Alones Creative

Introduction

If you're a baseball fan, you may know that Jens Stoltenberg threw the first pitch of the Washington Nationals game on July 8. He's NATO's current Secretary General.

In case you didn't know, you didn't miss much, as I'm only mentioning this because he was invited due to NATO's current summit in the nation's capital.

It's a special summit, as it's the alliance's 75th birthday, with an agenda packed with key items.

According to DefenseOne, four major topics will likely dominate the meeting:

- Potential NATO membership of Ukraine. Personally, I think this is a nothingburger, especially because there is no way to make Ukraine a NATO member as long as it has Russian troops on its land. It would automatically trigger Article 5 (a full-blown war with NATO).

- Supporting Ukraine long-term. It is likely that NATO will push for potential long-term commitments from member nations to support Ukraine.

- How will NATO deal with China? The war in Ukraine is just one piece of a complex geopolitical puzzle. The big elephant in the room is China. Not only does it support Russia, but it is also a major economic partner of the West with its own goals in the APAC theater. So far, nobody knows what to expect and how to potentially deal with the thing they don't yet expect (it's really that vague).

NATO’s leaders see China as a challenge but are far less clear on how to tackle it. Cooperation with NATO’s four Indo-Pacific partners remains limited. The alliance also seems unsure as to what extent it should focus on Asia as opposed to Europe. And member states don’t agree on the seriousness of the threat posed by Beijing. Developing a clearer strategy toward China will be among the priorities for those attending the 2024 summit. - DefenseOne

- Keeping the alliance strong. With NATO members like Hungary acting on their own in certain matters (like visiting Russia), the alliance is worried it is losing cohesion.

While none of this is truly groundbreaking stuff, I continue to believe we are in a new geopolitical environment with a consistently elevated threat level.

This bodes well for defense demand. Even President Trump is now considered to be bullish on global defense spending, as Politico wrote the other day:

“Hundreds of billions of additional money went into NATO contributions partly as a result of Trump,” said Skinner. “I’m very optimistic about a positive future for NATO if it gets the foundation right.” - Politico.

I'm especially bullish on "next-gen" defense spending, meaning big-ticket projects that aim to modernize NATO defense capabilities.

For example, on July 8, SpaceNews reported the U.S. Department of Defense has decided to proceed with the $140 billion Sentinel Intercontinental Ballistic Missile ("ICBM") program - despite an expected surge in costs from $96 billion to $140 billion!

One of the key partners in this program is L3Harris Technologies, Inc. (NYSE:LHX), the star of this article.

Thanks to its takeover of Aerojet Rocketdyne, it's the supplier of the largest solid rocket motors for what is officially called the "LGM-35A Sentinel" program.

It's also a company that has strategically positioned itself to become a more important partner for NATO defense, generating roughly a fifth of its sales outside the United States.

X/Twitter (@L3HarrisTech)

With that said, my most recent article on this company was written on April 26, when I called it a "Future Dividend Aristocrat With Strong Annual Return Potential."

Since then, shares have returned 5.6%. Despite lagging the 9.6% performance of the S&P 500, I will use this article to explain why LHX remains one of my all-time favorite portfolio holdings.

We'll also get to discuss new developments, including the company's presentation at the Bernstein Annual Strategic Decisions Conference, which is one of my favorite conferences.

So, as we have a lot to discuss, let's get to it!

In The Right Place, At The Right Time

The Sentinel program is just one of many examples that put L3Harris in a terrific spot to benefit from global defense modernization needs.

