aapsky

Investment thesis

Redwire (NYSE:RDW) has experienced strong momentum in securing space contracts, leading to a 52% increase in its Q1 revenue. However gross margins have declined sharply and hampered overall profitability. Despite management's guidance calling for a deceleration in revenue growth for the remaining quarters, future growth should remain strong due to the company's solid backlog and recent contract wins. I believe shares are fairly valued at 35 times EV to adjusted EBITDA. Although the growth prospects are attractive, the risks from dilution and weak margins lead me to assign a neutral rating.

Q1 earnings snapshot

Q1 earnings presentation

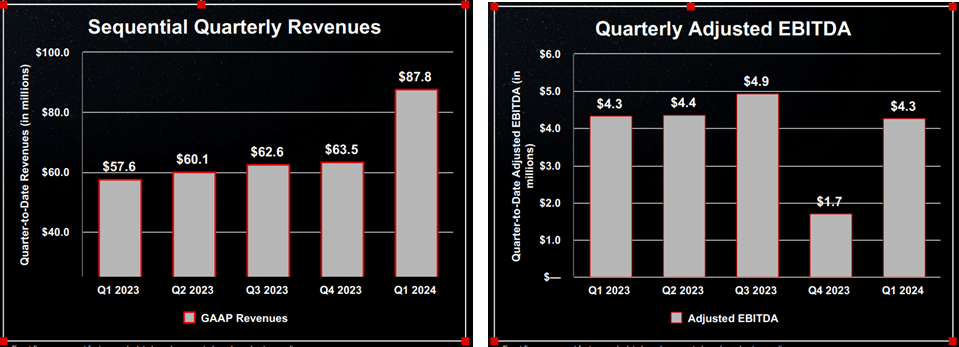

The company reported a 52% increase in Q1 revenue versus the prior year period, as shown above. This was driven by the 19% growth in its contracted backlog that the company achieved during 2023, which included large long-lead purchases that were fulfilled during Q1. Despite the strong revenue growth, adjusted EBITDA was only in-line with Q1 2023. The main reason behind this was the decline in gross margins to 16.8% versus 24.6% in Q1 2023. Management pointed out that gross profit was impacted by Estimate at Completion (EAC) adjustments which amounted to $3.9 million. Backing out this impact, gross margins would have ended up at 21.2%. When questioned during the Q1 earnings call about the future impact of EACs on gross margins, the company's CFO stated:

As far as the gross margins are concerned. On the EACs, we are driving towards low volatility, right? We don't want to see this level of EAC on an absolute basis, but it's really looked at on an LTM basis, not on a quarterly basis. You could see a movement up, but we are really trying to drive towards what great program management looks like, which is zero EACs.

Though he doesn't seem to expect the volatility in EACs to completely go away, he does emphasize that its impact will be reduced when viewing gross margins over a period of four quarters. Nonetheless looking ahead, management's guidance points to 23% growth expected in 2024 versus 2023. Following 52% growth in Q1, the guidance implies a significant deceleration in revenue growth for the remaining quarters.

