z1b

Patience is a powerful tool when it comes to waiting for a decent price before pouncing on a stock. Rushing into a purchase based on emotion or hype can often lead to overpaying, or investing in the wrong stock altogether. Being patient allows investors to wait for the right time and price, thereby giving themselves a better margin of safety.

Plus, getting a good price on a dividend stock is especially meaningful, considering that a lower price not only sets up the potential for more share price appreciation but also a higher starting yield.

Such appears to be the case with Brookfield Renewable Partners (NYSE:BEP), which is a dividend stock that I'd like to gain more exposure to and, as shown below, is again hitting a valley after running up above the $28 price point in recent months. The recent drop to $25.92 has also pushed up the dividend yield to an appealing 5.5%.

Seeking Alpha

I last covered BEP back in July, highlighting its stable and growing revenue base supported by long-term power purchase agreements. Thanks in part to dividends, the stock has done well for investors, providing an 8.3% total return since my last piece, outpacing the 4.9% rise in the S&P 500 (SPY) over the same timeframe.

In this article, I revisit BEP including recent business performance, and discuss why investors ought to consider BEP on the drop with a great starting yield, so let's get started!

Why BEP?

Brookfield Renewable Partners issues a Schedule K-1 and is a leading global renewable energy company with a diverse portfolio of assets including hydropower, utility-scale solar, wind, battery storage, and biofuels, among others.

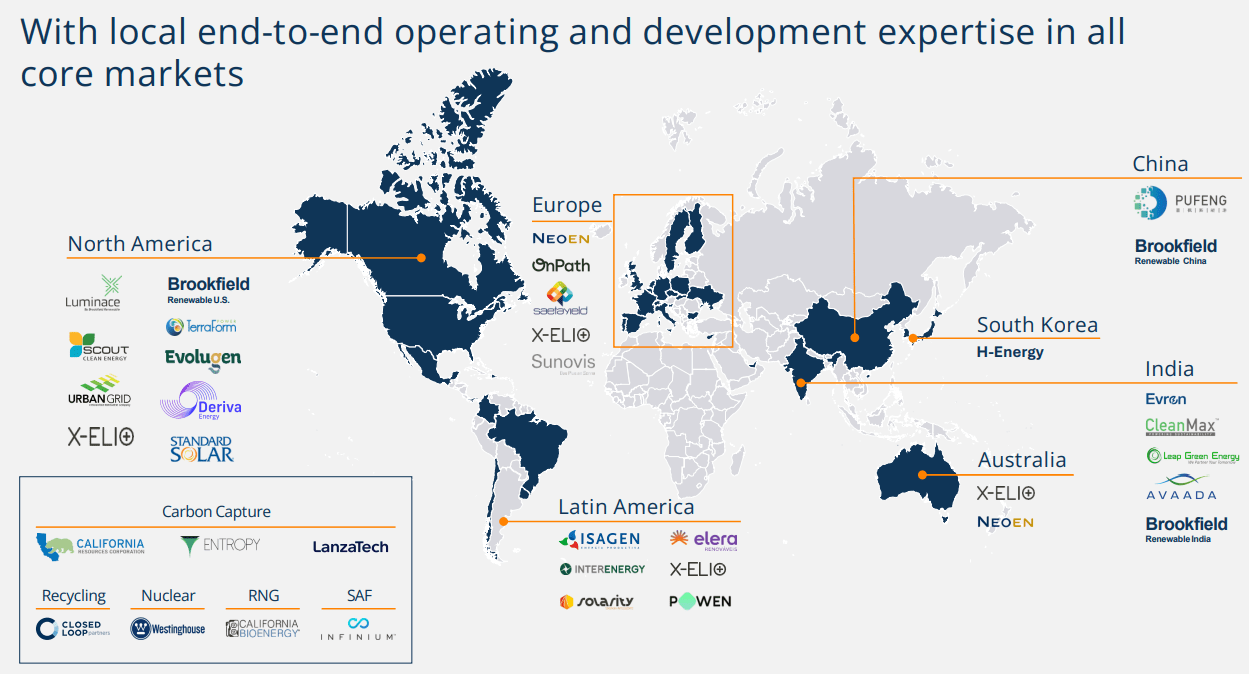

What I like about BEP is the fact that most (90%) of its revenues are contracted under PPAs (power purchase agreements) with an average life of 13 years. BEP is also inflation resistant, given that 70% of revenues are indexed to inflation. BEP has materially grown over the years, offering investors exposure to a range of renewable energy projects including carbon capture, nuclear, renewable natural gas, and sustainable aviation fuel across diverse geographies spanning North and South America, Europe, Asia, and Australia.

