JHVEPhoto/iStock Editorial via Getty Images

It's been a surprising earnings season so far in Q2, where many high-flying stocks have been pummeled and rebound plays have unexpectedly stepped into the spotlight. Such was the case for Expedia (NASDAQ:EXPE), the online travel giant that has been beleaguered by softer trends at its home-sharing subsidiary Vrbo and lost tremendous market value this year.

But in Q2, Expedia pulled off a much-needed turnaround. Whereas rivals Booking.com (BKNG) and Airbnb (ABNB) reported slower growth on weakening vacation trends, Expedia reported the exact opposite with accelerating bookings. Shares of Expedia have jumped ~10% since the earnings print, but even after these gains, the stock remains down nearly 15% for the year.

I last wrote a bullish note on Expedia in June, when the company was still reeling from its post-Vrbo slowdown. At the time, I had argued that the company had solid fundamentals in place, a long-term tailwind in its One Key program which outshines rivals' offerings, and cost cuts in place that were set to boost the company's profitability and make its valuation quite appealing. Now, we've also seen evidence of strengthening bookings in Q2 while peers are waning, leading me to reiterate my buy rating on Expedia.

I'm approaching Expedia from the point of view of both a bullish investor as well as a very frequent user (Platinum level on the company's One Key program). In my view, Expedia (and its sister brand, Hotels.com) has done a great job at being price-competitive with Booking.com and Priceline, especially with the fact that its One Key program yields at least a 2% cash back return on most bookings (up to 6% for Platinum users, and even higher for properties that are labeled as "VIP Access" with which Expedia has a close relationship). The fact that Expedia is showing improving growth rates in Q2 while Booking is experiencing a slowdown shows us that Expedia, long considered to lag behind Booking in terms of execution and customer appeal, is catching up and becoming competitive after a complicated rollout of the new rewards program.

Here is my updated bull case for Expedia:

- Expedia is home to a diverse family of brands covering all aspects of travel. Its best-known brands include Expedia itself, Hotels.com, Orbitz, Hotwire.com, and several others. With these brands, the company covers hotels, air travel, car rentals, vacation experiences, and others at a wide variety of price points.

- One Key program distinguishes Expedia against the competition. Though the One Key rollout and unifying Expedia's apps under a single technology stack was a complicated multi-year rollout that had many hiccups along the way, the fact remains that One Key is now the only rewards program that offers a cash-back yield (whereas Priceline's VIP program and Booking's Genius do not; and to date Airbnb still has not announced any type of loyalty offering). This often makes booking via Expedia the most cost-effective option when prices are at par.

- Doubling down on One Key with partner offerings. The company recently introduced a co-branded One Key credit card with Wells Fargo and Mastercard (with a fee and no-fee option, with sign-up rewards of $600 and $400 in One Key Cash respectively) - encouraging more spending on the Expedia family of brands.

- Verb is Expedia's answer to Airbnb. OTAs have now proven themselves to be capable of co-existing alongside Airbnb, with hotels serving a slightly different use case from vacation rentals. But Expedia also plays in the vacation rental space and captures this market through its Verb subsidiary, expanding its market.

- New leadership focused on profitability. Since Expedia's new CEO came in this year, the company has turned its focus from rolling out One Key to growing profitability and slashing expenses where possible.

Best of all, despite gross bookings growth rates converging to a near-similar pace, the market is still valuing Expedia at a substantial discount to its larger peer Booking. Expedia trades at an 11x forward P/E compared to just under 20x for Booking.com (even after the latter's post-earnings crash):

With both a modest valuation and a number of bullish catalysts under Expedia's belt, I'd continue to buy this stock as it starts a rebound rally up to a more normalized valuation.