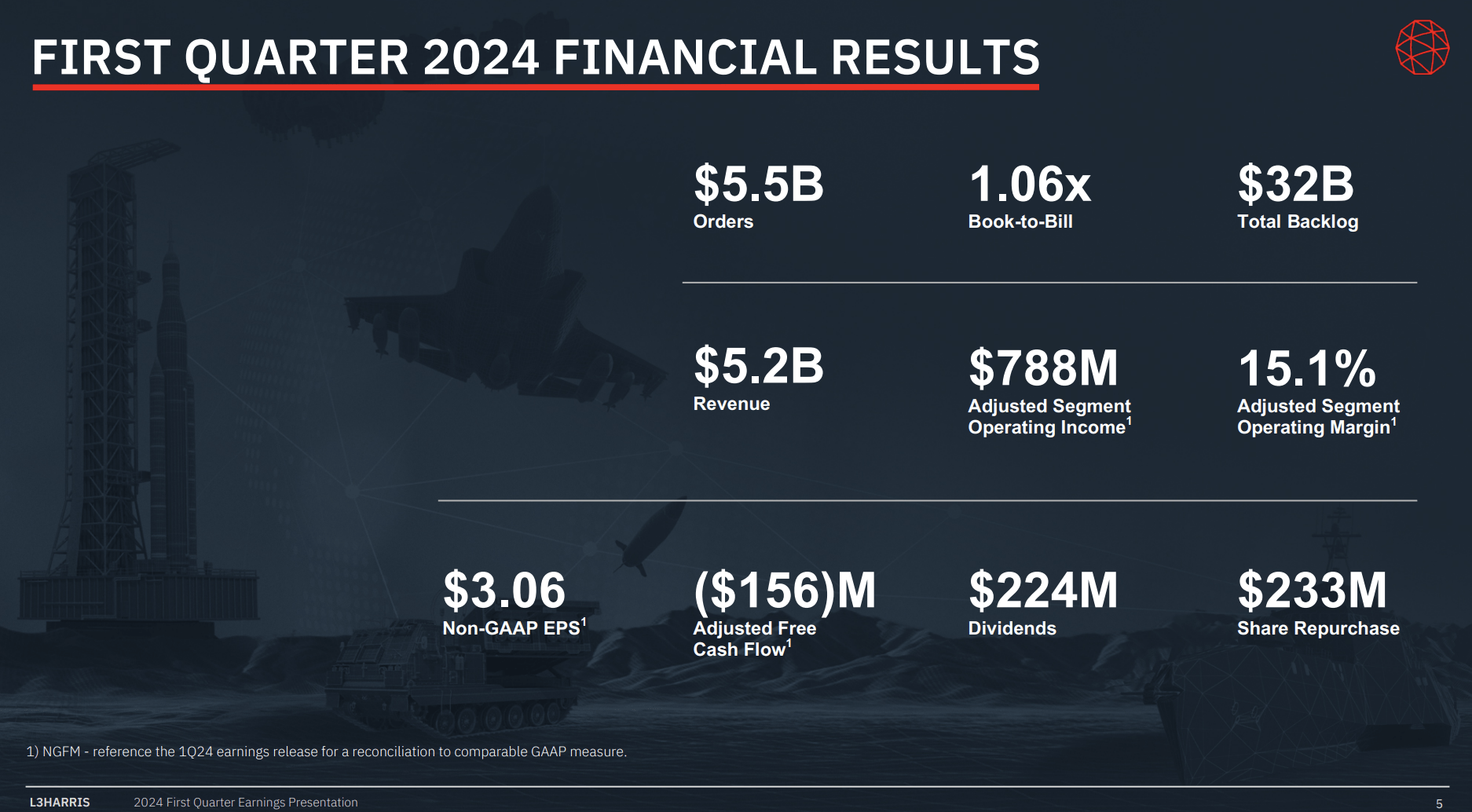

In the first quarter of this year, it reported a $32 billion backlog, including contracts for a $150 million program to provide secure networking to Taiwan and a $900 million contract for SDA tracking Tranche 2.

L3Harris Technologies

Additionally, the company noted the international pipeline remains strong, with significant opportunities in Europe and ongoing support for defense initiatives in Ukraine, Israel, and Taiwan.

Essentially, the pre-pandemic merger of L3 and Harris was a major step toward building a new company that could compete with the "big guys" in the industry and disrupt it in certain areas.

During the Bernstein conference, the company noted that the integration process has been efficient, with over $600 million saved in integration costs.

