Morsa Images

Individual stock investing can be a highly rewarding endeavor, so long as one isn't always following the crowd on the flavor of the day. That's because looking for the right stock can be a "treasure hunting" experience, in the same way that a shopper goes to TJ Maxx (TJX) or Ross Stores (ROST) for quality at a value price.

To paraphrase the words of investor legend Peter Lynch, if you look at 10 different stocks, you might find one that's interesting. That's because it's a market for stocks rather than the stock market, and because every stock is different, it boils down to a game of numbers.

This means that the more stocks you reject, the closer you get to ones that may be a right fit for your portfolio. This brings me to Plymouth Industrial (NYSE:PLYM), which I believe is an under the radar REIT that flies below much better, well-known peers like Prologis (PLD).

I last covered PLYM in March, highlighting its strong portfolio fundamentals and undervaluation, especially compared to peers. It appears that the market has thus far agreed with my thesis, with the stock giving investors a 12% total return since then, far outstripping the 3% rise in the S&P 500 (SPY) over the same timeframe.

In this article, I revisit PLYM and discuss why it remains a highly attractive industrial REIT for income and potentially strong total returns from here, so let's get started!

Why PLYM?

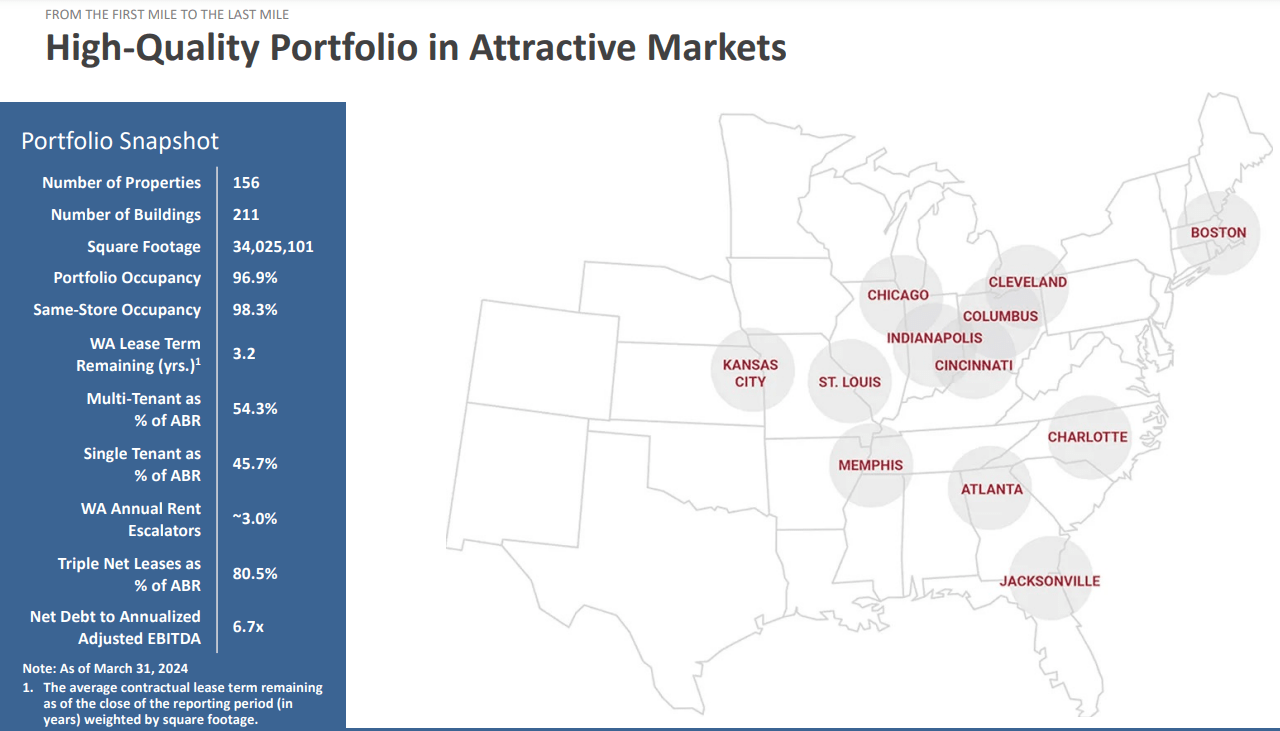

Plymouth Industrial is focused on owning and leasing out industrial properties in important secondary markets across the U.S. At present, it owns 156 properties that are 81% triple net leased.

