Elen11

Introduction

I first covered L3Harris Technologies, Inc. (NYSE:LHX) in late 2022 when I compared it to The Boeing Company (BA), discussing the characteristics of strong dividend growth investments. It's understandable that LHX stock served as the positive example, while BA stock was the negative example.

Since then, I have covered LHX several times here on Seeking Alpha and have turned increasingly bullish on the stock despite its poor performance in 2023 (and disappointing near-term dividend growth). Undoubtedly, L3Harris has faced headwinds related to its supply chains, wage inflation and also the integration of acquired business units. I always had the impression that the market saw L3Harris - especially since the merger of L3 Technologies and Harris Corp. in mid-2019 - as a company desperate to grow through acquisition, risking falling margins, lack of focus and ultimately stagnation or even decline.

To a certain extent, this narrative was understandable given the somewhat weak performance in recent years. Considering that LHX spent nearly $7 billion on acquisitions in 2023 alone (Viasat's Tactical Data Links product line for $2.0 billion and Aerojet Rocketdyne for $4.7 billion), it is easy to conclude that L3Harris is a poor investment. Finally, the lowering of the rating outlook to negative by Moody's in late 2022, when L3Harris announced the acquisition of Aerojet, most likely contributed to the poor performance (and narrative) as well.

I aggressively added to my position in 2023 despite all the negativity (which peaked in early October with LHX stock at $160) but it appears that all the market pessimism is now a thing of the past. LHX is trading at around $240, up almost 50% in less than a year. Considering that I wrote my last article in August 2023 and L3Harris will announce its second quarter results on Friday, July 26 at 8:30 a.m. Eastern Time, I think it's a good time for an update.

So in this article, I'll outline what to expect from L3Harris' upcoming earnings report and whether my view on the stock has changed after the fairly significant gains in a relatively short period of time, i.e. whether the rally is supported by improving fundamentals. In other words, I'll assess whether it's reasonable to expect LHX stock to continue to outperform the S&P 500 Index (SPY) - which has "only" gained about 30% over the same period, but is on a somewhat more jittery footing due to its concentration in highly valued technology stocks.

How Were L3Harris Technologies' Previous Earnings And What To Expect From The Q2 Report?

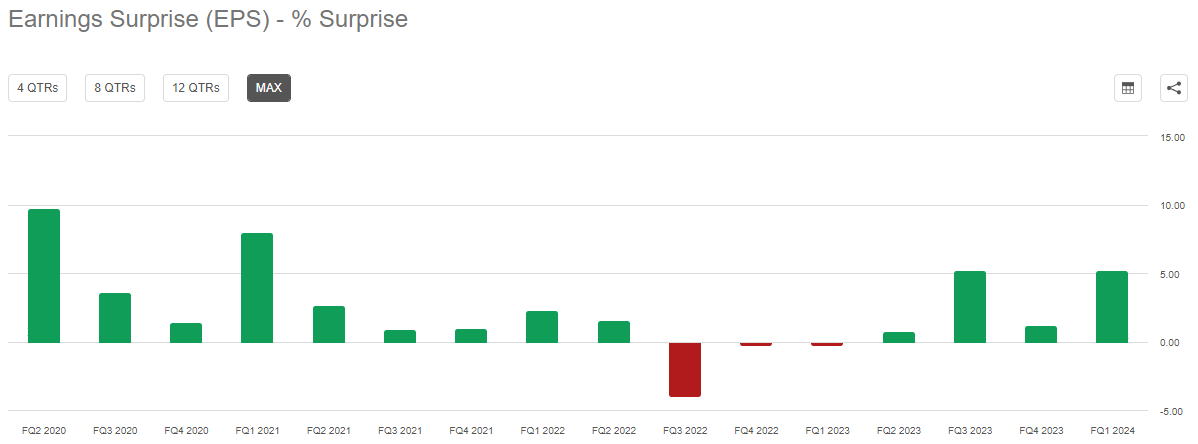

L3Harris routinely delivers adjusted earnings per share (EPS) in line with analyst estimates. Positive or negative surprises have not been particularly significant over the last four years (Figure 1), with the exception of high single-digit positive surprises in Q2 2020 and Q1 2021 and modest negative surprises in the second half of 2022 - when the company was suffering from significant supply chain issues.

