Hiroshi Watanabe

Investment overview

I give a buy rating for QuantumScape Corporation (NYSE:QS), as I see attractive upside in the stock if QS delivers its product as expected. So far, QS is making good progress on all fronts: R&D, manufacturing, and commercializing. The deal with PowerCo recently was also very positive, as it makes the QS balance sheet stronger and also reduces the CAPEX intensity of the business.

Business description

QS designs and manufactures solid-state (glass) lithium-ion batteries that are used in electric vehicles [EV]. The main value propositions are that these batteries are safer, can be charged faster, and have a higher energy density when compared to traditional batteries. As of 2Q24, QS is not making any revenue (still in R&D mode) and is still in cash burn mode. 2Q24 reported an operating loss of $134 million and an EBITDA loss of -$72.5 million, excluding stock-based compensation.

While the business is not generating meaningful revenue and profits today, I think the potential is huge if QS can deliver on what they promised. Progress so far has been promising, and I think patient investors will be able to reap the reward in due time.

Positive on licensing deal

QS

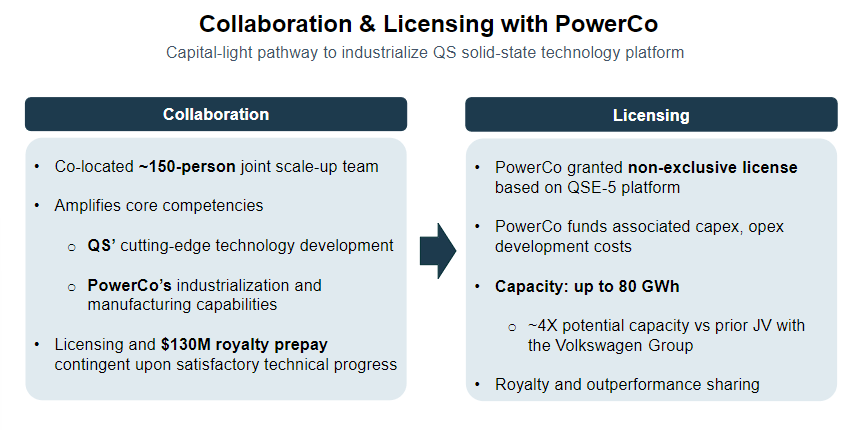

Earlier in June (11th July), QS announced a licensing deal with PowerCo (a subsidiary of Volkswagen). I am very positive about this on two fronts. Firstly, the deal includes a royalty pre-payment of $130 million and releases funds previously earmarked by QS for a JV. This eases the burden on the QS balance sheet and heavily extends the cash runway (more on this below). Secondly, it makes the QS operating model much more "asset-light", which means a high free cash flow profile over time as there are fewer capex needs and manufacturing costs.

R&D and manufacturing process on track

The most important part of the QS stock narrative is how well the R&D and manufacturing processes are doing, and encouragingly, they seem to be well on track.

