Anja W.

Now that I am enjoying the retirement phase of my investing life, I have discovered the joy of collecting monthly passive income in my Income Compounder portfolio. One type of security that I hold in my current IC portfolio includes a corporate bond fund. I believe it will outperform its peers on a total return basis due to the reduction of interest rates starting with the 50-bps cut announced by the Fed in September.

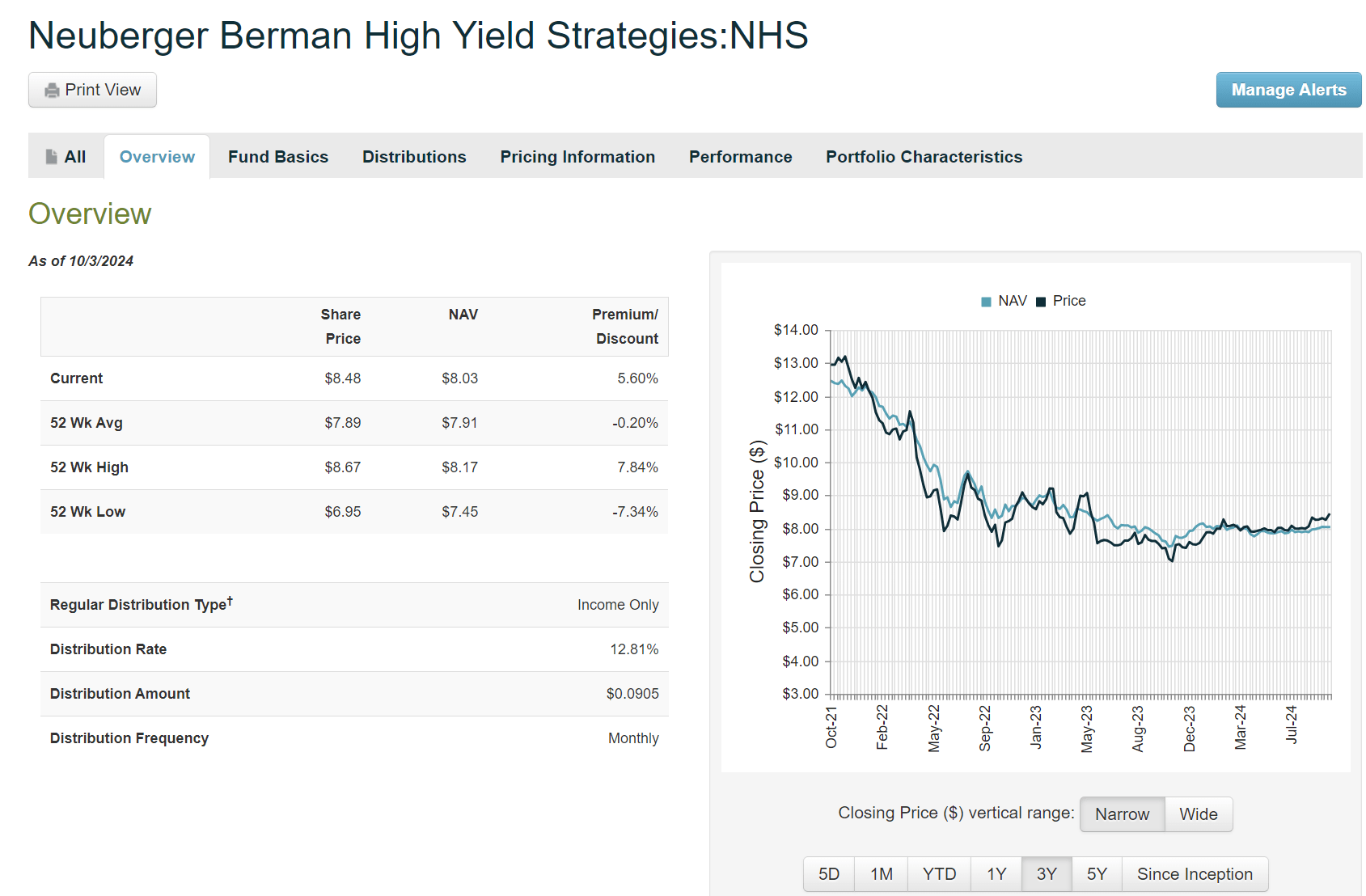

That closed-end fund ("CEF") is Neuberger Berman High Yield Strategies (NYSE:NHS) and it currently yields about 12.8% annually based on the monthly distribution of $0.0905 per share. I like NHS at $8.48 (as of 10/3/24) for its high-yield income, but I rate the fund a Hold because it now trades at a relatively high premium to NAV.

