FluxFactory

TopBuild Corp. (NYSE:BLD) is in the homebuilding industry, with a market leadership position on the insulation side of this space. Sailing through data center expansion trends and an improving interest rate environment, I believe the company is on its way to seeing some solid growth in the upcoming years. Although the stock's relative valuation is significantly higher than that of its peers, I believe it is priced for growth, and therefore is a good one to hold.

Overview

TopBuild Corp. is a Florida-based construction company that specializes in installing insulation and other specialized building materials in a number of verticals in the residential, commercial, and industrial spaces throughout North America. With a $12.4 billion market cap, and annual revenues exceeding $5 billion, TopBuild is among the largest players in this competitive space. It stands out due to its exceptional margin expansion, strong balance sheet, variable business model structure, and market beating returns over the last decade.

I believe, through its strong financial and market position, the company is well-suited to take on further growth in the upcoming years, supported by a number of broader tailwinds. I believe an improving interest rate environment is very promising for the construction space, as new projects can now be initiated at lower financing costs, which boosts the demands for TopBuild services, especially in its specialty distribution segment through insulation material installation.

Another key growth driver, which I find particularly compelling, is the growth in data centers across the US. Between 2023 and 2024, alone, North American markets saw a 70% jump in new data centers under construction. These facilities typically function in highly controlled and regulated environments, which make specialized and reliable insulation absolutely critical.

In the Pacific-Northwest zone, BLD is actively working on a 27 acre data center project, whereas in the Southwest side, the company is active with 6 large data center facilities. In just one of these, TopBuild had been awarded a contract to install more than 55,000 feet of linear insulation. The backlog involving these large data center projects continues to grow on, and will likely pour over revenue well through 2026.

Performance Review

Q2 2024 had been exceptional for TopBuild Corp., enjoying the combined benefits of greater volumes and an improved fiberglass pricing environment, delivering the highest quarterly revenue figure in its history of $1.37 billion. It did this in an extremely tough macro climate that brought volatility in housing demand and delays on projects on the commercial side. To add, the acquisitions the company had undertaken also added to its overall growth. This is clear in the company's topline which saw a general climb of 3.67% YoY, during the quarter. Looking at this from a segmented perspective, this was driven by a 5.2% climb on the installation side, and a 3.2% jump on specialty distribution. Impressively, residential sales saw a 6.7% climb during the quarter, with an improving landscape on single-family housing units.

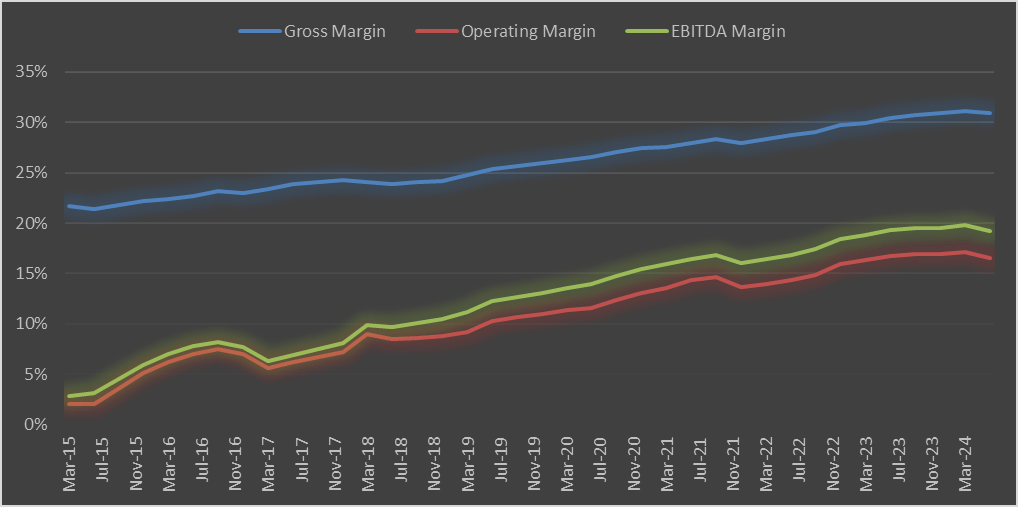

While the gross profit showed only slight improvement from $422 million to $424 million, the gross profit margin was less impressive with a 98 basis point reduction from 32.02% to 31.04%. This, however, is explained by an abnormally higher comparable in the prior year, due to a one-time benefit of nearly $10 million in 2023. Once accounting for this, the company's gross margin decline is limited to 30 basis points, mostly caused by a dilutive effect due to acquisitions.

