IvelinRadkov

Intro

We wrote about Eastman Kodak Company (NYSE:KODK) in January of this year when we implied that investor sentiment had become too bearish in the 'Print' & 'AMC' provider. Although a sustained pattern of multi-year lower lows had become the norm in KODK, we pointed out that the stock's valuation was now approaching bargain-basement levels. Evidence of the stock's compelling valuation was the stock's 18%+ GAAP earnings yield and the sizable gap between Eastman Kodak's share price and the underlying book value per share. Given some encouraging announcements we will get into later in the article, shares of KODK have rallied over 28% since our most recent commentary on the 4th of January this year. This a sizable return given the S&P500 has returned just over 11% over the same timeframe.

Although we still see encouraging trends concerning Kodak's valuation as mentioned and certain profitability metrics to boot, due to shares not being able to maintain gains throughout this month (March 2024), we are maintaining our Hold rating in the photographic film company.

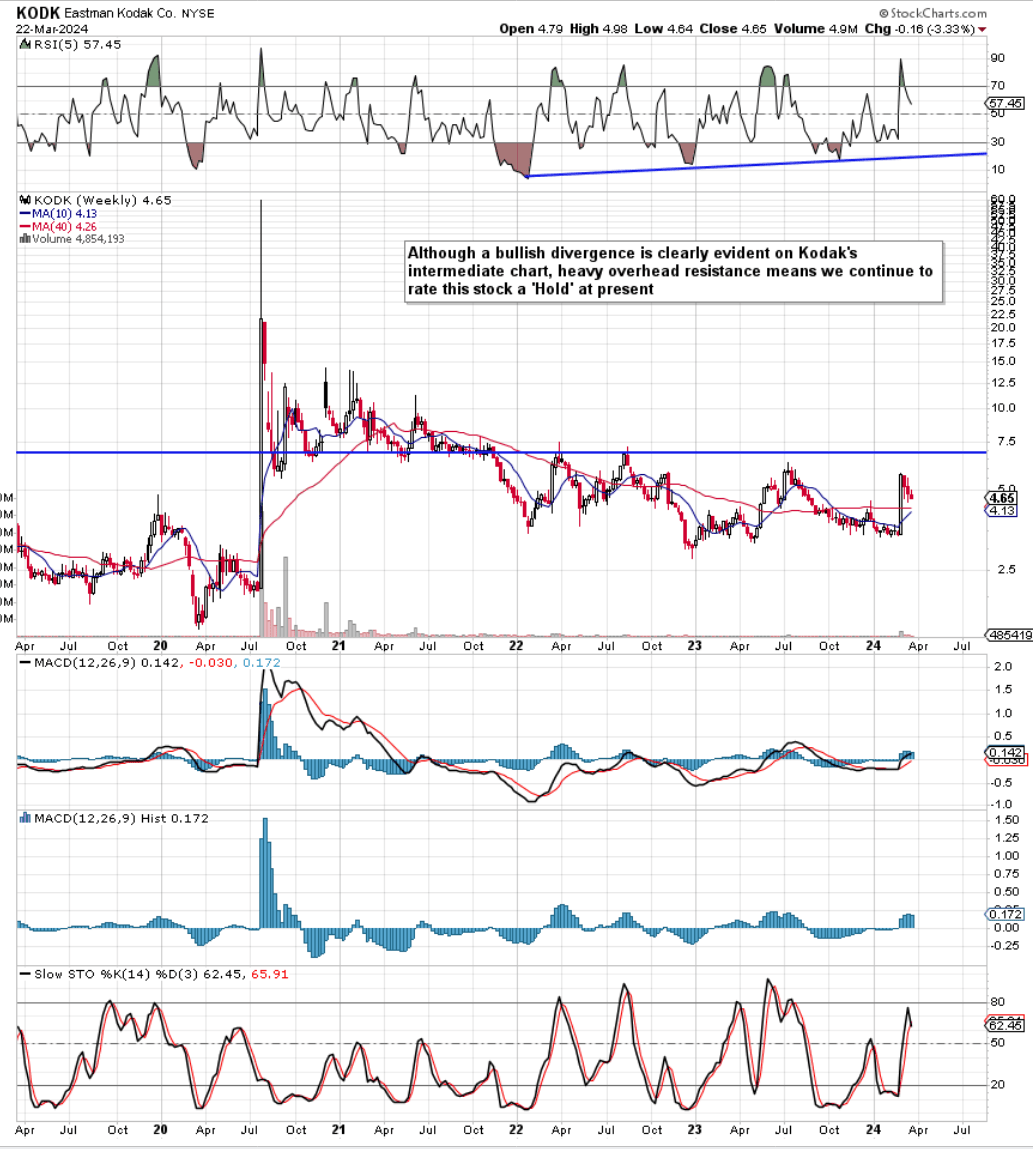

For us to upgrade the rating of stock, we must be able to see encouraging trends in the company's valuation, key profitability metrics and technicals. As we see below, although the stock spiked on heavy volume in late February due to the possibility of unlocking the pension fund surplus, the month of March as mentioned has been poor trading with shares giving back a meaningful chunk of those gains. This means (despite the rally) the stock's 10-week moving average continues to trade beneath the 40-week average. Therefore, considering the significant overhead technical resistance, we would need to see a bullish intermediate crossover before entertaining any thoughts of getting long KODK in a meaningful way.