Investor Presentation

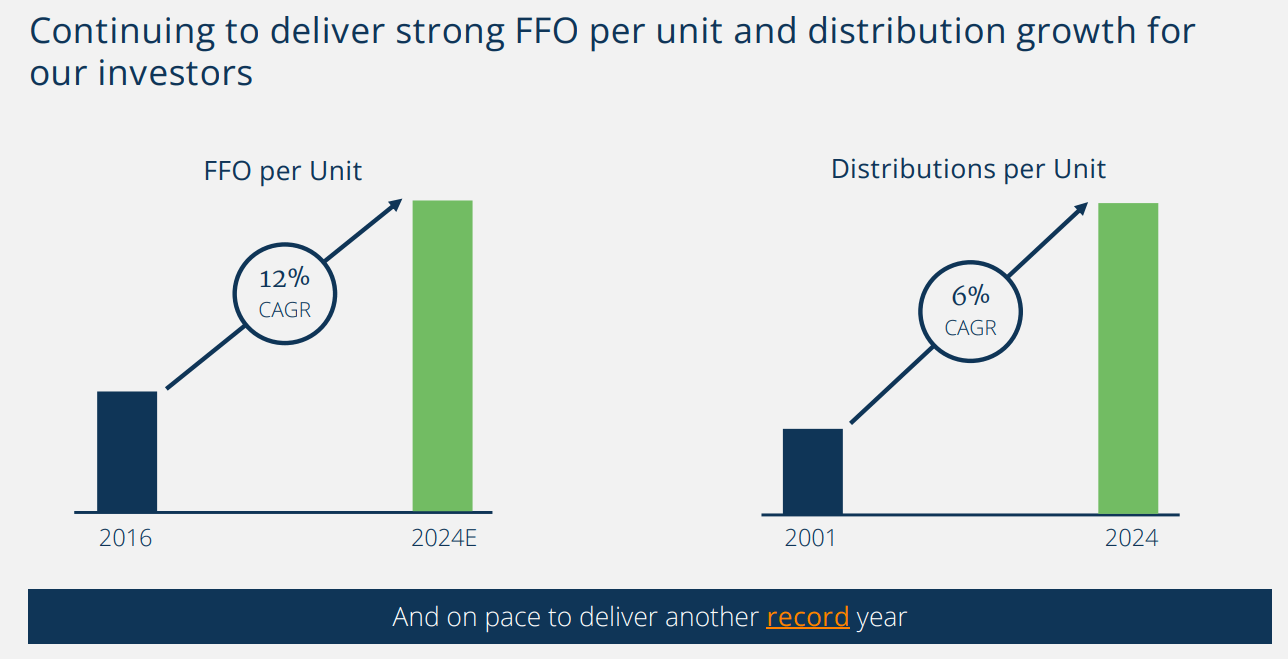

Importantly, BEP hasn't grown just for empire-building purposes, as it's demonstrated a track record of accretive results for shareholders. As shown below, FFO per Unit has grown at a 12% CAGR over the past 8 years, and Distributions per Unit has grown at a 6% CAGR since 2001.

Investor Presentation

Meanwhile, BEP is demonstrating solid growth with FFO growing by 9% YoY to a record $339 million during Q2 2024. FFO per unit grew by 6.3% YoY from $0.48 in the prior year period to $0.51. The robust growth is driven by the delivery of a number of completed projects across wind, solar, and battery storage, representing 1.4 GW of new capacity added to electric grids worldwide. In addition, BEP also saw robust performance from its existing asset base, with its hydro fleet benefiting from strong pricing in the current market, in which demand for clean power is accelerating.