A similar effect had been seen on the operating income side of things with its 0.63% decline to $236.7 million, and a margin fall of 75 basis points, once again exacerbated by the unusually high comp. The same was the case for the company's EBITDA, which actually jumped from $270.8 million to $271.7 million, while its margin saw a 9 basis point fall of 19.26% to 19.17%. When excluding the $10 million one-time benefit, there was actually a 10 basis point increase this year, leading to the highest EBITDA margin in the company's history. Moreover, incremental same-branch EBITDA margin amounted to a remarkable 41.2% figure.

Overall, it would appear that the company's performance during the quarter was lackluster, but when accounting for abnormalities, we see some pretty top-notch results, as identified above. These have come about despite some tough conditions, especially with the high interest rate environment throughout the first half of the year. As a result, projects on both the commercial and industrial sides have been delayed, and pushed on to 2025. I am encouraged by the fact that these were delayed, rather than cancelled, which could very well lead to a topline growth in the following year. The 50-basis point rate cut by the Fed is also a welcome sign, as I believe it will pave the way for the easing up of residential and non-residential construction projects, in turn improving demand for Top Build's offerings.

Positive results in a tough climate are a welcome sign. What I am drawn to in particular, however, is the company's sustained efforts on margin expansion, over the long term. While gross margin has shown a decent climb driven by more optimized pricing, higher volumes, and an improved control on costs of sale, the climb on the operating and EBITDA margins are especially impressive.

Author

Sustaining an expansion of margins this consistently despite carrying out acquisitions is a sign of a good business to me. Even the pandemic related business shutdowns in 2020 did little to stop this upward push on the margins.

A large part of this success lies in what the company calls its special operations team, which has a broad objective of maximizing productivity, and by extension, improving profitability margins. Considering that the company has over four hundred branches across its network, there is bound to be a bottom quartile struggling on the profitability front, with room for improvement. This is where the opportunity for further margin expansion lies.

Additionally, I am also drawn by the company's high variable cost model, with most of its costs lying in labor and to a lesser extent, in material purchases. The company has managed to control both these fronts very well in response to broader slowdowns, ensuring stable profitability margins, no matter what the situation. Considering its massive size and scale of operations, it is difficult not to be impressed by such a feat. This model is also why I am confident that, with an improved macro climate (the possibility of which, I believe, is quite probable), there is little doubt that the company will see a swift surge in its top and bottom line figures.

