Ole_CNX

Investment thesis

At the start of 2020, I wrote an article picking Cameco (NYSE:CCJ) (TSX:CCO:CA) as the stock that could be among the best long-term performers for the decade. It was trading at just under $9/share at that point. My most recent addition to my Cameco stock position was in early September when it dropped below $40/share. After the recent run-up in its stock price that brought its forward P/E ratio to over 90, I have been contemplating taking profits. However, it increasingly looks like the market is finally going all-in in terms of bullish sentiment on uranium, based on expectations of a new global nuclear power renaissance. Such periods of market enthusiasm do have a way of surpassing fundamental limits, so for now, I am holding my position, looking for a better opportunity to take profits, even though Cameco's valuation is getting to be increasingly hard to defend through fundamentals-based arguments.

Switching From A Buy To A Hold

Before we analyze the internal aspects of Cameco and the relevant external factors, I want to briefly address and clarify the reasoning behind my shift from a buy the last time I covered Cameco over a year ago, to a hold right now. Since I wrote that article, this stock has gone up over 100%, and at this point, I feel that the valuation is getting too far ahead of its otherwise solid revenues and earnings growth prospects. I by no means see a worsening trend in its overall performance or a deterioration of the uranium market on the horizon.

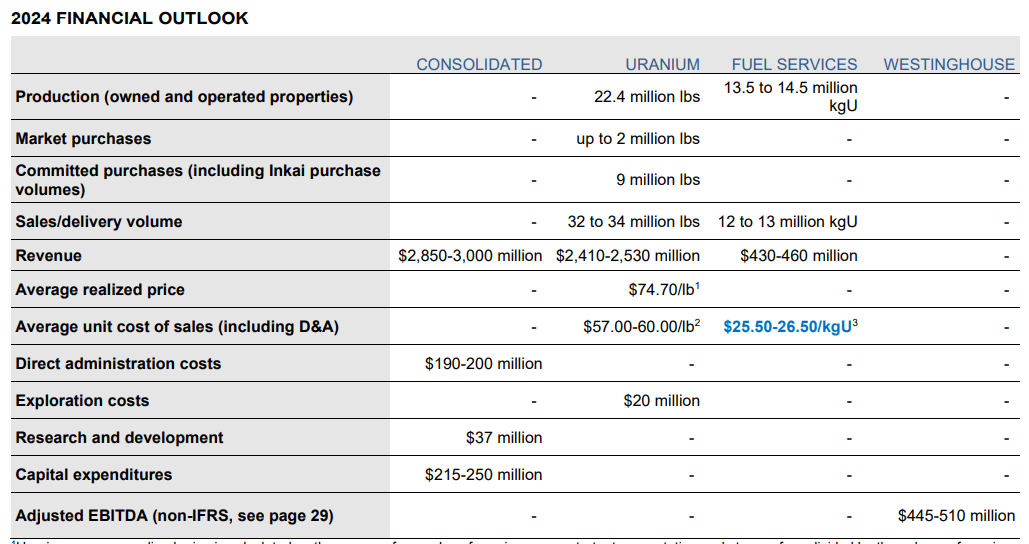

Cameco's Prospects For Production, Revenue, And Profit Growth, Vs. Its Runaway Valuation

For the latest quarter, Cameco saw an increase of 24% in revenues compared with the same quarter from a year ago. Revenues came in at $598 million. Its profits more than doubled for the same period from $14 million in Q2, 2023 to $36 million for the latest quarter. The outlook for the year suggests Cameco is currently trading at roughly eight times its expected revenues for the year.

Cameco

Uranium production surged by 61% compared with the same quarter from last year. Some of the uranium produced contributed to an increase in inventories, which acts as a drag on earnings since money was spent on operations that resulted in higher mined extraction than sales. In other words, Cameco's current profitability potential is better than the latest quarterly numbers suggest.

Cameco

One arguably negative trend observed in the last quarterly report was the decline in its cash position of just over $200 million. Its total debt declined by $300 million, and the value of inventories increased, which signals its net financial health is improving.

