Teerapong Kunkaeo/iStock via Getty Images

Intro

In nearly 20 years of investing in small and micro-cap companies, we believe we've encountered one of the most significant disconnects between market capitalization and asset value we've ever seen. You might assume this pertains to a company in a mature or declining market, but it's quite the opposite.

One of Comstock Inc.'s (NYSE:LODE) biggest challenges is its identity as a micro-cap conglomerate tech incubator operating under the guise of a gold mining company. This complex and unconventional business model makes it difficult for investors to fully understand, likely contributing to the gap between its asset value and market cap.

We previously published a paywalled article on Substack highlighting the SBC Capital deal as well as the background of the three subsidiaries that are included in that deal. Rather than revisiting the same points, this article focuses on updating and highlighting the significant changes over the past two months.

Let's begin with the less positive news. While the SBC deal appears to remain on track, the first tranche has not closed as quickly as Corrado, LODE's CEO, initially indicated. Based on our discussions with management, we believe there are minimal concerns about the deal closing. Corrado has consistently maintained that although the ultimate investor may move slowly, they have always kept their word, and he expects them to follow through on this capital commitment.

To facilitate the SBC deal's closing, LODE issued $3.25 million in convertible notes, with a conversion premium of 100% over the previous day's closing price. While the final price could vary, it translates roughly to a conversion price of $0.80 per share. Additionally, there is an option to issue $1.5 million in further notes. Management has indicated that the proceeds will enable the company to complete the necessary steps to finalize the SBC investment.

Now, onto the positive news. Three major developments have occurred in the last two months, aside from the substantial strategic investment in LODE. First, management announced that they will now offer solar panel dismantling and transportation services. This strategic shift is expected to accelerate the utilization of their recycling facilities.

Second, LODE signed an impressive licensing agreement for its fuels subsidiary, covering three refineries in Australia and New Zealand. We believe this will be the first of many such agreements for the Fuels division in the months ahead.

Finally, LODE acquired substantially all the assets of Quantum General Materials, adding further value to its portfolio and indicating a continuation of their technology incubation strategy. Recall prior to this announcement, the company owned about a third of GenMat.

Solar Panel Recycling - Comstock Metals

Comstock's most immediate revenue opportunity lies in its solar panel recycling business. LODE pivoted to this sector from battery recycling in 2023 after successfully demonstrating its ability to produce black mass in 2022. However, later in 2022, a collapse in primary metal prices, combined with a shortage of feedstock and intense competition, led the company to sell its battery recycling facility and shift its focus to solar panel recycling.

While LODE is not the first company to recognize the potential in solar panel recycling, it has targeted a critical bottleneck in the industry: the labor-intensive process of de-laminating the glass from solar panels. LODE has developed a proprietary method that can de-laminate panels in about seven seconds - a speed unmatched by any competitor at scale. This innovation positions LODE to be more profitable than its peers, even at lower processing volumes.

LODE's strategic positioning in the solar panel recycling business is compelling. The company recently demonstrated its ability to recycle 100% of commercial solar panels, a claim that no other recycler, to our knowledge, can make. Furthermore, management has emphasized that the cost of recycling panels with LODE is competitive with landfill disposal. Their commercial demonstration facility has proven that they can recycle panels at scale and recycle 100% of the materials.

Additionally, LODE has signed a lease for a much larger 100,000-ton facility adjacent to its current site and has obtained a permit to store hazardous solar waste for processing. With these developments complete, the company is now poised to scale this unique business. The only remaining obstacle was securing the capital to fund the first 100,000-ton facility - an investment of around $10 million. This challenge was recently addressed through a funding agreement with SBC Commerce.

Management has stated that they aim to build three of these 100,000-ton facilities by 2027. Initially, the plan was to complete three facilities by 2028, but the new investment should accelerate the timeline, allowing facilities 2 and 3 to come online concurrently rather than sequentially as originally planned.

