EvgeniyShkolenko

Spire Global (NYSE:SPIR) is an opportunity to bet on space and AI at the same time. Early in its life as a public company, one might think the stock is one to avoid.

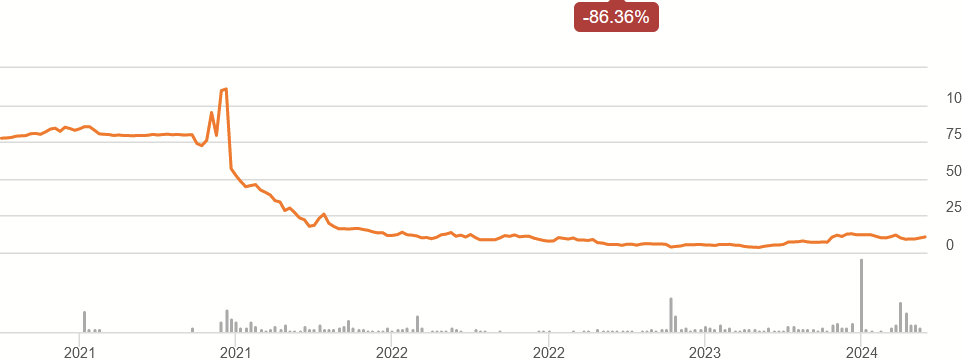

SPIR Price History (Seeking Alpha)

Currently, the market prices it as a microcap, waiting for Spire to generate positive cash flows. I believe that moment is approaching and that the new opportunities presented by generative AI have paved it wide open. There are some risks, but I think the stock is at least fairly valued for those, with asymmetric upside if all goes well, making this a great buy.

Business Model

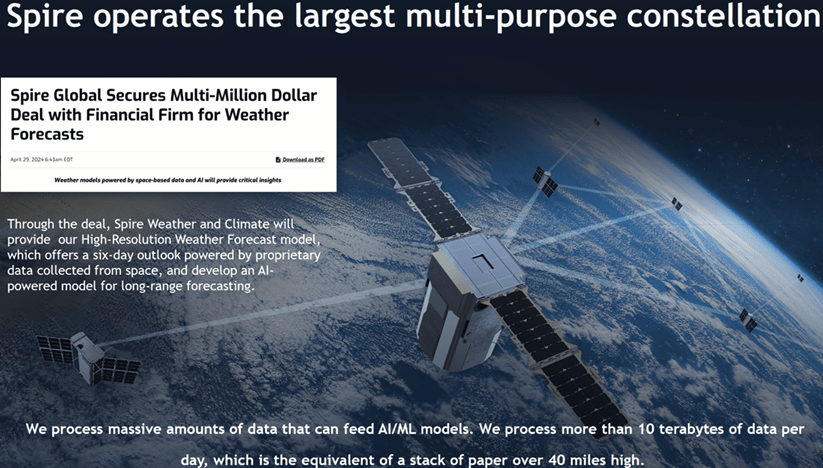

Founded in 2012, the company has spent its life constructing and growing its own satellite fleet. It claims to have the largest "constellation" of multipurpose satellites, with over 170 in orbit as of 2023. Combined with their ground stations, they provide a cloud-based platform, hosted online through Amazon Web Services.

Q1 2024 Company Presentation

This constellation collects proprietary data of the Earth from orbit, which is available for multiple sales, providing the company good operating leverage. Key areas where their constellation provides data solutions that are hard to replicate on Earth include maritime travel, aviation, and weather.

Additionally, they provide Space Services to customers, wherein they design, construct and deploy satellites specifically for customers, earning steady subscription revenues from it.

Since they aren't limited by tangible inventory, their business depends on their ability to maximize the sale of their services. They describe their strategy as "land and expand," where they focus on acquiring new accounts and maximizing all possible sales with that customer. This makes the sales process long-tailed, with bigger rewards down the road.