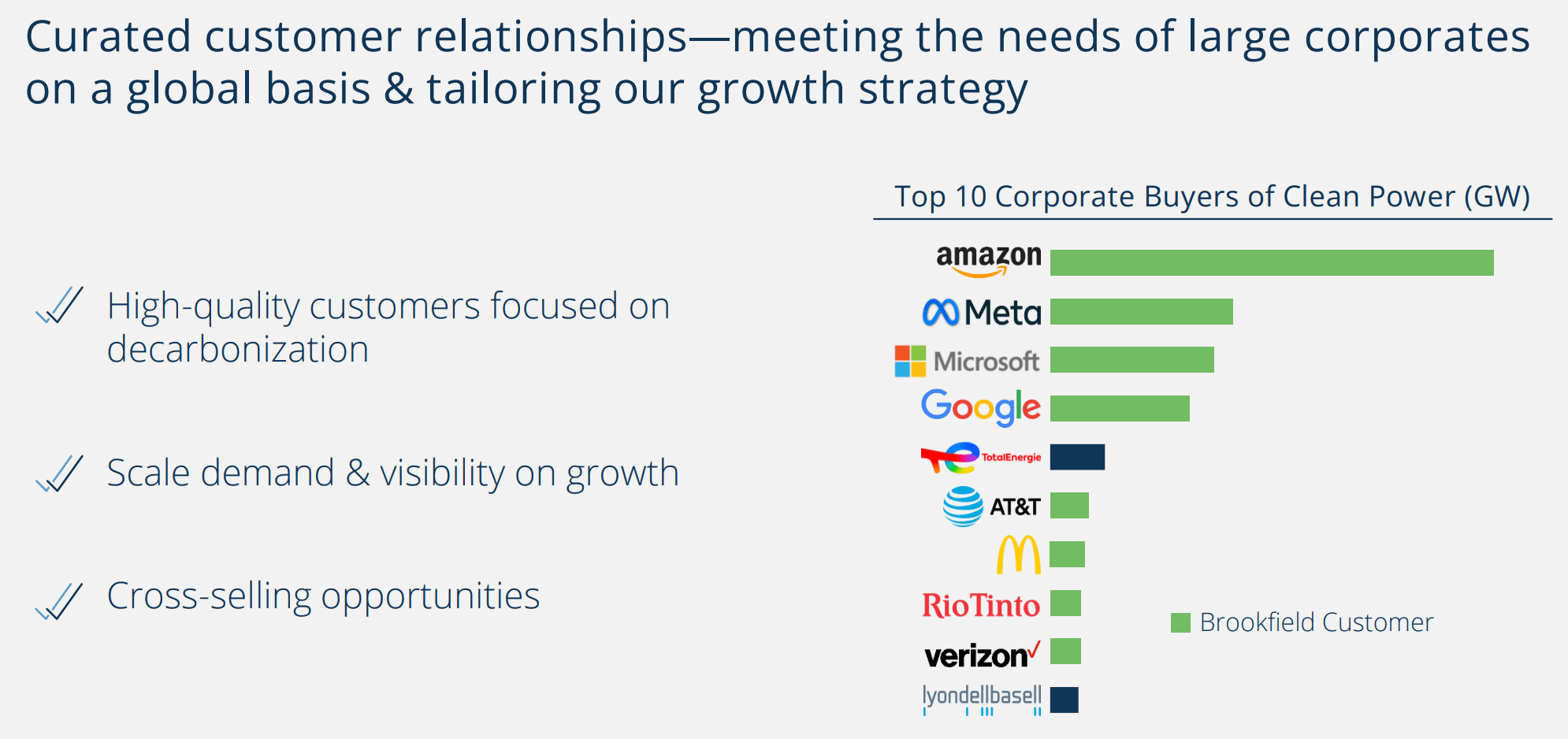

Management is guiding for double-digit FFO per unit growth this year, with the backing of a strong development pipeline, which now stands at over 230,000 MW, of which 65,000 MW has advanced stage land, interconnection and permitting status. This serves a wide range of corporate customers, which, as shown below, include Amazon (AMZN), Meta (META), Google (GOOG), AT&T (T) and McDonald's (MCD), among others.