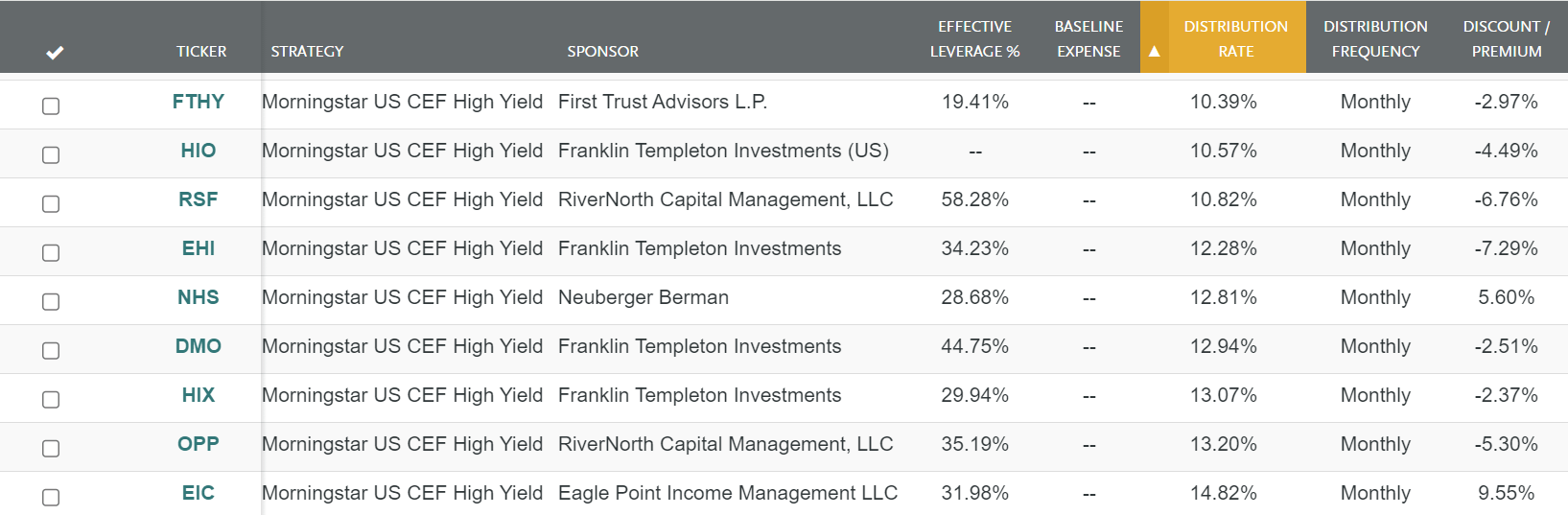

The screenshot below is from the CEFConnect fund screener showing the top 9 (sorted by distribution rate) High Yield CEFs offering monthly distributions with yields over 10% currently. Only DMO, HIX, OPP, and EIC offer higher yields. Each of those CEFs offer different asset classes to achieve the "high yield" designation, with HIX being the closest to a peer fund to NHS.

CEFConnect

I believe that the NHS with its holdings in corporate debt securities (e.g., bonds) will benefit from lower interest rates as bond prices tend to rise inversely to rates as explained in this SEC guide to corporate bonds.

The price of a bond moves in the opposite direction than market interest rates-like opposing ends of a seesaw. When interest rates go up, the price of the bond goes down. And when interest rates go down, the bond's price goes up. As shown above, a bond's yield also moves inversely with the bond's price. For example, let's say a bond offers 3% interest, and a year later market interest rates fall to 2%. the bond will still pay 3% interest, making it more valuable than newly issued bonds paying just 2% interest.