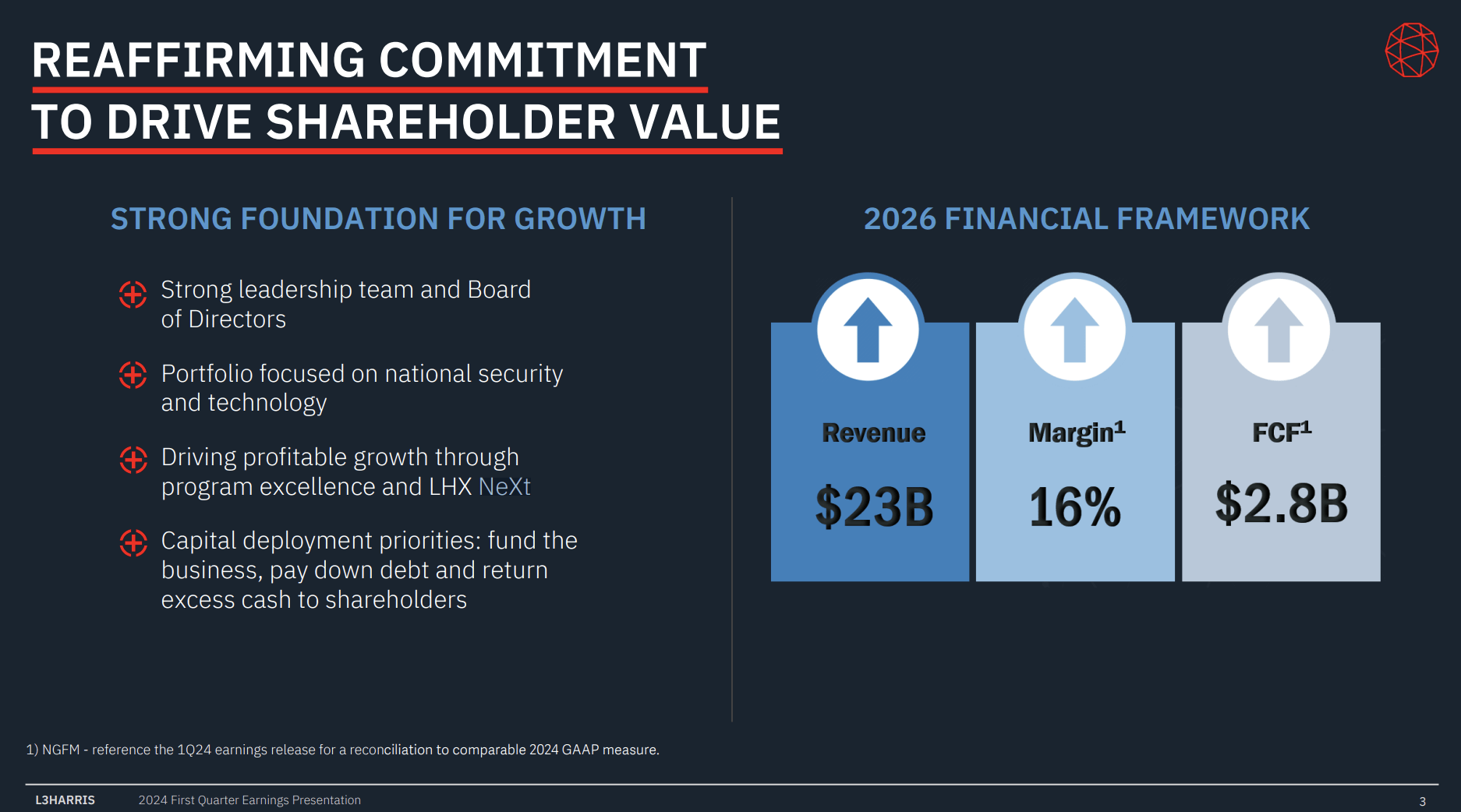

Moreover, despite challenges related to the COVID-19 pandemic, L3Harris believes it has effectively managed its transformation, which continues with the LHX NeXt initiative.

By 2026, NeXt aims to achieve $1 billion in gross cost savings, potentially helping the company achieve its 2026 goal of generating $2.8 billion in free cash flow.

L3Harris Technologies

To put things into perspective, $2.8 billion in expected free cash flow is 6.5% of the company's current market cap. That's a big deal for two related reasons:

- A free cash flow yield of 6.5% means the company can pay a 6.5% dividend or buy back 6.5% of its shares without borrowing a single penny. It obviously won't do that, but it shows how powerful a 6.5% FCF yield is.

- While it won't pay a 6.5% dividend, the company has plans to return 100% of excess cash to shareholders after hitting its 3.0x leverage target. In other words, 6.5% of its market cap will likely be returned as a mix of dividends and buybacks.

In my prior article, I wrote that the company is expected to hit its leverage target by the end of this year.

This allows the company to boost its 2.1% dividend next year and step up buybacks, which have been halted since it bought Aerojet Rocketdyne.

Nonetheless, despite the pause, LHX has bought back 15% of its shares over the past five years, which is very impressive and a taste of what's likely to come.

One of the reasons why the company expects elevated growth to last is that the defense budget environment, despite constraints, aligns well with its focus on national security and future warfare. This is due to the recent M&A and the aforementioned merger.