LODE receives approximately $500 per ton as a tipping fee for recycling solar panels. This means the company gets paid $500 per ton as soon as the panels are delivered. Additionally, LODE recycles 100% of the material, which costs them about $100-150 per ton. With the recovered silver, glass, and aluminum worth around $150+ per ton, LODE is achieving an 80%+ margin on its recycling business.

On August 20th, management announced the first sale of recycled materials specifically, aluminum, which makes up 10-15% of a panel's weight on average. This announcement seemed to generate interest from potential customers, and within a few days, LODE secured contracts with three new solar panel customers.

This surge in customer wins seems partially due to LODE's ability to recycle 100% of the panels coupled with the decision to offer decommissioning and transportation services. These three initial decommissioning contracts are worth nearly $500,000 in revenue for the solar business. While the decommissioning and transportation services will have a lower margin of 20-30%, they effectively secure a consistent supply of solar panels for the recycling operation. Management has confirmed that adding decommissioning and transportation services has significantly accelerated their solar panel recycling opportunities. The acquisition of solar panel supply is crucial for the 100,000-ton commercial-scale facility.

Each facility is expected to generate $50-60 million in revenue and $40-50 million in profit, depending on the amount of material recovered and recycled. With roughly 200 million shares outstanding, running the first facility at capacity could generate earnings of $0.20-0.25 per share. We anticipate that the facility will reach capacity by late 2026 or early 2027.

Management's plan is to have at least three such facilities operating by the end of 2027. Based on the rapidly expanding supply of end-of-life solar panels expected between now and 2030, we estimate that the three facilities will reach capacity by 2028-2029. If they do, the facilities alone could contribute $0.60-0.75 in earnings per share.

While this outlook is impressive, it's important to remember that if the SBC deal closes as expected, LODE will only own 60% of these earnings. Adjusting for ownership, this translates to $0.36-0.42 in earnings per share for LODE shareholders. Given that this is still three or more years away, we apply a conservative P/E multiple of 5x to value this earnings stream, implying that the solar business alone could be worth approximately $1.80-2.10 per share.

Renewable Fuels

As promising as Comstock's solar panel recycling business is, the renewable fuel opportunity presents an even larger and more exciting prospect for the company in the long run. While the potential is significant, we initially believed it was still a few years away from generating substantial revenue and earnings. However, recent developments have accelerated this timeline and changed our view.

In just the last few months, there have been several important updates for the fuels business. Historically, LODE's technology could convert one ton of woody biomass into 100 gallons of fuel equivalent, with plans to eventually increase this yield to 150 gallons. However, just two days after our article, the company announced that it had confirmed the ability to produce 125 gallons of fuel equivalent per ton of biomass, a 25% improvement.

In addition, management announced a new licensing and cooperative research and development agreement with the Department of Energy's National Renewable Energy Laboratory (NREL) to further develop Sustainable Aviation Fuel (SAF) and Renewable Diesel (RD). We believe this partnership is helping LODE progress toward its goal of producing 150 gallons of fuel equivalent per ton of biomass, ultimately achieving parity with carbon-based fuel sources.

While these technical achievements are impressive, they are not the most important news. LODE secured funding to build its first commercial-scale demonstration facility through the SBC Commerce agreement, but that may no longer be the first refinery to come online.

On September 18th, LODE announced the execution of a binding agreement with SACL to develop three renewable fuel refineries in New Zealand and Australia. In exchange for LODE's renewable fuel technology, SACL has agreed to pay LODE 6% of all construction fees, plus a 6% royalty on all future sales and 20% equity in each of the three refineries. We'll discuss the financial impact of this deal shortly, but it's important to note that management views this agreement as somewhat of an afterthought.

In numerous discussions with Corrado, he never mentioned plans in New Zealand or Australia, instead focusing on North America and Europe. After seeing the deal, we spoke with Corrado and characterized it as an "amazing deal for an afterthought." He didn't disagree. While the agreement came together quickly, the company remains primarily focused on North America and Europe.