Comparing Top High Yield CEFs

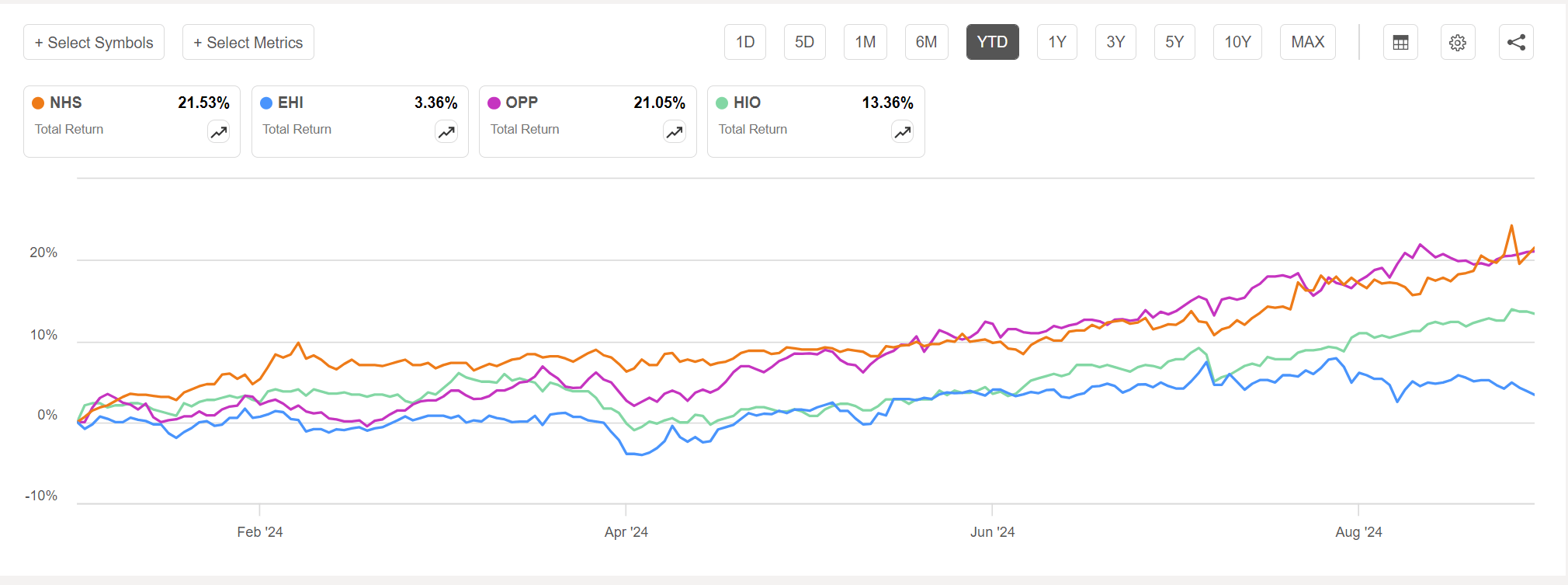

In a head-to-head total return comparison on a YTD basis, NHS is the clear winner compared to EHI or HIO (which also hold mostly corporate bonds and debt securities), while essentially running neck and neck with OPP. I did not include EIC or DMO in this comparison because both of those hold different asset classes, however, I do like and own shares of both of those funds as well.

