Nikada

Investment thesis: Recent economic data gave rise to a new market thesis that the Federal Reserve is behind the curve on interest rates, and we may be headed into a recession due to its failure to preempt an economic contraction. With the benefit of hindsight it becomes increasingly clear that the poor jobs report, in correlation with other metrics, the panic seems to have been unwarranted. Expectations of impending interest rate cuts seem unwarranted as well, even though it is not unlikely that the Fed will oblige the market and start cutting rates this fall, which will not help the US or the World to prevent an economic slowdown. The most likely trigger of the next economic downturn remains an oil price spike, leading to a stagflationary market selloff that is probably months away. The current volatility triggered by the false start to buying season is still an opportunity to selectively buy stocks while keeping most cash in reserve, expecting a broader, more favorable opportunity to deploy cash further down the road.

Not enough oil production growth to sustain continued global GDP growth at current levels.

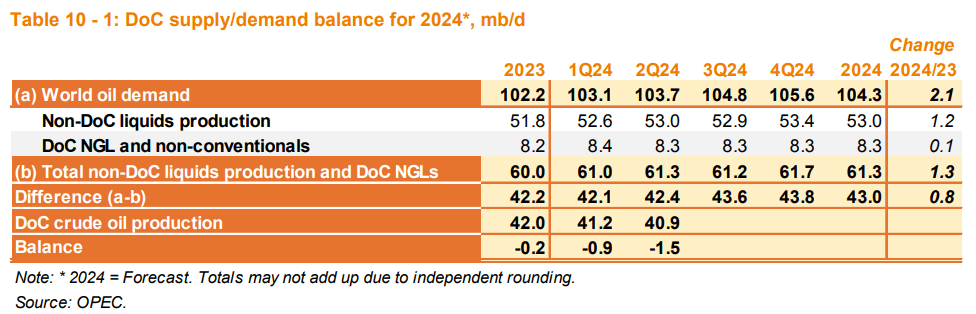

- OPEC estimates a Q2 shortfall in global supply/demand of 1.6 mb/d, while an estimated increase in demand by the end of 2025 is 3.6 mb/d.

OPEC currently estimates that the global liquid fuels market is experiencing a shortfall in supplies of 1.5 mb/d as of the last quarter.

OPEC

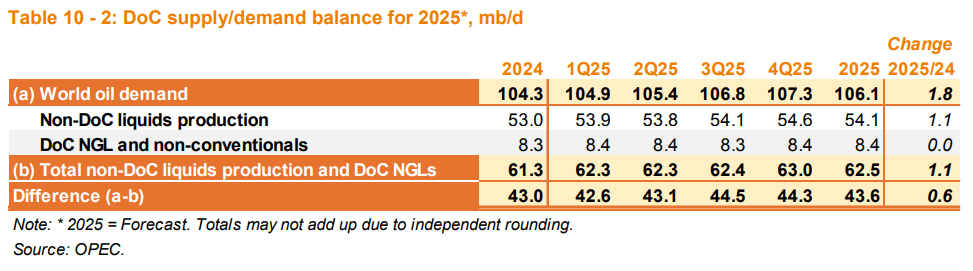

It did not provide a forecast in terms of the global supply/demand balance for the rest of the year, or for the following year, but it did provide quarterly demand estimates, which show that by Q4, 2025 global demand will be about 3.5 mb/d higher compared with Q2, 2024. Combined with what already looks like a significant supply/demand gap of 1.5 mb/d, it looks like we will need supply growth or demand destruction equaling about 5 mb/d by the end of next year to balance the global oil market.

