Dragon Claws/iStock via Getty Images

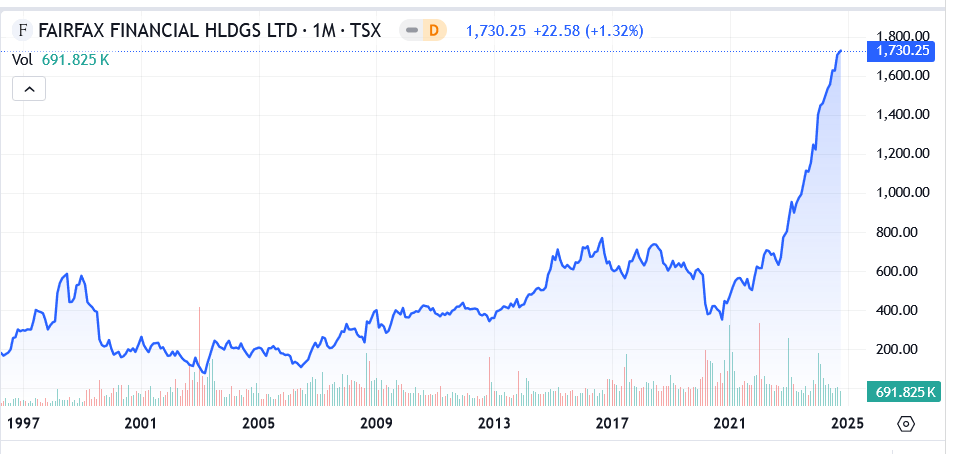

I must start with a Fairfax Financial (TSX:FFH:CA) (OTCPK:FRFHF) chart.

SA

What kind of miracle happened around 2021? Are there fundamental reasons for it? Is the chart going to continue straight up? How to value this beast?

Here is the basic background. Fairfax is a Canadian insurance company founded in 1985 by Prem Watsa, who was then 35. It trades in Toronto in Canadian dollars but reports in USD (US ADR is also available). Fairfax borrowed its model from Berkshire Hathaway (BRK.B) (BRK.A) and was so successful initially that the founder became known as Canadian Buffett.

It approached CAD ~$600 in 1998 but took another 16(!) years to repeat this achievement. After that - several years of inconsistent trading, COVID-related drop, and non-stop skyrocketing since 2021.

Berkshire, Fairfax, and everybody else

The Property and Casualty ("P&C") industry is as ancient as Babylon because its products are badly needed or even mandated across business cycles. In most cases, the industry is not subject to technological disruption.

On the negative side, insurance is a commodity without economic moats, or so economists say. Practically, scale, capital, and underwriting expertise protect big insurers fairly well. Catastrophic ("cat") events remain an existential threat to P&C carriers. However, diversification, various forms of reinsurance, and niche products mitigate or even hedge this risk.

As long as cat risks are manageable, P&C becomes attractive for investors due to its relative predictability over the long term.

P&C insurers possess funds from three sources: equity, long-term debt, and float. The latter designates funds received as customers' premiums before paying out claims. All funds from three sources can be invested and generate income. This is the reason why insurance is always related to investing.

Traditional insurers focus on underwriting while funds are invested mostly in high-grade bonds. A much smaller part, around 10% or so, may be invested in equities. Though countless variations exist, the principle remained unchanged until Warren Buffett.

For Berkshire Hathaway, underwriting remains a priority but funds on the balance sheet are invested in acquisitions of non-insurance companies and big long-term concentrated equity holdings.

Many readers of Buffett's letters interpret his words about float investing too literally. They think that Buffett courageously invests float in equities and acquisitions relying on his superhuman investment abilities. This is only partly true as displayed in the following table (all dollar numbers are in millions).

Author

In most years, the sum of cash and bonds on the balance sheet exceeds float. (Please note that float is an accrual concept. Within the insurer's investment portfolio, ALL funds are bundled together without boundaries, similar to a joint bank account!) Only when equities are very cheap or when Buffett sees extraordinary acquisition opportunities does float exceed the sum of cash and bonds, like in 2008 and 2009 or recently in 2022. In these years, Buffett really invested float in equities.

Even though Berkshire often holds more cash and bonds than its float, the difference is typically small. In most years, Buffett aggressively invests funds outside float, maintaining only a modest cushion for unexpected events like cat events. This is feasible because Berkshire has multiple other cash sources, such as cash flows from subsidiaries, dividends from equity holdings, and untapped borrowing capacity. Traditional insurers’ management is seldom this bold.

Only a handful of companies went Buffett’s way including Fairfax. However, the difference between Fairfax and Berkshire is huge. Not only in terms of their market caps (~$30B vs ~$1T) but also in terms of their operating model. Fairfax is much closer to traditional insurers than Berkshire!