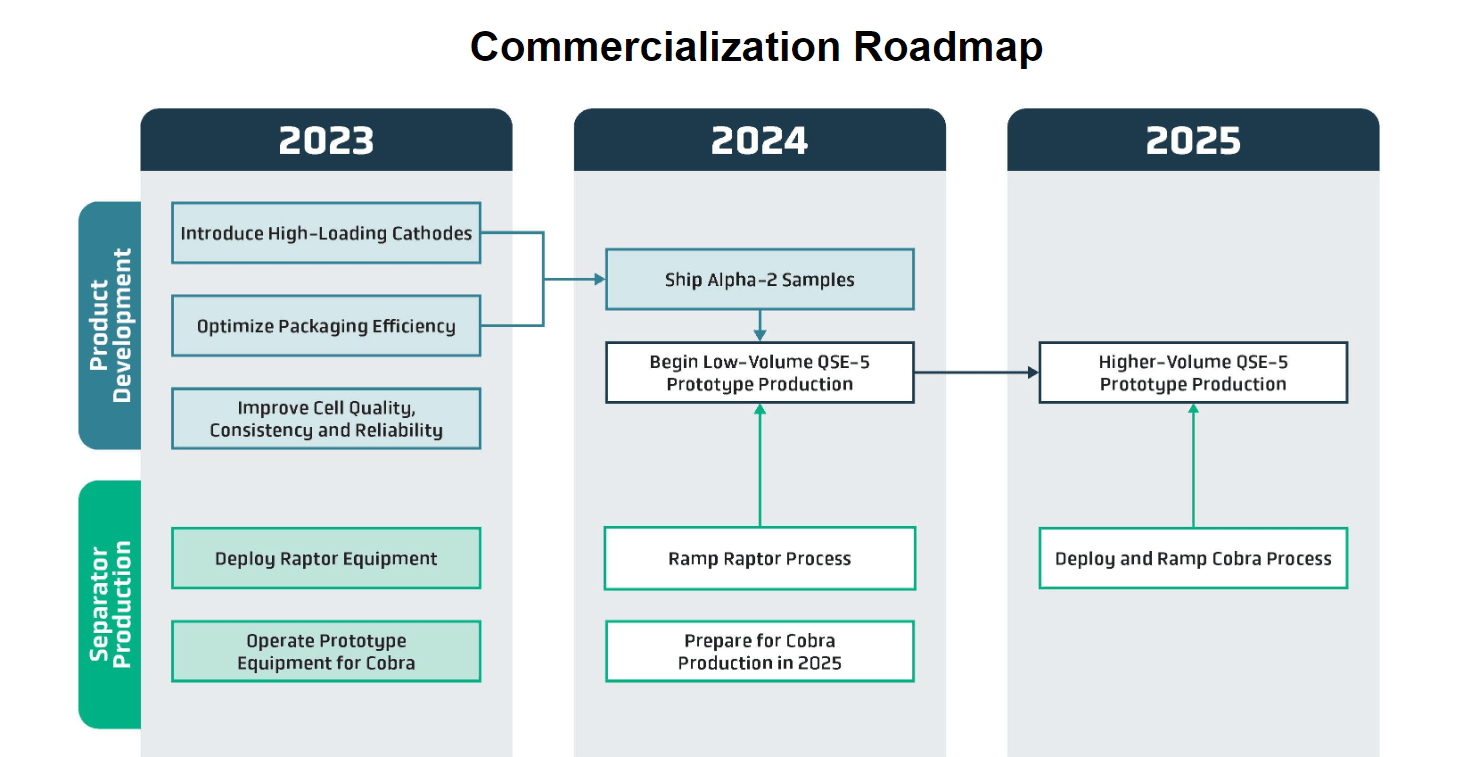

On R&D and commercial traction, QS commented that customer engagements remain robust and that it has shipped Alpha-2 prototypes to multiple customers in the automotive and consumer electronics sectors. This is promising because it lends credence to the product quality and reliability of the QS product, especially since it is still in prototype. One of my concerns with this battery technology (for EVs) is safety, especially in terms of battery fires. Positively, QS has shown good test results so far. Specifically, it was highlighted that the prototype cell testing demonstrated thermal stability up to 300 degrees Celsius. This is very good when considering that conventional high-energy lithium-ion cells burst into flames between 175 and 180 degrees.

QS

If this works out well, it sets up a positive outlook for QS's upcoming QSE-5 cell (this is the main commercial opportunity). I am not expecting any major hiccups here, as the deal with PowerCo includes creating a dedicated and co-located team of experts from both companies that will collaborate to industrialize the battery technology.

QS

On the manufacturing side, things are promising too. Progress so far certainly gives more confidence in Cobra (QS's next-gen process to mass produce QSE-5). The only trackable metric/progress now is the ramp up in Raptor (you can think of this as the lite version of Cobra). If Raptor progresses well, it should also mean that Cobra will work out well too. I take comfort in knowing that QS has finished ramping up on Raptor and that it is able to allocate more resources to the development of Cobra. This tells us two things. Firstly, results from Raptor must have been promising (QS uses Raptor as a testbed for Cobra). Secondly, QS is one step closer to meeting its 2025 target by ramping up Cobra for mass production.

The upcoming key milestone to track is whether Raptor can successfully produce a B-sample product by the end of 2024. This will send a strong message to the market that Cobra is likely to work out well. Note that Cobra is a core component of the tech platform that PowerCo will be licensing.