OPEC

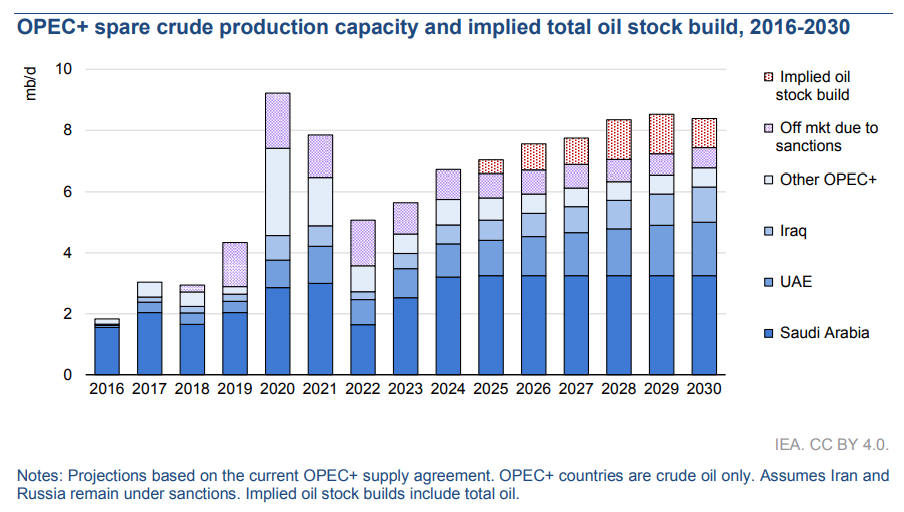

- IEA does not share OPEC's tight market viewpoint.

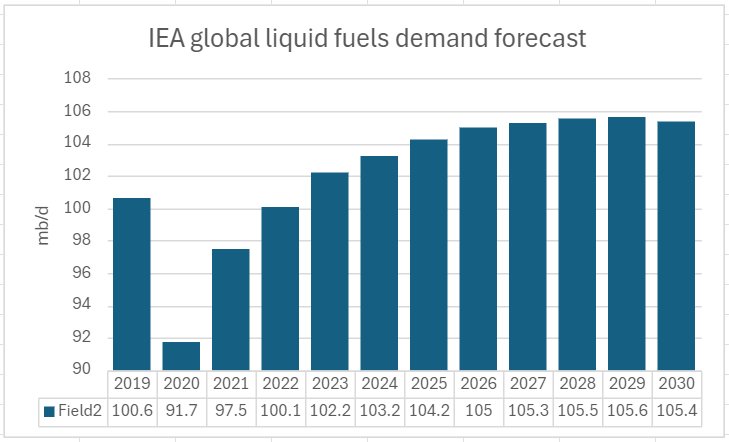

Unlike OPEC, the IEA sees massive spare capacity builds going forward for OPEC+, while global demand for liquid fuels is seen as slowing dramatically.

IEA

Data source: IEA

It remains to be seen which outlook turns out to be correct. It could also be that neither one will be correct. At the moment, I am more inclined to trust OPEC's outlook on supplies, while on the demand side, perhaps OPEC is a little bit on the optimistic side, and the reality might be somewhere closer to an in-between the two forecasts for this year and next. If this is the case, chances are that unless an unforeseen trigger event for a significant global recession will preempt it, an oil price spike is likely to happen by the end of this year or at some point next year, at the latest. The oil price spike will then trigger a recession. Either way, a recession is likely to occur, before the end of next year.

The growth scare triggered by the jobs data headline seems unwarranted.

The recent stock market selloff we are seeing is mostly fed by a few data points that suggest a slowdown in economic activity, while other data points that point to the contrary, are ignored.