Q2 download

Let's now discuss Expedia's latest Q2 results in greater detail, which surprised the markets with a beat where many other travel stocks floundered. The Q2 earnings summary is shown below:

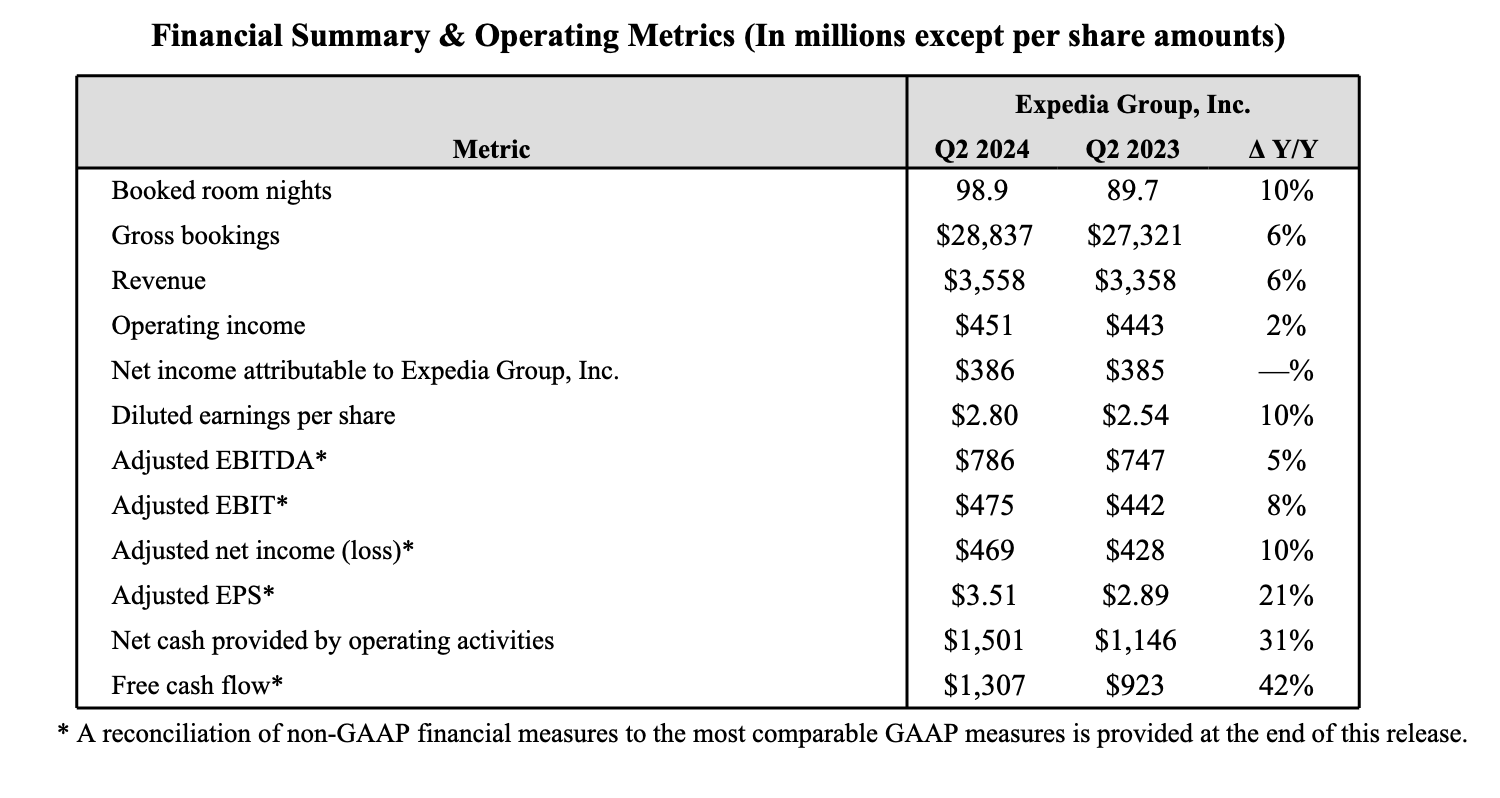

Expedia Q2 results (Expedia Q2 earnings release)