Figure 1: L3Harris Technologies, Inc. (LHX): Earnings per share surprise on a quarterly basis (Seeking Alpha)

Adjusted EPS for Q1 2024 was 5% above consensus and revenue also beat expectations (2.4% surprise). For Q2 2024, the consensus for adjusted EPS is currently $3.18, based on revenue of $5.31 billion. The earnings revisions on a quarterly and annual basis do not indicate any potential for significant negative or positive surprises. For example, the adjusted EPS consensus for 2025 and 2026 has remained virtually unchanged over the last six months, and the consensus for 2024 is only 1% lower than six months ago. LHX stock currently trades at 18x estimated 2024 adjusted EPS.

The currently expected figures for Q2 2024 imply adjusted EPS and revenue growth of 7.2% and 13.1%, respectively. However, these figures should not be interpreted as organic growth - LHX consolidated Aerojet Rocketdyne starting Q3 2023. In light of the still ongoing challenges, this raises the question of whether Mr. Market has been getting ahead of himself, or whether LHX stock's outperformance is supported by improving fundamentals.

LHX Stock – Is Mr. Market's Optimism Justified?

To a certain extent, the strong performance of LHX stock is due to slightly higher profitability forecast in the first quarter and ambitious longer-term targets. For example, L3Harris expects to generate $2.8 billion in free cash flow in 2026 on revenues of $23 billion. These figures correspond to an annualized growth rate of 11.9% and 5.8%, respectively. The difference between sales and free cash flow growth shows that management expects significant operational rationalization and margin expansion in the coming years. It should also be borne in mind that Aerojet only contributed around half a year to revenue in 2023 due to consolidation at the start of Q3, which widens the gap between free cash flow and top-line growth even further - from around 6% to almost 8%.

In order to achieve double-digit free cash flow growth, L3Harris is currently implementing a restructuring program called "LHX NeXt", which is a major contributor to the current non-GAAP earnings adjustments. The other big adjustment item - which will also impact GAAP EPS over several years - is the amortization of intangible assets related to acquisitions. And while I'm not a fan of recurring large earnings adjustments, I think they're understandable as long as LHX returns to mostly internal growth (see my article on JNJ's - significant - earnings adjustments for a more detailed explanation) and management is actually able to deliver on its restructuring commitments.

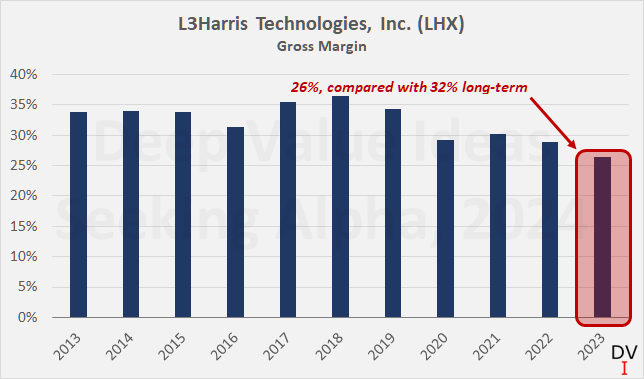

The current emphasis on cost reduction and business integration is illustrated by the recently announced layoffs, which will affect around 2,500 employees (i.e. 5% of the total workforce). This is a key component of the LHX NeXt program (slide 19 ff., 2023 Investor Day presentation), which aims to achieve gross cost savings of $1 billion between 2024 and 2026 (previously $500 million). Reducing supplier spend through inflation clawback and rationalization is the key component that should help LHX return to a stronger gross margin (Figure 2). I think it is worth remaining patient in this context, and I consider the potential for margin expansion to be significant.