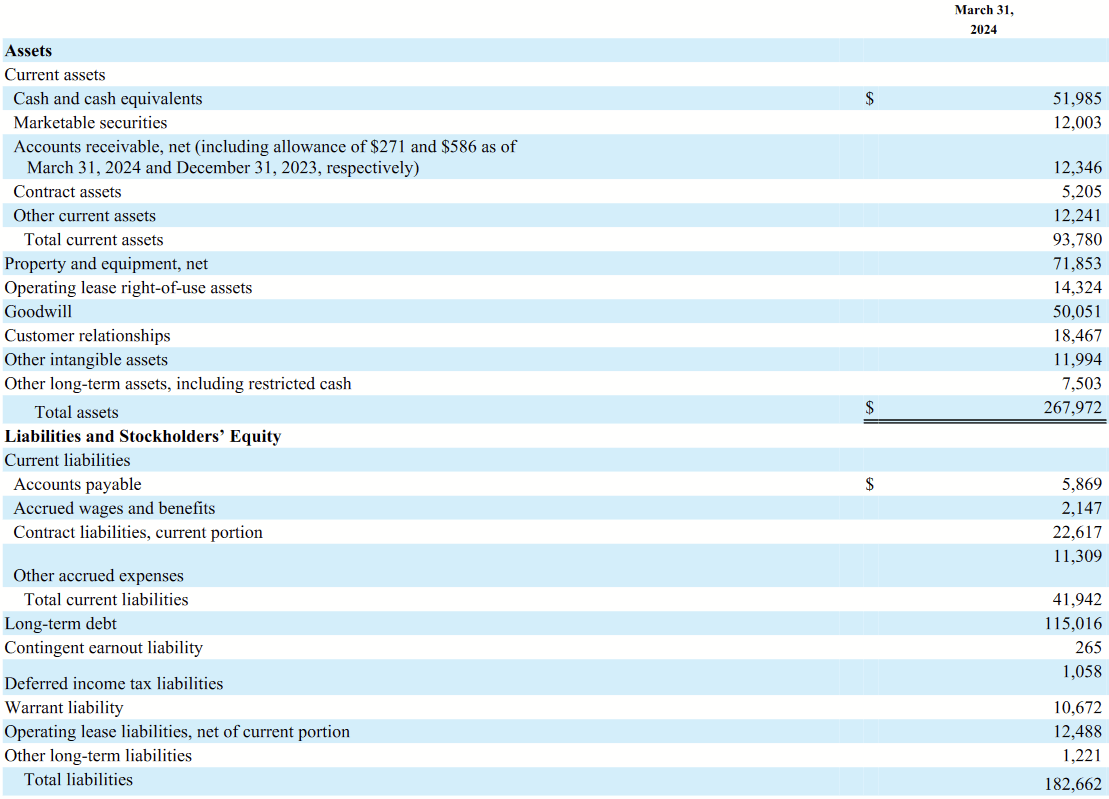

Balance Sheet (Q1 2024 Form 10Q)

Since its cash flows are not yet positive, the company has had to raise capital to progress, through equity and debt. This means $115M of long-term debt was on its balance sheet as of Q1 2024.

Debt Maturity (Q1 2024 Form 10Q)

Most of this comes due in 2026.

Future Outlook

The question is if Spire will successfully transition to positive cash flow, and how soon that will occur. Let's look the things that will affect that.

Expenses

With gross margins around 60% in 2023, it's largely a matter of reaching enough scale.

Income Statement (2023 Form 10K)