Solid backlog and significant recent contract wins

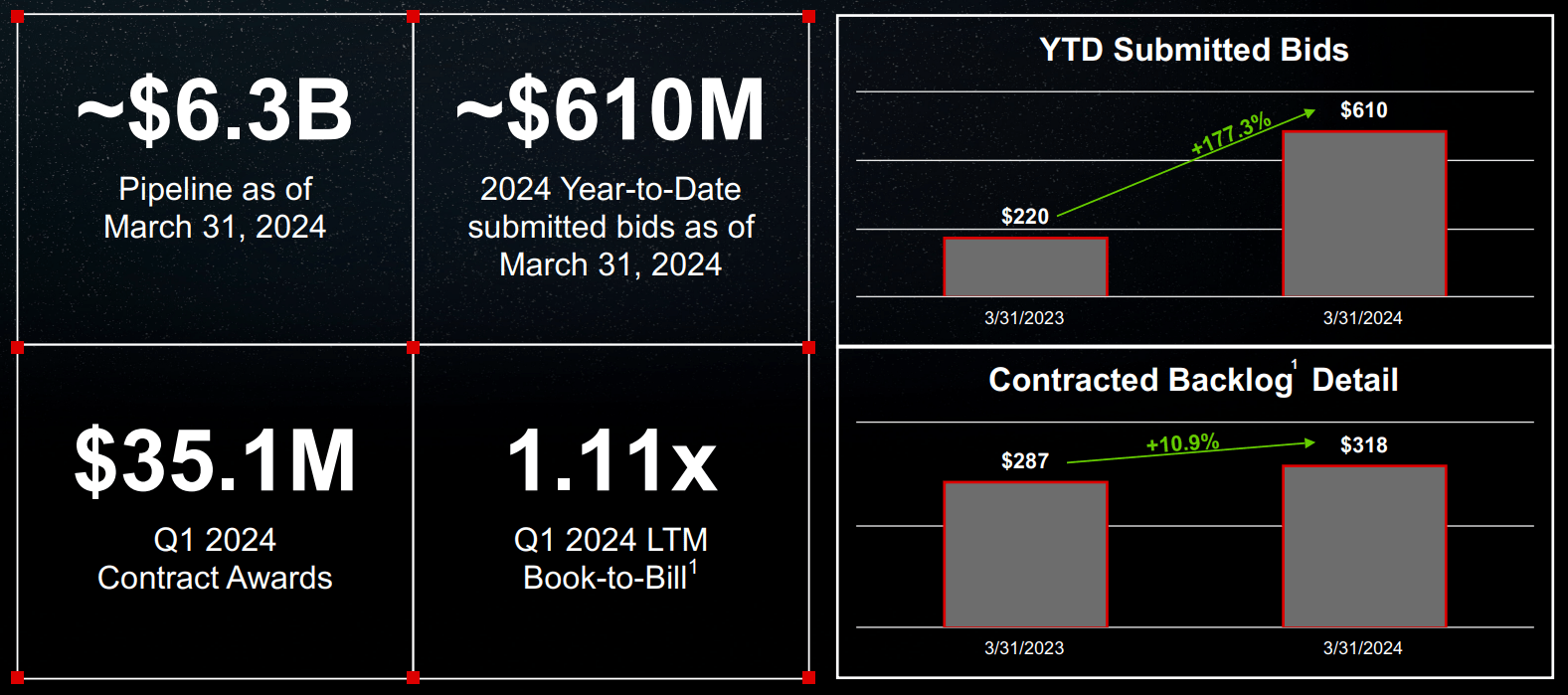

The company carried solid momentum into this year following the signing of a $142 million order for its Roll Out Solar Arrays (ROSA) at the end of last year. This year the company was chosen to deploy the ROSA product for Thales Alenia Space’s satellites. Furthermore, the European Space Agency awarded the company a contract for building a robotic arm prototype for the agency’s Argonaut Lunar Lander. Last month the company was awarded a contract from the Defense Advanced Research Projects Agency (DARPA) for a project that involved Redwire's SabreSat VLEO platform.

Q1 earnings presentation

The company's contracted backlog was 10.9% higher in Q1 than in the prior year period even before the recent contract wins mentioned above. As shown in the image above, the contracts for which the company has submitted bids was 177% higher than at the same time last year. The reasons behind this sharp increase was highlighted by its CEO when he said:

In terms of the bidding, you can see that bidding is accelerating and that's a function of two dynamics. One is more aggressively going to market, but two, as part of the growth principles is bidding those higher-level production contracts for higher quantities as well as some larger contracts for -- we're the full systems integrator, right? So that's really the takeaway from, I think the key takeaway from the increase in the number of bids.

Management also highlighted the recent success of its proprietary in-space pharmaceutical manufacturing platform PIL-BOX. After seeing promising results from its recent mission, management expects 16 additional PIL-BOX missions this year. Though revenue contribution from this business segment is expected to be insignificant for the next few years, Redwire's CEO highlighted the optionality that this presented saying:

Recent venture funding for related industry players has revealed a significant valuation premium for pharmaceutical microgravity development, validating that the venture optionality associated with this subset of Redwire's business has real value.

Risks to consider

Dilutive impact from convertible preferred stock

Q1 10-Q report

In November 2022, the company raised $80 million through the issuance of convertible preferred stock. The annual dividend yield on these shares amounted to 13% if paid in cash, and 15% if paid using the company's shares. According to the company's latest Form 10-Q, the total number of convertible preferred shares outstanding was 93.89 million, with a conversion price of $3.05 per share. Upon conversion, the number of ordinary outstanding shares in the company is expected to increase by approximately 31 million. Thereby shares outstanding would increase from 65.6 million to 96.6 million, implying a potential dilution of around 47%.

In addition to the potential dilution that shareholders face, there is a possibility that the holders of the convertible preferred shares may chose to sell their shares once they are converted, as the ordinary shares do not pay a dividend. This could create an overhang on the company's stock price.

Weak profitability

Adjusted EBITDA was only $4.3 million in Q1, even though it is expected to be the highest revenue quarter for the year. Moreover FCF remained weak at just $0.4 million. Stock based compensation remains high at close to $10 million annually, which makes me believe that achieving profitability on a GAAP basis is more likely to be beyond 2025. Despite SG&A expenses reducing to 19.8% of revenue in Q1, from 27.8% of revenue in the same period last year, volatility in gross margins makes it hard for me to see a clear path to the company achieving solid double-digit margins on the bottom line.

Customer concentration

The company derives a significant portion of its revenue from large customers. According to its 2023 Annual report, two of its largest customers accounted for 30% of its total revenue last year. If these customers were to reduce their spending, the company could see a severe impact. However in Redwire's case this risk is somewhat mitigated by the fact that these customers are mostly government organizations.

Valuation

Since the company is expected to be unprofitable on a GAAP basis, I believe valuing the company based on EV to adjusted EBITDA and EV to Sales (EV/S) is more appropriate. Adjusted EBITDA can be considered a close proxy for FCF, when adjusting for capex and interest expenses which are running at roughly $12 million and $7 million annually, respectively. Management's guidance for this year calls for revenue of $300 million, which is believed to be a conservative number. In line with the trend in recent quarters, I assume that the company is able to achieve an adjusted EBITDA margin of 7% for the full year, which would result in an adjusted EBITDA of $21 million.

With a net debt of $60 million, and assuming its Convertible Preferred shares are fully converted, shares are valued at an EV to adjusted EBITDA multiple of 35, based on the current share price of $7. Correspondingly its EV/S multiple is 2.5. A much larger and vertically integrated peer Rocket Lab (RKLB), is also unprofitable but growing significantly faster and trades at an EV/S multiple close to 5. According to me, shares appear fairly priced when balancing the company's lack of profitability with its strong pipeline and backlog that supports high double-digit growth in the mid-term.

Conclusion

Shares appear to be fairly valued based on my current estimates. The company's solid order backlog coupled with its recent contract wins could potentially help it exceed management's current guidance, and carry this momentum into the next year. On the other hand, the significant risks that I've highlighted above make me stay with a Neutral rating.