Interest on long-term debt reached $28.9 million, which amounts to 4.8% of revenues. I tend to worry once this ratio surpasses 5% because an excessive debt servicing burden can eventually hurt a company's earnings, and other aspects of its financial performance & health.

Production, Earnings & Revenue Growth, Vs. Valuation

Cameco is seeing robust growth in production & revenues, which arguably makes it a growth stock; therefore, it makes some sense for it to be trading as a growth stock.

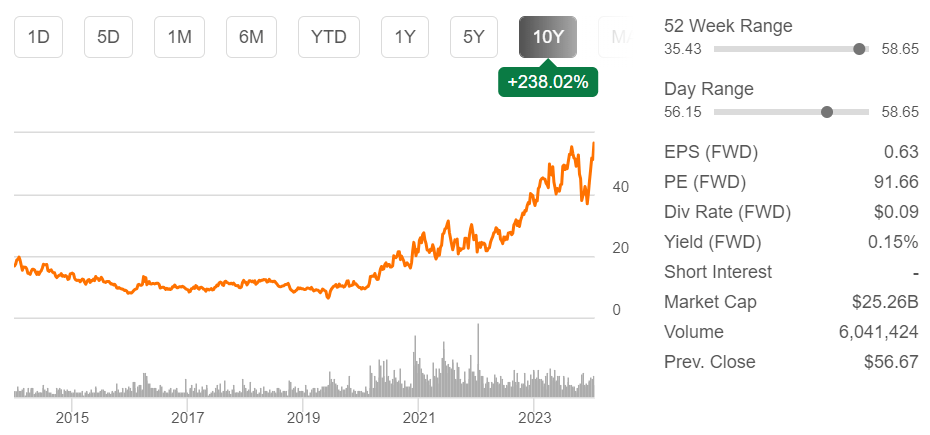

Cameco stock price & other metrics (Seeking Alpha)

As we can see, Cameco currently has a forward P/E ratio of over 90 which is significantly higher than many of the popular tech stocks that tend to dominate the finance & investment news cycle. For this valuation level to make sense, there has to be a credible argument in favor of robust growth expectations going forward.

An important factor to consider in this regard is whether Cameco has decent production growth prospects. There are many projects where Cameco can either increase production or start new mining operations. The Millennium Project in Saskatchewan is one such opportunity to significantly increase production if the market signals warrant the full development of the mine. It is estimated that it has 53 million pounds of indicated resources in place, as well as 20 million pounds of inferred resources. Based on these resources, Cameco could increase production by about 7 million pounds per year, on average, once production commences.

The Yeelirrie Project in Australia has 128 million pounds of measured and indicated resources. It is unclear at what pace of production Cameco will produce those resources, once it decides to bring them online, but at the moment it does not see a need to commence development. The Kintyre project in Australia is in the same standby status phase, and it has almost 60 million pounds in indicated & inferred resources.

Between these three projects that are on standby, Cameco can bring an extra 250 million pounds of uranium or more to the market. The current value of these standby resources based on the uranium spot price is about $20.8 billion. Assuming a 10-year mine life on average, these mines could hypothetically provide an extra $2 billion/year in revenues if they were to be brought online simultaneously. With all else held equal, earnings would double as well.

While Cameco's standby projects have the potential to increase production significantly, perhaps double its current output, it does not seem to be nearly enough to justify its current market cap. Uranium prices, and by extension Cameco's realized price, need to rise significantly in order to help it catch up to its valuation.

