InterNetwork Media/DigitalVision via Getty Images

Following a disappointing start to the year, investors in satellite data provider Spire Global Inc. or "Spire" (NYSE:SPIR) were looking forward to an improved second quarter report after the close of Wednesday's regular session as projected by management on the Q1/2024 conference call and also reflected in consensus expectations.

But rather than delivering on its promises, the company filed a notification of late filing on form 12b-25 with the SEC:

The Company is in the process of reviewing its accounting practices and procedures with respect to revenue recognition related to certain contracts in its “Space as a Service” business (the “Contracts”) under applicable accounting standards and guidance.

The re-evaluation relates to the potential existence of embedded leases of identifiable assets in the Contracts and the related recognition of revenue for pre-space mission activities. The Company is also considering any related internal control matters associated with the Contracts.

Due to this ongoing review, the preparation of the Company’s condensed consolidated financial statements as of June 30, 2024 and for the three and six months ended June 30, 2024, will require additional time to complete. Depending upon the results of this review, the Company may be required to restate or revise its previously issued financial statements.

(...)

While the Company’s review is ongoing, at the time of filing this report, the type of Contracts that the Company has identified for re-evaluation resulted in recognized revenue of approximately $10 to $15 million on an annual basis. Depending on the results of the review, additional financial measures such as gross profit could also be impacted. However, the Company believes that the re-evaluation of its revenue recognition for these Contracts will not impact the Company’s statements of cash flows for any period.

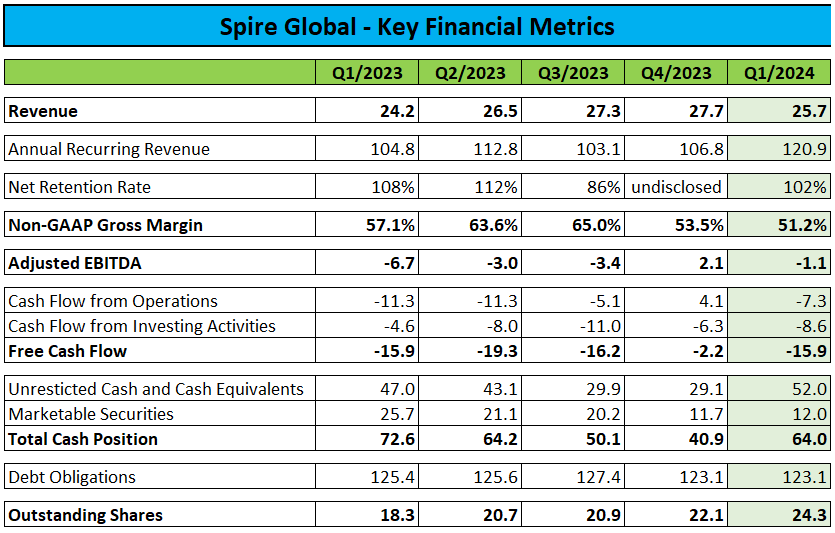

While accounting deficiencies should not be taken lightly, a non-cash impact of up to $15 million on Spire's annual results doesn't seem be the end of the world for a company with over $100 million in annual revenues last year:

Regulatory Filings

However, the bad news doesn't stop here as Spire also warned of debt covenant violations (emphasis added by author):

As a result of this ongoing review and the related delay in the preparation of the Company’s financial statements for such periods, the Company will be unable to deliver the quarterly financial information that is required to be provided to the lenders under the Company’s financing agreement (the “Financing Agreement”) with Blue Torch Finance LLC (“Blue Torch”), as administrative agent and collateral agent, and certain lenders, as of and for periods ended June 30, 2024, and potentially future periods, depending on when its review related to the Contracts is complete.

Further, based on preliminary information, but subject to change as a result of the ongoing review described above, the Company believes that it may not be in compliance with the maximum debt to EBITDA leverage ratio financial covenant under the Financing Agreement as of June 30, 2024.