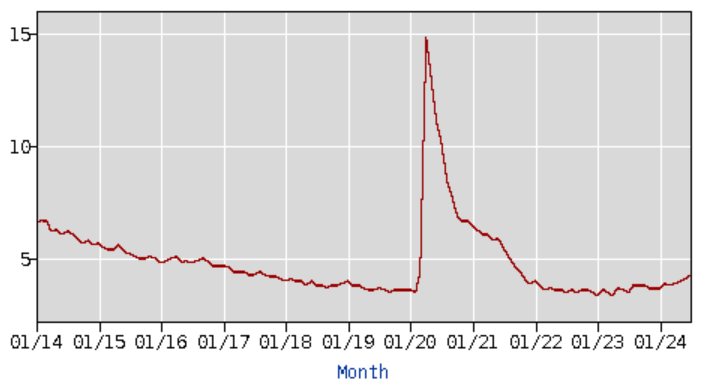

Bureau of Labor Statistics

The employment trend has been heading in the wrong direction for about a year and a half now, but the last data point we got for July, showed an increase from 4.1% to 4.3%, creating a sudden panic, though it just seems to fit the trend. It should be noted that we continue to see job gains, albeit at a slower pace, but those gains are not keeping up with the increase in the number of jobseekers.

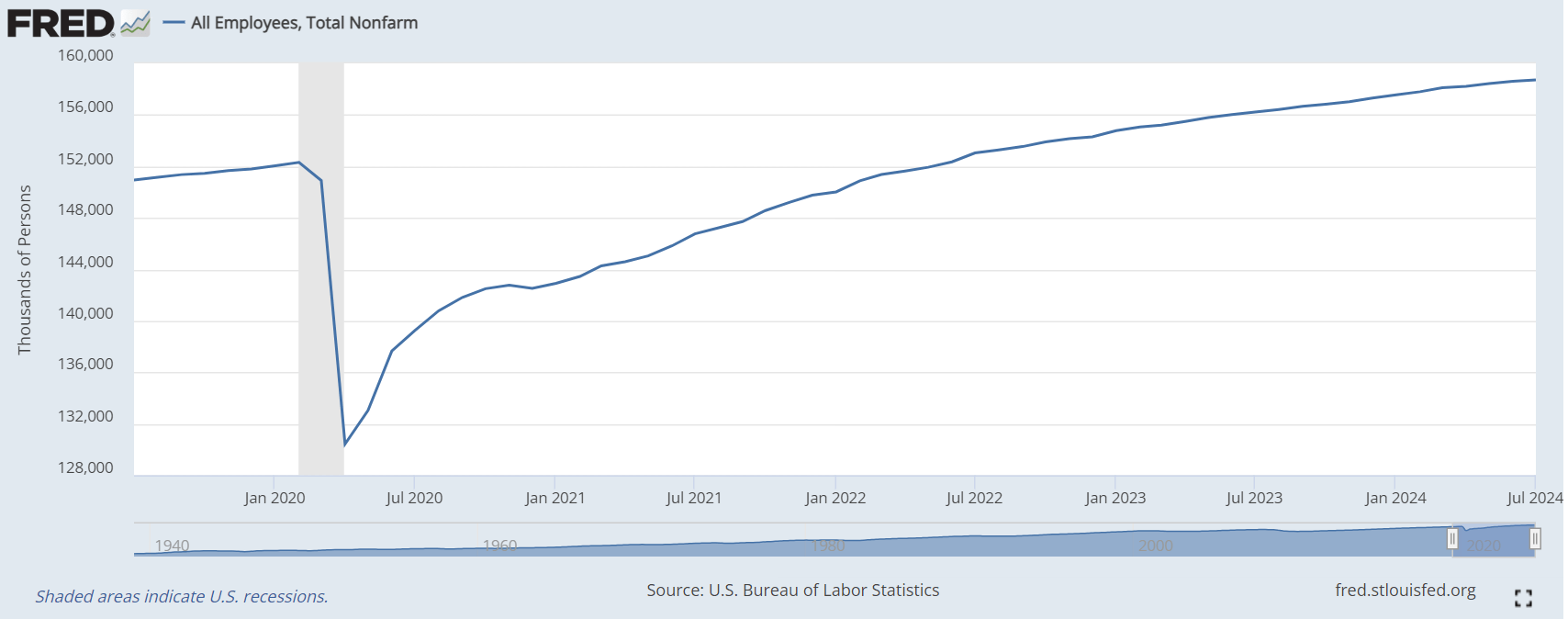

Federal Reserve Bank of St. Louis

Household finances are headed in an unhealthy direction, but we are not yet at a breaking point.

