Jon Lovette/DigitalVision via Getty Images

Although Expedia Group stock (NASDAQ:EXPE) is here at an attractive valuation with a forward PE of around just 11, the company is showing many bad signs that imply an impossibility of getting real growth. In my view, the stock is not a buy, but due to uncertainty and the relatively low valuation, it is nothing more than a hold.

Expedia brief business model

Expedia, as presented in its 10K filing, is an online travel company. It offers around 3 million lodging properties, including hotels and alternative accommodations. The company also offers offerings from around 500 airlines, rental cars, insurance, and experiences.

Expedia Group has not only the evident Expedia brand but also Hotels.com, Vrbo, Orbitz, Travelocity, ebookers, and Wotif. All of these brands have a similar business model, working either as an Agency or a Merchant. You can see both business models compared here. Expedia also owns Trivago, which is a travel advertising business, instead of actually brokering the travel products between a consumer and a business. Trivago is a very small part of the business with only around 2.6% of revenues.

Expedia's business model was hit hard during the pandemic, and is just recently completely recovering both revenues and operating margins.

The company has two main competitors who are bigger than EXPE. On the one hand, Booking, which is in both hotels and alternative accommodations, competes directly with Hotels.com, the Expedia brand, and Vrbo. On the other hand, Airbnb is the leading actor in the alternative accommodation online offering. Both companies have significant advantages over Expedia; in my opinion, the main one is being able to spend more on advertising and, therefore, get better deals with businesses and higher margins. Also, I think the Airbnb brand is more iconic than Vrbo. It is also important to remember that Expedia has been in a management transition process since February of this year.

Expedia Q2 2024 results

Recently, Expedia reported its Q2 2024 earnings results. The company showed, at first glance, good or even impressive results. Gross bookings and revenue went up 6% year-over-year, adjusted EBITDA and adjusted EPS increased 5% and 21% respectively. This looks good, but in my opinion if analyzed deeply the stock might be finding a mid-term peak growth, which could justify the low stock valuation multiples.

The bad

There are some bad results with EXPE for the last Q2 2024. The first sub-optimal news comes from the nominal increase in revenues of $200 million when compared with the nominal increase in selling and marketing of $214 million. This lower performance in advertising, in my opinion, talks about Expedia reaching a ceiling in organic growth. For example, Booking, perhaps its most similar competitor, reported in its last earnings release that it spent $138 million more in marketing expenses but received $397 million more in total revenues. This suggests that Expedia is getting outcompete and is trying to overuse its balance sheet to bring some growth that will end-up not being sustainable.

Because of that marketing spending, in its last earnings call, the management expressed that the Expedia brand increased revenues by 20%, and Vrbo came back to see some modest growth from Q1. This is, in my opinion, another terrible sign since the company cannot compete with Airbnb either, which also recently reported an 11% growth year-over-year and more than double EXPE's net revenues. This is very important because, in my view, eventually, the biggest company in the sector will be able to outspend in marketing the others and end up with a huge edge, as what happened years ago with Booking beating Expedia in revenues and growth.

To combat that difficult competition, the management is trying to implement integrated loyalty programs between the legacy business, and Vrbo, like the OneKey initiative. This is insufficient in my opinion to give good competition. It is important to remember that all this is happening while the company is in a management restructuring and has cut jobs of around 1500 workers or close to 9% of the workforce at the year's beginning.

Bad balance sheet and capital allocation

While those operating expenses reduction measures are being conducted, the company has done buybacks by $1.2 billion in this year. The management is in my opinion taking too much risk with these measures, mainly because the balance sheet is losing too much solidity, and when bad times arrive, because this is still a cyclical business after all, the stock would eventually see significant volatility.

Another problem to the balance sheet comes in the form of the current liabilities not being well covered by current assets. This gap has increased considerably from negative $2 billion to $4 billion, leaving the company more vulnerable. So in that sense, while the music is playing, everything is going to be working correctly, but when it eventually stops, like in 2020, this could leave the company suffering too much pain.

The long-term debt situation is also not good. LT Debt has been for a while at around $6.2 billion but now has decreased by $1 billion due to maturities that have been reached this year. This debt is approximately 5 times this year's projected earnings and has made EXPE pay around $500 million in interest expenses last year. This will increase as the debt rollover will have to be made at higher interest rates than the current 3.7% that EXPE is paying. It might likely double due to Expedia's not that great BBB- credit rating in Fitch.

This is another sample, in my opinion, of the bad capital allocation that the management has done, announcing to complete $3.6 billion in buybacks, instead of paying down debt which will bring more solidity to the cashflows and the stock, instead of adding risk, uncertainty and volatility due to the weakened balance sheet.

What now for EXPE?

In the current earnings call, the management also reported some softness in July's revenues, as clients are looking for lower price accommodation. The company expects to grow this year's bookings by around 5%, which is not impressive if it is going to be achieved by increasing advertising expenditure more than the revenues EXPE actually gets.

The stock is not expensive, but since the business is getting riskier by the bad capital allocation and balance sheet's overuse, it is easy to see the stock falling more than its competitors in a macroeconomic downturn and not performing well enough in the aftermath.

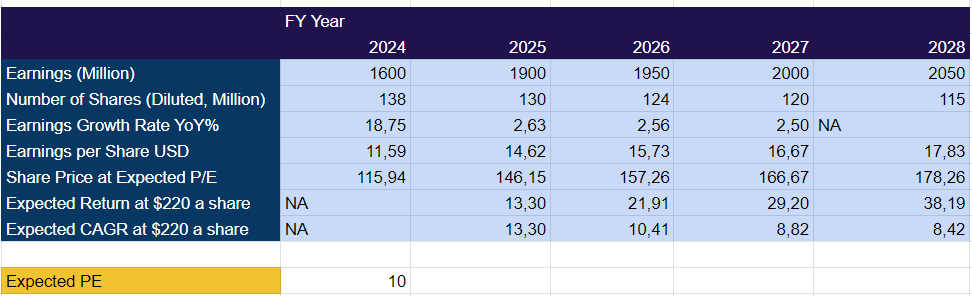

Valuation, upside and downside risks

From a valuation perspective, at this price, Expedia stock is not enticing for the risks the company is assuming. In this valuation framework, I am computing earnings estimates done by the analysts until 2025, which, frankly, might be too optimistic. In my opinion, numbers should be lower due to a lack of competitiveness, an increase in debt payments, and general low growth and cyclicality.

Using projected earnings and the company doing aggressive buybacks, the company might give up to an 8.4% CAGR, which is not impressive for the low quality of the business, the cyclicality, and the riskier balance sheet.

Image created by the author based on Annual Reports Projections (Author)

A buy case could be made, though, if numbers manage to climb higher than expected due to a strong macroeconomic environment and the balance sheet overleverage ends up paying off while the debt is less of a threat due to higher earnings. For this reason, at this low valuation and an economic environment that has shown relative resilience it is difficult to grade this stock as a sell.

Conclusion

Expedia is a second-class category business behind the leaders of Booking and Airbnb. This situation has meant a tangible disadvantage for the company's ability to grow and compete due to less available marketing spending. Additionally, the brand-new management is implementing risky financial strategies that are weakening EXPE's balance sheet. These measures could backfire quickly in a bad macroeconomic environment, as the balance sheet might suffer in the long term.

I consider this stock cannot be a buy if the management is taking these risky measures, but at this low valuation, still in a somewhat resilient economy, and with the significant buybacks, the stock is not a sell either; therefore, for me, it is an avoid or hold.