UiPath shocks investors with a poor outlook for fiscal 2025, leading to a substantial sell-off and doubts about its valuation.

The departure of the CEO and a challenging economic environment have exposed cracks in UiPath's narrative, resulting in slower deal closures and inconsistent execution.

The company's drastic revision of its full-year guidance just 90 days after the previous forecast has shattered investor confidence and highlighted the cardinal sin of growth companies.

Looking for a helping hand in the market? Members of Deep Value Returns get exclusive ideas and guidance to navigate any climate. Learn More »

Dragos Condrea/iStock via Getty Images

Investment Thesis

UiPath (NYSE:PATH) shocked investors with a remarkably poor outlook for fiscal 2025. And to be clear, as we headed into this earnings report, I was bullish on PATH.

However, I know from experience that there's no point in compounding one poor investment decision, through sunken cost biases, with another poor investment decision.

In fact, I believe that the only way to outperform the market is by being upfront and recognizing one's mistakes. Everyone makes investment decisions. But the amateur blames someone else, while the professional blames themselves and works to rectify and recoup their poor decision.

As it stands right now, including the premarket sell-off of 30%, PATH is being priced at 50x forward operating profits. A completely unjustified premium for what it offers investors.

Rapid Recap

In my previous article, I said,

[...] after a rocky few years, UiPath is turning around its prospects, and for now, the stock is attractively valued.

Author's work on PATH

With the benefit of hindsight, this turns out to have been a falsehood. UiPath was able to pull together an alluring narrative and convince many notable investors of its strong market positioning. But alas, aside from an alluring narrative, there wasn't enough to support its valuation.

UiPath's Near-Term Prospects

UiPath creates software to help businesses automate repetitive tasks. That's the pitch.

Think of it like a digital assistant that can handle routine work, such as data entry. UiPath's software, often called a "robot" or "bot," can do these mundane tasks quickly and accurately. This helps customers save time, reduce errors, and allow employees to focus on more important work.

Now, beyond its narrative, the reality is slightly less compelling. The departure of UiPath's CEO, Rob Enslin, introduces untimely uncertainty during this critical period.

Additionally, UiPath described a challenging environment with slower deal closures and increased scrutiny on multi-year contracts, particularly affecting mid-market customers.

The inconsistent execution, including contract challenges and changes in sales compensation, has led to its outlook being dramatically altered from 90 days ago.

Therefore, given this context, let's now delve into its financials.

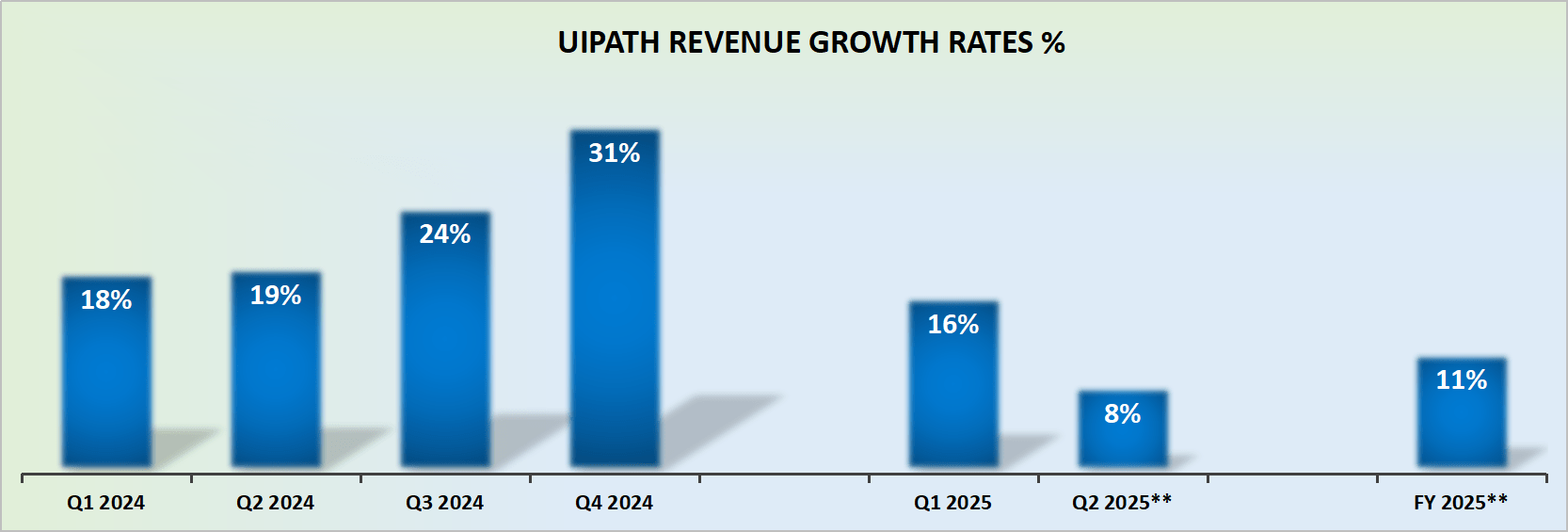

UiPath's Guidance Negatively Surprises

PATH revenue growth rates

A lot can be forgiven about growth companies. Indeed, a lot of a CEO's colorful stories can be bought into provided the company continues delivering strong growth. Essentially, a growth company must deliver strong growth.

