Andrii Dodonov/iStock via Getty Images

Investment Thesis

I covered Fastly, Inc. (NYSE:FSLY) back in Mar. 2024, and I laid out my investment thesis focusing on 3 areas:

Operational Efficiency: Can Fastly mitigate its current operating losses while sustaining growth?

Sales Execution: Is Fastly capable of addressing its sales execution challenges?

Revenue Growth: Can Fastly reverse the trend of consecutive quarterly revenue declines and re-ignite its growth trajectory?

Recently, Fastly reported its 1Q24 results, and safe to say that the market was disappointed. The stock plummeted by 33%, suggesting that the market does not think Fastly can effectively address its operational challenges. The main contribution to the decline was the company's forward guidance for 2Q24 and FY24, as Fastly projects a continual revenue decline.

Was the share price decline warranted? In my view, after assessing its results, I do think the market's concerns were valid, although, I'm not sure if it deserved a share price decline that is as brutal as 33%. Nonetheless, there are still some operational challenges that Fastly has to overcome, and until Fastly can deliver a more robust execution, pessimism will continue to be priced in.

As of now, I continue to maintain a "hold" rating for the company.

Discussion of Financial and Operating Metrics

FSLY Quarterly Results

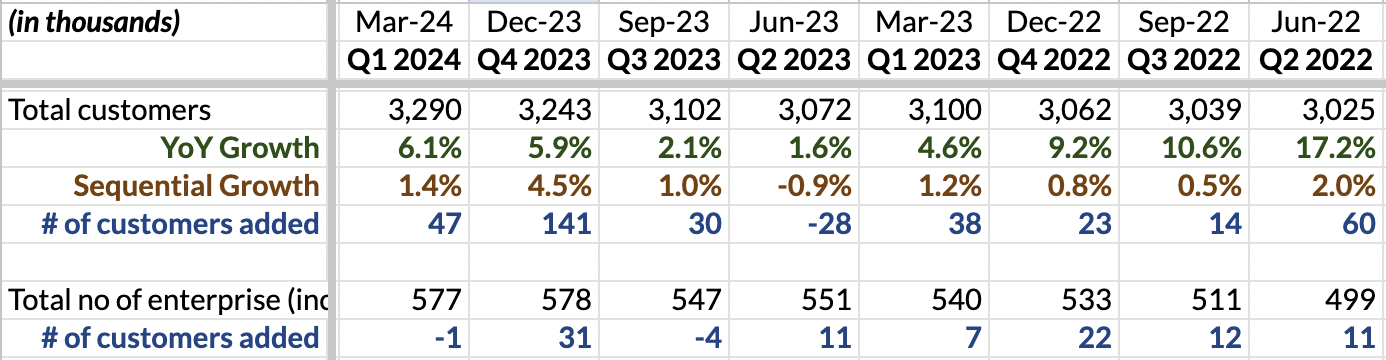

In 1Q24, Fastly delivered revenue growth of 13.6% on a year-on-year basis, bringing its total revenue to $133.5 million, which is the midpoint of management's guidance provided in 4Q23. As you can see, revenue continued to decline steadily over the quarters.

In its latest 1Q24 earnings call, this was attributed to "reduction of revenue from a small number of our largest customers." As their largest customers are using multiple vendors and shifted a portion of traffic to other vendors, revenue contribution from these customers dropped from 40% to 38%. Furthermore, management has also observed that customers in general are spreading out their traffic across more providers, and Fastly's customers are also not increasing their traffic levels as much on its platform.

Previously, I have brought up my concern over Fastly's customer concentration risk and this quarter has proved that this poses as one of the biggest risks at the moment. The need to diversify its revenue remains a top priority for the company.

FSLY Quarterly Results

Fastly's primary revenue comes from enterprise customers, defined as those spending over $100,000 annually. In 1Q24, the total number of enterprise customers dipped slightly to 577 from 578 in 4Q23. However, Fastly has indeed added 18 new enterprise customers this quarter, only for this gain to be offset by existing customers who reduced spending below the $100,000 threshold. Since Fastly's revenue is usage-based, this causes revenue to be extremely volatile, especially in the current macro-environment where companies are cutting back on costs. Excluding the headwind, Fastly would have added 65 new customers, which is still an improvement from a year ago when they only added 38 customers. This is one of the positives that investors can take away from its 1Q24. Also do note that it is not fair to compare it to 4Q23 as the fourth quarter is usually a strong quarter for the company. However, whether these customer acquisition efforts can be maintained in the long run remains to be seen.