The constraints the company discussed are pressured government finances. As expected, the surge in interest rates resulted in the U.S. government spending more on interest expenses than defense (and Medicare) this year, which is a mind-blowing development.

Congressional Budget Office

Nonetheless, because the modernization of the armed forces is a top priority (i.e., the Sentinel program), L3Harris continues to reap the benefits of consistent growth in defense spending - both in the U.S. and abroad.

To add some color here, during the Bernstein conference, the company highlighted its diversified multiple-domain product portfolio.

As we can see below, it has significant exposure in four key segments, one of which is Aerojet Rocketdyne, which gave it exposure to more than 50% of the content of every single missile program in the United States!

L3Harris Technologies

Moreover, the company's strong presence in the tactical radio business, with a modernization process for the U.S. Army and Navy and significant international demand, has provided it with more than $2 billion in backlog.

Moreover, it is expecting significant growth in space, which was a $7 billion business last year.

At the time of its merger, L3Harris had no satellites in orbit. Currently, it has over 60 satellites either in orbit or in backlog.

There's a lot of classified satellites. These are constellations with 3- to 5-year lives. So this is a replenishment factor. It's taking capability that was historically airborne and moving into space.

So from our side, having the ability to have literally dozens or hundreds of satellites in orbit with 3- to 5-year lives, it really becomes an annuity. And I think it differentiates us from our competitors. And these are $40 million, $50 million satellites, not $1 billion satellites, mainly in low earth orbit, some other orbits, but we're proud of what we've accomplished. - LHX at 2024 Annual Bernstein Strategic Decisions Conference.

The company is also increasingly repurposing its weather-focused technologies for missile tracking and missile warning purposes. This makes it a bigger player in the classified space market and opens up new revenue opportunities.