Figure 2: L3Harris Technologies, Inc. (LHX): Gross margin (own work, based on company filings)

In addition to reducing supplier spend and rationalizing its workforce, which goes in hand with reducing the number of facilities from 275 to 200, the company will consolidate its IT landscape, which appears to be unnecessarily complex, as a result of the grown structure (merger in 2019 and subsequent acquisitions). In numbers, LHX still operated 85 data centers at the end of 2023, but expects to reduce this number to just two by 2026.

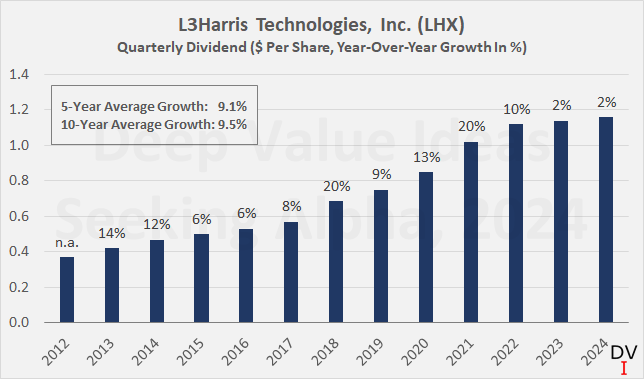

It is clear that a successful integration of Aerojet Rocketdyne, a return to a gross margin of over 30%, a free cash flow margin of over 12%, and significant debt reduction are important to return to more meaningful dividend growth as seen in the years prior to the acquisition of Aerojet Rocketdyne:

Figure 3: L3Harris Technologies, Inc. (LHX): Quarterly dividend and growth rates (own work, based on company filings)

And while I don't want to be misunderstood as a yield chaser, the current starting yield of 2.0% is simply very low - too low, I should say - if LHX is only able to deliver low single-digit dividend growth going forward.

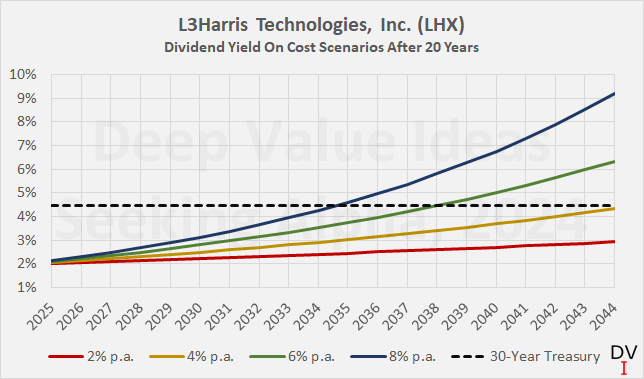

In such a case, a hypothetical investor would probably be better off with U.S. Treasuries or low-risk corporate bonds. With an annual dividend growth rate of 2% and 4%, LHX investors buying the stock today would be looking at a yield on cost of just 2.9% and 4.3% respectively after 20 years, compared to the current 30-Year Treasury yield of 4.45%. Of course, this example doesn't take into account capital appreciation and reinvestment risk of bonds, but if LHX really can't return to its former glory, I doubt the stock would appreciate significantly.

Figure 4: L3Harris Technologies, Inc. (LHX): Hypothetical dividend growth scenarios, compared to the current yield of the 30-Year Treasury (own work, based on company filings and US30Y data)

Nevertheless, I am confident that LHX can return to its previous track record, but investors will have to be patient. There is a lot to like about LHX's product and services portfolio, and in particular the acquisition of Aerojet Rocketdyne has improved L3Harris' negotiating position with the U.S. Department of Defense directly, or indirectly through other defense prime contractors such as Lockheed Martin Corp. (LMT) or RTX Corp. (RTX).

