cemagraphics

Introduction

I've been following Gogoro (NASDAQ:GGR) closely, and I've written a total of five articles about the company on SA to date. The latest one came out in February 2024 and back then I said that its expansion beyond Taiwan had been underwhelming.

On May 9, Gogoro released its Q1 2024 financial results and I think they were weak as hardware and other sales slumped by over 20% year-on-year while a vehicle recall and battery upgrades slashed the gross margin in half. The company is launching two new smartscooter models, but I doubt that this is enough to turn the business around, and I'm keeping my rating on Gogoro's stock at sell despite the 26.8% decrease in the market valuation since my previous article. Let's review.

The Q1 2024 financial results

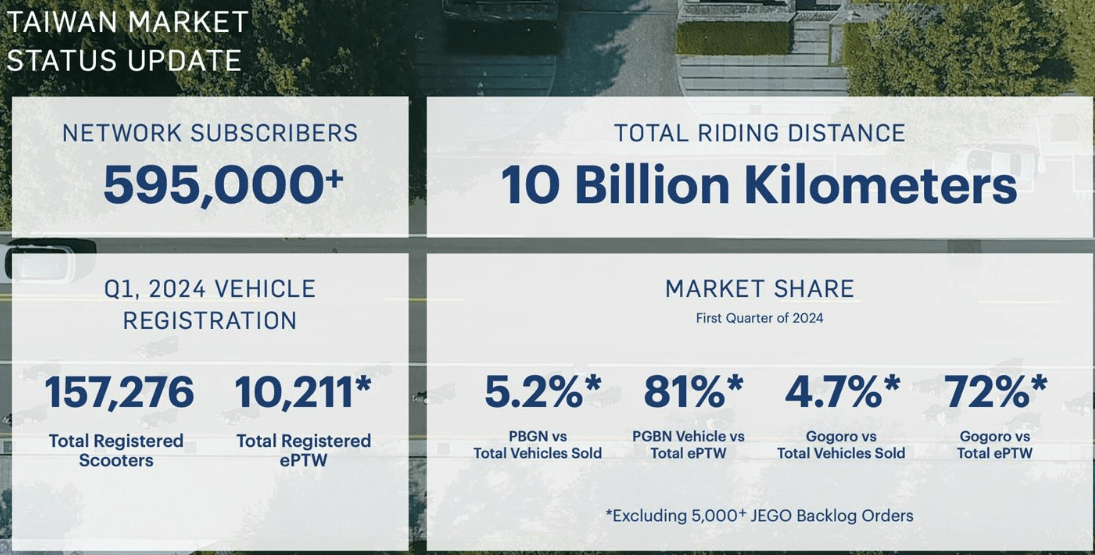

In case you are unfamiliar with Gogoro or my earlier coverage, here's a brief description of the business. The company has a network of battery swapping stations for electric scooters throughout Taiwan and also sells vehicles. In addition, Gogoro is involved in electric scooter rental through GoShare. As of March 2024, the company's battery swapping service had more than 595,000 subscribers, which makes it a monopoly in Taiwan.

Gogoro

In January 2024, Gogoro announced that it planned to enter Chile and Colombia in the second quarter of the year, but I'm skeptical about the company's growth plans considering it has failed to make inroads in Europe and Asia to date despite plans to do so for several years.

