Nadzeya Haroshka/iStock via Getty Images

Investment thesis

PROS Holdings (NYSE:PRO) leverages AI to provide pricing optimisations for its clients. As more companies are driven towards using AI to improve and optimize their operations, PROS provides an effective way for its clients to improve their pricing strategies and thereby increase their sales and profitability. The PROS offering, originally developed for airlines' ticket pricing, has since been adopted across various industries for B2B sales applications.

The company has shown solid revenue growth in recent quarters and sequential margin improvements, thus demonstrating the inherent scalability of its business model. It is expected to generate solid FCF this year and I argue that the current valuation leaves room for plenty of upside, especially if management is able to meet its 2026 target of becoming a rule of 40 company. Additionally, given its promising growth outlook and rising margins, I rate PROS shares as a Buy.

Business highlights and financial snapshot

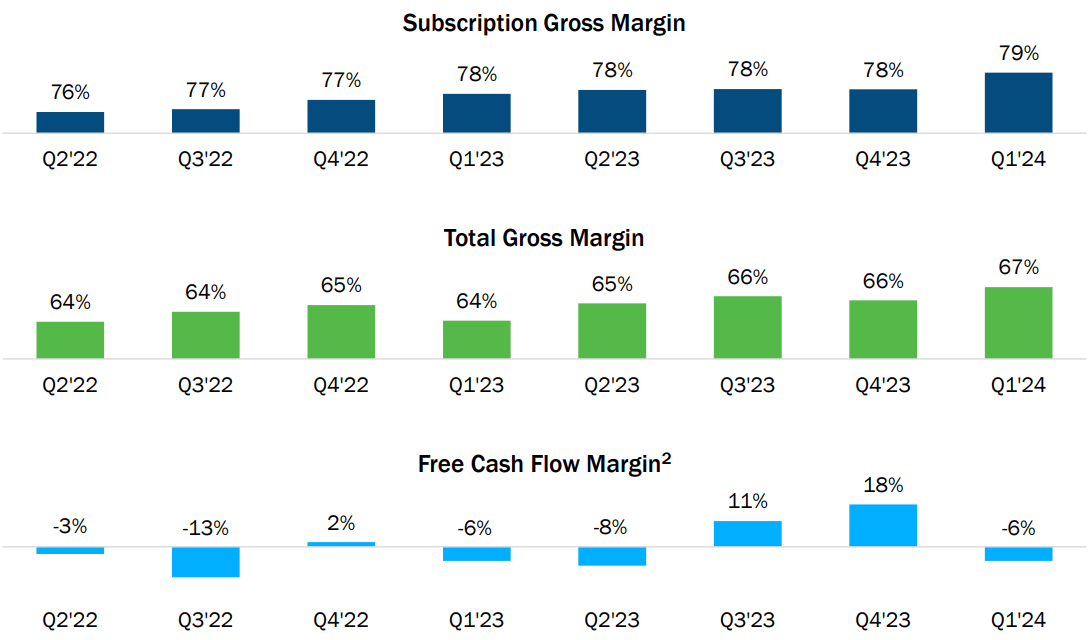

Total revenue was up 10% year over year in Q1, propelled by a strong 15% growth in subscription revenue. Profitability was impressive with solid margin improvements in all relevant metrics as shown below.

Q1 Investor Presentation

The highlights from the quarter included significant customer wins and a new partnership. On the earnings call, the company's CEO mentioned the signing of Les Schwab as a customer and touted PROS's dynamic pricing algorithm as being the main driver for the win when he stated:

I would say, look, the adoption of dynamic pricing algorithm, especially for the B2B industries, which is over $30 billion of the TAM opportunity, is huge. I mean the adoption is still low. And it’s a great example to have Les Schwab, for example, this quarter. That’s one of the very important criteria in them selecting PROS is really to power their over 500 retail stores with real-time pricing. So we see this use case applying very broadly in the B2B space.

The company also entered into a partnership with Microsoft (MSFT) whereby the PROS price quote would be directly integrated into Microsoft 365. Its CEO outlined the significance of the partnership with and the advantage of now being a part of the Salesforce (CRM) ecosystem saying:

I think both Microsoft and PROS are very proud of this innovation. This is just the beginning, but it definitely will increase visibility within the Microsoft ecosystem. And we’re very focused from a go-to-market on how we’re going to amplify that visibility. One of the transformative areas of the Sales Copilot that’s unique -- and I think it’s been very clever on the Microsoft side -- is this technology can integrate with any CRM. So not just the Microsoft ecosystem but also the Salesforce ecosystem because you can plug in Sales Copilot on top of both salesforce and Microsoft.