In addition to the proper integration of Aerojet and the overall streamlining of the company's operations, the successful reduction of debt is an important goal that must be achieved before L3Harris can return to more meaningful dividend growth and share repurchases.

At the end of the first quarter of 2024, L3Harris had net debt of more than $13 billion, not even including operating leases, which I estimate at around $800 million (discounted basis). Considering that the company currently generates $2.0 billion of free cash flow, this puts LHX's leverage at over six times free cash flow.

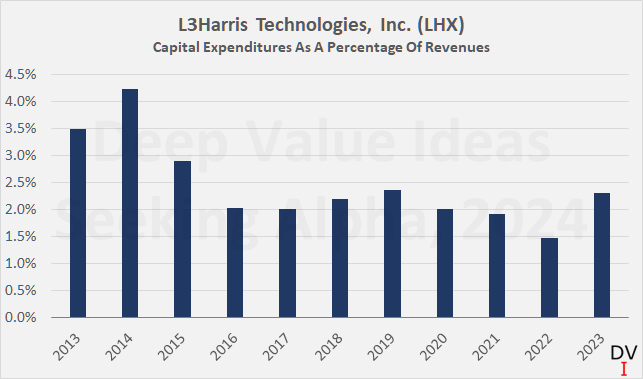

According to Moody's, LHX's pro forma leverage (debt to EBITDA) is around 4.5x. Although it could be argued that the difference is due to the current high capital expenditures, this is not the case according to Figure 5. LHX's management expects to reinvest around 2% of revenue back into the business, as in previous years. It is therefore most likely that the difference is largely attributable to EBITDA adjustments that are not reflected in free cash flow.

Figure 5: L3Harris Technologies, Inc. (LHX): Capital expenditures as a percentage of revenues (own work, based on company filings)

However, as the costs of L3Harris' rationalization program gradually decline and savings are realized, management expects to generate free cash flow of approximately $2.8 billion in 2026. Factoring in stock-based compensation as a cash expense, I estimate that the company can retire up to $3 billion in debt between 2024 and 2026. This estimate takes into account a current dividend payout of approximately $880 million, dividend growth of 2% p.a., and a slight increase in shares outstanding due to performance shares granted. I consider it unlikely that LHX will return to share buybacks in the foreseeable future.

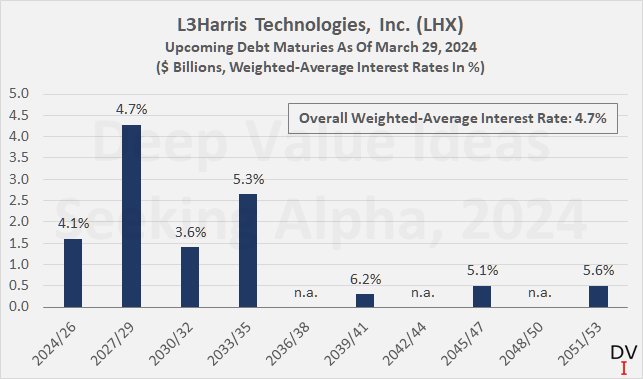

As a result, LHX's debt to EBITDA ratio should fall to less than 3.0x by the end of 2026. In terms of free cash flow, the leverage ratio would fall to below 4.0x. I think this deleveraging plan is realistic given the increasingly long-term nature of LHX's revenue streams, solid backlog and significantly increased cost savings expectations. However, I would argue that aggressive deleveraging is definitely a top priority - not only to return to more meaningful dividend growth, but also given the $4.3 billion in maturities between 2027 and 2029 (Figure 6) and current interest coverage of less than 5x pre-interest free cash flow.

Figure 6: L3Harris Technologies, Inc. (LHX): Debt maturity profile as of March 29, 2024 (own work, based on company filings)

Conclusion – Why I Believe Mr. Market Has Been Getting Ahead Of Himself

Over the years, L3Harris Technologies has evolved into a defense company with a well-diversified range of products and services, characterized by solid margin potential and a high order backlog, which amounted to $32.1 billion at the end of Q1 2024, approximately 1.5 times estimated revenues for 2024. The company finds itself in a solid demand environment, amid rising geopolitical tensions and increasing militarization of space.