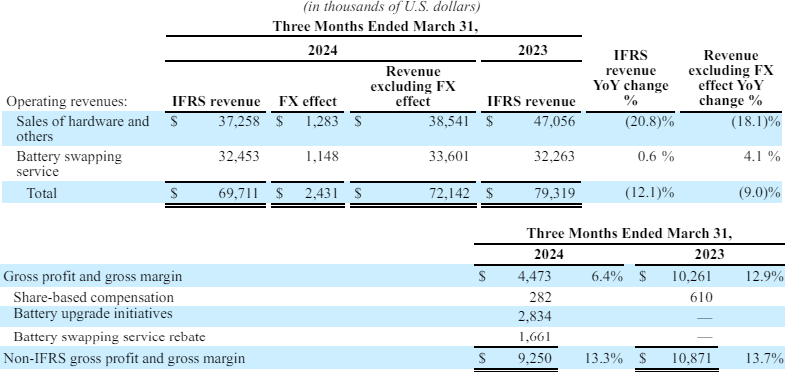

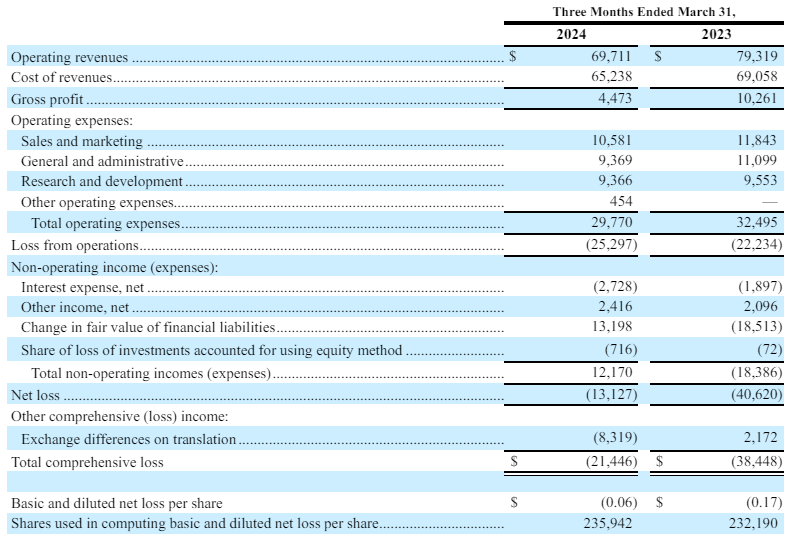

Turning our attention to the Q1 2024 financial results, we can see that it was a challenging quarter for Gogoro as operating revenues went down by 12.1% year-on-year to $69.7 million while the gross margin slumped to 6.4% from 12.9% a year earlier. The battery swapping service revenue inched up by 0.6% to $32.5 million, despite a 10.6% jump in subscribers as a result of rebates to some customers due to a vehicle recall and battery upgrades. Sales of hardware and other revenues, in turn, decreased by 20.8% to $37.2 million due to a slowing scooter market in Taiwan. Considering the registrations of powered two-wheelers (PTWs) for the island went down by 11.2% while the registrations of electric PTWs crashed by 39%, I think that Gogoro performed reasonably well during the quarter. In addition, the gross margin was above 13% if we exclude rebates and battery upgrades as Gogoro continued to cut SG&A and R&A costs in a bid to improve margins. Adjusted EBITDA was $9 million for Q1 2024 compared to $10.6 million a year earlier. On a negative note, interest expenses soared by 43.8% year-on-year to $2.7 million due to higher interest rates.

Gogoro

Gogoro

Looking at the balance sheet, I'm concerned that the net cash position shrank to $48.6 million from $98.3 million in December 2023. Operating cash flow for Q1 2024 was just $0.9 million, while CAPEX came in at $34.4 million. The tangible book value was down to $230.6 million from $248.7 million a quarter earlier.

Future of the company

I expect Gogoro's scooter sales to return to growth in either Q2 or Q3 2024 as the company is launching two new models of smartscooters - the high-tech performance Pulse and the entry-level Jego. The latter has a manufacturer's suggested retail price (MSRP) of about $1,800 and had attracted over 6,500 fully paid preorders by late April when shipping began. Pulse, in turn, has an MSRP of about $3,500, but I can't find information about the number of pre-orders. Gogoro still expects to generate revenues of between $385 million and $420 million in 2024, and I think this looks achievable as the scooter market in Taiwan should improve over the coming months. According to Gogoro (page 2 here), the two biggest PTW makers in Taiwan expect the local market to decline by 14% to around 750,000 units in 2024, which suggests that we are unlikely to see a recovery anytime soon. However, Gogoro foresees a growth in the local electric scooter market for 2024 thanks to its new models as well as the transition from internal combustion engine vehicles to electric ones.

Valuation

Assuming Gogoro manages to meet its 2024 revenue guidance and the adjusted EBITDA margin stands at about 13%, the company should generate adjusted EBITDA of between $50.1 million and $54.7 million for the year. This translates into a forward EV/adjusted EBITDA multiple of between 5.8x and 6.3x. While this level doesn't seem high for a growing company, I'm concerned that there are a lot of positive developments baked into the numbers for the second half of 2024. It's possible that Taiwan's scooter market decline further in the coming months, or that electric scooters gain market share slower than expected. In addition, Gogoro looks overvalued based on several other key financial indicators. The company is still in the red, FCF is nowhere near positive territory, and the price to book value ratio is close to 1.6x. The momentum for the stock price still seems negative, and I think that it could fall below the $1.00 mark by the end of 2024.

I continue to think that short selling seems viable here, as data from Fintel shows that the short borrow fee rate is 6.45% as of the time of writing. However, opportunities to hedge the risk through call options are limited, as the only available strike price is $2.50. In addition, the short squeeze might be high right now. While the short interest is only 1.39% of the float, it currently takes more than 15 days to cover. In view of this, it could be best for risk-averse investors to avoid Gogoro's stock.

Turning our attention to the upside risks, I think the major one is that I could be underestimating Gogoro's short-term prospects. If Taiwan's scooter market recovers faster than expected and the company manages to boost its share of the pie through strong order for Pulse and Jego, the stock could gain significant momentum. Another risk here is that the market valuations of microcap companies can soar for spurious and unknown reasons.

Investor takeaway

Gogoro booked underwhelming financial results for Q1 2024 due to a weak scooter market in Taiwan as well as a vehicle recall and battery upgrades. In my view, Q2 and Q3 should be stronger thanks to the start of sales of Pulse and Jego. That being said, I expect Gogoro to remain in the red over the next few quarters and FCF to continue to be negative. While short selling seems viable due to the relatively low short borrow fee rate, the short squeeze risk is significant here, and I think risk-averse investors should avoid Gogoro's stock.

If you like this article, consider joining Microcap Review. I post my portfolio and shortlist there, and you can also find exclusive ideas from our community of investors. I like to focus on undervalued companies that the market is ignoring, like an island of misfit toys.