What a growth company must not do, in any conditions, is pull back on its guidance. This, my fellow readers, is one cardinal sin that cannot be forgiven. And that's the sin that UiPath committed.

And not only that, but to downwards revise a company's full-year guidance just 90 days after the previous result, by no less than approximately 1,000 basis points at the midpoint of the range? Oh my, that leads to a complete and unmitigated loss of faith in the company's colorful stories. And along with that, the premium that investors are willing to pay.

Including the premarket drop of 30%, PATH is being priced at 50x forward operating profits.

For a while, this thesis was one of a company that could be counted on for some reacceleration of its topline, combined with rapidly improving profitability.

More specifically, UiPath was supposed to be growing its non-GAAP operating profits from $233 million last year to approximately $300 million in this fiscal year. And now?

Now, not only is there not going to be any increase in profitability, but the profitability is actually expected to shrink by 35% y/y.

Given this context, are investors truly likely to pay 50x forward non-GAAP operating profits? Evidently not.

The Bottom Line

In conclusion, UiPath has taken investors on a wild ride with a bleak outlook for fiscal 2025, leading to a substantial premarket sell-off and raising serious doubts about its valuation.

Initially, the promise of UiPath's automation solutions convinced many prominent investors of its potential. However, the departure of its CEO and a challenging economic environment have exposed cracks in the narrative, resulting in slower deal closures and inconsistent execution.

The company's drastic revision of its full-year guidance, just 90 days after its previous forecast, shattered investor confidence and highlighted the cardinal sin of growth companies: pulling back on guidance.

As investors reassess the 50x forward operating profit valuation, it's clear that UiPath's once alluring tale has taken a turn for the worse. After all, in the unforgiving world of investments, failing to deliver on growth is a sin too grievous to be pardoned.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

Deep Value Returns' Marketplace continues to rapidly grow.

Michael Wiggins De Oliveira is an inflection investor. This means buying into cheap companies at the moment when their narrative is changing and the business is on a path toward becoming significantly more profitable over the next year.

With a focus on tech and “the Great Energy Transition (including uranium)”, Michael runs a concentrated portfolio with approximately 15 to 20 stocks and an average holding period of 18 months.

Through his 10+ years analyzing countless companies, Michael has accumulated outstanding professional experience in tech and energy and a following of over 40K on Seeking Alpha.

Features of the group include: Insights through his concentrated portfolio of value stocks, timely updates on stock picks, a weekly webinar for live advice, and "hand-holding" as-needed for new and experienced investors alike. Deep Value Returns also has an active, vibrant, and kind community easily accessible via chat.

Seeking FCF is an associate of Michael Wiggins De Oliveira

Show more

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

@OverTheHorizonHave you noticed that she bought over 330,000 shares of UiPath also one day before the crash? She paid more than $18 per share. So, she must believe the share price is definitely worth more than that.People hate her now, but she is smart and experienced.I expect the share price goes higher than $18 after PATH reports Q3 results.

@Jerry_Slo well, someone told other members and me "We have been using Ul Path since 2019 and this RPA solution is the best on the market. The possibilities of process automation with Ul Path are very powerful. We have 17 jobs running and save well over 10,000 man hours. For complex automation, there is no way around Ul Path". All information without guarantee.

It's good to acknowledge our mistakes. I too recommended PATH at a higher price and am paying quite the price for it. It happens with high growth small cap tech stocks that lose their growth trajectory. That said, I'm not selling at this rock bottom price, I'm holding, but not adding until we see some progress on revenue growth. The founder returning should be a step in the right direction. The valuation is now down to 4.8X Sales with 12-14% growth and 26X Jan 2026 adjusted earnings with mid twenties growth. Worst case scenario - these estimates turn out to be too high. For now there isn't compelling evidence that RPA businesses will get engulfed by AI.

I appreciate your honesty but this is the worse advice you can give someone. Yes, everyone should recognize their mistakes and yes, everyone should rebalance their portfolio. However, you are too quick to do that.UIPATH is a real company solving real automation problems. The company have real customers and will certainly be in a different place long term. The CEO shake up wont even be a thing everyone remembers in a year from now.My advice, HOLD and sit tight if you dont want to DCA.