However, the company has faced multiple headwinds in the post-pandemic period, primarily stemming from supply chain issues. In addition, L3Harris has taken on significant debt to shoulder the acquisitions of Viasat's TDL assets and rocket engine company Aerojet Rocketdyne - both of which are excellent portfolio additions, in my view.

It was no surprise that L3Harris announced a major efficiency optimization and cost savings program last year, and I view it as a positive that the expected savings were increased from $500 million to $1 billion at the 2023 Investor Day. First quarter results were solid and management is already seeing a modest improvement in profitability.

The second quarter earnings report, which will be released on Friday, July 26, will be interesting to analyze, especially with regard to further progress in operational streamlining. In my view, there are many low-hanging fruits that can be harvested, such as the consolidation of data centers and related applications, the focus on a single ERP system with the help of artificial intelligence-assisted data migration, as well as a modest reduction in supplier spend, also thanks to increasingly stronger bargaining power. As a result, I expect positive news, and I also think it is unlikely that the company will miss adjusted EPS estimates, given its track record to date and the insignificant revisions.

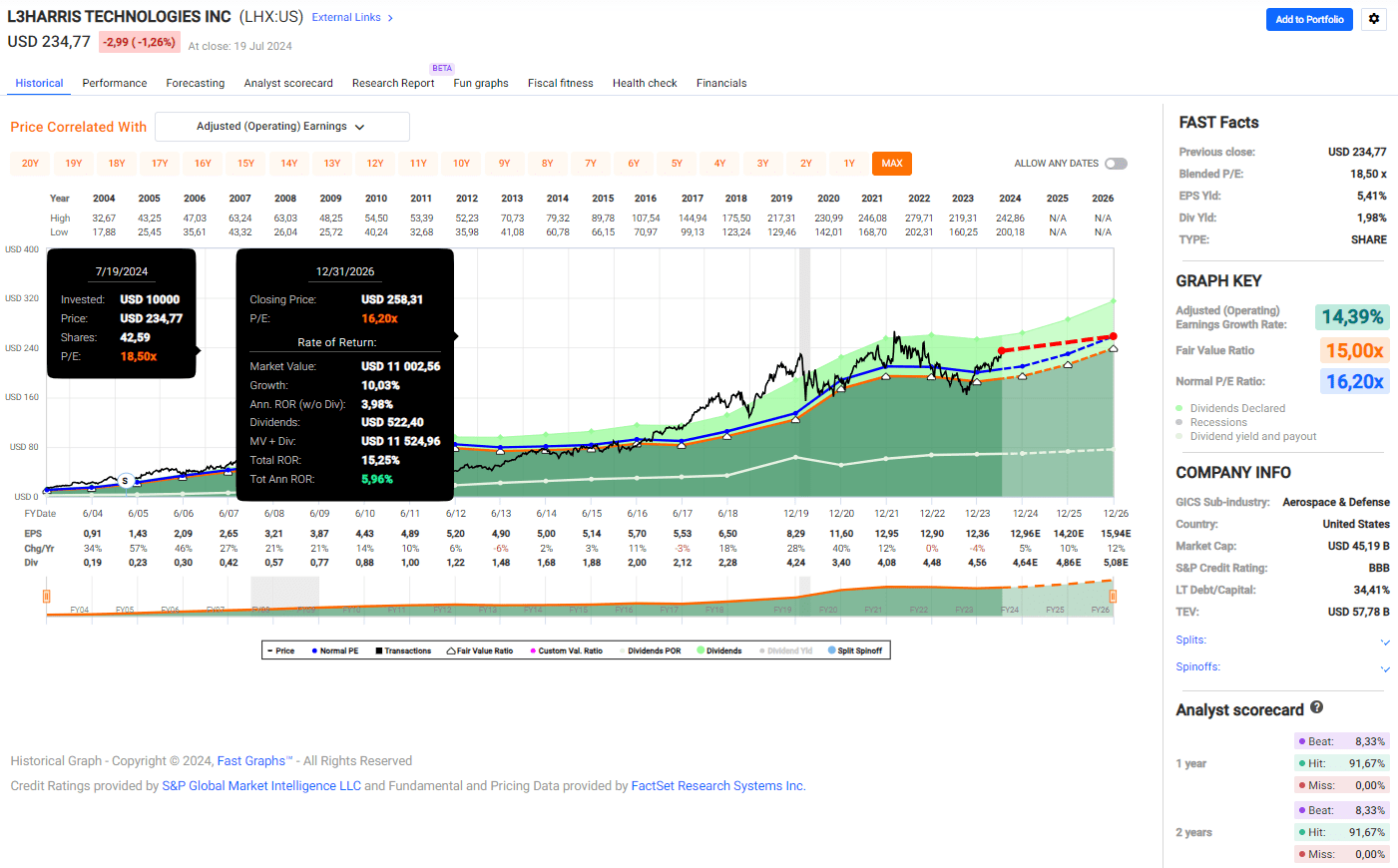

However, I think the market has already factored in many of the improvements highlighted in the Investor Day presentation and has also reacted positively to the Q1 report, with LHX stock up 14% since April 25. Judging by the FAST Graphs chart in Figure 7, LHX stock offers no margin of safety and the company's operational recovery is largely priced in. It should also be noted that the chart is based on adjusted operating earnings, which will continue to diverge significantly from GAAP earnings for several years amid ongoing restructuring.