Fairfax and traditional insurers

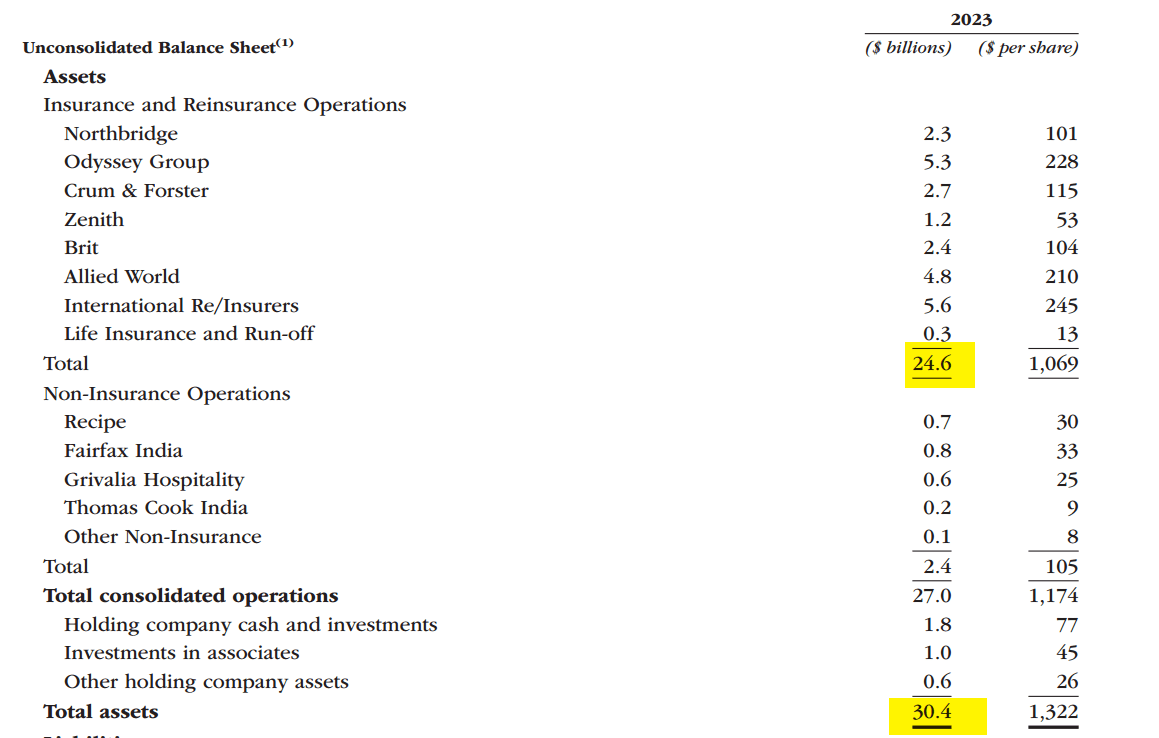

(Re)Insurance companies represent 24.6/30.4~81% of Fairfax's assets as displayed on the balance sheet from the latest Prem Watsa's letter.

Fairfax

Non-insurance companies represent 2.4/30.4~8% of assets with the holding company's investments and cash representing the balance. It tells something about Mr. Watsa's thinking. He prefers to acquire insurers rather than other businesses! This differs from Buffett's operations.

At the end of 2023, Berkshire had ~$1,070B of assets on its balance sheet. "Railroad, Utilities, and Energy" constitute ~$259B or ~24%. The rest (~$811B) is called "Insurance and Other" which includes insurers and holding company cash and investments including stocks, manufacturers, retailers, etc. In Berkshire's 10-K, I did not discover the separate number for insurance assets. However, there is a clue. Statutory equity of BRK's insurers was $303B at the end of 2023. GAAP equity should have been higher and assets - higher still. My rough estimate of BRK's insurance assets would be below $500B or below 50% of its total assets.

Within the spectrum from traditional insurers to Berkshire, Fairfax is much closer to traditional insurers. And this partially explains Fairfax's recent success. Mr. Watsa made it very clear in his letter: "We have benefited greatly from a hard market in insurance that began in 2019". For many years, Fairfax was patiently buying promising insurance companies until unquestionably benefited from this when favorable conditions materialized.

Over the last ~10 years, Mr. Watsa made sizable investment mistakes. One of them was investing $1.375B in Blackberry back in 2014, a big part of which was lost. He characterized it as follows: "Another horrendous investment by your Chairman. To make matters worse, imagine if we had invested it in the FAANG stocks! The opportunity cost to you our shareholders was huge! Please do not do the calculation! No technology investment for me!".

Another of Mr. Watsa's mistakes was hedging Fairfax's exposure to equities for several years. The opportunity cost was significant as equities were marching ahead.