Investor Presentation

Over the medium term, BEP stands to benefit from its agreement with Microsoft (MSFT) to deliver over 10.5 GW of new renewable energy capacity between 2026 and 2030. MSFT's recent agreement with Constellation Energy (CEG) to reopen the Three Mile Island nuclear plant also bodes well for BEP, as its Westinghouse Nuclear Services business stands to benefit from growing demand from corporate customers including technology companies and centralized utilities.

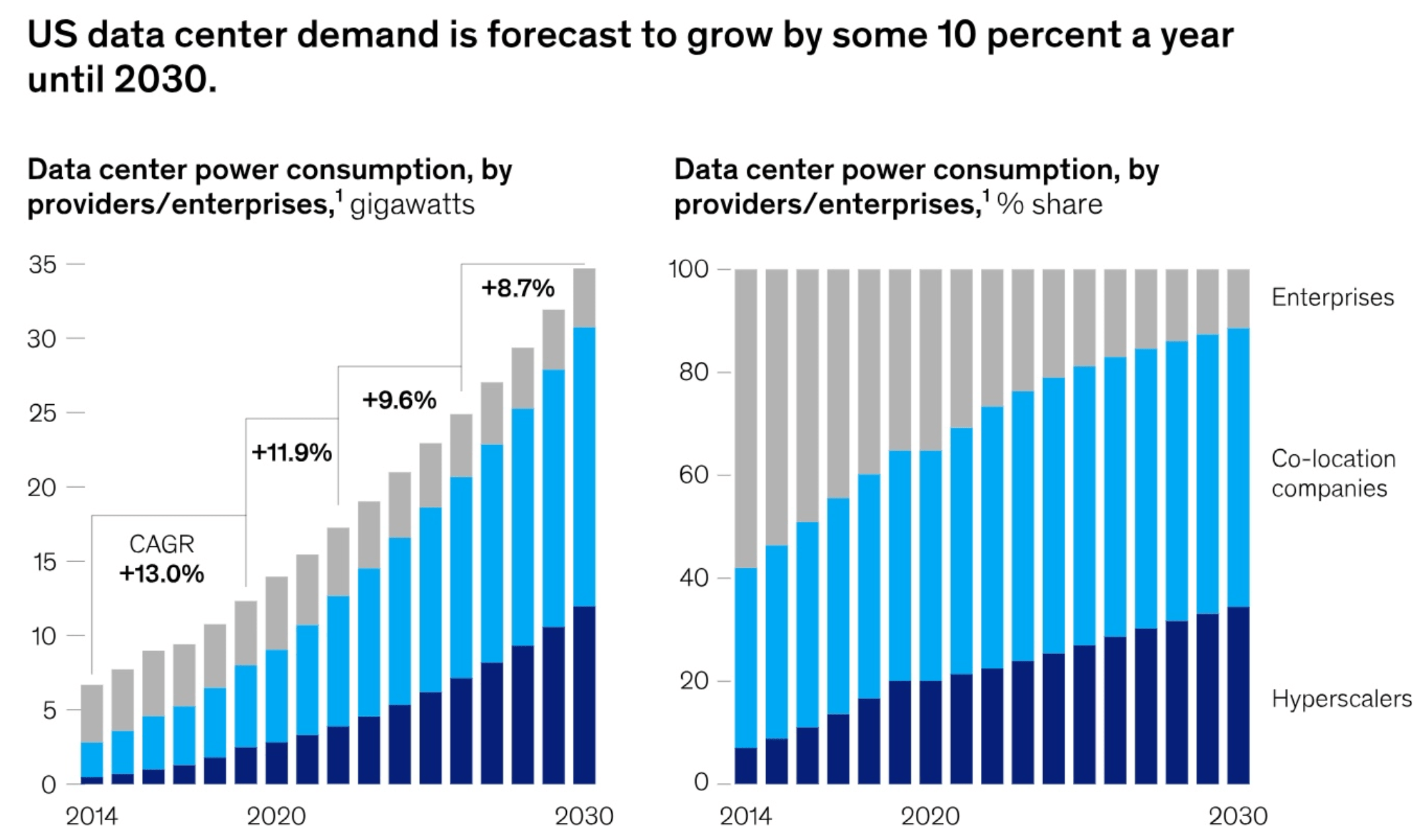

Data centers for Microsoft and other tech players represent a material growth driver for BEP, with management estimating that 10% to 20% of global electric consumption could come from this segment by 2030. According to McKinsey, US data center power demand is expected to grow at a 10% CAGR through the end of this decade.

