jetcityimage

July 16th was not a good day to be a shareholder of discount retailer Five Below (NASDAQ:FIVE). After the market closed, shares of the company fell by roughly 10%. This came in response not only to a management shake-up, but also to a change in guidance for the firm's upcoming second quarter release. Overall, data from the company shows some deterioration in overall performance. When you add on top of this the worries that the management shake-up is certain to hit investors with, it's no wonder why shares declined.

To be clear, July 16th has not been the only time that the retailer has faced trouble. Year to date, excluding this after hours move, shares are already down 53.1%. This is in spite of the fact that management has been able to achieve attractive top line and bottom line growth over the past few years. Previously, shares of the company were just too pricey to make sense. At least that's what I claimed in my last ‘hold’ rating of the company back in August of 2023. But given the drop seen by the shares, I ultimately upgraded this to a ‘buy’ in an article that was published in early June of this year.

Unfortunately, since then, the stock has continued to face downward pressure. Shares are down 14% from the time that article was published through the close of business on July 16th. By comparison, the S&P 500 is up 5.9%. These recent developments now create a great deal of uncertainty as to what the future holds. And because of that, investors who cannot deal with volatility should definitely consider taking a step back. But for those who don't mind that volatility and who still believe in the firm's long-term picture, this after hours close might be an ideal time to jump in.

Some bad news

After the market closed on July 16th, the management team at Five Below made a rather startling announcement. According to them, effective immediately, the company’s current President and CEO, Joel Anderson, is stepping down. This includes from his position on the retailer’s Board of Directors. In his place has stepped Kenneth Bull to serve as interim President and CEO until the Board of Directors can identify a permanent replacement. For those not familiar, Kenneth Bull has up until this point served as the company’s Chief Operating Officer. In addition to this, Thomas Vellios, Five Below’s Co-Founder, Non-Executive Chairman, and former CEO is assuming the role of Executive Chairman until a new CEO can be identified.

The stock market is very sensitive when it comes to changes at the top level. Usually when a high-ranking executive steps down immediately, it's either because something really bad is brewing or it's due to a health concern. The press release says nothing about health or spending additional time with family. Instead, it merely stated that Mr. Vellios is stepping down ‘to pursue other interests’. There very well could be an explanation for this development that does not mean anything bad for the company. But the typical assumption when this kind of development does occur in this nature is that something nasty is brewing beneath the surface.

Until more news comes out, any sort of guess regarding these changes is speculative in nature. And it's because of how speculative it is that investors should tread carefully. But this was not the only development that management announced. In the same press release, the firm talked a bit about upcoming results covering the second quarter of Five Below’s 2024 fiscal year. They stated that total sales for the 10-week window of time ending July 13th of this year ended up being 9.5% higher than what was seen in the first 10 weeks of the same window of time. While this is an impressive amount of growth, it can only be attributed to a rise in store count. This is because comparable store sales during this window of time have been estimated by management to be down to the tune of 5%. And for the full second quarter of this year, management expects this to worsen to a decline of between 6% and 7% year over year.

This is rather troublesome. As I pointed out in my prior article on Five Below, the firm has had comparable store sales declines in the past. The most recent was the 2.3% drop experienced in the first quarter of 2024. But these have almost always been short term blips on the radar. While these declines may not seem significant, they can have a material impact on profit margins. This is because we are dealing in a low margin space that is highly competitive. The asset intensive nature of this business, combined with competitive pressures, makes comparable sales declines painful.