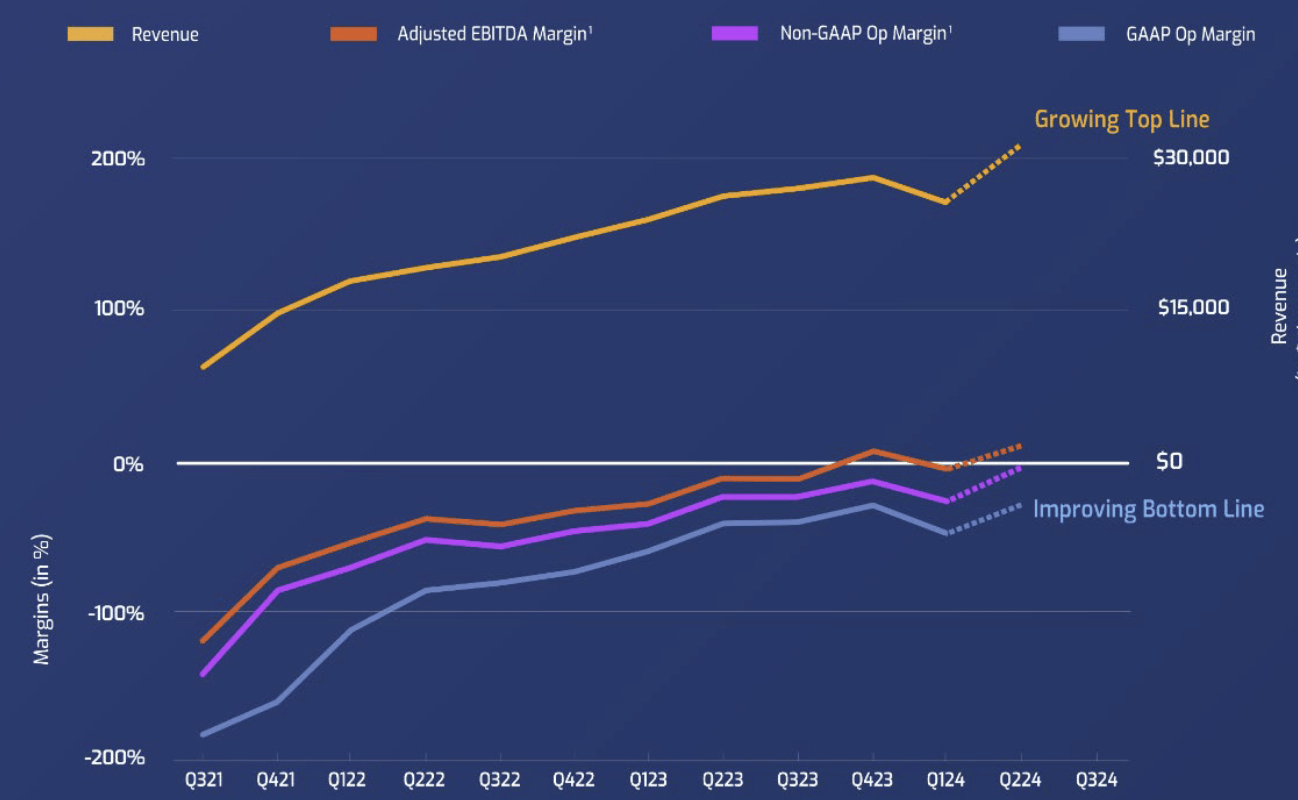

Seen here, operating expenses remained flat from 2022 into 2023, while revenues grew. Q1 2024 likewise showed somewhat lower expenses than the prior-year quarter.

Q1 2024 Company Presentation

I believe the business is already showing signs of its operating leverage. Capex is a different question, though.

Cash Flow Statement (2023 Form 10K)

It increased quite a bit, from $18.9M in 2022 to $30M in 2023. For free cash flow to turn positive, this figure can't grow like that. When asked if it would change much for the foreseeable future in Q1 earnings, CEO Peter Platzer had to say:

And no, really not. I mean, we basically have a fully deployed constellation and it's basically a replenishment what we're planning...Some of the assets that we're seeing de-orbit we will replace and replenish. And no, we still believe that it's between $5 million $7 million as we mentioned, what we will need for our internal for our own needs from a data generation standpoint.

He is talking about the capex for the Spire platform there.

2023 Capex (2023 From 10K)

That accounts for about 20% of all capex, so that part will remain relatively flat. Capex on the Space Services is what's been growing, as that is where they are experiencing more growth as well.

AI-Driven Demand

One of the biggest drivers of growth has been the recent emergence of generative AI. With unique assets and proprietary data from orbit, Spire is combining this with the learning power of AI to provide better predictive models to customers.

Platzer made the following observation:

Just two years ago, weather experts expressed skepticism regarding the efficacy of AI driven weather models. However, within a year, a prominent global weather agency began establishing an AI weather forecasting team and model. Recent analysis reveal that their AI model surpasses the accuracy of their long standing physics based model...

He later added, more concretely:

This is just the beginning of a long list of opportunities. Weather impacts almost every aspect of the human experience. We expect interest from governmental organization, logistics companies, energy and commodity firms, insurance companies and companies with infrastructure that can be impacted by adverse weather. It is estimated that weather impacts $30 trillion of GDP and 10% of that or $3 trillion is mitigatable. This is an absolutely massive market and Spire is in a prime position to capture a portion of it.

Weather models are just one type of data solution they could provide with their constellation, but it is an important one, a very real one. I've reviewed plenty of insurance stocks as well, storms are the biggest culprit for the one that have bad years. Anything that gives them better risk models and more precise pricing is going to be in hot demand, and they can sell these data and learning models to multiple insurers.