Expectations for the upcoming quarters

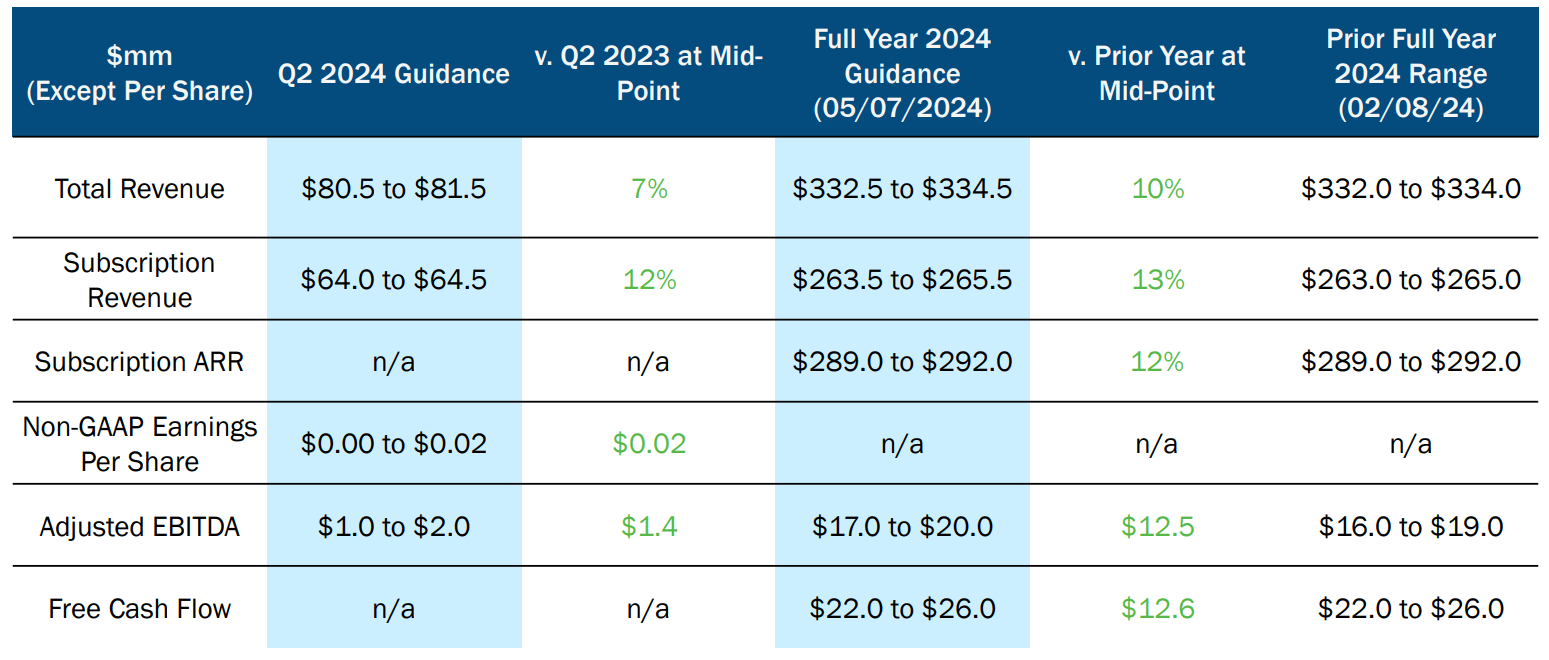

Earnings guidance

Q1 Investor Presentation

The company's management has guided to just a 7% year-over-year growth in total revenue Q2 as shown above. The sequential deceleration was explained by management as being due to the timing of revenue recognition between Q1 and Q2. When comparing guidance for H2 2024 versus the same period in the prior year, we see that total revenue growth expected is approximately 11%, which is solid when compared to the 10% growth seen in Q1. Notably, FCF is expected to be strong at around $24 million, reflecting a FCF margin of 7.3%. Stock-based compensation is expected to decline slightly to around 13% of revenue this year.

Considering management's history of guiding conservatively, I wouldn't be surprised if the company comfortably exceeds the guidance given. Furthermore, the company's CFO commented on his confidence in the guidance stating:

Our visibility is improved to the degree that I can actually comment and say, we expect to see a meaningful bump up in services revenue in the second half of the year. I can also say that similarly on the subscription side, we have a better idea of what Q3 is going to look like given the bookings that we’ve had in Q1.