Other data points that should be of concern for the market include signs that US consumers are seeing a weakening of their financial position.

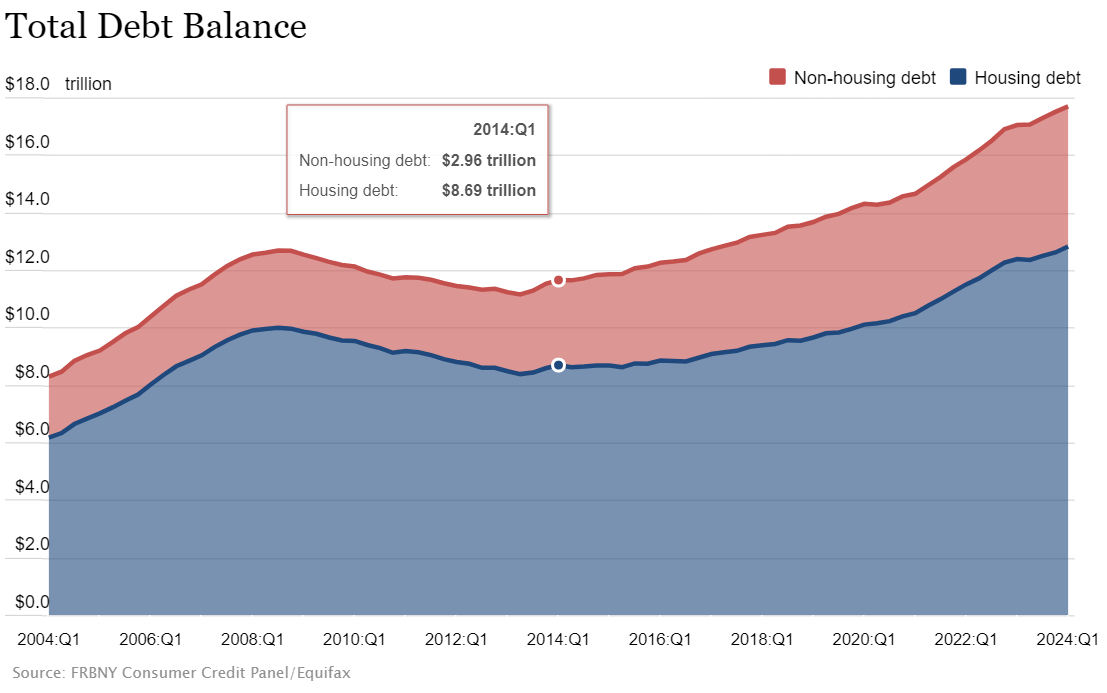

US total household debt (Federal Reserve Bank of New York)

The household debt situation is both a short-term worry and a long-term reason to be concerned. Household debt increased by over 50% over the past decade, with non-housing debt in particular, which is higher interest debt, rising by about 65%. This increase comes within the context of much higher interest rates compared with a decade ago.

What this means in the short term is that within the context of higher interest rates, consumers risk having their finances enter a vicious cycle, where more debt has to be accumulated just to keep pace with rising interest costs.