Author - SEC EDGAR Data

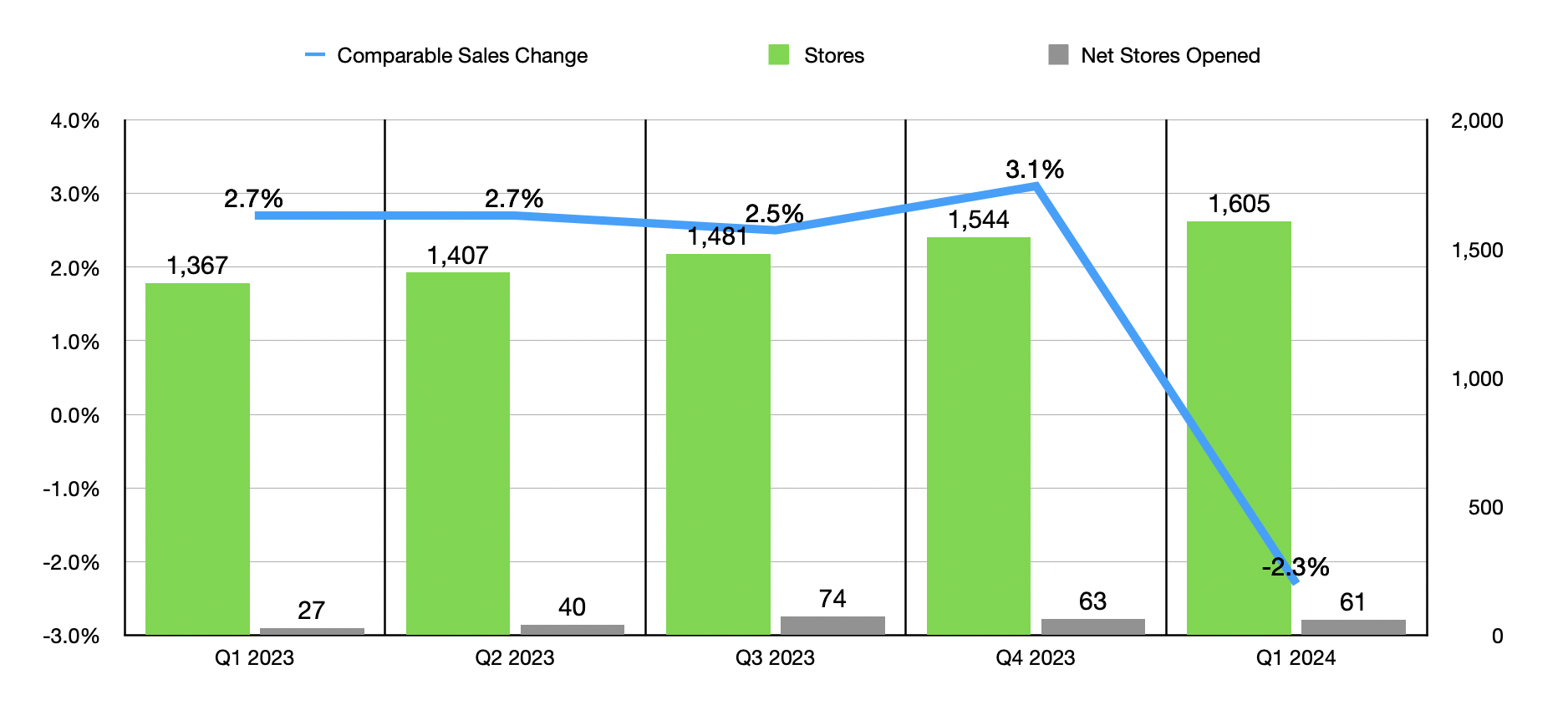

As I stated earlier in this article, Five Below has a history of attractive growth. In the chart above, you can see the number of locations in any given quarter, as well as the number of new locations built during that time. You can also see the comparable sales change on a year over year basis. In the five quarters covered, only the first quarter of 2024 saw a year over year decline when it came to comparable store sales. In my prior article on the business, I did tell investors this was probably not terribly worrisome. And based on guidance that existed at that time, I claimed that we would see improvements in subsequent quarters. This is because management was forecasting comparable store sales growth for 2024 in its entirety of between 3% and 5%. Given this recent update, this is looking increasingly unlikely.

In its statement, the management team at the firm said that revenue in the second quarter of 2024 will likely come in at between $820 million and $826 million. At the midpoint, this is still 8.4% above the $759 million reported for the second quarter of 2023. However, analysts were actually expecting sales of $839.8 million. As I alluded to earlier, this will also have an impact on the company's bottom line. Management is now forecasting earnings per share of between $0.53 and $0.56. In addition to being lower than the $0.84 per share reported the same time last year, this will also fall short of the $0.65 per share that analysts were hoping for. This would mean net income of between $29.3 million and $30.9 million. That compares to the $35.9 million that analysts were anticipating.

Author - SEC EDGAR Data

It's unclear what this all means for the long term picture for the company. But even if we make some adjustments, because of the decline in share price recently, Five Below might still warrant a bullish outlook. In my prior article on the firm, I used management's forecast that called for the retailer to have 3,500 locations by the year 2030. That is up from the 1,605 locations that the business had at the end of the first quarter of this year. So we are looking at a more than doubling in physical footprint. It would not be surprising if these plans are scaled back, particularly if this press release is just the start of what could be additional pain down the road.

The good news is that even if we make some reasonable assumptions, shares might still be worth more than what they are trading for. Given the comparable sales decline of 6.5%, at the midpoint, anticipated for the second quarter of this year, and applying that to projected revenue per store per year, reaching the company’s store count target by the year 2030 would imply annual revenue of $7.08 billion. This is down from the prior forecast I gave of $7.56 billion. Given the margin contraction anticipated for this second quarter release compared to what was seen last year and applying that contraction to the firm's various profitability metrics, we would see a business that, in 2030, would generate around $488.8 million in net income, $807.5 million in adjusted operating cash flow, and $942.8 million worth of EBITDA.

Using the same trading multiples as in my prior article on the retailer, I calculated a market capitalization for the company in the future of between $7.99 billion and $11.97 billion. At the low end, that would translate to annualized upside of 7.2%. But on the higher end of the spectrum, we are looking at about 14.1% per annum. Historically speaking, the market does see upside of around 11% to 12% per annum. So this would constitute a market beating return. This does not factor in the ability to raise prices with inflation, which will probably be between 2% and 3% per annum. If we just strip out inflation from the annualized upside in the market, using midpoint figures, then you're comparing this amount of upside for the company to an annualized gain of about 9%.

Author - SEC EDGAR Data

Takeaway

Fundamentally speaking, the picture for discount retailer Five Below is now changing rather rapidly. To be perfectly honest with you, this should be concerning to investors. The change in guidance is one thing. But when you add on top of this the fact that it occurred simultaneous to a major management shake-up, I think that investors would be right to be worried. For those who don't mind volatility and uncertainty, the company very well could turn out to be a good prospect. But seeing as how I am a more conservative investor, I believe that this is justification to downgrade the stock to a ‘hold’ until additional data comes out. That won't be until the firm reports second quarter earnings results, likely sometime around the end of August or early September.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!