Balance sheet enough capacity to sustain investments

QS

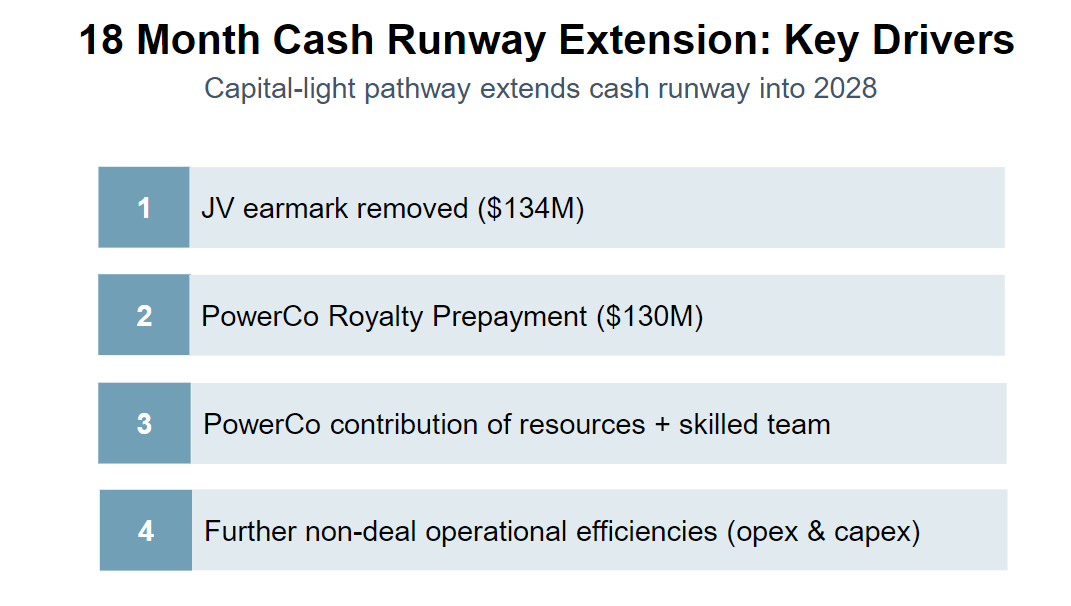

The big question mark is whether QS has sufficient cash to last until it starts generating meaningful revenue. Based on my math (and also management's estimates), QS should have no problems lasting long enough. As of 2Q24, QS has total cash and cash equivalents of ~$940 million and no debt (operating lease liabilities are $55.6 million, but not meaningful). Since the deal with PowerCo was announced in July, it means that $264 million is not included in the 2Q24 balance sheet. Total cash and cash equivalents should be around $1.2 billion.

Current EBITDA guidance calls for FY24 adj EBITDA (excluding SBC) to be between -$250 and -$300 million and CAPEX for FY24 to be between $70 and $120 million, but with the expectation that it will come at the lower end of the range. This sums up to around ~$320 million. With the current cash balance, QS should be able to last close to 4 years before it needs to raise capital (call it mid-2028). Readers should also be reminded that this deal makes QS less OPEX and CAPEX intensive, so the cash burn rate should taper down gradually.