Seeking Alpha

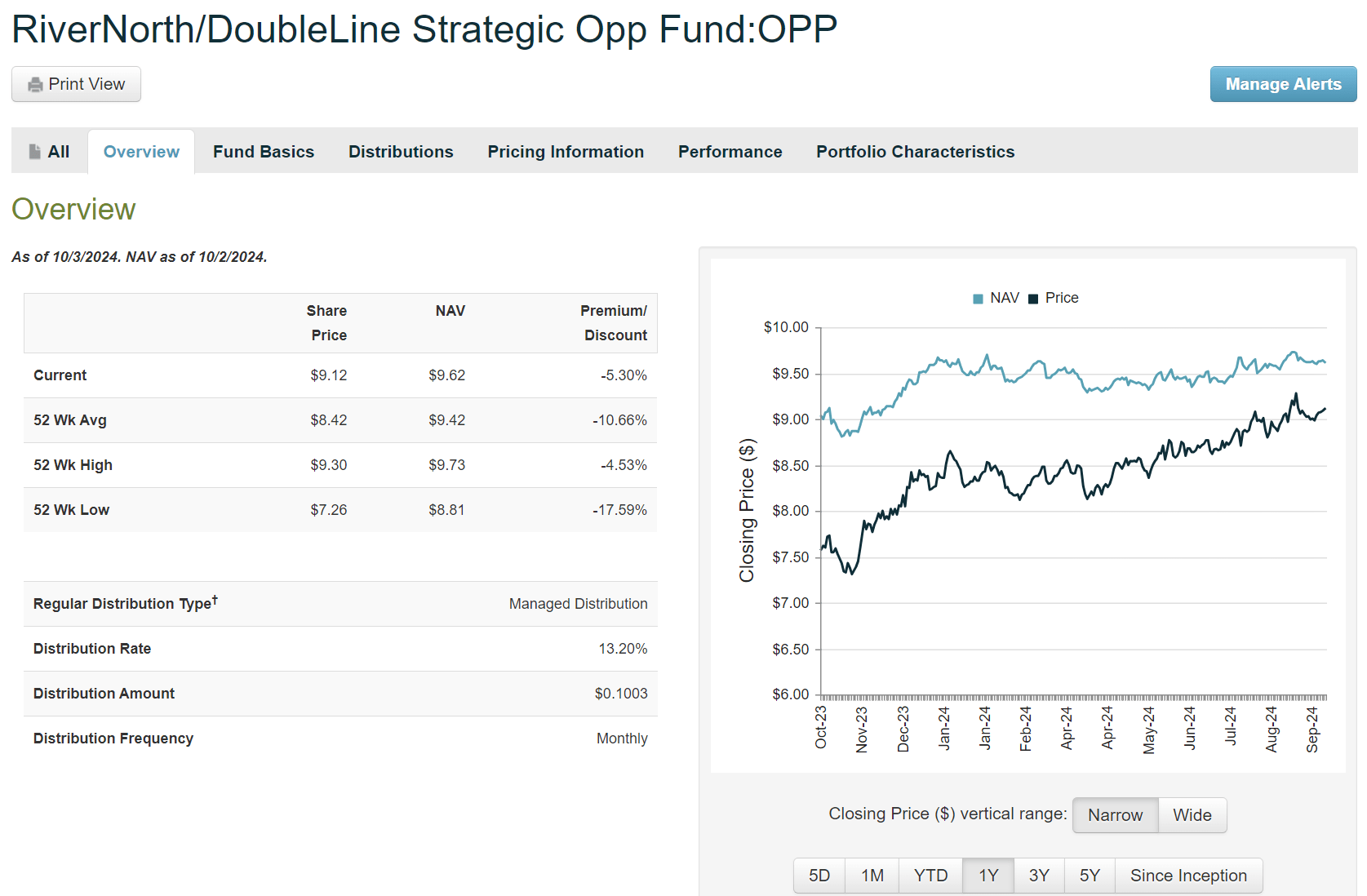

I also own RiverNorth/DoubleLine Strategic Opportunity Fund (OPP) which does invest in some corporate bonds (about 17% according to CEFConnect) and also government bonds and other fixed income securities. I like OPP and have previously written about its sibling fund, RIV. Both funds offer a high yield managed distribution that is set every January and remains level throughout the year.

OPP currently yields about 13.2% and trades discounted to NAV of -5.3%. Like NHS, I believe that OPP will also see some capital appreciation from rising bond prices on its holdings due to lower interest rates. OPP has been closing the discount over the past year and will likely continue to increase in price. It will possibly even be trading at a premium in 2025 when it announces the new distribution in January, which I expect will be an increase over this year.

CEFConnect

What is the Outlook for Fixed Income in H2 2024?

In a recent insight from Neuberger Berman regarding the Q3 2024 outlook for fixed income investments, expectations are for slowing growth and moderating inflation.

So far in 2024, the story has largely been one of changing expectations about inflation and interest rates-first bullish, then bearish, then more hopeful again. Developed economies are slowing-more rapidly in Europe than in the U.S.-and inflation has eased, but remains well above target levels. Most central banks remain cautious, seeking to avoid a bounce-back in inflation, but in our view risking downside policy mistakes. In general, we anticipate some further action on rate cuts this year, continuing into 2025 as pricing pressures come under greater control, justifying movement from cash positions into the short to intermediate "belly" of the yield curve.

In credit, we perceive a still-healthy environment, but with cracks around the edges, as lower-income consumers and many companies tighten their belts in the face of higher rates and prices. Although we believe tight spreads remain justified, they amplify the need to look carefully at risk-reward and capitalize on opportunities where they emerge, for example, in agency mortgage-backed securities (MBS), hybrids or local emerging markets, which are benefiting from moderating inflation, better relative growth and appealing real yields.

Why NHS and Why Now?