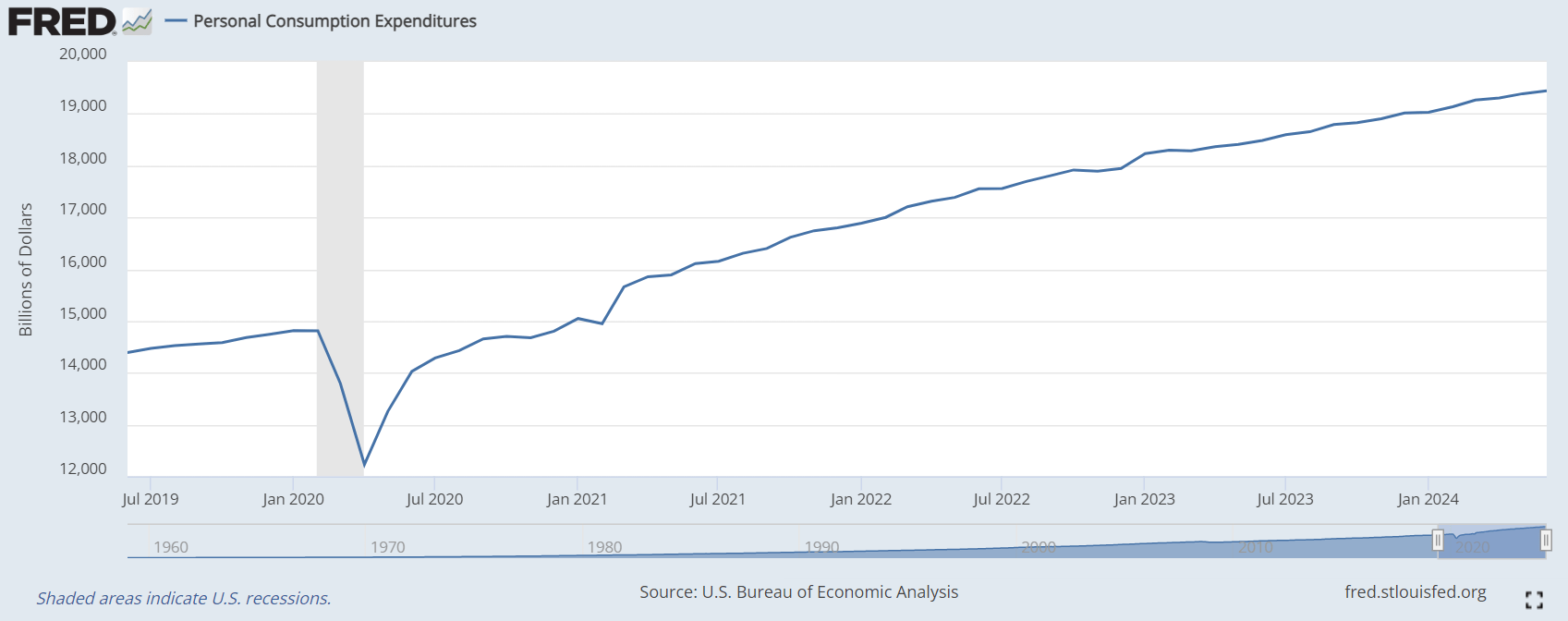

Federal Reserve Bank of St. Louis

At the moment, consumer spending is still rising, at a similar pace as household debt, with both increasing by about 6.5% since the beginning of 2023. At the same time, the personal savings rates declined from over 4.4% to just 3.4% for the same period. Consumer spending growth is currently driven by a combination of rising debt and a drop in savings for many households.

Consumer demand is still rising, meaning that higher interest rates are yet to have a fully detrimental impact on consumers. Even though inflation rates continue to linger above 3%, significantly above the Fed's target of 2%, the emerging argument is that the Fed is behind the curve, and they should have already started lowering interest rates, to prevent a recession that based on the data available, it may not be imminent. My personal view is that the market is increasingly getting desperate to see those rate cuts because without those rate cuts the current market is overvalued.