PLYM's properties are strategically located in what it calls the "Golden Triangle", which signifies cities that are within one day's driving distance from 70% of the U.S. population. This region also includes more than half of the U.S. GDP.

As shown below, this includes cities across the Midwest like Indianapolis and Kansas City and Southeastern cities like Atlanta and Jacksonville.

Investor Presentation

PLYM continues to demonstrate strong fundamentals with Same Store Cash NOI rising by 9.7% YoY during Q2 2024. This was driven by strong leasing activity due to high demand for its properties, as reflected by 18.8% cash spread on new leases and 19.5% cash spread on renewal leases executed during the second quarter. Moreover, same store occupancy is very high at 98.2% and total occupancy including new developments now in service also stands high at 97.0%.

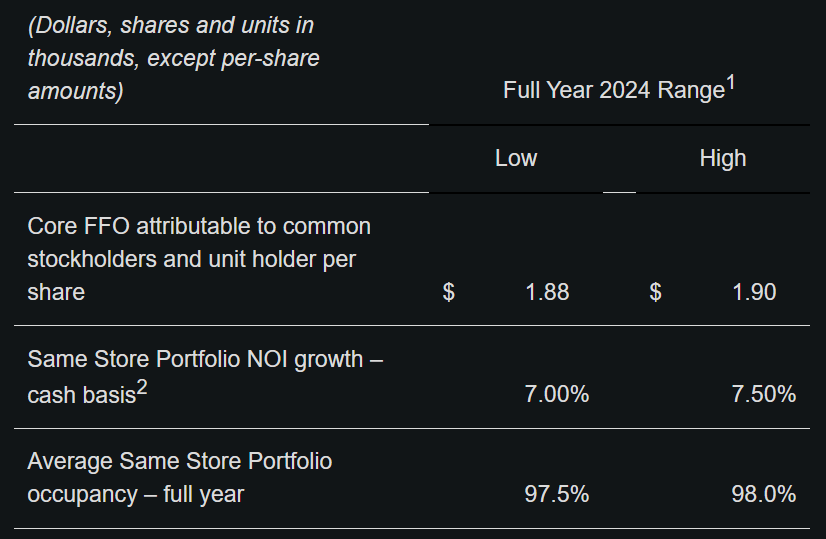

Management is being cautiously optimistic for the full year 2024, guiding for Core FFO per share of $1.89 at the midpoint of the range, representing potential 3% growth from $1.84 achieved in 2023. As shown below, this is driven by strong expected occupancy in the 97.5% to 98% range, and robust SS NOI growth of 7.25% at the midpoint of the range.

PLYM Financial Guidance (Q2'24 Earnings Release)

PLYM's continued growth is also predicated upon external acquisitions, including the one in Memphis during Q2, which management highlighted as being accretive to shareholders during the recent conference call:

The acquisition in Memphis is accretive and significantly expands our presence in this core market to almost 7 million square feet. This portfolio fits the Plymouth model perfectly. A strong initial NOI yield and the ability to realize the mark to market opportunities relatively quickly to drive returns higher.

