John M Lund Photography Inc/DigitalVision via Getty Images

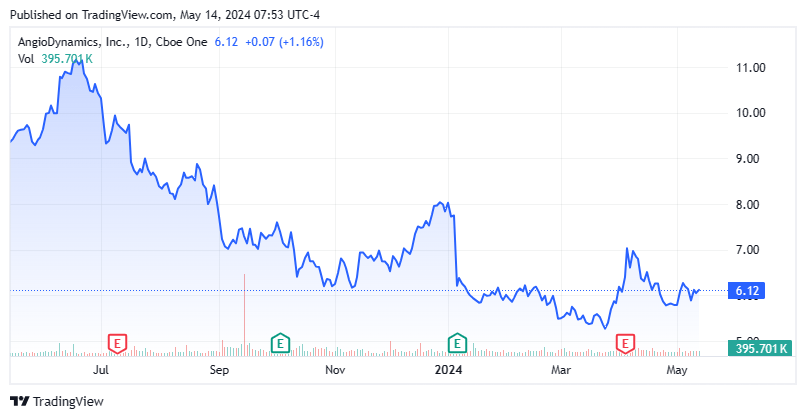

Shares of medical device concern AngioDynamics, Inc. (NASDAQ:ANGO) fell to an all-time low of $5.26 on March 25, 2024, as it struggles for profitability in the middle of a restructuring. The company hasn’t turned a profit since 2017, and isn’t projected to do so until FY27, after it exits the business of manufacturing its own devices. However, with no debt, an increasingly higher margin portfolio as it divests and discontinues lower margin products, and a price-to-sales of less than 0.7 net of cash, the recent insider buying merited a deeper dive. An analysis follows below.

Seeking Alpha

Company Overview:

AngioDynamics, Inc. is a Latham, New York-based medical technology concern primarily focused on developing and marketing minimally invasive, image-guided devices that address cancer and vascular disorders. Unable to achieve GAAP profitability since 2017, the company is in the process of a restructuring that will result in the elimination of its manufacturing capabilities, while emphasizing its profitable medical technology business. AngioDynamics was formed as a division of E-Z-EM in 1988 and was spun out during 2004 in an offering that raised net proceeds of $3.0 million at $11 per share. Its stock trades just under $6.50 a share, equating to an approximate market cap of $250 million.

The company operates on a fiscal year (FY) ending May 30th. For the avoidance of doubt, FY23 refers to the 12-month period ending May 30, 2023.

Revenue Disaggregation

AngioDynamics disaggregates its top line into two segments: Med Tech and Med Device.

Med Tech is clearly the area of emphasis for management. It primarily features thrombectomy devices and one atherectomy instrument, Auryon. Approved for numerous procedures to treat deep vein thrombosis and peripheral arterial disease, Auryon is designed to remove plaque from arteries through the delivery of laser pulses. The device is also used in small vessel thrombus management, zapping blood clots to clear occluded vessels. Launched in 2020, it surpassed $100 million in cumulative sales in November 2023.

For large vessel thrombus management, the company markets AngioVac and AlphaVac, which aspirate large blood clots in the heart and other large vessels, respectively. The latter added pulmonary embolism to its previously green-lighted venous thromboembolism indication on April 4, 2024.

AngioDynamics also sells soft tissue ablator NanoKnife, which delivers short electric pulses to precisely eliminate cancer cells. Due to the targeted nature of the device, it appears well suited for treating prostate cancer, an indication the company anticipates having by the end of calendar 2024, after it wraps up a trial in July.

Management places the total global addressable market for its Med Tech devices at $9.8 billion.

During the first nine months of fiscal 2024 (YTDFY24), this unit produced net sales of $77.1 million, up 10% from YTDFY23 and 33% of total. Gross profit was 62.8%, down 100 basis points from the prior year period. Owing to the protracted decline in the company’s stock price, management elected to take a $159.5 million impairment charge to write down the carrying value of this unit in 3QFY24.

Med Device generated YTDFY24 net sales of $155.9 million, down 12% from YTDFY23 while comprising 67% of total. Gross profit was 43.5%, down 330 basis points from the prior year period. Owing to the unit’s low gross profit margin, the company has been shedding assets, specifically divesting of its peripherally inserted central catheter (PICC) and midline catheter businesses for a consideration that could total $45 million, while discontinuing two radiofrequency ablation devices and a line of support catheters in February 2024. In total, these products contributed ~$50 million in FY23 net sales, leaving this segment’s focus on its EVLT laser system to treat varicose veins and angiographic catheter assets.