Just a week ago, a video was posted to LODE's YouTube channel in which Corrado discussed the Australian fuel deal. In the video, he disrupted our expectations once again. While we initially thought it would take 5-10 years to build these refineries, Corrado mentioned that LODE will receive "6% of the capital costs of the projects, total in engineering fees. With capital costs potentially exceeding $2.5 billion over the next 3-4 years, this translates to $120-130 million in engineering fees."

Reading between the lines, this suggests that all three refineries could be built within 4-5 years, with revenue from engineering fees starting within the next 12 months. However, that's just the engineering fees. According to BioBased Diesel Daily, the three SACL refineries are expected to generate over $1.5 billion annually in sales at current market prices.

While fuel sales likely won't materialize for a few years, the ongoing royalty from these three refineries will be worth approximately $90 million per year in recurring revenue. Additionally, Comstock Fuels will own 20% equity in each refinery. Based on the projected $2.5 billion construction cost, this equity stake is valued at $500 million.

In summary, this one fuel deal is worth around $125 million, or $0.63 per share, in one-time engineering fees, $90 million annually in royalties, and $500 million in refinery equity. Not factoring in the recurring nature of the royalties, this implies a total value of approximately $4 per share. The $90 million in annual royalties will be highly profitable, contributing around $0.45 in recurring earnings by 2028.

However, assuming the SBC deal closes, LODE shareholders will only own 60% of these earnings. Using the same conservative 5x earnings multiple as before, 60% of $0.45 in earnings implies that this revenue stream is worth approximately $1.35 per share, plus $0.40 in engineering fees and $1.50 in equity across the three refineries. Once SBC's share is accounted for, this deal is worth at least $3 per share to LODE.

While this deal is impressive on its own, it represents just one opportunity in the renewable fuels space. As Corrado mentioned in the video, "We have had numerous other parties come forward wanting to do a similar deal." We expect to see a similar agreement in Europe in the coming months and anticipate an even larger deal in North America. Combined, these deals could represent two to three times the economic value of the Australian fuel deal, significantly enhancing the value of this subsidiary.

One final thought: we've confirmed that the SBC Commerce deal was negotiated without knowledge of the impending Australian license. This suggests that closing this agreement should make SBC even more interested in finalizing the strategic investment, boosting our confidence that the deal will close. However, even if the SBC deal were not to close, the company now has funding via a commercial partner, and there are likely additional sources of capital interested in getting involved.

Generative Materials Acquisition

At first glance, this acquisition might seem unusual for a gold mining company, but it aligns well with Comstock's strategy of acquiring companies early in their development cycle, guiding them to commercial readiness, and integrating them into Comstock's business units.

In this case, there's an immediate opportunity to incorporate GenMat's intellectual property into Comstock's nascent fuels business, though there are likely additional synergies. From our past conversations with Corrado, he's emphasized that the company is laser-focused on maximizing the theoretical conversion yields of woody biomass, and achieving that will require the aid of artificial intelligence (AI).

In the press release discussing the acquisition, Corrado stated that our "interest in GenMat was and remains grounded in the critical need and use of artificial intelligence for materials science and mineral discovery, for breakthrough energy applications and other mature industries with large addressable markets. Artificial intelligence is even more critical today, as rapidly evolving AI platforms have begun to accelerate the pace of global innovation and redefine industries and competitive requirements. Frankly, anyone who is not integrating AI into their core competencies and capacities will likely either be disrupted or completely replaced."

Comstock's Chief Technology Officer, Kevin Kreisler, further added that by "focusing and building on GenMat's team and competencies in materials science, computational chemistry, and computational machine learning, while incorporating the bleeding edge of emerging artificial intelligence technologies [we] will reinforce our competitive advantages in our metals, mining, and fuels businesses."

While this acquisition may not be a game-changer in the short term, we believe that GenMat has the potential to deliver value to LODE and its shareholders over time. Although the immediate value of this deal might seem limited, it highlights Comstock's ongoing commitment to its incubation strategy.