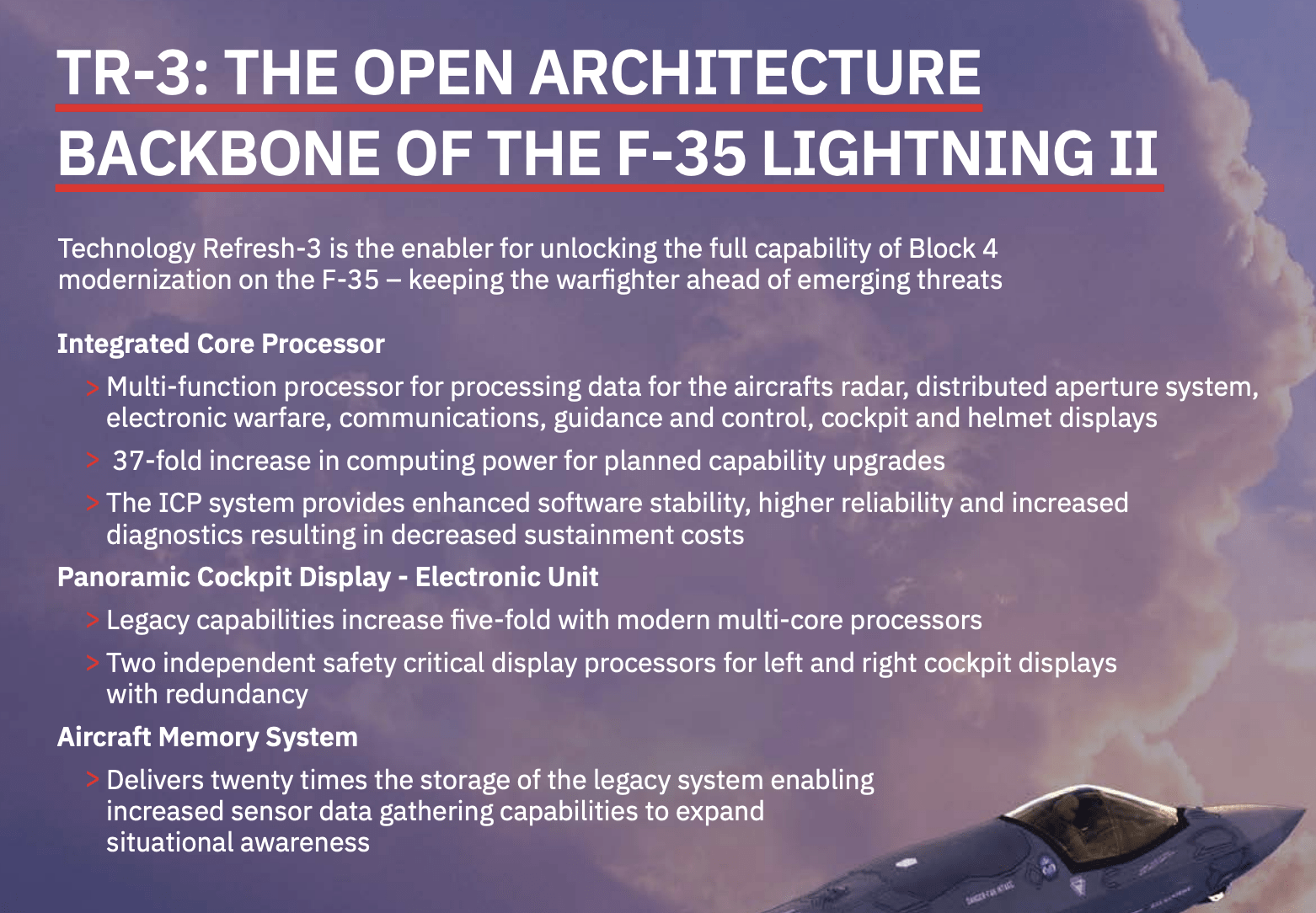

Additionally, the company has a strong core business, as it's a core contractor for the F-35, F-22, and F-16 programs.

In fact, the current TR-3 (Technology Refresh 3) update for the F-35 is aimed at improving sensor suites, long-range precision weapons, electronic warfare features, and data fusion.

Although the TR-3 update has run into delays, L3Harris delivers key products for all TR-3 requirements, making it an increasingly essential player in the F-35 program.

L3Harris Technologies

What does this mean for its valuation?

Valuation

Not only does LHX have a very favorable free cash flow outlook, but it also has a great earnings growth trajectory.

Since I wrote my article in April, analyst expectations have increased.

The table below shows FactSet consensus EPS expectations. The latest numbers are also visible in the FAST Graphs chart below the table.

| Year | EPS (Current) | EPS (April 25) | Y/Y Growth (Current) |

| 2024E | $12.96 | $12.70 | 5% |

| 2025E | $14.19 | $14.07 | 10% |

| 2026E | $15.96 | $15.68 | 12% |

As we can see, after challenging years regarding inflation and supply chain headwinds, analysts see a path to accelerating EPS, which I expect to last.

This tremendously benefits dividend growth and buybacks, as I already briefly mentioned, and gives LHX a great valuation.