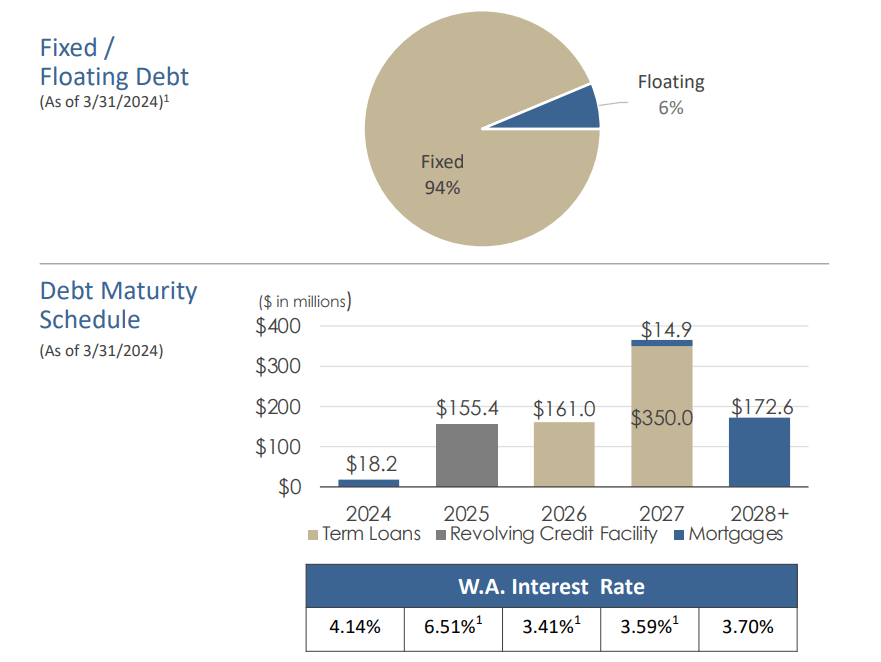

Risks to PLYM include potential for competition from new supply in its key markets should interest rates go down. Moreover, a 'hard landing' to the U.S. economy could result in tenants pulling back on their need for space. Moreover, PLYM carries slightly more leverage than I'd like, with a net debt to EBITDA ratio of 6.4x.

However, it's worth noting that PLYM has made good progress on improving its leverage, as the aforementioned ratio is down from 6.7x in the prior quarter. As shown below, 94% of PLYM's debt is held at a fixed rate, and it has just $18 million worth of debt maturities for the remainder of this year.

PLYM Debt Profile (Investor Presentation)

This lends support to the 4.0% dividend yield, which is well-covered by a 51% payout ratio, based on the aforementioned $1.89 Core FFO/share guidance for 2024.

Lastly, PLYM remains good value at the current price of $23.86 with a forward P/FFO of 12.6x. This sits far below that of its closest peer, STAG Industrial (STAG), which also invests in secondary markets and carries a P/FFO of 16.8x and far below that of Prologis's 22.9x P/FFO.

Sell side analysts who follow the company estimate 6-8% annual FFO per share growth over the next 2 years, which I believe is reasonable considering that the Fed is done with raising rates with the anticipation of a rate cut in September, which should ease pressure on debt refinancing for PLYM down the road. This also means that more of the rental lease spreads can flow to the bottom line for investors.

With a 4% dividend yield and mid to high-single digit annual FFO/share growth, PLYM could deliver market beating returns, and a growth in valuation to match closer to that of its peers provides an added potential growth kicker for investors.

Investor Takeaway

Plymouth Industrial presents an attractive investment opportunity flying under the radar with a strong portfolio, particularly in strategic secondary markets in the U.S.

PLYM is demonstrating impressive leasing activity, high occupancy rates, and steady NOI growth. Despite potential risks from market competition and economic downturns, PLYM's cautious leverage management, substantial fixed-rate debt, and attractive dividend yield underscore its financial health.

With a favorable valuation at a substantial discount to peers, well-covered dividend yield with plenty of retained capital, and promising growth outlook, PLYM stands poised for market-beating returns, making it a compelling choice for income and growth-focused investors.

Gen Alpha Teams Up With Income Builder

Gen Alpha has teamed up with Hoya Capital to launch the premier income-focused investing service on Seeking Alpha. Members receive complete early access to our articles along with exclusive income-focused model portfolios and a comprehensive suite of tools and models to help build sustainable portfolio income targeting premium dividend yields of up to 10%.

Whether your focus is High Yield or Dividend Growth, we’ve got you covered with actionable investment research focusing on real income-producing asset classes that offer potential diversification, monthly income, capital appreciation, and inflation hedging. Start A Free 2-Week Trial Today!