The Company is in active dialog with Blue Torch regarding potential waivers and/or amendments to the Financing Agreement, which may include a fee payment or potential additional financial covenant requirements, in an effort to avoid the collateral agent exercising remedies available to it under the Financing Agreement. For the avoidance of doubt, there is no assurance that the lenders will agree to any waiver or amendment to the Financing Agreement on terms acceptable to the Company or at all.

Please note that just four months ago, Blue Torch agreed to increase the maximum debt to EBITDA leverage ratio for the monthly periods ending June 30, 2024, July 31, 2024 and August 31, 2024 in addition to reducing the minimum liquidity covenant from $30 million to $20 million in exchange for a $10 million prepayment and a $0.2 million early termination fee.

Remember also that on the Q1/2024 conference call, management projected the company to achieve positive adjusted EBITDA in the second quarter and advertised a near-term refinancing of the $108 million outstanding under the Blue Torch term loan facility (emphasis added by author):

We expect positive adjusted EBITDA in Q2 '24 and remain on track for positive free cash flow this summer. We believe these accomplishments put us in an even stronger position to refinance our existing Blue Torch Capital loan to lower our cost of funding. We have continued to make progress on this front, having spent time with numerous financial institutions to better understand the current market landscape. Given market conditions prevalent as of today, we're targeting to have the refinance completed by the end of 2024.

However, with Spire likely facing a protracted accounting review and resulting inability to remain current with its SEC filing obligations, the company won't be able to refinance its debt obligations anytime soon.

Even worse, with Spire apparently having violated an adjusted EBITDA-related covenant, I would expect second quarter results to have fallen well short of management's projections again. That said, it will likely take several months or even quarters for the company to file its Q2 report on form 10-Q.

In the meantime, Spire will be at the mercy of its lender. But that's still not all.

Earlier this week, one of Spire's key customers, NorthStar Earth & Space Inc. ("NorthStar") asked for a court injunction to stop the company from shutting off the data flow from their space situational awareness satellites operated by Spire. In addition, NorthStar appears to have issued a notice of contract default to the company.

While I didn't manage to obtain the full court application, an alleged default under one of Spire's most prominent contracts certainly won't help the company obtaining a waiver and additional covenant relief from its lender.

For my part, I would expect the loan parties to enter into a forbearance agreement to provide more time to sort things out. Without reliable financial statements, Blue Torch is not likely to provide another waiver or additional covenant relief, and Spire won't be able to raise equity in order to repay the term loan.

Without an amicable solution, Spire Global would likely be required to file for bankruptcy protection which could result in Blue Torch becoming the new owner of the business by the means of a credit bid in a court-supervised auction pursuant to section 363 of the U.S. Bankruptcy Code.

Under this scenario, I would not expect any sort of recovery for common shareholders.

But right now, Spire Global needs to tackle several key issues at the same time:

- Complete the accounting review and prepare revised financial statements.

- Address debt covenant violations in order to avoid a default.

- Improve execution to make sure that the company delivers upon its financial targets in the future and avoids a liquidity crunch.

- Come to terms with NorthStar.

With market participants left in the dark regarding the company's financial performance and considering the risk of a near-term debt default, investors should consider moving to the sidelines until the dust clears.

Bottom Line

At least in my opinion, Spire Global is not likely to file its second quarter report on form 10-Q anytime soon, thus leaving key stakeholders in the dark regarding the financial performance and condition of the company for an extended period of time.

But without reliable financials, Spire's lender is not likely to provide a waiver and much-needed covenant relief.

Under a worst-case scenario, the company might end up in bankruptcy, with common shareholders at risk of holding the bag.

Given the company's vastly increased risk profile and substantial uncertainties regarding the path forward for the business, investors should consider moving to the sidelines.

Consequently, I am assigning a "Sell" rating to Spire Global's shares.

Massively Outperform in Any Market

Value Investor's Edge provides the world's best energy, shipping, and offshore market research. Even during turbulent market conditions, our long-only models have outperformed the S&P 500 by more than 30% YTD.

We also offer income-focused coverage geared towards investors who prefer lower-risk firms with steady dividend payouts. Our 8-year track record proves the ability of our analyst team to outperform across all market conditions. Join VIE now to access our latest top picks and model portfolios.