Restructuring

These moves come on the heels of the company shedding its cash-generating dialysis and lung biopsy sealant businesses for $100 million (approximately two times sales) in June 2023, allowing it to eliminate its high interest rate debt. Furthermore, management announced that its manufacturing footprint would shift from its facilities in upstate New York to a fully outsourced model by 3QFY26. Prompting the aforementioned discontinuation of some Med Device products – as their transition to a contractor model was deemed uneconomic – this move is expected to both save AngioDynamics $15 million annually in FY27 and unbind it from the limitations of its current operating profile, enabling it to produce higher margin products at scale.

Share Price Performance

The restructuring has somewhat correlated with its stock’s abysmal performance since November 2021. After trading as low as $7.48 during the Covid-19 selloff in March 2020, shares of ANGO rallied 328% to an all-time high of $32.00 in November 2021, as the return of in-patient procedures sparked hopes of a return to profitability. Unable to achieve that goal, AngioDynamics’ stock retreated 84% to an all-time low of $5.26 on March 25, 2024, as competition squeezed margins in its portfolio, while its focus on the higher-margin Med Tech products did not generate enough top-line growth to outrun operating expense inflation.

3QFY24 Report

That said, there were a few silver linings in the company’s 3QFY24 report of April 4, 2024. On a pro forma basis (which excludes divested and discontinued business lines), it posted a loss of $0.16 a share (non-GAAP) and Adj. EBITDA of negative $3.6 million on net sales of $66.0 million, versus a loss of $0.14 a share (non-GAAP) and Adj. EBITDA of negative $1.5 million on net sales of $61.1 million.

Although comps versus expectations are difficult given the in-quarter divestiture of revenue-generating assets, this report highlighted Auryon sales of $11.8 million (up 15% year-over-year) and NanoKnife sales of $6.0 million (up 47%). The latter’s razorblade model featured disposable sales up 20%, outpaced by a 231% surge in instrument sales. AngioVac net sales were flat at $5.5 million. And although AlphaVac revenue was down 45% to $1.1 million, that result was accompanied by news of its label expansion into pulmonary embolism, setting up a full launch for that indication in 1QFY25. In total, MedTech sales improved 13% year-over-year and comprised 38% of revenue on a pro forma basis, while the trimmed-down Med Device category saw net sales rise 5%.

To reflect the divestitures and discontinuations, management adjusted it outlook to a loss of $0.56 a share (non-GAAP) with gross margin of 53.0% (previously 50%) on net sales of $272.5 million ($322.5 million) versus $0.55 a share (non-GAAP) on gross margin of 54.9% on net sales of $257.2 million in pro forma FY23. The drop in pro forma gross margin reflects product mix within MedTech and expenses associated with the transition to an outsourced manufacturing model. The revised guidance was based on range midpoints.

Furthermore, a few days prior (March 31st), AngioDynamics announced that it had settled 12-year-old patent litigation claims with Beckton, Dickinson (BDX) for $7 million, with six subsequent $2.5 million annual payments that are subject to rise contingent upon net sales of AngioDynamics’ port products.

The market liked what it heard, rallying shares of ANGO 16% to $7.03 in the two subsequent trading sessions.

Balance Sheet & Analyst Commentary:

Also encouraging is the company’s debt-free balance sheet that reflected cash of $78.5 million on February 29, 2024, a byproduct of the aforementioned dialysis and lung biopsy sealant divestitures. That said, AngioDynamics did burn through $33.2 million of cash from operations in YTDFY24. It does not pay a dividend nor currently repurchases its own stock, although the latter situation may change with its relatively high cash levels and little interest – at least advertised – in acquisitions.

Despite the abysmal operating and share price performance, Street analysts are on board with management’s approach, featuring two buy and two outperform ratings with a median price objective of $14.50. On average, they expect AngioDynamics to generate a loss of $0.52 a share (non-GAAP) on revenue of $287 million in FY24, followed by a loss of $0.49 a share (non-GAAP) on flat sales in FY25.

President & CEO James Clemmer shares the Street’s optimism, having purchased 10,000 shares of ANGO at $6.70, shortly after his company’s 3QFY24 financial report on April 8th.

Verdict:

That said, the only way to get excited about a low-growth revenue generating concern that is not projected to turn a profit until FY27 – its first in ten years – is for the valuation to be compelling. The default metric is price-to-sales, which currently stands at under 1.0 and south of 0.7 net of cash. With gross margin north of 50%, the valuation is compelling. However, management admitted that margin would “ebb and flow” as it transitions to its contract manufacturing model (i.e., double pays for overhead).

The bet is that AngioDynamics, Inc. stock is putting in a bottom, but it is likely to remain range bound until its restructuring demonstrates meaningful signs of success. It is one to keep an eye on, but I will pass for now.

Author's note: I present an update my best small and mid-cap stock ideas that insiders are buying only to subscribers of my exclusive marketplace, The Insiders Forum. Our model portfolio has more than doubled the return of its benchmark, the Russell 2000, since its launch. To join our community and gain access to our market beating returns, just click on our logo below.