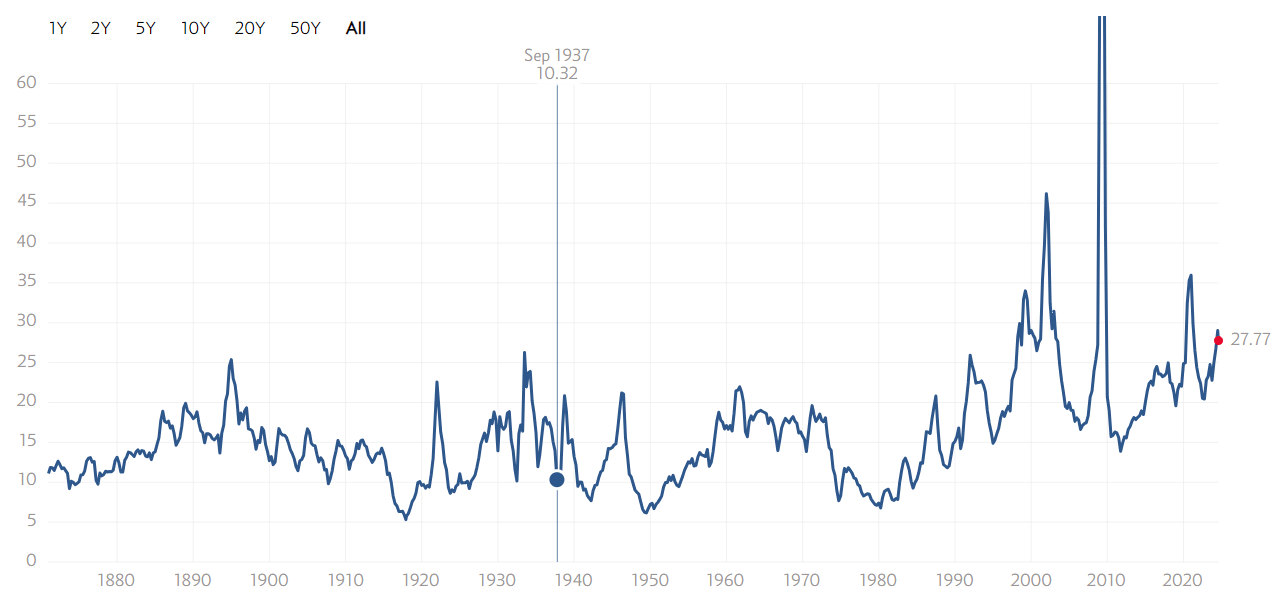

S&P 500 historical P/E ratio (Multipl.com)

By historical standards, the current P/E ratio of the S&P 500, sitting at over 27 currently, is far above the long-term average of 16. A market valuation higher than the historical trends was justified in the post-2008 financial crisis environment due to lower interest rates. We are now in a third year of higher interest rates, with the market still waiting for a return to pre-2022 low-interest rate conditions. It might therefore be understandable why any data point that supports the interest rate cut thesis becomes amplified and rises in prominence over other data points that may point to the contrary.

Investment implications:

- A volatile market makes for selective buying opportunities.

In the immediate aftermath of the disappointing jobs numbers, the recent stock market downturn was a brief opportunity for investors to start kicking the tires on some investment opportunities or add to existing positions. I slightly increased my modest position in Intel (INTC) stock, once it was hit by a double whammy in the form of disappointing financial results, as well as a broader market selloff. I also added to my current Ford (F) position and Albemarle (ALB), which trades at 1/3 of its all-time high share price. In both cases, I improved my average cost/share significantly. I started a position in AMD (AMD), which is my second venture into this stock so far this decade. I am willing to incrementally add to my current positions in these stocks if their price continues to decline in line with the overall market, unless new company-specific details emerge that will cause me to change my mind. As of now, I am keeping most of my sizable cash position in reserve, in expectation of a broader market selloff.

- A selling opportunity may arise before a broad market buying opportunity will materialize.

If my thesis proves to be correct, there will be an oil price spike before there is a recession. If this is the case, there will be an opportunity to take profits, for those invested in oil-producing companies. I currently own Suncor (SU) as well as CNQ (CNQ) stocks. Suncor is by far my biggest stock position at this point; thus an oil price spike is an ideal scenario for those looking to take some profits. I already sold some of my Suncor shares once it went over $40/share back in May. My next target for incremental selling is $45/share. I am also looking to add to my Suncor position if its share price declines below $30, in case my thesis does not prove to be correct. I will probably maintain a sizable stock position in this company throughout.