Given the early stage of the business, we were pleased to see that Comstock did not commit significant capital to this opportunity. The deal involves a payment of approximately $1 million in three installments plus 3% of any future sale or IPO proceeds exceeding $100 million.

Valuation

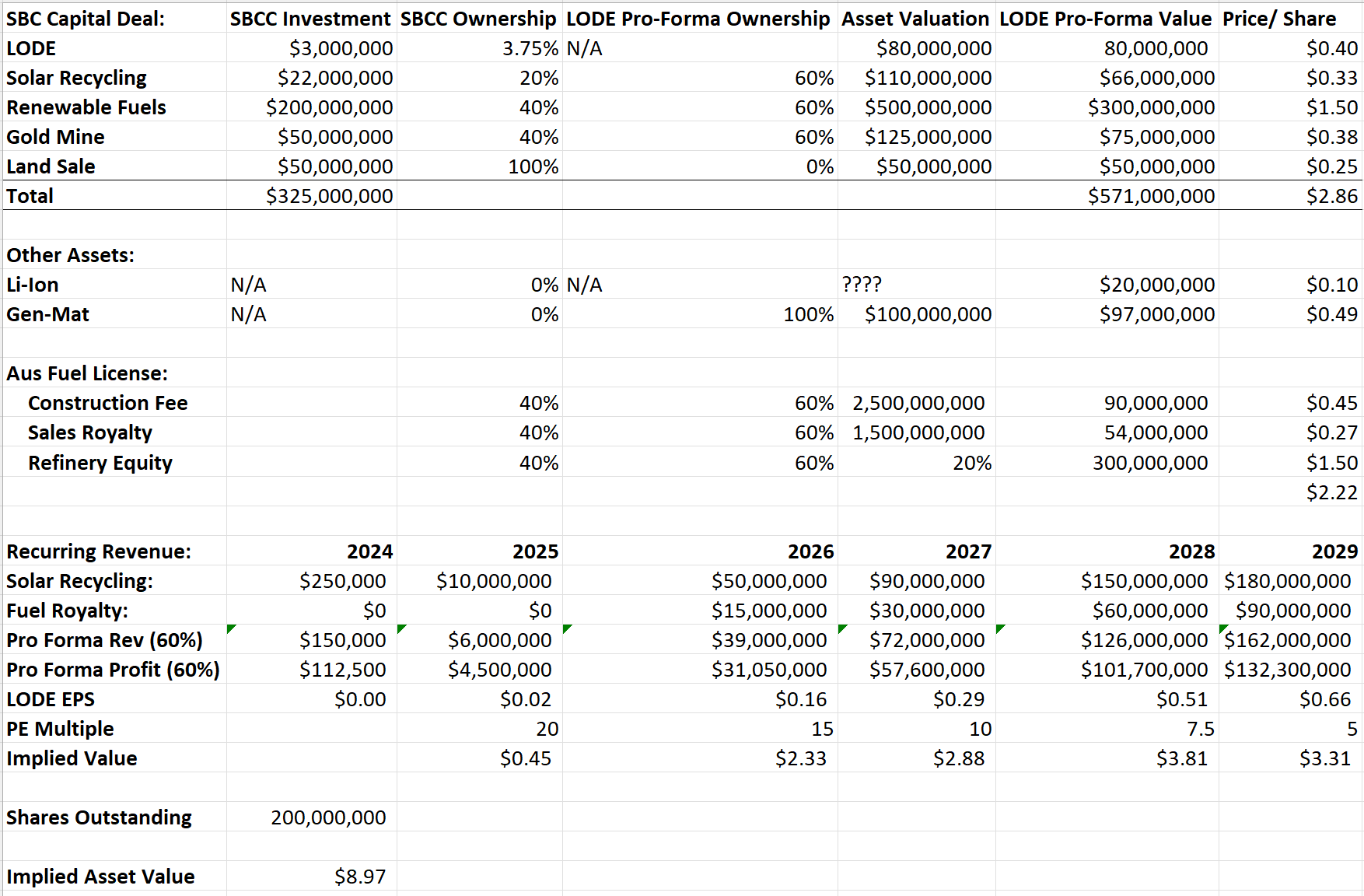

To highlight the significant disconnect between Comstock's current market capitalization and the implied asset values, it's useful to break down the valuation of each business subsidiary, including the land sale, the SBC Commerce investment, GenMat, and the Australian fuel license. The table below serves as the basis for a sum-of-the-parts (SOTP) valuation of LODE.

Notably, within the next 60 days, LODE is expected to finalize its SBC Commerce deal, crystallizing asset values exceeding half a billion dollars. This is particularly striking given that the company's current market capitalization is around $90 million.

LODE - SOTP (Company Disclosures and Author's calculations)

In addition to the implied asset value, LODE has two high-margin, recurring revenue streams that will begin generating earnings and cash flow in 2025, with a strong growth trajectory through 2030 and beyond. Despite the recent rise in share prices, we believe there is still a significant disconnect between the company's asset values and its market capitalization.

One challenge LODE faces is the complexity of its business and the lack of readily available information for investors. In the scenario outlined above, we've laid out a conservative valuation based on current company data and management guidance.

We begin by valuing the SBC Commerce deal, which forms the top section of our analysis. Specifically, we take the equity payments SBC is making for each of the three subsidiaries, adjust for LODE's pro forma ownership, and include the $50 million from the land sale to calculate the implied value of LODE's remaining stake in the subsidiaries. Even without factoring in the Australian fuel deal, the SBC deal alone implies a valuation of nearly $3 per share for LODE, which is significantly higher than the current share price.