What investors should look for

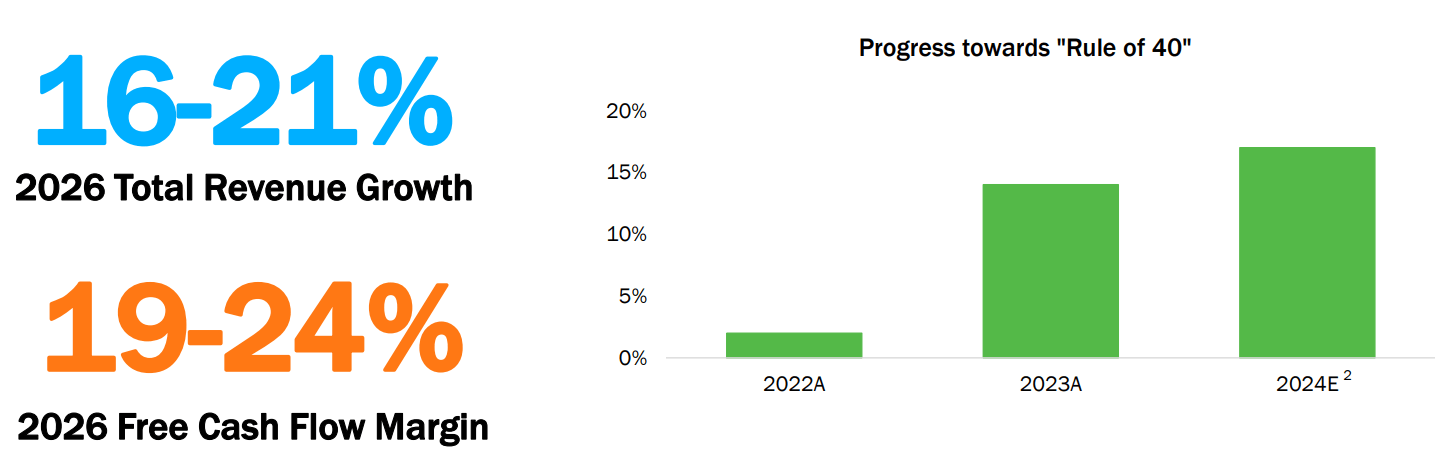

The crux of the investment thesis is the company's ability to reach the 2026 financial targets set by the management team. Therefore, investors need to track the progress towards these targets every quarter. A key factor that will drive growth in the business is upselling new products to its existing customers through a product-led growth strategy. The company plans to sell multiple offerings from its platform through a marketplace that customers can easily activate. This scalable business model is expected to enhance revenue growth and substantially improve profitability, advancing towards the 2026 targets for revenue growth and FCF margins outlined below.

Q1 Investor presentation

Investors should also monitor the company's gross revenue retention, which has remained strong at close to 93% in recent quarters. This metric should increase as more customers adopt multiple offerings and the platform becomes stickier. Moreover, the company's partnership with Microsoft could help in significantly boosting the company's sales productivity and therefore investors should watch for any further commentary from management regarding this in upcoming earnings calls.

Valuation

According to management's guidance, adjusted EBITDA for FY24 is expected to be $18.5 million at the midpoint. At today's share price of $25 and considering the company's net debt position of around $140 million, it has an enterprise value of $1.32 billion, based on 47 million shares outstanding. Shares therefore currently trade at an EV to adjusted EBITDA multiple of 71. Similarly, based on the midpoint of management's FCF guidance for FY24, shares trade at a Price to FCF multiple of 49.

Since the company is still in the early stages of improving its margin profile, I believe the valuation metrics based on this year's estimates tend to underestimate the true earnings power of the business. I therefore chose to value the business based on a hypothetical scenario where management is able to meet their 2026 FCF margin targets in FY24 itself. Based on FY24 revenue guidance of $333.5 million, FCF would end up close to $67 million when calculated assuming FCF margins of 20% which is roughly where management aims to reach by 2026. In this scenario, shares are valued at a Price to FCF multiple of 17.5.

I find the company's valuation appealing due to its promising growth prospects, potential for margin expansion and significant market opportunity. This attractiveness is further highlighted when compared to the valuation of other B2B SaaS companies providing AI-based data analytics solutions, such as Riskified (RSKD) and Amplitude (AMPL).

Risks

In my view, the primary risk for investors in the company stems from competitive pressures. Specifically, Salesforce's CPQ offering poses a significant threat, while Sabre (SABR) and Amadeus (OTCPK:AMADF) have competitive offerings for the travel space in particular. Understanding PROS's competitive advantage over its rivals is challenging, although it stands out for offering a more integrated platform solution.

The company is vulnerable to macroeconomic headwinds, notably due to its substantial revenue concentration in the travel segment. Additionally, there is potential regulatory risk, highlighted by the recent FTC scrutiny of AI-based pricing practices among several companies, including PROS.

Buy PROS Holdings

Despite certain identified risks, I consider the shares a Buy due to the attractive valuation and the promising outlook for sustained growth and improving profitability. The company is well-positioned to benefit from ongoing AI tailwinds.