Saranya Yuenyong

DLocal Limited (NASDAQ:DLO), the payment processor focused on emerging markets, has reported continued payment volume growth but increasingly weak margins, especially leaving investors pessimistic after the Q1 report that showed thinning results.

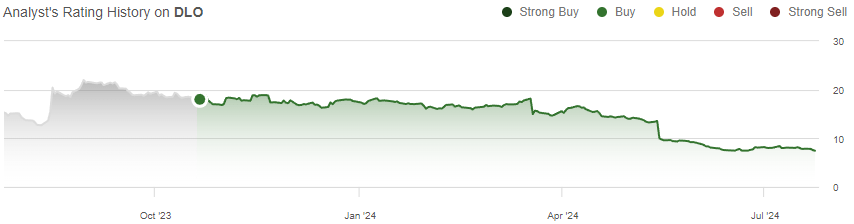

After my previous article on the company, titled “DLocal: Hypergrowth Leaves Room For Stock Appreciation”, the stock has lost -59% of its value compared to S&P 500’s return of 29% - the article’s Buy rating has so far aged incredibly poorly as DLocal’s take rates have recently crashed creating thinning margins. Upon revisit, the stock seems increasingly cheap, but shareholders should remain extremely cautious as risks have risen regarding DLocal’s future take rates, affecting the margin level.

My Rating History on DLO (Seeking Alpha)

Payment Volumes Have Kept on Growing

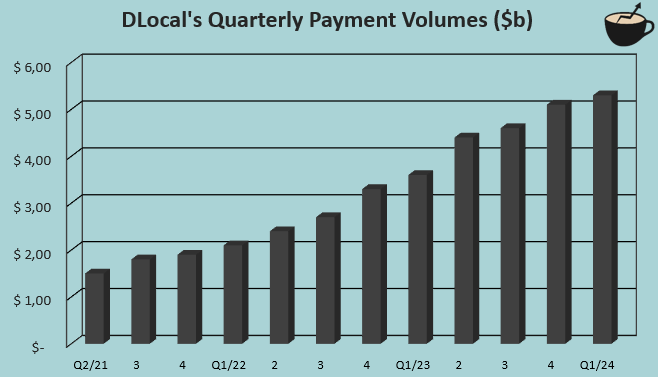

DLocal has continued growing the payment volumes on the platform from my previous article, with Q1 reaching payment volumes of $5.3 billion. Revenues have also continued growing, latest by 34.3% in Q1 driven by great growth in Brazil, Mexico, and Egypt, but countered by revenue declines in the risky Argentinian market and Nigeria.

Author's Calculation Using TIKR Data

Revenues should continue to grow well with drivers a new partnership in Africa with Ebury among continued growth with current partnerships – the long-term volume growth thesis should stand the same despite considerable weakness in certain markets.

The Lower Take Rate Is a Significant Problem

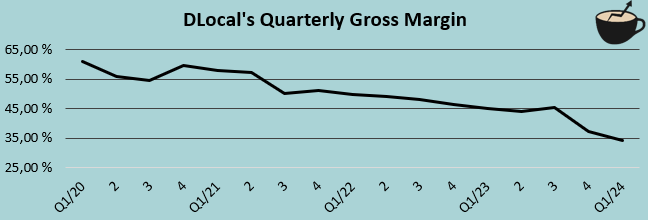

While DLocal’s gross margins have already seen pressure from lower take rates historically, the Q4 and Q1 results took an increasingly large hit into just a gross margin of 34.1% in Q1, leading to the very large sell-off of the stock in past months. As a result of the lower gross margin level, the operating margin only stood at 14.6% in the latest quarter, at around a half of the long-term level as SG&A continued to scale with larger operations.

Author's Calculation Using TIKR Data

The company has noted the very weak financial performance in Q1, and relates the weakness to several factors including a large merchant reaching a lower-priced tier in DLocal’s scheme lowering the take rate along with re-negotiated fees, seasonal pay-in weakness, delays in merchant launches, and the weakness in Argentinian business.

I believe that the Argentinian weakness explains a part of the weakness - investing in emerging markets is known to come with notable risks that have realized in the country. Still, the more critical underlying question remains around DLocal’s future take rates – the profitability was already immensely pressured in Q1 from lower gross margins, and future declines could weaken the investment case further.

DLocal had a take rate of around 3.5% in Q1, compared to StoneCo’s (STNE) 2.7% in the quarter, PagSeguro’s (PAGS) 3.9%, and Nuvei’s (NVEI) just 0.6% - compared to the two first peers with a relatively comparative performance and business, DLocal currently seems to have a sustainable take rate. Yet, as the companies’ served markets and supported transaction types’ volumes differ very largely resulting in different take rates, a very different take rate profile is likely sustainable between the companies, and investors shouldn't necessarily anchor expectations to other companies.

DLocal’s future take rate should be watched with skepticism, as the KPI is critical for DLocal to generate its typically high margins. The weakness has been related to a number of temporary measures including the large merchant’s renegotiation and higher proportional local-to-local volumes, but I take the effects’ temporality with caution. Growing clients’ lower-priced tiers are likely to pressure the level further in upcoming quarters and years, but the level of the decreases is still unknown.