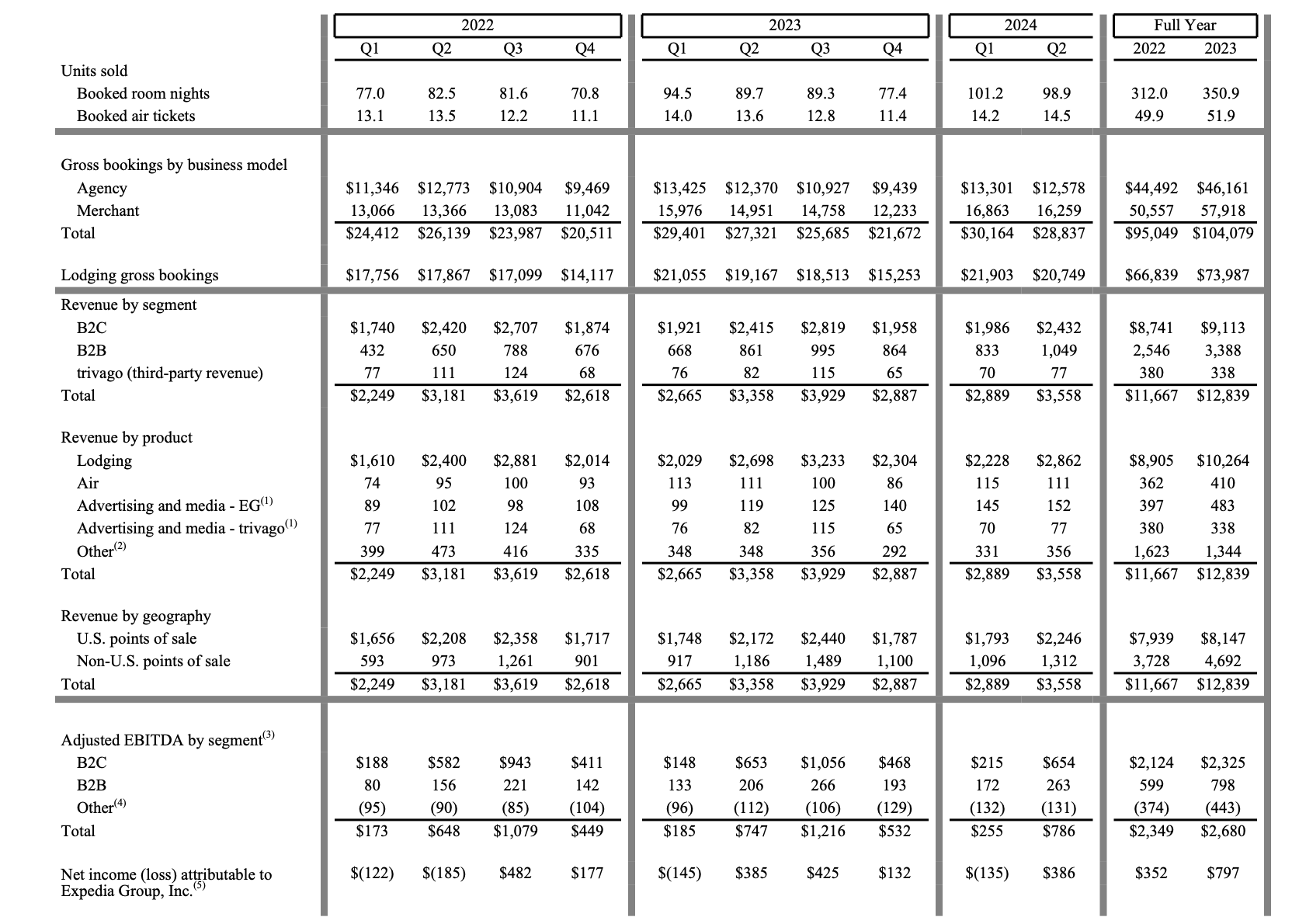

Revenue grew 6% y/y to $3.36 billion, ahead of Wall Street's expectations of $3.53 billion (+5% y/y). This was on the back of a 6% y/y growth rate in gross bookings to $28.8 billion, which accelerated from 3% y/y growth in Q1 as shown in the trended chart below:

Expedia trended bookings results (Expedia Q2 earnings release)

The company saw strength in room night trends, with room nights booked growing 10% y/y to 98.9 million. Importantly as well, the company notes that Vrbo saw a turnaround in performance after hitting a low point in Q1, which the company attributed to boosted marketing investments as well as better supply of vacation rental properties.

It's not entirely smooth sailing for Expedia, as the company pointed out that its international segment is doing better than the U.S., where Airbnb cited on its earnings call that American bookings have softened. But overall, CEO Ariana Gorin noted on the Q2 earnings call that the travel environment remained healthy, and hotel prices have held up:

The travel environment was healthy in the second quarter. And like the last few quarters, we saw stronger demand internationally relative to the U.S. Compared to last year, we grew room nights mid-single digits in the U.S. low double digits in Europe and in the high teens in the rest of the world. Prices held up for both hotel and vacation rentals but we saw continued pricing pressure for air and car. In terms of trends so far in the third quarter, we've seen some softness in demand and Julie will provide more details on this in a few minutes. But regardless of the market environment, we're focused on executing what's in our control and what we know will drive long-term value.

Now, let me talk a little bit about the second quarter results themselves. In our Consumer business, we grew gross bookings by 1% which was an improvement of nearly 400 basis points in the first quarter. Our focus on the basics, traffic, conversion, attach rates and marketing efficiency is showing solid early results. The traffic growth across our 3 core brands which are Expedia Hotels.com and Vrbo accelerated sequentially by roughly 500 basis points and conversion rates continue to improve. The percent of bookings through our apps also increased, up over 500 basis points year-on-year. And in terms of attach, multi-item trips grew by 9% compared to last year. And this is important because when travelers buy more than one product from us, they're getting more value, so they're more likely to repeat."

It's worth noting that Booking.com's gross bookings growth rates decelerated from 10% y/y growth in Q1 to 4% y/y growth in Q2 (6% on a constant currency basis; unfortunately Expedia doesn't provide constant-currency normalizations to compare against). So whereas Expedia started out from a weaker point in integrating its One Key program and restoring confidence in Vrbo, it's now improving dramatically to a point where its growth is on par with Booking.com.

From a profitability standpoint, Expedia's adjusted EBITDA grew 5% y/y to $786 million, with adjusted EBITDA margins remaining roughly flat y/y at 22%. The company notes that overhead costs declined by -3% y/y driven by the company's headcount restructuring, but this was offset by deeper marketing investments that the company put in place, including at Vrbo. Still, we note the company's pro forma EPS of $3.51 quashed Wall Street's expectation of $3.16 with 11% upside.

Risks and key takeaways

I'll stress here that the coast is not perfectly clear for Expedia. Like Airbnb and Booking.com, Expedia also warned of a potentially softer travel environment heading into Q3. In particular, it noted that it saw in July a trend of lower ADRs (average daily rates) with more price-sensitive consumers opting for cheaper hotels. As such, the company is expecting gross bookings and revenue in Q3 to range between 3-5%, representing a slight deceleration from current-quarter results.

Still, I'd argue that Expedia is no more exposed to macro-related travel slowdowns than any of its peers, and the fact that Expedia's bookings growth finally caught up to Booking's in Q2 is a great sign of competitive parity between the two. With Expedia trading significantly cheaper than Booking (a stock I'm neutral on), plus having a long-term competitive advantage in already having unified its brands under the attractive One Key program, Expedia is my favored horse in this race.