But there's more. LODE has also recently acquired the remaining stake in GenMat. According to the 8-K filing, if LODE sells or IPOs GenMat for $100 million, the founder will receive 3% of the deal value. While it may take a few years to reach a $100 million valuation, we expect LODE to eventually monetize the business. LODE also holds an equity stake in Li-Ion, which it has been monetizing, and is worth roughly $0.10 per share.

Next is the major Australian fuels deal, which is crucial for several reasons. Beyond the financial impact, it validates Comstock's technology and provides a strong cash flow source via construction fees over the next few years. The deal includes a combination of one-time engineering fees, permanent equity in the three refineries, and a 6% royalty on future sales. After adjusting for SBC's 40% ownership of the fuels subsidiary, we estimate the one-time pieces of this fuel deal will contribute approximately $2.25/share of equity value over the next 3-4 years.

Finally, we estimate the value of the recurring revenue streams from the fuels and solar panel recycling businesses. This section of the analysis involves numerous assumptions, but the goal is to illustrate how valuable these segments could become over time. Based on the three Australian refineries and the three solar panel recycling facilities announced so far, we expect LODE's pro forma sales (accounting for its ownership stakes in the subsidiaries) to peak around 2029.

For this analysis, we assume LODE maintains a 75% margin in solar recycling and a 95% margin from fuel royalties. Using these assumptions, we calculate a rough earnings estimate through 2029, then apply a conservative 5x earnings multiple to LODE's pro forma 2029 earnings, which implies more than $3 per share in value from these two business lines.

When we add up all these components, we estimate an asset value of nearly $9 per share. While we don't suggest the stock should immediately trade at $9, this analysis provides a reasonable roadmap for how shares could reach that value over the next 3 to 5 years. In the short term, however, we believe a $2.50 target price based on closing the SBC Commerce deal by year-end is a reasonable starting point.

Risks

- SBC Commerce deal falls through.

- Technology Risk.

- Unexpected regulatory changes.

- Inability to penetrate new markets.

- Inability to procure necessary regulatory approval.

- Competition pressures pricing.

- Inability to add new partners.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.