Looking Ahead at Q2 And Beyond

The company has a 2024 outlook including $25-27 billion in payment volumes, $320-360 million in gross profit, and $220-260 million in adjusted EBITDA, and DLocal still communicated to expect to hit the guidance’s lower bound in 2024 after the weak Q1.

Especially the gross profit outlook is in my opinion critical, and investors should watch the outlook with skepticism – while gross profit improved by just 1.8% in Q1, the company guides for an expansion of at least 15.6% in 2024, expecting quite dramatic sequential improvements.

DLocal is going to report the company’s Q2 results on the 14th of August in post-market hours, and I believe that sequential improvements start to become critical with DLocal’s expectation of greater 2024 gross profits. Wall Street analysts currently expect revenues of $203.1 million and an EPS of $0.10, corresponding to revenue growth of 26.1% but an EPS decline of $0.05 year-on-year.

The Stock Is Incredibly Cheap, But Beware of Risks

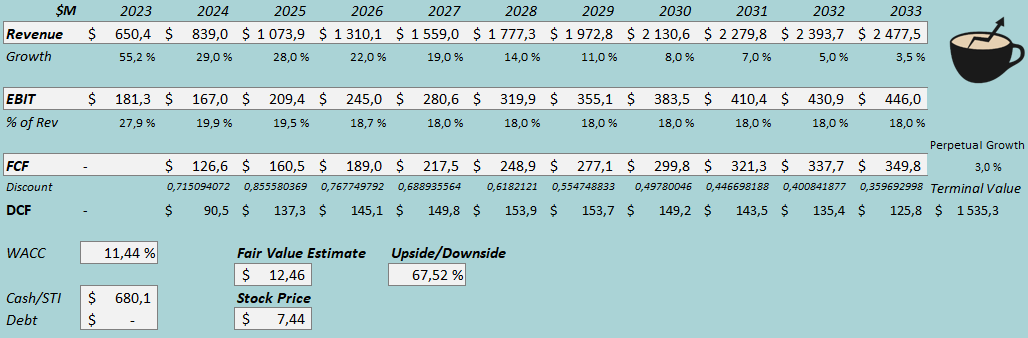

I updated my discounted cash flow [DCF] model. In the model, I now estimate growth of 29% in 2024, followed by 28% in 2025 and a sequential growth slowdown into 3% perpetual growth – I believe that the CAGR of 14.3% from 2023 to 2033 represents a fair assumption with DLocal’s continued momentum.

With potential further take rate declines, the margin outlook has worsened considerably from my prior estimates. I now estimate the EBIT margin to be pushed back into just 18.0% instead of my previous 31.0% estimate. The estimate still comes with a caveat, as DLocal guides for a significantly better performance especially in 2024 in terms of the gross profit growth, but even larger declines are still very much possible due to the dramatic nature of the Q1 decline.

DLocal should still have a good cash flow conversion, but I have adjusted the conversion from EBIT downwards due to higher recent tax rates paid.

DCF Model (Author's Calculation)

The estimates put DLocal’s fair value estimate at $12.46, 68% above the stock price at the time of writing. With the recent weakness in stock price, the investment is still attractive if the profitability can be kept at a reasonable level, posing great upside.

The valuation comes with very large downside risks due to the risky nature of especially the margin level, though.

CAPM

A weighted average cost of capital of 11.44% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author's Calculation)

I now estimate no long-term debt for DLocal with the company’s remaining strong balance sheet. To estimate the cost of equity, I use the 10-year bond yield of 4.26% as the risk-free rate. I previously used the United States’ equity risk premium, but I believe that the company’s target markets’ equity risk premium is more accurate instead – I now use Brazil’s, Mexico’s, and Nigeria’s average equity risk premium of 9.17, estimated by Aswath Damodaran in July. Yahoo Finance now estimates the beta at 0.75. With a liquidity premium of 0.3%, the cost of equity and WACC both stand at 11.44%.

The Risk Level Is Extremely Elevated

As mentioned, the take rate is an especially large risk in the investment case, as the weak Q1 performance has demonstrated. Especially the short-term future should show DLocal’s margin potential better, and the Q2 report could come with an another profitability weakening leading to an even weaker performance.

The company’s presence mainly in developing countries is also a risk, as the Argentinian operations have shown. I still believe that the growth momentum should stand strong despite some markets’ weakness, but the risk should be noted – DLocal comes with extremely elevated risks especially in the short term, and while I am still optimistic of the valuation, the potential of further losses from the current level can’t be completely written off.

Takeaway

DLocal’s margins have deteriorated especially in Q1, making the stock perform incredibly poorly after my previous bullish article on the stock. While underlying payment volumes continue growing incredibly well, the margin level now poses a large risk to investors especially in the short term with DLocal still guiding for improvements in 2024 that should be taken with skepticism. The valuation has become attractive even with lower margins, and as such, I remain with a cautious Buy rating.

Still, I now note the increasingly rising risk level with DLocal’s take rate level and overall margins, and the company’s geographical risk that has already pushed earnings down in Argentina – investors should note the very notable possibility of further stock declines if earnings improvements don’t happen throughout 2024, potentially breaking my remaining bullish view.