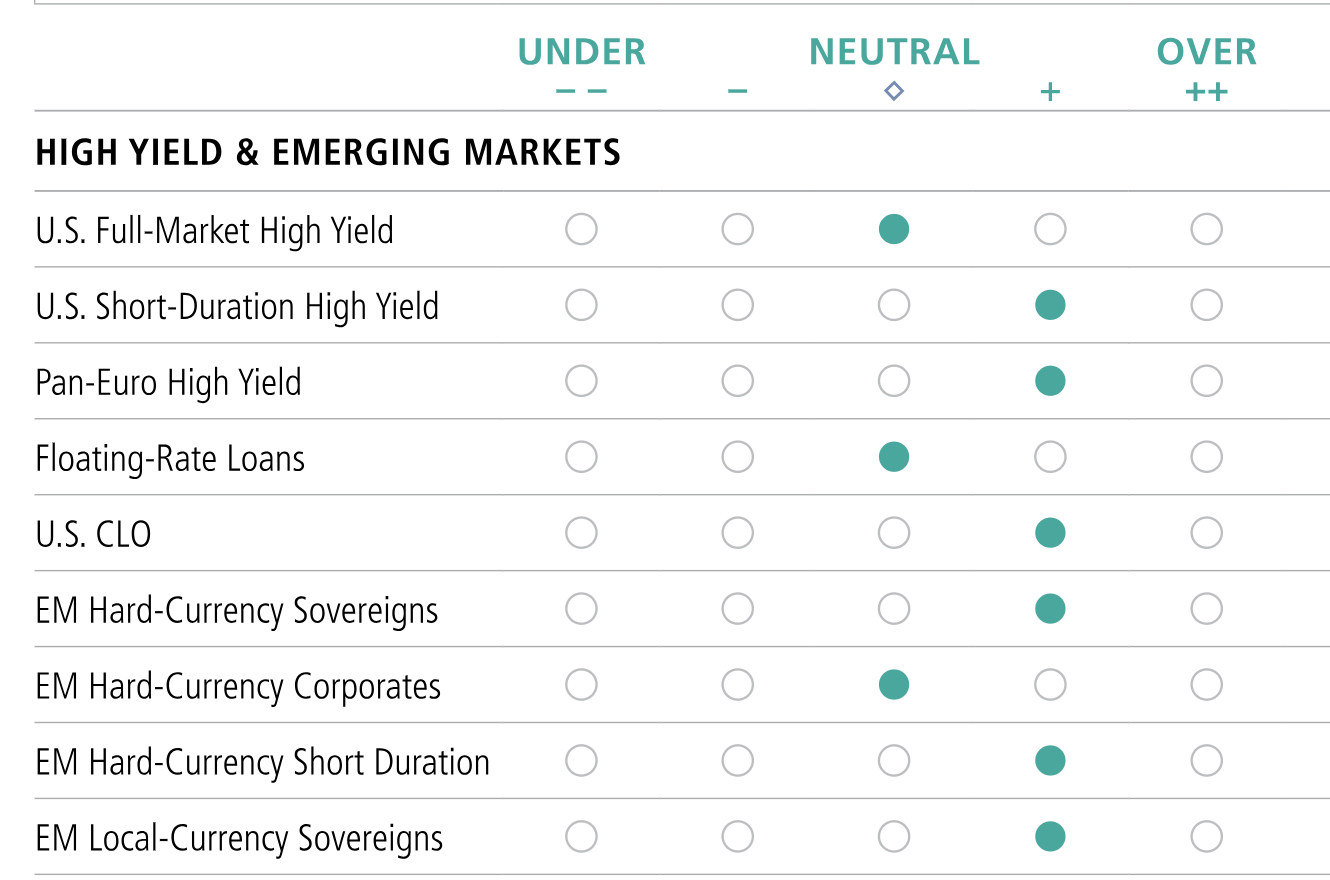

NB suggests a slightly overweight position in US short-duration high-yield assets, which is mostly what they hold in the NHS fund.