KODK Intermediate 5-Year Technicals (stockcharts.com)

Potential Unlocking Of $1.2 Billion Pension Surplus

Notwithstanding the encouraging Q4 earnings report announced on the 14th of March this year, the grand majority of gains in KODK in 2023 has come from the Bloomberg report which outlined how KODK management was entertaining the idea of dipping into its successful pension fund which currently reports a $1.2 billion surplus.

Suffice it to say, that when one runs through the numbers here (taking into account the validity of Kodak's pension surplus), one could make the argument that shares should be trading significantly higher. We state this because if the entire $1.2 billion surplus came into the coffers of the company, Kodak's net-debt position would change from a present -$200 million approximately to +$1 billion after the current $450+ million debt load is retired. The balance sheet would essentially be transformed in that shares would be trading for only a mere 37% of its adjusted cash position with the company's adjusted book multiple dropping to a mere 0.16.

Therefore, what bearish investors need to take into account here is that despite Kodak's ongoing revenue growth woes, one would think that adding this amount of capital to the balance sheet simply has to reprice the stock upward over time. Remember, Kodak remains healthily profitable and is generating cash flow with gross margin continuing to go from strength to strength as we see in the company's latest Q4 numbers.

Gross Profit Tailwind Protecting Bottom-Line Profitability

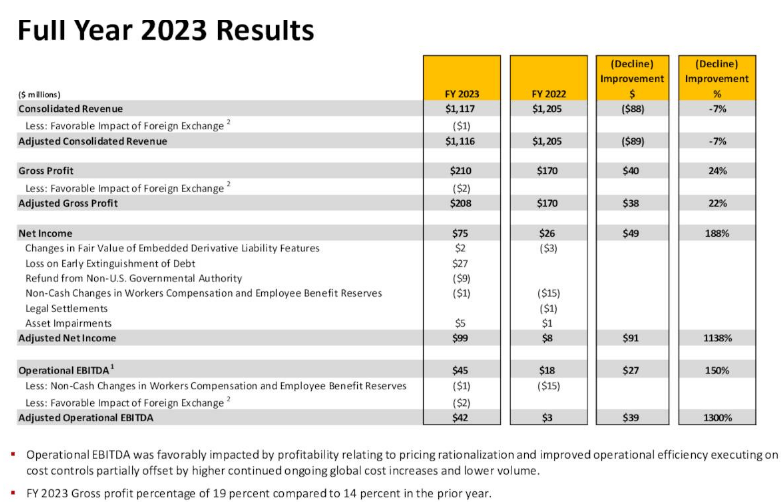

Although growth-orientated investors will focus on the sizable $35 million fall in revenue in the fourth quarter of fiscal 2023, gross margin increased from 14% in Q4 of 2022 to 17% in Kodak's most recent quarter. This means gross profit for the full year improved by $40 million with full-year gross margin increasing to 19% from 14% in full-year fiscal 2022. Management pointed to more efficient operations where the driving of smart revenue and the sustained reduction of cost of sales remain principal reasons for the upward trend in the company's gross margin.

The key now for Kodak is to find a way to stabilize top-line negative growth. Management in this respect remains committed to continued investing in its Print Solutions, Film & AMC (Advanced Materials & Chemicals) so that increasing value can continue to be given to customers on the front end of the business. Furthermore, management has made it clear that it wants to be the 'last man standing' in the film manufacturing segment due to growing demand citing the need for an increase in capacity. The company's key gross margin metric remains key in that Kodak is now boasting a trailing net profit margin of almost 7%. Suffice it to say, a business with growing margins is better shielded from rising costs all things remaining equal.

KODK Full Year 2023 Results (Seeking Alpha)

Risks

Despite the positives outlined above, Kodak's current market cap of approximately $365 million deems the company a small-cap play. This means that below average trading volume has the potential to move the stock aggressively (in either direction) due to the lack of significant volume. Furthermore, the lack of forward-looking guidance, negative sales growth, and the significant overhead technical resistance are reasons enough to maintain our Hold rating at this present moment in time. Remember, the lack of a dividend as well as the absence of a compelling share-buyback program means investors must solely rely on share-price capital gains to report a return on investment over time.

Furthermore, although full-year revenues of the AMC segment increased by $21 million to hit $255 million, revenues of the Print segment fell by $110 million in fiscal 2023 to come in at $828 million. Management will point to the better EBITDA numbers coming from the AMC segment but many times negative revenue growth is frowned upon by investors, which means some stabilization will be needed in this area before long.

Conclusion

To sum up, we are reiterating our Hold rating in Eastman Kodak despite news on the company's expansive pension surplus, growing gross margins and growing GAAP profits in fiscal 2023. Negative sales growth remains a problem and as mentioned earlier, shares have some significant overhead technical resistance to overcome before a return to a bull market can be confirmed in this play. We look forward to continued coverage.