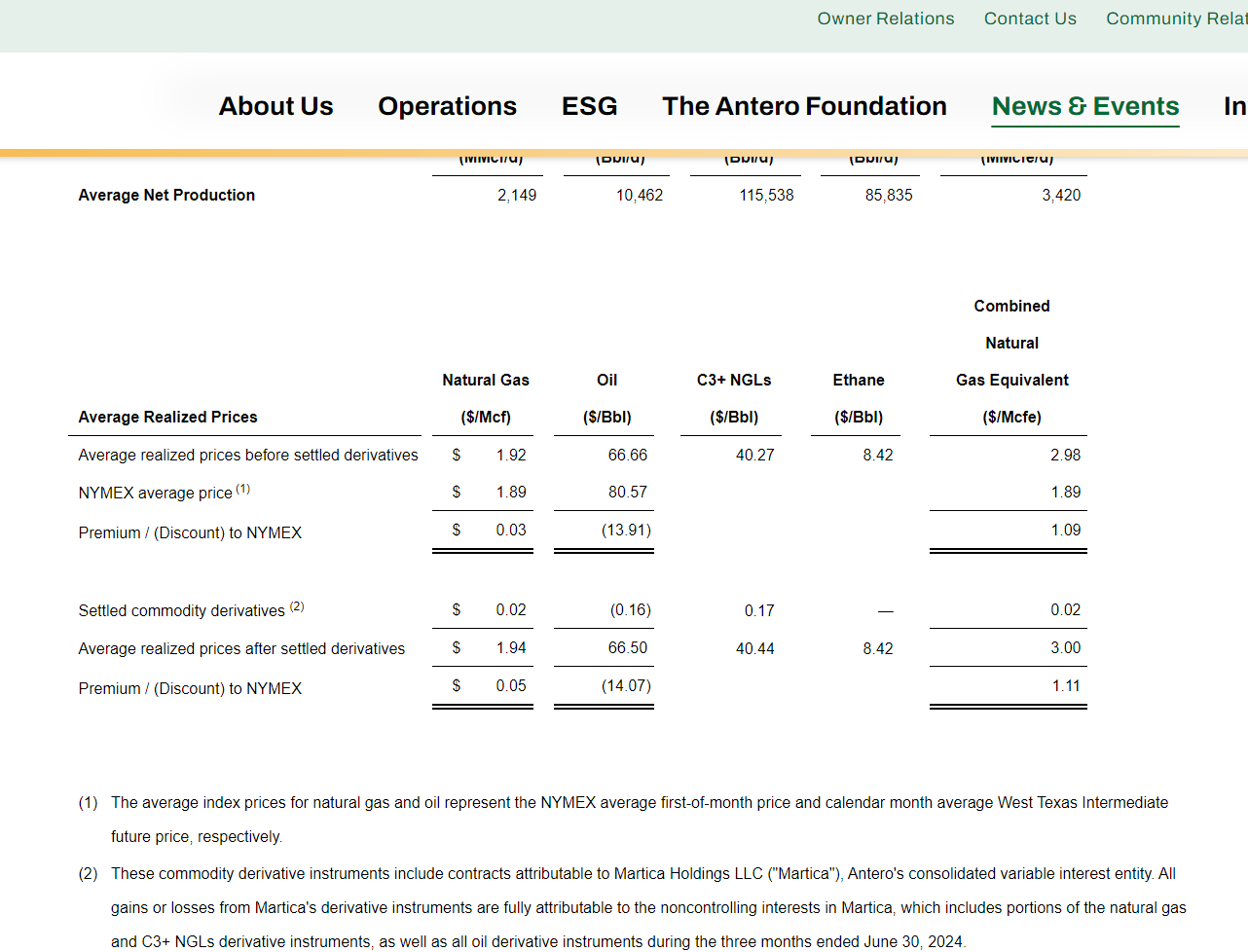

Antero Resources Average Price Received Calculation (Antero Resources Second Quarter 2024, Earnings Press Release)

When management gets better prices, then the natural gas result is shown above. Typically (but not always) Antero Resources beats that NYMEX benchmark. That generally means it has the highest or some of the best prices in the Marcellus basin.

With prices like those, the company is likely to have better prices than Expand reported for the third quarter before the effect of the liquids is considered.

Effectively, this lowers the breakeven point when compared to someone like Expand Energy that shows a price below the benchmark. What is even more interesting is that the settled derivatives, shown above, raise that advantage a little bit more.

It demonstrates that a determined management is not limited to the price of the hedging. This is a management that has not been afraid to redirect the natural gas to a market that is stronger than the hedging price. Shareholders then get the difference, even if it is not the market price of the stronger market.

So many managements do not spend nearly enough time getting the value they should be for their production. A lot relies upon superior geology to get better results. Expand clearly has a lot of profit potential when it comes to getting the product to market in the future.

Summary And Last Article

The last article noted that any GAAP or really losses of any kind could have and should have been avoided. Now the merger with Southwest Energy to create Expand is going to make cost control and marketing of product produced all that more important because the Haynesville is long known as the highest cost dry gas basin in North America.

The merger definitely expands the presence in that high-cost basin. So far, the results of the sale of the Eagle Ford properties and the expansion into the Haynesville are reduced profits, with still more reduced profits on the horizon.

This management has good enough geology that it reported positive adjusted earnings. But the strategy to expand the Eagle Ford operations would likely have done far better.

In the future, management will get the chance to demonstrate superior profitability. But until that track record is established, this remains a strong sell because there are operators out there that are doing far more with their assets than this company.

That includes the fact that this company, like other natural gas producers, will benefit from the recovery of natural gas prices when that inevitable recovery begins. There is simply too much money on the table that management needs to get to shareholders for this to be an investment consideration.

Risks

Any upstream operation is subject to the volatility and low visibility of future commodity prices. This company has the additional burden of having to shut-in expensive Haynesville production until prices get better. Because there is exposure to a higher cost basin, this company overall experience longer periods of losing money (on at least that part of the operation) and therefore needs the profitable periods to be very profitable. There is competition that suffers far less in a cyclical downturn.

This management has not really emphasized either cost control or maximizing the prices received for production. The investment grade rating is really about the debt being paid. It says nothing about management performing in the top quartile of the industry when it comes to costs and sales prices. In this case, there is a lot of improvement that is possible.

A loss of key personnel could set back the future company plans. In this case, some key personnel may need to go for this company to make progress on cost control and selling price maximization. However, if that happened, there is no assurance that the next executive lineup would do any better.

I analyze oil and gas companies like Expand Energy and related companies in my service, Oil & Gas Value Research, where I look for undervalued names in the oil and gas space. I break down everything you need to know about these companies -- the balance sheet, competitive position and development prospects. This article is an example of what I do. But for Oil & Gas Value Research members, they get it first and they get analysis on some companies that is not published on the free site. Interested? Sign up here for a free two-week trial.