Neuberger Berman

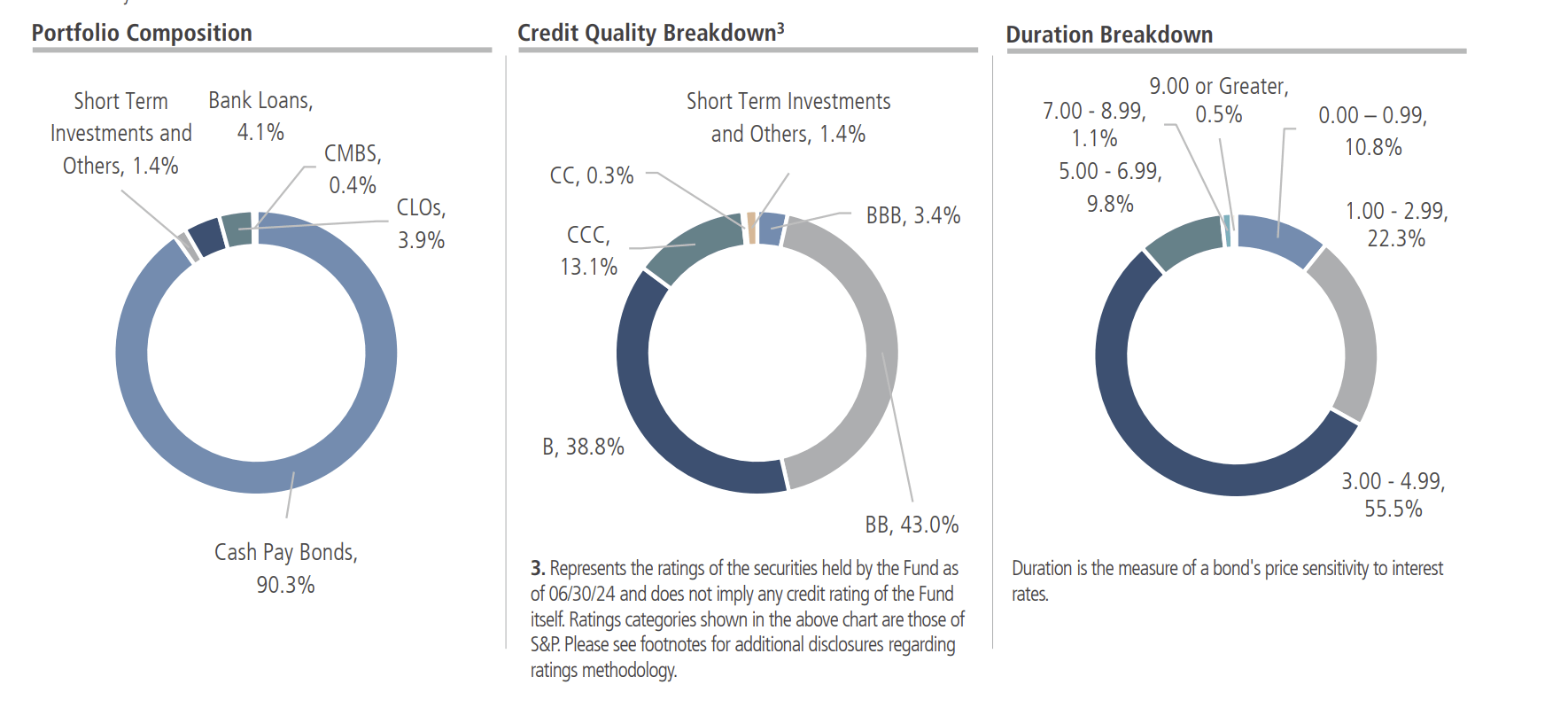

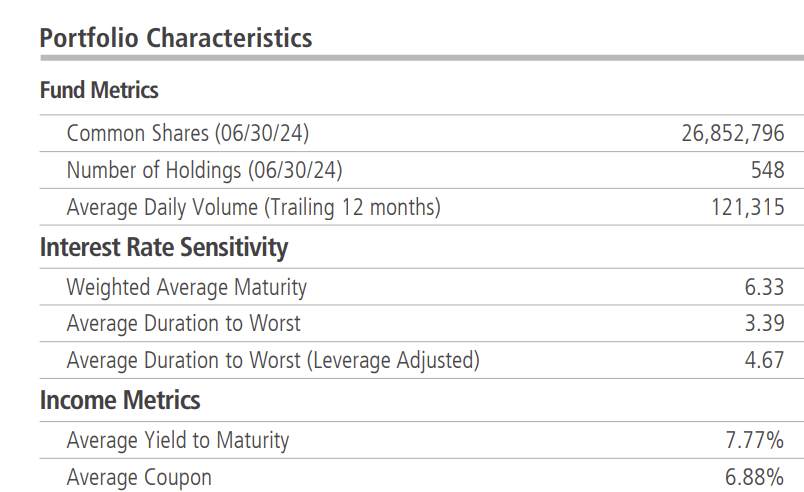

According to the NHS fund fact sheet, portfolio holdings consist of about 90% cash pay corporate bonds, along with about 4% in bank loans and 4% in collateralized loan obligations, or CLOs, with weighted average maturity of 6.33 years as of 6/30/24.

NHS fact sheet

The portfolio characteristics are summarized in the fact sheet and included 548 holdings as of the end of June. Credit quality is non-investment grade, with the majority of bonds rated B and BB.

NHS fact sheet

According to the fund manager commentary, through the first half of 2024 high yields spreads have remained tight, although started to widen in Q2. Default rates remain historically low and, despite slowing growth, are expected to remain lower than average through at least the first half of 2025.

The high yield bond market finished the month of June and the second quarter with solid returns driven by encouraging financial results for most issuers, resilient economic data despite signs of slowing growth and supportive market technicals. Spreads on the ICE BofA U.S. High Yield Constrained Index ("Benchmark Index") widened by just 5 basis points in the month closing at 345 basis points.

While high yield spreads overall were only slightly wider on the month, yields on the high yield market-as measured by the ICE BofA US High Yield Index-remained attractive closing the month at 7.94%. The yield on U.S. 10-Year Treasuries ended June at 4.39%, down 11 basis points over the month but up 18 basis points over the second quarter.

Overall, high yield issuers' aggregate fundamentals of EBITDA growth, free cash flow, interest coverage and leverage remained in somewhat favorable ranges. While most issuers reported in line or better than expected earnings in the recent quarter, some lower rated issuers continued to see some idiosyncratic or industry-specific earnings pressure. Default rates remain low but are up from the all-time lows reached in 2022. Our latest bottom-up base case 2-year cumulative default estimate for U.S. high yield over 2024 and 2025 of 5.5% - 6.5% is around the historical 2-year cumulative average.

NHS Past Performance and Distribution History

When evaluating the recent past performance of a fixed income fund like NHS, it is important to keep in mind the macro conditions that were present during the period in question. For example, looking at a chart of 3-year price performance, it would appear that NHS declined substantially since 2021, although the price has traded close to par (at small discounts or premiums to NAV) during that time. This poor performance was mostly due to fixed income assets getting hammered in 2022 due to rising inflation and increasing interest rates.