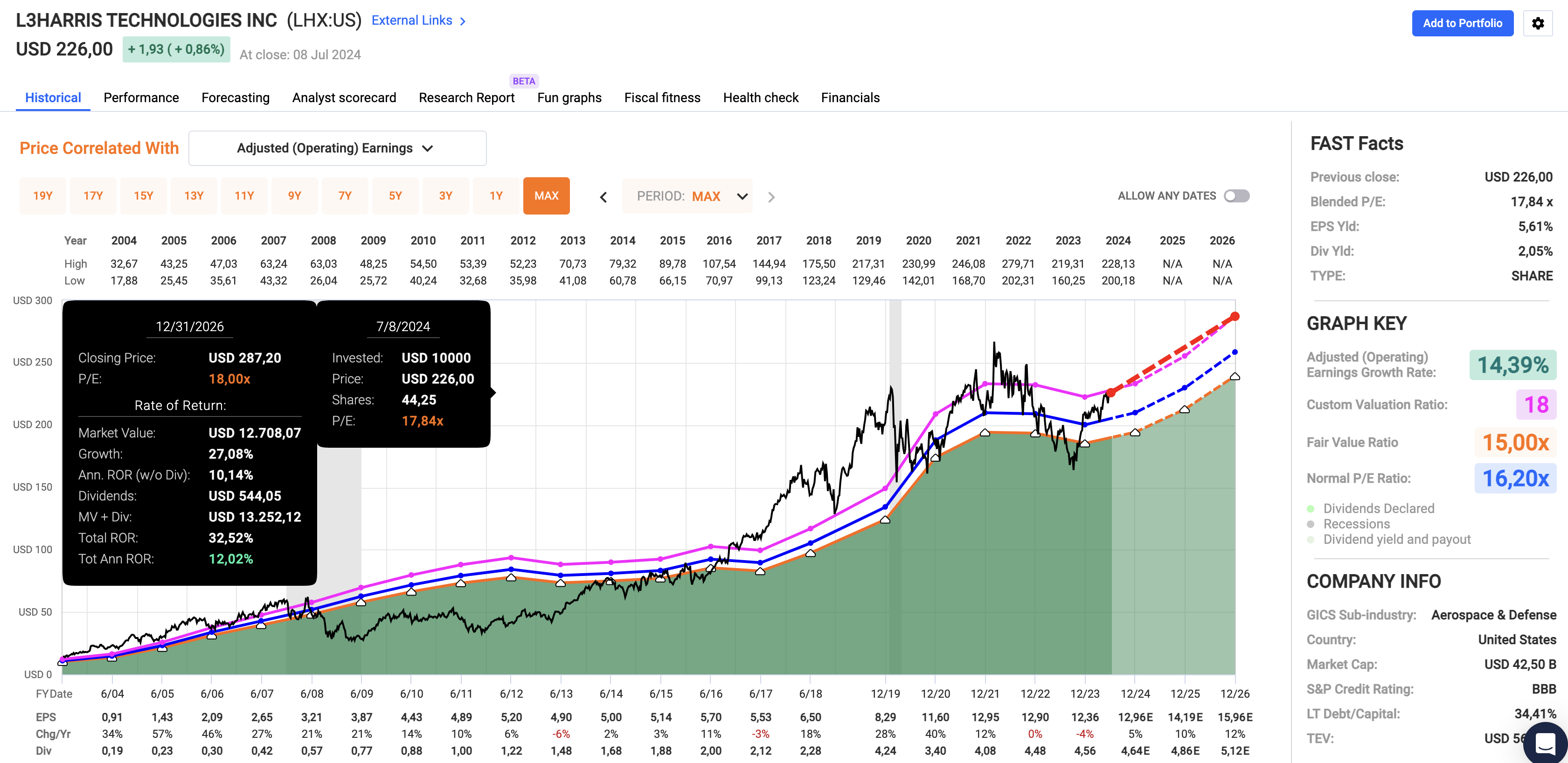

If we apply an 18x multiple to these growth expectations (which I consider a conservative multiple), we get a fair price target of almost $290 and a realistic path to double-digit annual returns.

FAST Graphs

Although the company is subject to factors it cannot influence (economic growth, inflation, rates, geopolitics, etc.), I continue to buy LHX on weakness for my portfolio and all family portfolios.

While I own several great companies, LHX has become one of my favorites, which continues to carry a Strong Buy rating.

Takeaway

L3Harris Technologies is a standout in the defense sector, especially with NATO's increasing focus on modernization.

Its involvement in the $140 billion Sentinel ICBM program, a $32 billion backlog, and F-35 involvement are just three good examples of its relevance.

The company's strategic positioning and promising international pipeline, particularly in Europe and with NATO allies, provide sustained growth.

With a favorable free cash flow outlook, a history of impressive buybacks, and plans to return 100% of excess cash to shareholders, LHX is set to grow shareholder value significantly.

Despite external economic challenges, the company's innovative edge and strong market presence make it a cornerstone of my portfolio and one of my all-time favorite dividend growth stocks with a terrific valuation.

Pros & Cons

Pros:

- Strategic Positioning: L3Harris is crucial for NATO defense, with significant contracts like the $140 billion Sentinel ICBM program, F-35 updates, communication, and satellites.

- Strong Backlog: A $32 billion backlog provides steady revenue and growth opportunities.

- International Expansion: About 20% of sales are outside the U.S., with opportunities in Europe and NATO initiatives.

- Free Cash Flow: An expected 6.5% free cash flow yield means more dividends and buybacks, boosting shareholder value.

- Innovation and Modernization: Leading in next-gen defense projects, LHX is a key player for future warfare technologies.

Cons:

- Debt Reduction Impact: Because LHX is focused on reducing debt, it has temporarily slowed down dividend growth and buybacks.

- Market Volatility: Like any investment, LHX is subject to market fluctuations, which could impact short-term performance.

- Competitive Landscape: LHX operates in a competitive industry, facing competition from other defense companies and potential regulatory challenges.

Test Drive iREIT© on Alpha For FREE (for 2 Weeks)

Join iREIT on Alpha today to get the most in-depth research that includes REITs, mREITs, Preferreds, BDCs, MLPs, ETFs, and other income alternatives. 438 testimonials and most are 5 stars. Nothing to lose with our FREE 2-week trial.

And this offer includes a 2-Week FREE TRIAL plus Brad Thomas' FREE book.