FSLY Quarterly Results

One of the negatives from the 1Q24 results was its negative operating margin, as it worsened from 30.9% to 34.6% during the quarter. With declining revenue growth and higher operating losses, the market has likely lost confidence in Fastly's ability to achieve profitable growth, making it one of the partial reasons why the stock has taken a plunge. However, that is not all.

FSLY 1Q24 10-Q

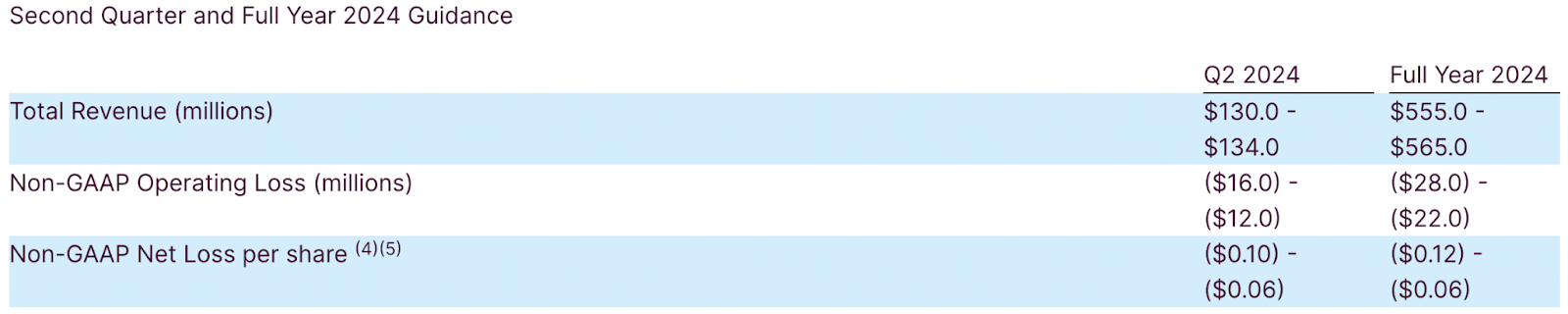

The main contribution to the share price decline was management forward guidance for 2Q24 and FY24. More specifically, the guidance meant that there would be stagnant growth in 2Q24 from 1Q24 and roughly 10% growth in FY24, which is down from the 17% revenue growth we witnessed in FY23. Consequently, the market reacted with disappointment, reflecting heightened uncertainty about Fastly's ability to effectively execute strategies for re-accelerating growth and achieving profitability. Unless Fastly can deliver more robust execution, pessimism will continue to be priced in.

Valuation

Relative Valuation

After the brutal decline in share price, Fastly is now priced at a significant discount to peers based on EV/sales basis as sentiments have further weakened. While investors can surely take a bet to capitalize on FSLY's low multiple in hopes that Fastly may deliver better-than-expected execution, I would, however, advise investors to stay on the sideline until there is clear visibility of improvements in Fastly's business.

Conclusion

In conclusion, Fastly's recent performance and forward guidance underscore several ongoing challenges the company faces. The decline in revenue growth, exacerbated by reduced spending from key customers, highlights the pressing need for Fastly to address its customer concentration risk and pursue strategies for revenue expansion. Despite efforts to onboard new enterprise customers, the impact of customer spending thresholds on revenue volatility remains a concern, particularly amid a macroeconomic environment marked by cost-cutting measures.

The deterioration of Fastly's operating margin and the disappointing forward guidance for 2Q24 and FY24 have further eroded investor confidence, leading to a significant decline in share price. While the current valuation presents an apparent opportunity for investors seeking discounted assets, I would advise investors to steer clear until there is clear evidence of Fastly's ability to execute its growth and profitability strategies effectively.

In light of these factors, maintaining a "hold" rating on Fastly seems prudent until there is greater visibility into the company's ability to overcome its current challenges and regain market trust through more robust execution.