CEFConnect

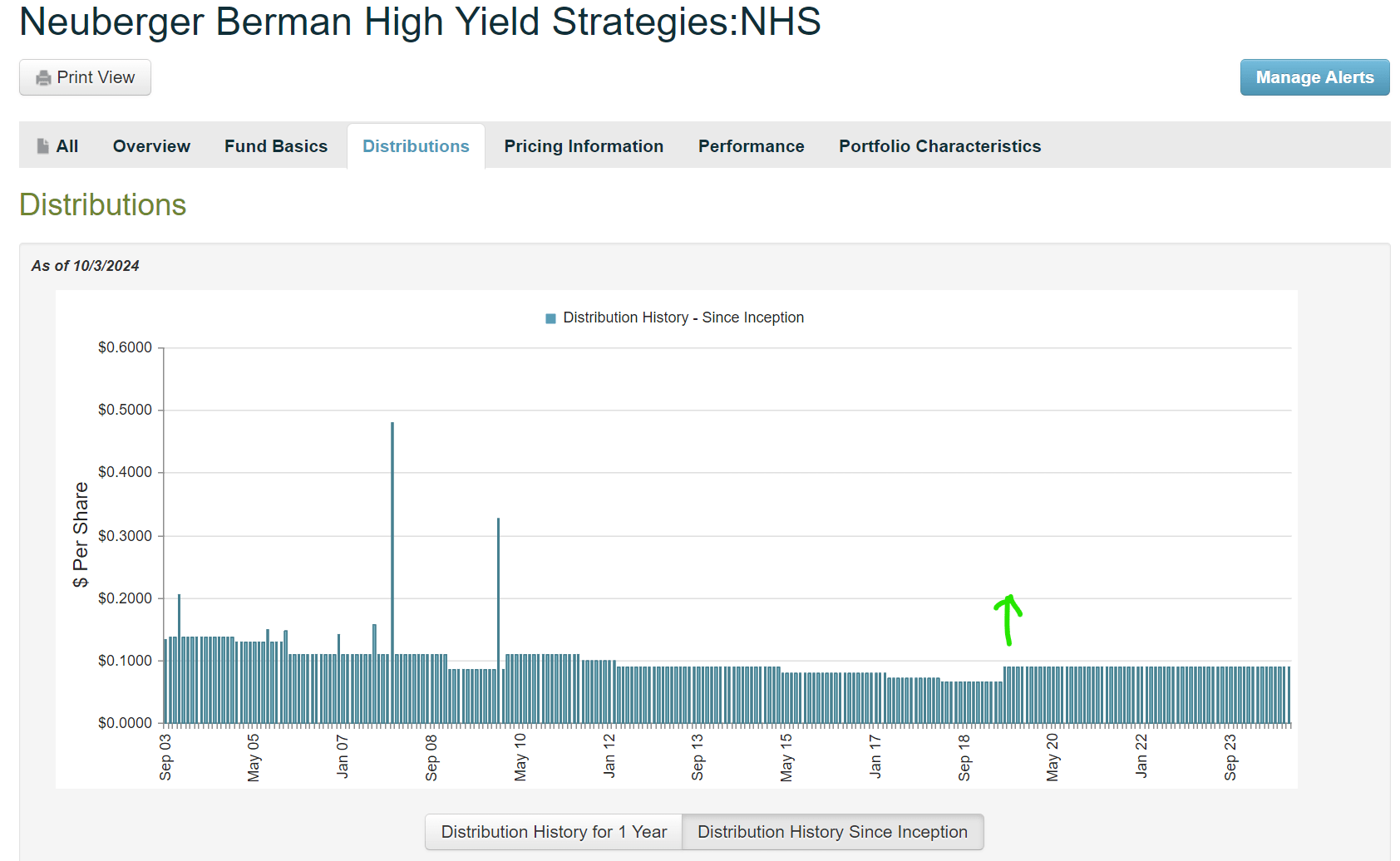

Now that inflation has moderated, and interest rates are starting to come down below 5%, fund performance has begun to improve again, and the fund now trades at a premium of 5.6% while NAV is rising. Meanwhile, the fund continues to pay the same monthly distribution of $0.0905 since May 2019, without a reduction even during the COVID-19 crash of 2020 when other CEFs were forced to reduce the distributions. The distribution history from CEFConnect graphically illustrates the steady distribution over the past 5 years.

CEFConnect

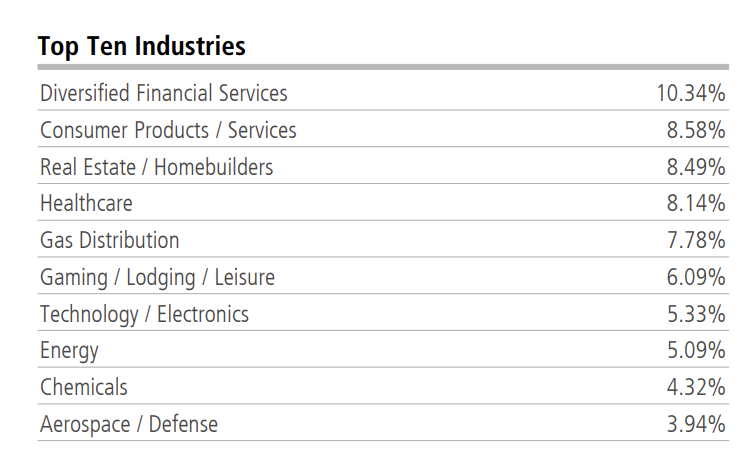

The top 10 industries include moderately defensive and relatively stable businesses that should continue to pay the coupons on their bonds even in a declining economy. This is probably one reason why the fund has been able to maintain the steady distribution even as the price of the fund declined.

