peepo

Introduction

EHang Holdings Limited (NASDAQ:EH) is a Chinese start-up focused on developing and manufacturing passenger-carrying eVTOL aircraft. The company's key product is the EH216, a two-seat pilotless multicopter designed for intracity air mobility. The EH216 is also the only eVTOL model in China that has received all certifications for commercial operation.

I initiated coverage on EHang in April with a positive view of its first-mover advantage in China's eVTOL market. However, the stock has corrected to $12.4 since then before yesterday's spike. The weak performance, in my view, was attributable to profit-taking, lukewarm sequential growth in the first quarter, and investors' lack of confidence in the pace of eVTOL development in China due to weak macro conditions.

2Q Results Fired on All Cylinders

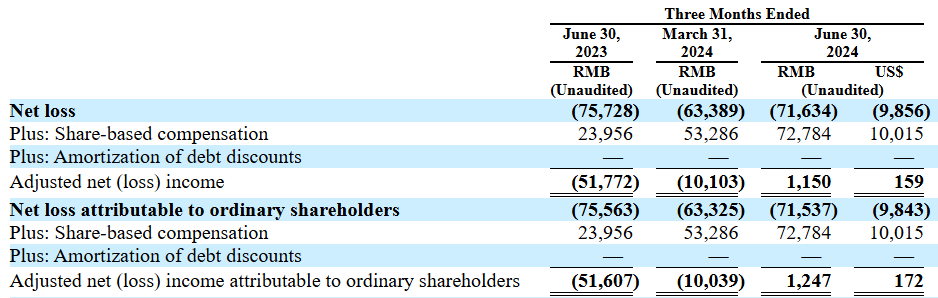

Firstly, EHang delivered strong QoQ revenue growth (see the below chart), exceeding its revenue guidance of CNY90 million and market expectations. Its gross margin remains high above 60%, while adjusted net profit reached breakeven for the first time on a non-GAAP basis.

Chart 1: EHang's 2Q revenue surged quarter on quarter

Source: SEC filing

Chart 2: EHang reached breakeven on a non-GAAP basis

Source: SEC filing

Secondly, its eVTOL deliveries were up 88% QoQ to 49 units. This marked a significant improvement in production efficiency following the receipt of the Production Certificate (PC) for EH216. Prior to obtaining the PC, every eVTOL required an individual inspection by the CAAC before it could be delivered.

Management stated that they have 1100 EH216 orders on hand from domestic customers, which will be delivered in the next 2-3 years. Also, by examining its balance sheet, EHang's contract liability rose 270% to CNY138.5mn from 6 months ago (see chart 3). The contract liability item represents prepayments from its clients for placing orders, which is approximately 30% of the total price. A quick back-of-the-envelope calculation based on the price of CNY2 million per unit suggests that around 230 orders are very firm and are likely to be delivered in the near term.

Chart 3: EHang contract liabilities surged in the past 6 months

Source: SEC filing

Thirdly, by the end of 2Q, EHang has built a substantial cash balance of CNY998mn through equity raising and positive cashflows. Although capex estimates were also revised up to US$15 million and US$20 million for 2024 and 2025, respectively, we believe, with this level of cash, EHang can easily finance its expansion for multiple years, without needing to raise additional capital.

Rising competition is unlikely to impact EHang in the near future.

Several Chinese eVTOL companies have entered the certification process since 2023, but they are unlikely to obtain a Type Certificate in the next 18 months, in reference to EHang's certification process of 31 months.

Further, many eVTOL types that are being certified are different from EH216, except for XPeng's Voyager Series. The EH216 is a 2-seater pilotless multi-copter suitable only for short-distance travel, due to battery limitations. However, the merits of such aircraft include requiring a small landing space, being suitable for hovering which is particularly useful for sightseeing purposes, and high cost-effectiveness.

As mentioned in my EHang initiation, the general aviation (GA) market for sightseeing purposes in China has no regulatory hurdles, as it operates in a confined space for only a short period of time with limited involvement in the government's air traffic control. This is in contrast to GA for transportation purposes, which faces a lengthy approval process for commercial operation. Additionally, there is an underdeveloped air control infrastructure in China for general aviation. Therefore, even with more competitors entering the market after 2026, the direct competition with EHang will remain limited for some time in my view.

Overseas market expansion will be a key catalyst

During the earnings conference, many investors raised questions about its overseas certification process, particularly in the UAE, as investors perceived the overseas market as less competitive and high margin. However, management did not provide a concrete timeline, only mentioning that the UAE's General Civil Aviation Authority, or GCAA, is moving toward a framework agreement with CAAC for mutual recognition of airworthiness certification. If EHang can make concrete progress on its overseas certification, I expect the stock to be re-rated.

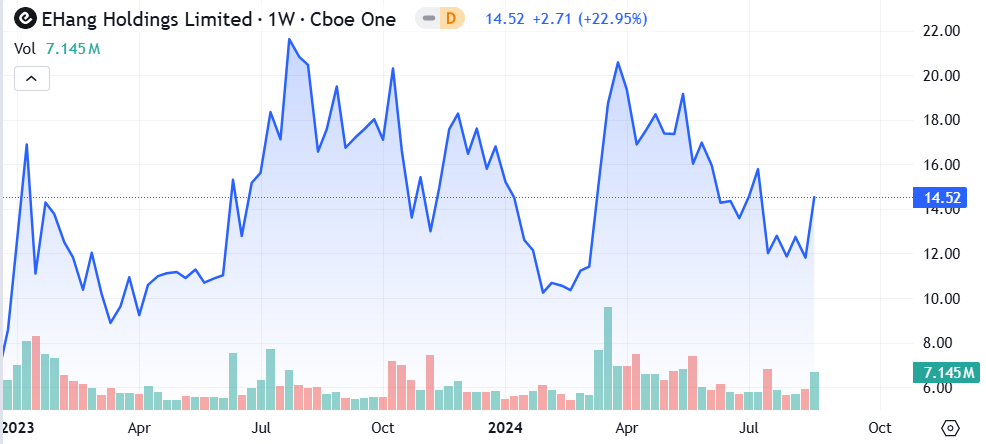

EHang has experienced a roller-coaster ride YTD

From January to March, EHang's share price dropped from $17 to $10 as investors took profits in light of a short selling report on EHang's overseas order backlog. The stock then doubled to $20 in April as investors cheered for more supportive government policy on eVTOL. But profit-taking and lukewarm 1Q results caused another sell-off again to $12.4, before spiking on a 2Q earnings beat.

Chart 4: EHang's share price was in a very wide range-bound

Source: Seeking Alpha

Looking forward, as EHang's business stands on more solid ground with large contract liabilities and a healthy balance sheet, I don't expect the stock to trade back to its previous low of $10 in the past 3 years. However, for the stock to rally back to $20, it requires a strong catalyst such as overseas certification or investors' improved view of China-based assets.

Conclusion

EHang delivered a pleasant surprise in 2Q results. The business has turned more stable and less risky, with surging firm orders and a healthy balance sheet. While the stock may need strong catalysts to offset investors' concerns about the Chinese economy and domestic competition, I believe the stock's downside is limited given the fundamental improvement.