McKinsey

Last but not least, BEP's pending acquisition of Neoen includes a recent 20-year capacity contract for 800 MW of batter storage from an Ontario grid operator. Management commented on the value of this acquisition during the recent conference call:

Neoen's core markets are some of the fastest growing for renewables globally with strong corporate power demand and high barriers to entry. Neoen's pipeline and development capabilities perfectly fit the growing demand we are seeing for clean energy solutions.

The addition of Neoen to our portfolio immediately makes us a top player in each of its 3 core markets. where we can supplement the company's existing end-to-end local capabilities with our global value add in areas such as procurement, corporate contracting and capital markets.

Lastly, we highlight that Neoen is a global leader in battery storage. Neoen has almost 2 gigawatts of battery storage operating or under construction and a significant global pipeline which will further diversify and complement our technology tool kit.

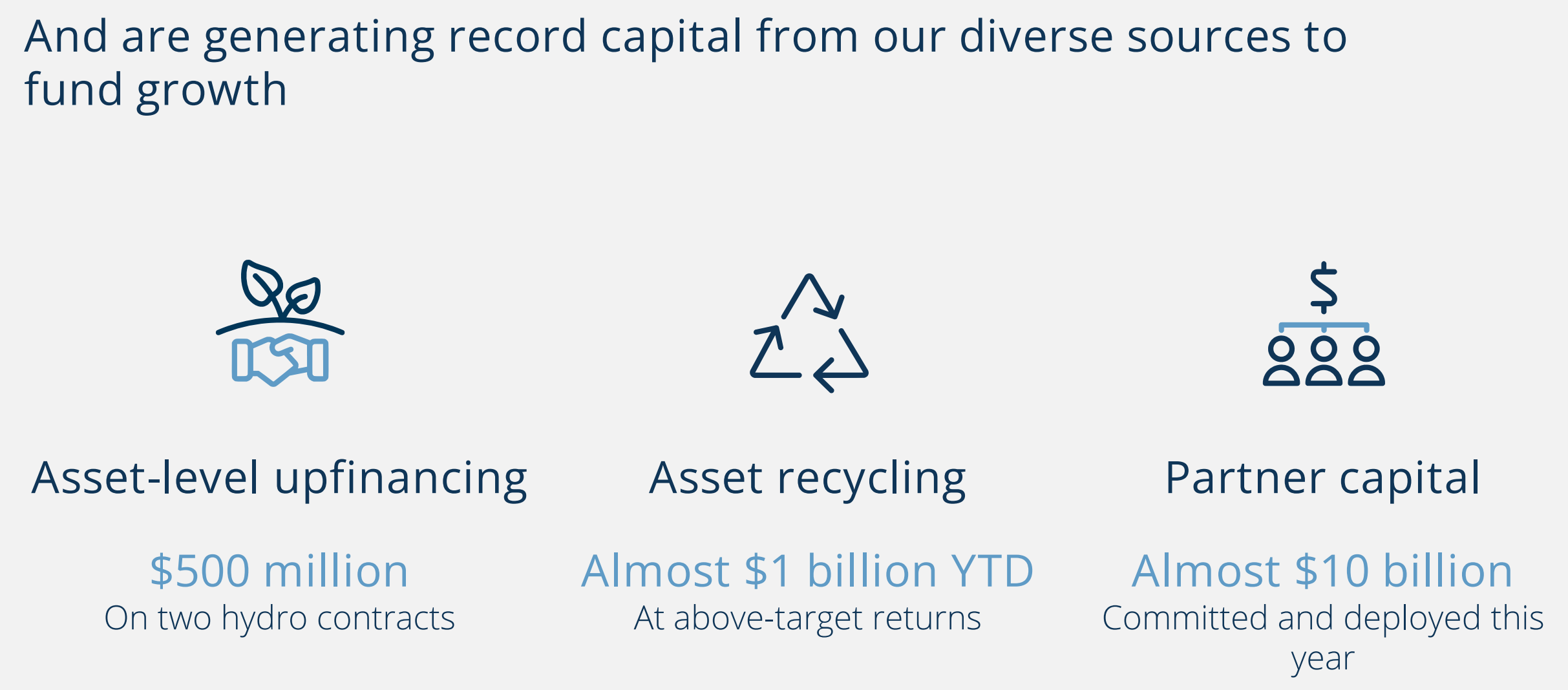

BEP carries a strong balance sheet to fund growth, with a BBB+ credit rating from S&P and $4.4 billion in available liquidity. 96% of BEP's debt is held at a fixed rate, and it carries well-staggered debt maturities, with no debt maturing this year and a weighted average debt term of 12 years. As shown below, BEP has a range of options to fund growth including asset-level financing, asset recycling, and partner capital, which don't require material leveraging of balance sheet debt.

Investor Presentation

Importantly for income investors, BEP currently yields 5.5% and the distribution is well-covered by a 77% payout ratio, based on management's FFO per share guidance of $1.84 at the midpoint of range for this year. The current quarterly dividend rate of $0.355 stands 5.2% higher than the prior year period.

I find BEP to be appealing after the recent dip to $25.92 with a forward P/FFO of 14.1. This is considering the 5.5% distribution forward expectations of 10% FFO per unit growth for this year and potentially beyond, given the strong demand and robust pipeline of opportunities. The distribution yield and forward growth rate support potential market-beating total returns from here, thereby giving the current valuation a strong margin of safety.