Valuation

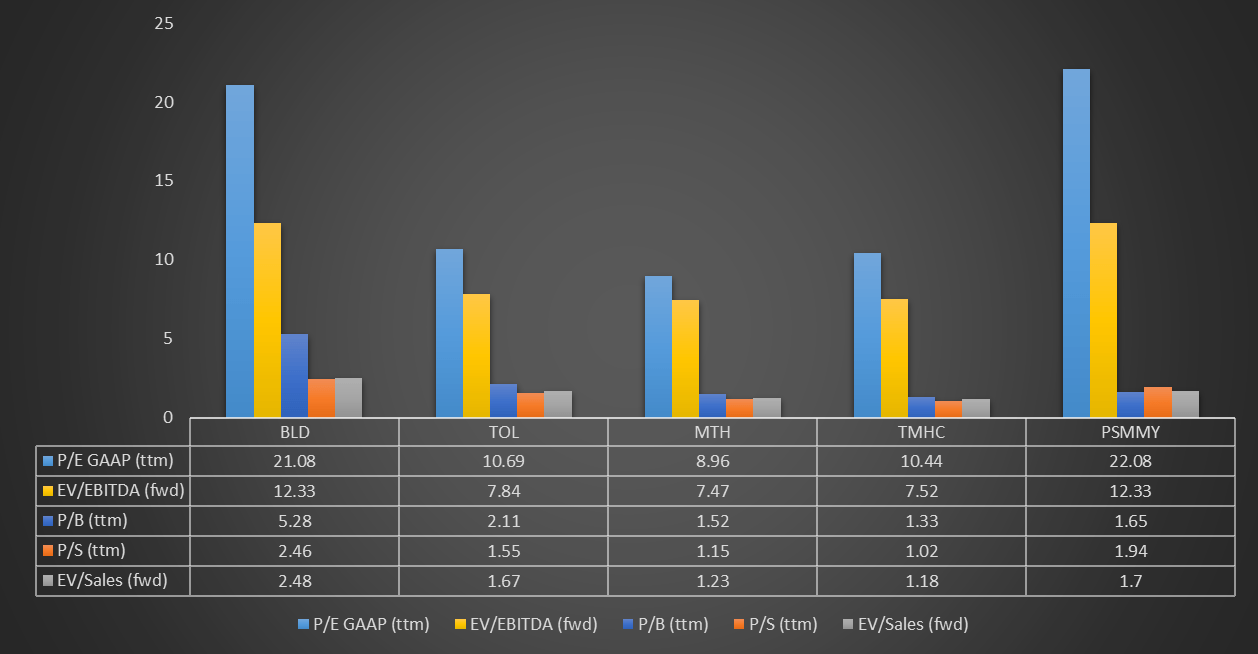

In the last 10 years, while the S&P 500 had taken on a climb of 192%, BLD has undertaken a momentous take-off of almost 1700%. That's almost nine times the growth the S&P 500 undertook, showing the incredible potential inherent to the stock. With robust tailwinds supporting its sails and a successful approach to growing its profit margins, the stock shows all the signs of being a no-brainer. However, does the stock's valuation also confirm this opportunity?

In order to examine this, I compare the company to its peers from the homebuilding industry. Laying out these companies' price and valuation multiples across, we see a noticeable disparity that shows how much higher the overall market is pricing BLD in pretty much all the chosen multiples:

Author

Normally, with a disparity this significant, I would be inclined to rate any stock a sell. However, I do believe, however, that the stock is priced for growth, and these are fair levels we are seeing. High price multiples demand a return that is larger than that of its peers, and I feel that this is quite likely with BLD. An improving macro environment is quite probable, especially with the lowered interest rate, the company's high variable cost structure, and an improved pricing environment. I believe the market also has priced the stock with the expectation to see some strong growth in the upcoming years.

For these reasons, I rate the stock a hold.

Risks to Thesis

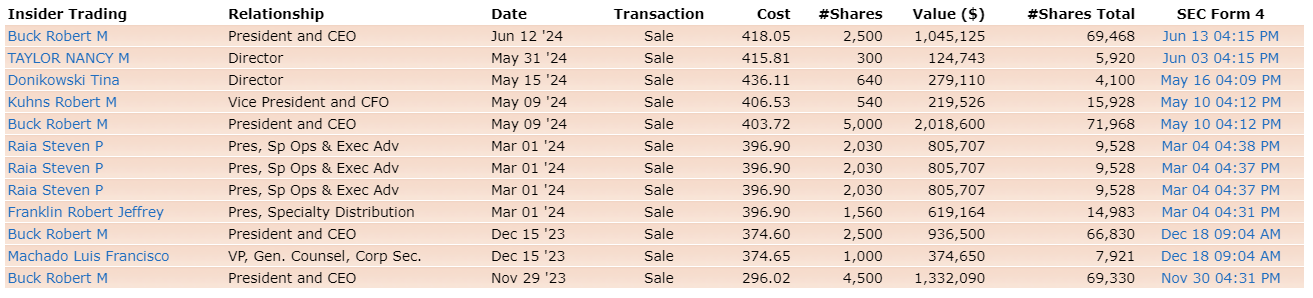

Although I believe my value thesis on BLD is pretty solid, I should point out the main risk I see to my thesis. Insiders have been engaged in substantial selling throughout 2024, with the most substantial transactions coming from the CEO and President, Robert Buck:

Finviz

Direct selling at these volumes could be a cause for concern and also casts doubt on my $492+ target estimate on the stock. These are individuals with a much clearer understanding of the company's operating margins, expansion, and ability to meet topline estimates.

Moreover, the insider ownership of below 0.7% also adds to my concerns of how little the company's management has a stake in the success of the stock, over the long term.

While these things could be seen as dissuading to some, I think it should not be that big of a deal. These transactions have all occurred before the Q2 results were announced, and in the four months since, there has been no notable sales seen. I do not think the company faces the risk of any sort of downfall, even though the sales this year by higher ups does raise some questions.

Investor Takeaway

TopBuild Corp. is a solid company with good fundamentals and a proven growth track record. I am especially encouraged by its consistent profit margin expansion over the years, even while powering through tough macro environments, and engaging in acquisitions, which typically dilute margins.

With strong tailwinds and an improving economic environment, I believe the stock is capable of continuing its margin expansion trend along with overall growth. Going by these trends, there is a significant upside to BLD stock. Although it shows price multiples significantly higher than its peers, I believe the stock is priced for growth, and that is why the market is likely applying a premium to its price.

{kind=link}

{kind=link}

{kind=link}