There are unique advantages to these space assets and the unique data they provide. This is a barrier to entry, so I agree that Spire can ride the AI wave reliably and without too much concern about major competition.

Short-Term Uncertainty

Platzer also explained that the Space Services segment may have setbacks in quarterly results. He elaborated:

...I'm a physicist as you know, Erik, but even the best physicist cannot really perfectly predict how the solar activity is doing things from a week-to-week and month-to-month basis. So it's a highly dynamic process where things can move from you have an asset for another six months to you have an asset for another six weeks can actually happen reasonably quickly, right.

So this means launch of Space Services satellites could be delayed, affecting individual quarters. Nevertheless, Platzer was confident about the long-term prospects:

So I think again, looking at a number that is a few months out from a growth perspective, it is not what the Spire market demand is showing us. What we are seeing is still the same long-term demand for our products, and if anything that it is increasing. So our long-term growth prospects way above 20% have not changed one iota.

The market may not appreciate this for the shares, especially for a microcap stock. SPIR needs to be treated as a long-term investment.

Non-Insured Risk

In both the earnings call and the risk factors of the SEC filings, management has mentioned that their space assets are not insured. A market for such an insurance product simply does not exist. If something were to happen to their spacecrafts, there's no policy to recover the financial loss.

Debt Risk

In the earnings call, management also expressed hopes to refinance their large principal under their term loan by the end of the year. This assumes that their expectation of positive cash flows by this summer will pan out.

Currently, the interest on that loan is SOFR + 7% (with other provisions), a pretty high rate. Interest expense in 2023 was $19M, a pretty large drag on cash flow. Refinancing on favorable terms is not only key to push back that large principal, but also to reduce interest expense favorably.

In Q1, they even sold shares to repay $10M of that principal, so there's already some precedent of dilution to manage the debt. This I see as being of the bigger, potential foils to my thesis.

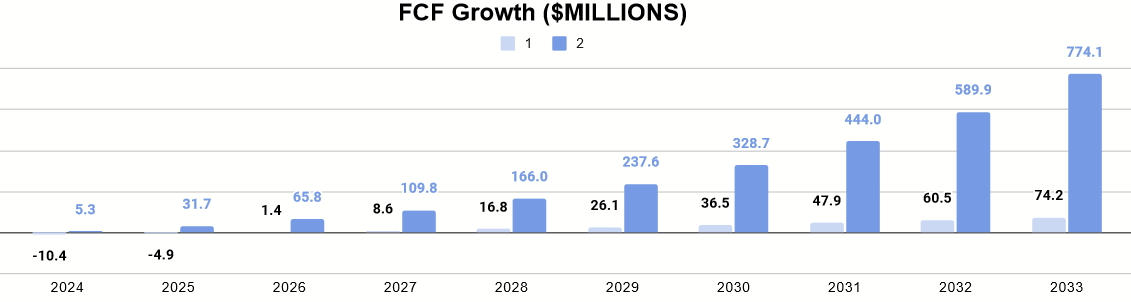

Valuation

I'd normally do a Discounted Cash Flow model or a valuation, but I'm going to keep it simpler this time since positive cash flows do not yet exist.

Author's calculation

Using 2023's financial data, we look at a couple of scenarios, low growth and high growth.

Author's calculation

With a current market cap of $229M, we can see that SPIR might be fairly valued for Scenario 1, depending on your discount rate. In Scenario 2, we see a river of cash by comparison. 2033's FCF estimate would assume about a billion dollars in revenue after a decade, and I believe that's practical with the kind of data solutions they provide and the ability to scale up contracts. As Platzer noted:

In every single segment, we see contracts showing up that are 10 times the size that those contracts used to be. Six figure contracts become seven figure contracts, seven figure contracts become eight figure contracts, and we do see further demand in this kind of regard as well.

It will depend on how much more share dilution occurs, but today's $229M business could easily be a $2B business with those numbers. Whether it works out to a 10x or a 4x with the shares, I'd still be happy with that.

Conclusion

Spire Global is the right business to benefit from generative AI, perhaps one of the best that isn't making semiconductors. By integrating it with satellite data (that few other entities could hope to gather) and providing customers the means to launch their own, Spire is riding a huge wave of demand for better data and better models.

Some risks exist, such as the debt on their balance sheet and the inability to insure any of their orbital assets, but overall the turning into positive cash flow is nigh. While it may not be tomorrow, I think it will take off, and that makes SPIR a nice Buy for the early bird.