Figure 7: L3Harris Technologies, Inc. (LHX): FAST Graphs chart, based on adjusted operating earnings per share (FAST Graphs)

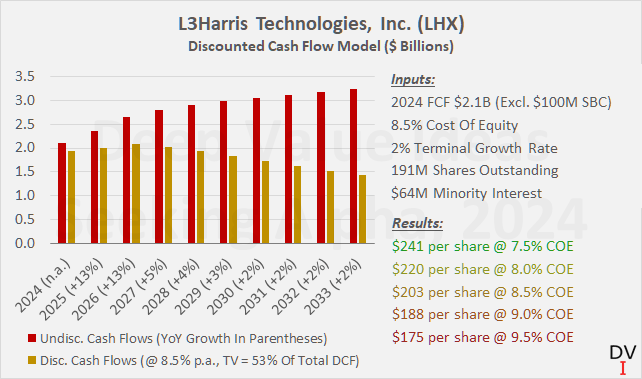

I conducted a discounted cash flow analysis (Figure 8), which confirms this observation. A discount rate of 8.5% seems reasonable, considering LHX's currently quite pronounced leverage, significant maturities in 2027-2029, and the still largely unrealized cost-saving measures as well as associated implementation risk. However, the analysis also takes into account management's free cash flow guidance for 2024-2026, so it is not exactly pessimistic. With these data, LHX shares should be worth around $200 today, and the current stock price of $235 implies a cost of equity of 7.5% to 8.0%.

Figure 8: L3Harris Technologies, Inc. (LHX): Discounted cash flow analysis, including a cost of equity sensitivity analysis (own work, based on company filings and own estimates)

Taken as a whole, and also given the need for aggressive deleveraging before L3Harris can return to more meaningful dividend growth and share buybacks, I am personally not interested in adding to my position at this time and believe it is likely that LHX shares will enter a phase of stagnation before more tangible results in the form of improved profitability and deleveraging are presented. Conversely, given the solid foundation, strong demand environment, realistic deleveraging plan and operational rationalization program, I view LHX as a solid long-term position and am not thinking for a second about selling or trimming my position - despite solid gains in a relatively short period of time.

Thank you very much for reading my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.