NHS fact sheet

By remaining overweight in gas distribution, chemicals, real estate/homebuilders, capital goods, and diversified financial services, the fund should see additional benefits from lower interest rates going forward. In the management commentary from the fund fact sheet, the outlook for US High Yield remains positive for the second half of 2024.

We remain constructive on U.S. high yield. In our view, U.S. high yield valuations and yields are attractive and compensating investors for the relatively benign default outlook. Despite solid but slowing economic growth, higher-than-desired inflation and tight labor markets, we believe most market participants see rate normalization coming at some point later in the year. Our analysts continue to be focused on the specific fundamentals of individual issuers in their coverage, assessing the base and downside cases. Relatively healthy consumer and business balance sheets and positive nominal GDP growth should continue to provide support for most issuers' fundamentals, in our view.

Summary: Consider NHS for High-Yield Income from Corporate Bonds

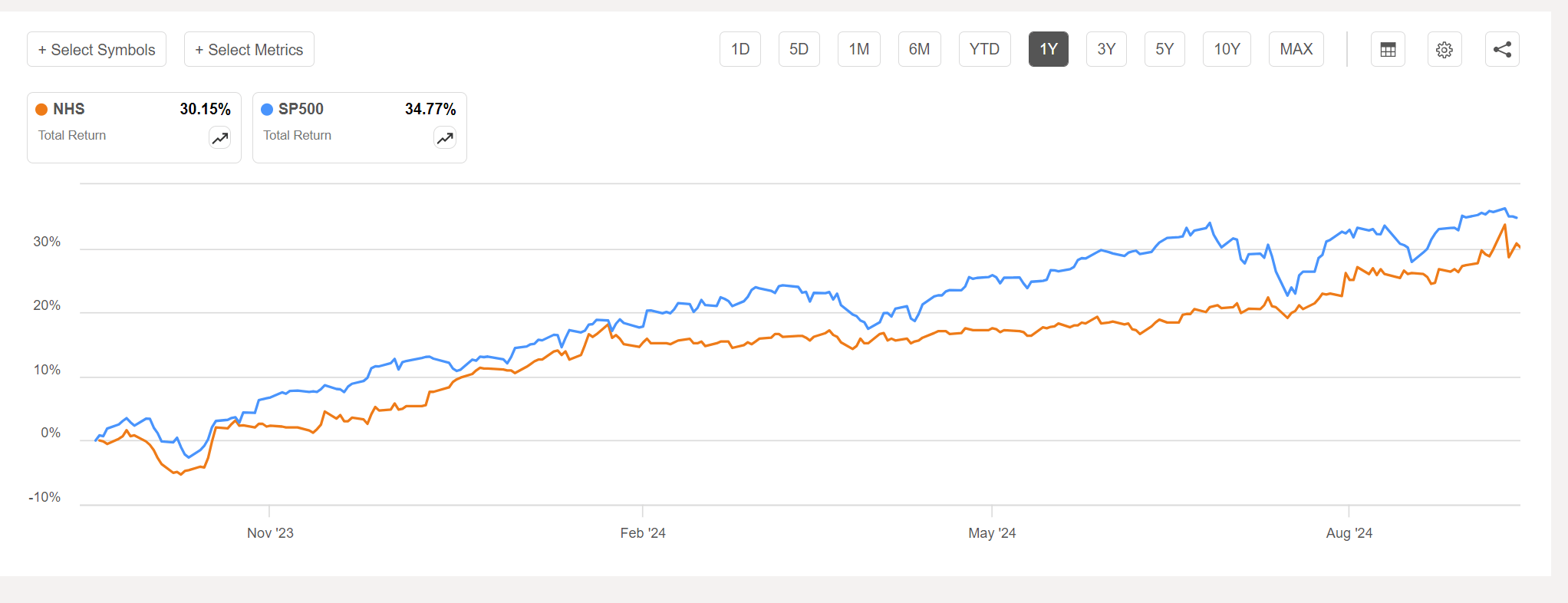

While the past performance of NHS suffered post-Covid from rising inflation and higher interest rates, the fund has recovered and now offers a compelling opportunity to collect a high-yield income from steady monthly distributions. The fund should also see some additional capital appreciation due to lower interest rates as the prices of the underlying bonds rise, which we are already seeing in the rising NAV over the past year.

In fact, the one-year total return for NHS exceeds 30%, approaching the return of the SPY, which is practically unheard of for a high-yield income fund.

Seeking Alpha

However, as I discussed earlier in this review, the premium to NAV has now reached a recent high of 5.6%, which is much higher than the previous 5-year average discount of about -2.5%. While the premium is somewhat justified given the portfolio holdings and the likely benefits of lower interest rates on bond prices, I would expect some price volatility to continue. Therefore, I give the fund a Hold rating given the current high premium.

If NHS is not already on your radar, I suggest giving it a fresh look. Watch for an opportunity to pick up some shares on the next market correction, or whenever the market price retreats closer to NAV as it has in the past.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}