Risks to the thesis include BEP's diversified approach toward renewable energy, which means that it could potentially grow at a slower rate than pure-play operators that specialize and focus on one source, like nuclear power. Plus, just under half of BEP's revenues come from hydropower, exposing it to periods of potential weakness based on weather patterns. Lastly, competition from fossil fuel sources like natural gas, which is currently cheap and abundant, makes renewable power less attractive without government subsidies.

Lastly, more risk-averse investors may want to consider BEP's Preferred Series A stock (NYSE:BEP.PR.A). This preferred issue currently trades $21.38, representing at a 14% discount to its $25 par value, and it yields an appealing 6.1%. The dividends paid by BEP.PR.A hold precedence over the common dividend and are cumulative, which means that any missed payments must be made up lest the company goes insolvent.

While the call date of 3/31/25 is coming up in 6 months' time, investors appear to be giving that a low probability event considering the aforementioned 14% discount. Even if BEP.PR.A is called in March of next year at $25 per share, investors could be looking at a yield to call of around 16%. As such, BEP.PR.A represents a viable, high-yielding alternative to the common stock.

Investor Takeaway

Brookfield Renewable Partners offers an attractive buy-the-dip investment opportunity for long-term, income-focused investors with its current 5.5% yield, supported by a robust growth pipeline and well-covered distributions.

With largely contracted revenues and significant inflation protection, BEP is positioned for steady cash flow growth. The company's diverse portfolio across hydropower, solar, wind, and emerging technologies like battery storage and carbon capture, combined with its expanding global reach and partnerships with leading corporations like Microsoft, make it a compelling play on the growing demand for clean energy at the current valuation and yield.

Read The Full Report on iREIT+Hoya

iREIT+HOYA Capital is the premier income-focused investing service on Seeking Alpha. Our focus is on income-producing asset classes that offer the opportunity for sustainable portfolio income, diversification, and inflation hedging. Get started with a Free Two-Week Trial and take a look at our top ideas across our exclusive income-focused portfolios.

With a focus on REITs, ETFs, Preferreds, and 'Dividend Champions' across asset classes, members gain complete access to our research and our suite of trackers and portfolios targeting premium dividend yields up to 10%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}