@down_to_finance I've made over $100k following Michael's advice YTD. CLS, HOOD, HIMS, APP just to name a few. He can't be right all the time. Your statement is asinine.

@Michael Wiggins De OliveiraYou are actually compounding your mistake. PATH was NOT a buy above $20 a couple of months ago! But it is a STRONG BUY today.These are the reasons:- the marketcap now is $6.9 billion. - PATH has no debt and $1.9 billion in cash. - the company is expected to generate $300 million of FCF this year. $300 million FCF for an EV of $5 billion is great.The CEO departure is not a big deal. Remember, he was a CEO or even co-CEO for just one year. The founder and the the person who was the CEO for 17 years before that is coming back to take over the company.Also, the lower than expected guidance for the rest of the year is likely a kitchen sinking. The new CEO will take over the company AGAIN, after 1 year pause, and will have lower expectations to beat.In my opinion, in 5 years from now, after the next recession will be in the rear view mirror, PATH could be worth more than $48 per share, or 400% higher than today. By then they are likely to deliver $1 billion of FCF per year.

@Abcd8 Re your comment: "The CEO departure is not a big deal. Remember, he was a CEO or even co-CEO for just one year. The founder and the person who was the CEO for 17 years before that is coming back to take over the company. Also, the lower than expected guidance for the rest of the year is likely a kitchen sinking. The new CEO will take over the company AGAIN, after 1 year pause, and will have lower expectations to beat."You've mentioned some very important information, especially since we often hear about analysts' earnings projections and forecasts being revised lower before earnings seasons even arrive, meaning CEOs may be given lower, more manageable hurdles to clear. Should Mr Market accept that UiPath's founder be "given a chance and some time to do well," his every earnings beat may be cheered on with a spike upwards in the stock price.Also, as he's the founder, the company will be deemed to be in safe hands for at least the short to medium term, which may be all the time he needs.I'm currently more interested in other stocks, but I think there's a strong case for trading the counter-trend of the current downward fall in UiPath's stock. It could be a slow climb back up, but it's one that I feel is worth it.For me, one of the biggest negatives is that there doesn't seem to be enough job openings mentioning UiPath, and you need human beings to roll out the RPA solutions across client systems in the first place, before any efficiencies or rationalisation benefits can eventually be accrued. But that's a surmountable problem, in time.

@BlueblackI expect the share price to go up fast. At least by 50% by the end of the year.They also do implementations through global partners such as Accenture.What other stocks do you like more?

I am buying more, the call shed light on what was going wrong, and due to accounting the ARR and revenue get distorted from cash flow which the CFO said is US$300m plus with net cash of US$1.8bn the co has plenty of space to fix sales drive. The market has been extremely punishing and rewarding on Q results that provide good trading options. The only reason to sell now is if one thinks the co is not viable i.e. a dying business model, product or service.

@Michael Wiggins De Oliveira hi Michael - had no idea you responded. I didn’t sell. I’m only responding now because I honestly don’t understand your point. Stretched valuations get unstretched. There is a price that invites new investment. I was simply asking you if your sell recommendation was at 18 or at the first opportunity to sell (12 bid context). Do you invest at 5? Does that jibe with your earnings forecast? There was nothing tricky about my enquiry.

@To Div or Not to DivPersonally? I would sell out.If I'm wrong, and the facts show I'm wrong, why to keep repeating the price I paid in the past?The business is clearly worse than I expected. It's frustrating, of course, but that's the game

Short term pain IMO. Time for longs to buy. If our interpretation of a company changes every quarter in this high inflation and interest rate environment, there won’t be any company left to invest except NVDIA. Good to know your perspective @Michael Wiggins De Oliveira and thanks for your efforts. Hope you’re right short term and myself long term!

Thanks for the article Michael, it's good to have someone to share the pain with when things go wrong. It was hard watching the free fall last night and it's even harder to deal with the feeling of being suckered in by what now appears to have been 'creative' fabrication. You are right, there is no good news here and it's def time to sell just as soon as the market opens...

with a strong balance sheet, SA Quant and Wall Street buy rating, plus 30% downfall of price, do you think that this stock is still a sell? I was planning to buy some UiPath and CRM stock today, after downfall.

Equity compensation has always been too high. Still is. Share count has doubled since its IPO. Revenue growth doesn’t matter when expenses are always close behind gobbling up any scale the company may have reached.

@russwise This is the main reason I stayed away from this company. All the cash flow is going to SBC's - nothing left for outsider investors. An activist needs to come in and kick ass.

Disagree with this article? Submit your own. To report a factual error in this article, . Your feedback matters to us!