Uranium Market Prospects

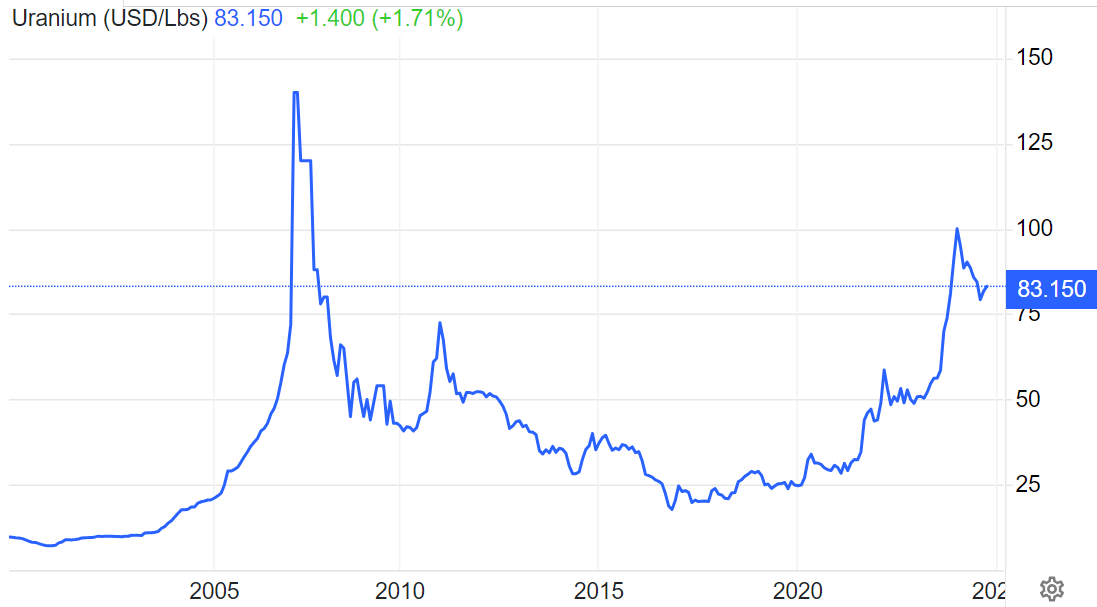

Trading Economics

The spot price roughly quadrupled since I called the bottom of the uranium market almost a decade ago. It may be tempting to assume that after such a dramatic increase in uranium prices, there is very little upside left.

The one aspect of nuclear power that needs to be understood is that, unlike most other commodities, its consumption dynamics are not as easily affected by price swings. Nuclear reactors need fuel, and the cost of fuel in the total cost of nuclear power production makes up a relatively small percentage of the total cost. For instance, The Nuclear Innovation Alliance estimates that raising the cost of uranium ore from $30/lb to $130/lb will increase the cost of producing nuclear power by about 1/6.

Higher uranium prices will not cause nuclear power plants to shut down. It does not prevent new ones from being built, especially the ones that are already under construction. The four-fold increase in uranium prices since the bottom certainly doesn't seem to curb the growing enthusiasm for nuclear power.

The latest positive trend seems to be a push to use small nuclear reactors to power AI data centers. More broadly, utilities and national governments have an eye on nuclear power as a solution for dealing with issues such as reducing emissions or dealing with hydrocarbon fuel shortages. For instance, nuclear power seems to be gaining traction in the EU after it ended its dependence on Russian natural gas. Italy is the latest nation to pursue new nuclear reactors. Not long ago, it was thought that nuclear power had no future in the EU, given pressures to shut down existing reactors.