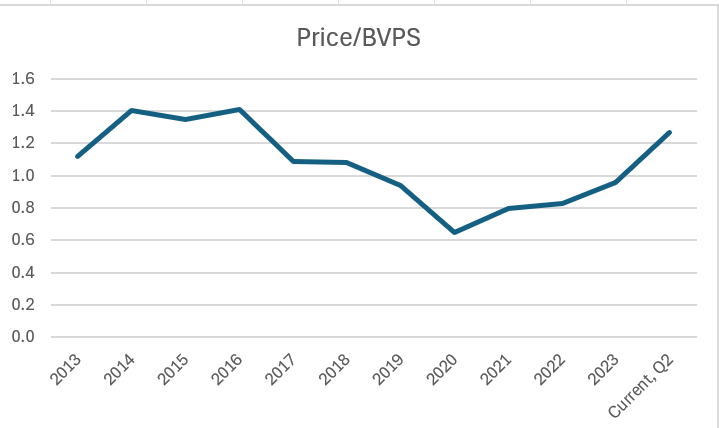

The unwinding of unsuccessful investments, the onset of a hard market in insurance, and share buybacks contributed to a rapid increase in Fairfax's book value per share—from $478 in 2020 to $979 in Q2 2024. This, in turn, led to a rerating of Fairfax’s valuation, with its P/BVPS rising from around 0.6 in 2020 to the current 1.3.

Author

What is Fairfax's value?

In terms of P/BVPS, Fairfax is slightly less expensive than Berkshire. Typically, BRK trades around 1.5 but is about 1.6 now. On the same basis, Fairfax is about 1.3 which is not exceptional as displayed on the chart. Most of Fairfax's insurers have gradually improved their operations and consistently delivered combined ratios below 100% while quickly growing.

It is well demonstrated in the table from Mr. Watsa's last letter that lists main Fairfax's insurers:

Fairfax

Growth is important for valuations. Being much smaller than Berkshire, Fairfax is in a good position to grow faster and have higher valuations! It is hardly guaranteed, but 1.3 for the price-to-book ratio may not be the limit.

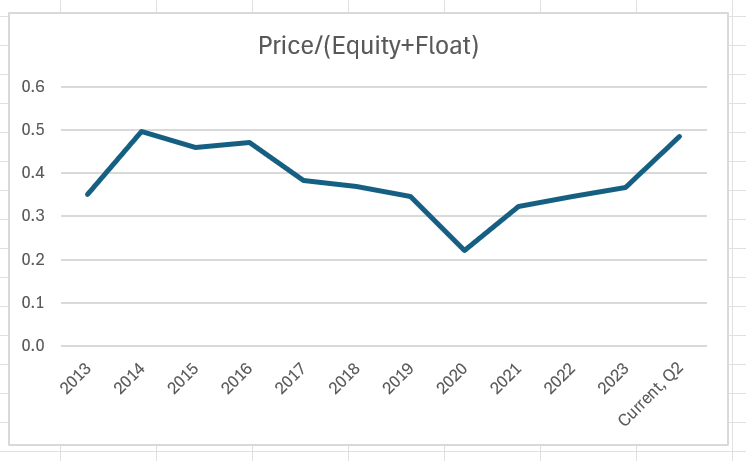

My regular readers know that I like to value Berkshire as the sum of equity and float. I explained the method several times in my publications with the latest here.

Imagine a P&C insurer that a)always underwrites profitably, b)consistently grows premiums, and c)reserves conservatively so that unfavorable development of prior years' reserves occurs rarely if ever. Both Berkshire and Fairfax, as well as good traditional insurers, fit this description.

Under these circumstances, our insurer can theoretically invest float the same way as equity since it will always have funds to pay claims from incoming premiums! Certainly, nobody is doing this but hopefully, you get the idea.

In practice, Progressive (PGR) - the best big insurer I know - trades higher than the sum of equity and float, Berkshire is close to the sum of equity and float and it makes sense to test Fairfax. The result is below:

Author

The valuations are twice as low as that of Berkshire! And they are consistent with 2014-2015. However, I would argue that today's Fairfax is a stronger company than 10 years ago.

Both metrics (P/BVPS and P/(BVPS+FPS)) imply that Fairfax has still some room to grow, perhaps to P/BVPS of 1.5 in line with regular Berkshire's trading range. Berkshire's quality is beyond comparison, but Fairfax's insurance business may grow faster. Correspondingly, FFH's value may be about 1.5*979*1.36 ~ CAD 1,997 vs. its current price of CAD 1,786.

Conclusion

I should have bought Fairfax a couple of years ago or even in 2023 when it was trading at book value but missed it. Today it might be still a buy but I am less certain.

The soft insurance market may suppress insurers's growth rates and profitability and in the case of Fairfax, I would not rely on anything else as it appears too small to move a needle. The investment in Blackberry has shown risks associated with concentrated stakes in non-insurance businesses.

Staying overly conservative, I will rate Fairfax as "Hold" but will gladly revisit it if the stock valuations drop.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}