Valuation

QS

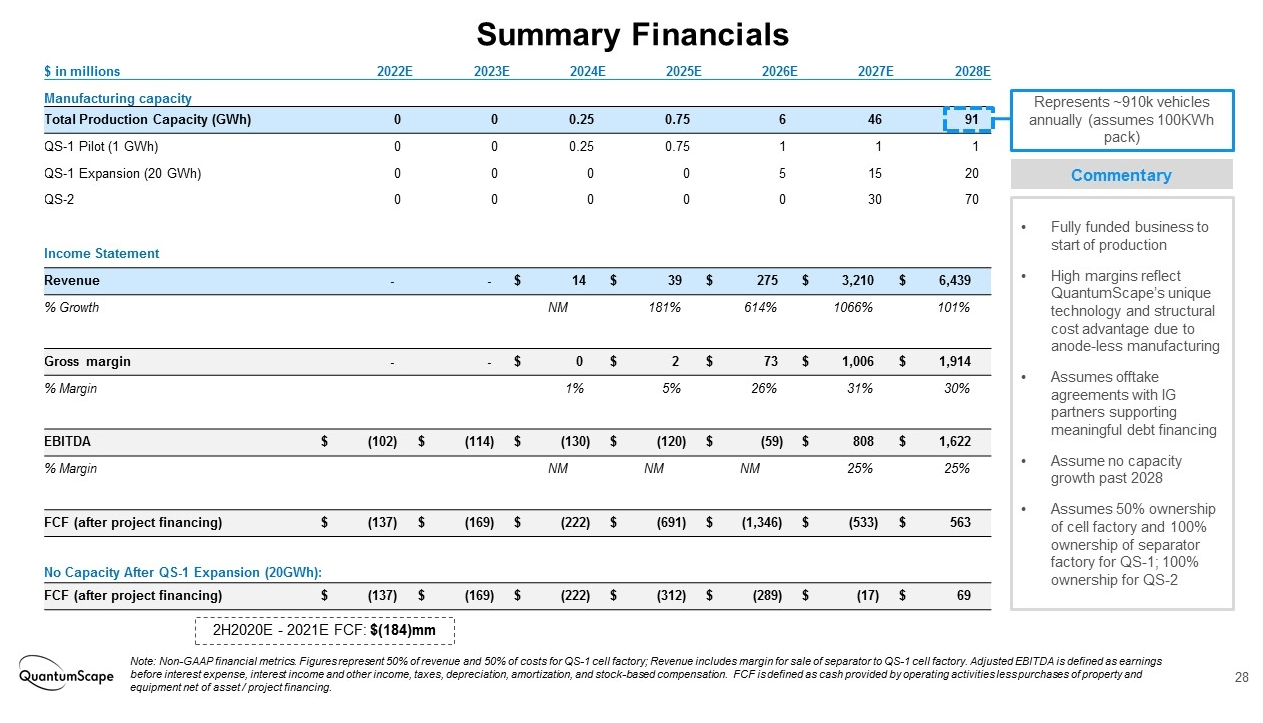

Given that QS is still in the R&D phase, forecasting the business is tough given the lack of historical precedent. Rather than plucking numbers from the sky and inputting them into Excel, I think a better way is to benchmark current performance against management's initial expectations. In the SPAC presentation, the expectation is for QS to start generating revenue in FY24 and turn EBITDA positive in FY27. As of 2Q24, QS is still not generating any revenue, and I think it's safe to say this is not going to be the year as Cobra is only expected to start high-volume production in FY25. This means that QS is about 2 years behind expectations.

May Investing Ideas

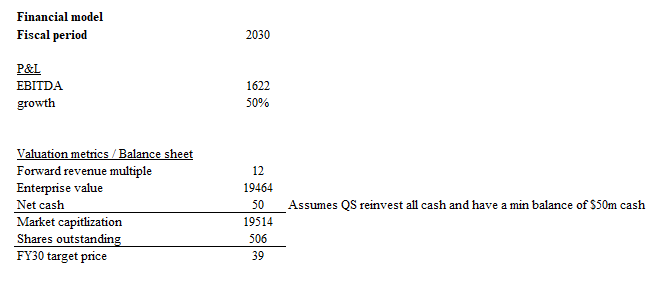

Assuming QS only achieves its ~$1.6 billion EBITDA target in 2030 and the stock trades at ~12x forward EBITDA (this is S&P 10-year average multiple), Given that QS is still growing, it should minimally trade at market level. QS is worth an enterprise value of ~$19.5 billion, or FY30 share price of ~$39. Note that the $50 million won't swing the target price by a lot, but logically, it should go down from here since FCF after project financing only turns positive in the same year QS generates $1.6 billion of EBITDA.

Risk

There are no guarantees that QS will be able to deliver the product successfully as expected. If the product doesn't work out as well as it should, the entire investment thesis for QS will be challenged, and the equity value will take a strong hit. This is the biggest risk for QS, and it's a risk that one has to take when investing in such a business.

Conclusion

I give a buy rating for QS as the upside is attractive. There is promising progress made on multiple fronts, including R&D, commercialization, and manufacturing, which gives confidence that QS can start to generate revenue soon. The recent licensing deal with PowerCo has also strengthened the company's balance sheet and reduced its CAPEX intensity. The risk is that QS fails to deliver, and this is something that investors must be comfortable with when investing in the stock.