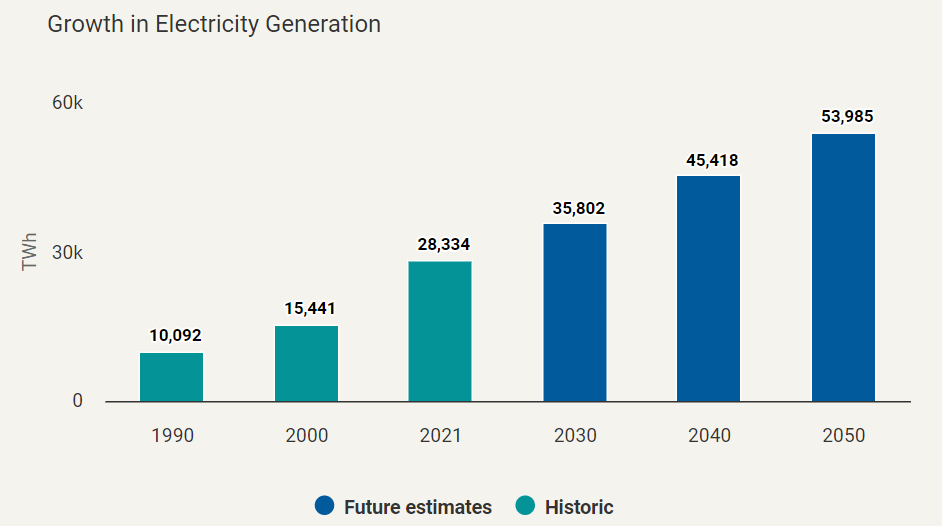

Several factors, ranging from environmental concerns associated with burning coal, to supply growth constraints for the oil & gas industry due to a lack of new conventional field discoveries so far this century are all having a positive impact on non-hydrocarbon energy demand growth. The electrification of the global economy is estimated to lead to an approximate doubling of electricity demand by 2050 from current levels.

Cameco

Initially, it was hoped that wind & solar power would replace current hydrocarbon electricity generation, as well as nuclear power, which is also opposed by environmental groups.

A very little noticed and discussed turning point came about in 2021, when the EU, which is a leader in wind & solar power generation suffered through a serious energy crisis, due to the intermittent nature of renewable energy. Germany, for instance, saw a 13% decline in onshore wind power generation in 2021, compared with the previous year. Other countries experienced a shortfall as well, which led to a massive increase in natural gas demand to compensate for the shortfall, thus a massive price spike. It is not entirely well known and understood that the EU's natural gas price crisis started in the fall of 2021 before the Ukraine war became a full-blown confrontation in 2022.

The discussion that needs to be had around the subject of energy security within the context of the push for intermittent energy sources to dominate the grid is not a pleasant one, which is why the discussion is not taking place in the public sphere. It does seem that at government policy and private sector levels, the lessons of the 2021 energy crisis in the EU were learned, even if with some delay. There are currently 59 new reactors under construction, in addition to the 441 reactors that are currently operational. Four of the reactors currently under construction are in the EU. Based on Italy's latest signals, we will likely have significantly more nuclear reactors under construction in the EU within a few years. Other countries around the world are also looking at nuclear power as an increasingly desirable solution to their energy needs.

There are still about 750 million people who lack electrical power in their homes, while the world's population is growing by tens of millions of people every year, which means that potentially hundreds of millions of new electricity consumers are going to be added every year going forward. At the same time, the global personal transport system is becoming more electrified. AI data centers are increasing their energy use at a rate of about 20% per year.

These are all factors that are set to increase electricity consumption per capita, even as the number of consumers of electricity is rising as well. Adding it all up, electricity demand growth, which is already forecast to be robust, has the potential to surprise on the up-side. Environmental & hydrocarbon availability issues are likely to put a strain on the world's ability to meet that demand. We are also coming to terms with the limits of wind & solar. As a result, nuclear power demand may surge around the world. With the prospect of small reactors coming online within a few years, which have the potential to scale up nuclear power capacity much faster, as well as old reactors having their life extended, global uranium demand may surge within a few years beyond some of the most optimistic expectations.

Investment Implications

After the sizable increase in its stock price, and considering its high P/E ratio, ordinarily, this would be a stock I would be selling. I first bought Cameco stock in 2017, and I traded it semi-actively along the way, reducing my position after significant stock price upswings while adding more after significant dips. I intend to continue doing this for the foreseeable future. I believe that the uranium market is just in the early phases of a prolonged bull run. Most of the long-term fundamentals are going in its favor. I intend to take profits again once its stock price rises above $60. Then I will probably add more shares to my portfolio in response to the next significant dip in its stock price. For now, the stock is a hold from my perspective. It had a good run, and the market is currently bullish on the entire sector. Actively trading it on the way up, taking some profits after new record highs, while buying the dips can help to enhance returns, which is needed going forward because an almost 600% increase in its stock price that we saw in the first half of the decade is unlikely to be repeated in the second half, no matter how positive the outlook for the uranium market happens to be going forward.