- Some indicators suggest economic activity is still relatively robust, leaving the Federal Reserve with the option of waiting for inflation to drop to its 2% target before making a move.

Now that the knee-jerk reaction to the unemployment rate increase is behind us, we can take a step back and more closely examine the report. We can also look at other metrics to get a better sense of where the economy is headed. First and foremost, we have to recognize that the economy is still adding jobs, even if it is at a slower pace than the increase in the actively working or looking labor force. The latest weekly unemployment claim numbers suggest that there isn't a significant layoff trend.

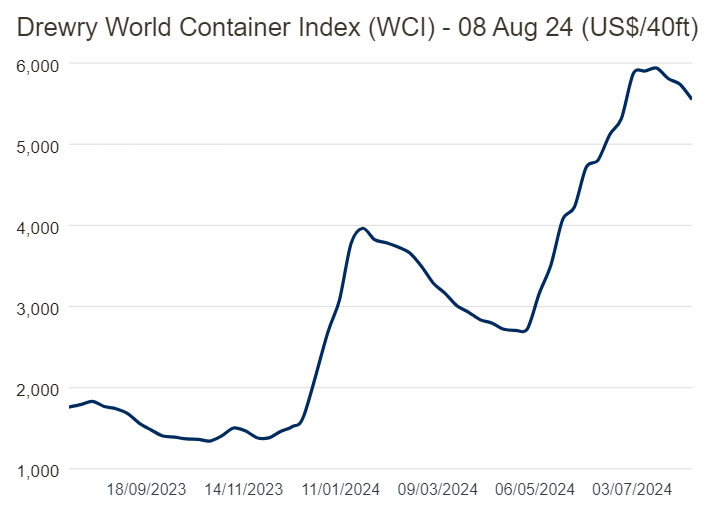

Other data, such as global shipping rates, suggest that the global economy is still active in terms of moving physical goods.

Drewry

While there has been a dip in shipping costs, it is not yet a sizable move, given that we are still seeing shipping costs that are double compared with the start of the year.

Other metrics of interest include US liquid fuel demand trends, which were recently revised higher. This suggests that economic activity in the US, including transport, and personal travel is going strong. The worsening debt versus household savings trends, with both headed in the wrong direction, arguably indicates that consumer demand is set to weaken at some point going forward, which will then put a damper on economic activity growth. The classical government intervention to a trend of weakening economic growth, through higher fiscal spending, is unlikely to materialize, given that deficits are running in the $2 Trillion/year range based on CBO projections. If anything, it may have to be reined in, to a more sustainable level. At this point, it is not yet clear that an event of slowing consumer & government spending is unfolding to justify the panicked calls for the Federal Reserve to start lowering interest rates.

Looking at the macro trends as I see them, I do not see a clear-cut argument in favor of aggressive rate cutting. The Federal Reserve may therefore move very cautiously at best on lowering rates before inflation declines to the desired 2% target. As of right now, even though signs suggest we should expect further improvements, we are still looking at 3% CPI inflation. The combination of continued resilience in global economic activity, coupled with global oil supply constraints that can be inflationary, may still throw a wrench into the market's gears in terms of rate cut expectations if the OPEC data and forecasts prove to be correct.

The recent market selloff, triggered by a misunderstood jobs report, is likely the start of a period of market volatility, but not necessarily a major market correction. The long-running Fed rate cut guessing game will most likely continue, and we may even see some vindication this fall for those who have been betting on the start of rate cuts. Oil prices will likely rise this fall unless a dramatic change in global economic activity will lead to a sizable and sustained cut in demand. Higher oil prices will in turn lead to a stagflationary environment because it pushes inflationary pressures higher while putting additional pressure on consumers. In other words, we are likely to see a deep market selloff as the economy starts to contract, while fiscal & monetary policies that helped keep past downturns more shallow & brief will not come to the rescue. That will be the start of the real buying opportunity, and if my thesis proves to be correct, the price of oil is what we have to watch as the main signal, not the Fed.